You might also like

- Class 3233Document18 pagesClass 3233Lal Malsawma MalzNo ratings yet

- The meaning and factors of foreign exchange ratesDocument5 pagesThe meaning and factors of foreign exchange ratesRohini ManiNo ratings yet

- Presented By: Name of The Student Roll. No SignatureDocument54 pagesPresented By: Name of The Student Roll. No SignatureRohan KhilareNo ratings yet

- Flexible Exchange RateDocument38 pagesFlexible Exchange RategoodwynjNo ratings yet

- A Assignment On:: Submitted To: Submitted byDocument31 pagesA Assignment On:: Submitted To: Submitted byatul1157No ratings yet

- Inside the Foreign Exchange Universe: (An Essential Guide to Forex)From EverandInside the Foreign Exchange Universe: (An Essential Guide to Forex)Rating: 4 out of 5 stars4/5 (1)

- Foreign Exchange Market Research PaperDocument8 pagesForeign Exchange Market Research Paperrfxlaerif100% (1)

- Exchange Rate Determination Puzzle: Long Run Behavior and Short Run DynamicsFrom EverandExchange Rate Determination Puzzle: Long Run Behavior and Short Run DynamicsNo ratings yet

- International Business FinanceDocument17 pagesInternational Business FinanceChirag Jain100% (1)

- Chapter 9-Pricing and FinancingDocument22 pagesChapter 9-Pricing and FinancingcchukeeNo ratings yet

- Chapter 9: Pricing and FinancingDocument26 pagesChapter 9: Pricing and FinancingMukesh ChulyarNo ratings yet

- Ibt Rev PDFDocument4 pagesIbt Rev PDFRose Vanessa BurceNo ratings yet

- Foreign E..Document7 pagesForeign E..Nil SpywareNo ratings yet

- Research Project ReportDocument55 pagesResearch Project ReportharryNo ratings yet

- Big Picture C UlocDocument5 pagesBig Picture C UlocAnvi Rose CuyosNo ratings yet

- Unlicensed-Foreign ExchangeDocument26 pagesUnlicensed-Foreign ExchangeSourav KamilyaNo ratings yet

- Stock Exchange & Portfolio ManagementDocument10 pagesStock Exchange & Portfolio ManagementbhaviinpNo ratings yet

- Project Report On Currency MarketDocument54 pagesProject Report On Currency MarketSurbhi Aery63% (8)

- Introduction to Currency ExchangeDocument54 pagesIntroduction to Currency ExchangeMansi KotakNo ratings yet

- Background of Foreign Exchange MarketDocument9 pagesBackground of Foreign Exchange MarketLiya Jahan100% (2)

- The Foreign Exchange MarketDocument3 pagesThe Foreign Exchange MarketDavina AzaliaNo ratings yet

- FX Market Guide: Trading, Participants & FactorsDocument2 pagesFX Market Guide: Trading, Participants & FactorsErica CalzadaNo ratings yet

- Foreign Exchange MarketDocument24 pagesForeign Exchange MarketGaurav DhallNo ratings yet

- Foreign Exchange: Depreciation of The Dollar. The Exchange Rate Between The Japanese Yen and The U.SDocument6 pagesForeign Exchange: Depreciation of The Dollar. The Exchange Rate Between The Japanese Yen and The U.StekkiangNo ratings yet

- Foreign Exchange Market OverviewDocument26 pagesForeign Exchange Market Overviewjasneet kNo ratings yet

- Exchange Rates Bài 1Document12 pagesExchange Rates Bài 1Giang ChauNo ratings yet

- DVK BOOK Currency FuturesDocument68 pagesDVK BOOK Currency FuturesSaubhagya SuriNo ratings yet

- Currency WarsDocument10 pagesCurrency WarsEscobar AlbertoNo ratings yet

- Foreign Exchange MarketDocument3 pagesForeign Exchange Marketyeram_sidNo ratings yet

- FOREX TITLEDocument29 pagesFOREX TITLEOmarNo ratings yet

- Foreign ExchangeDocument30 pagesForeign ExchangeAmy SorensenNo ratings yet

- INTL BUS: FX MKT, MONETARY SYSTEMSDocument7 pagesINTL BUS: FX MKT, MONETARY SYSTEMSYomi BrainNo ratings yet

- A Report On Foreign Exchange Risk Management: by Kavita P. ChokshiDocument34 pagesA Report On Foreign Exchange Risk Management: by Kavita P. Chokshikpc87No ratings yet

- Chapter 9 - Foreign Exchange MarketDocument18 pagesChapter 9 - Foreign Exchange MarketMerge MergeNo ratings yet

- Stock Market and Foreign Exchange Market: An Empirical GuidanceFrom EverandStock Market and Foreign Exchange Market: An Empirical GuidanceNo ratings yet

- Foreign Exchange MarketDocument41 pagesForeign Exchange Marketvishali100% (1)

- Impact of Currency Fluctuations On Indian Stock MarketDocument5 pagesImpact of Currency Fluctuations On Indian Stock MarketShreyas LavekarNo ratings yet

- Analysis On The Relationship Between The Evolution of Stock Prices and Exchange Rates in Emerging Markets - Case of RomaniaDocument17 pagesAnalysis On The Relationship Between The Evolution of Stock Prices and Exchange Rates in Emerging Markets - Case of RomaniaDumitrică PaulNo ratings yet

- Swap Chapter 1Document18 pagesSwap Chapter 1sudhakarhereNo ratings yet

- Introduction To Foreign ExchangeDocument36 pagesIntroduction To Foreign Exchangedhruv_jagtap100% (1)

- Definition of Foreign Exchange MarketDocument2 pagesDefinition of Foreign Exchange MarketSagar MehtaNo ratings yet

- Foreign Exchange MarketDocument3 pagesForeign Exchange MarketJayesh BhandarkarNo ratings yet

- FM Asg# 2 - 2010Document16 pagesFM Asg# 2 - 2010zakavisionNo ratings yet

- ForexDocument59 pagesForexMehul MalaviyaNo ratings yet

- Project ForexDocument63 pagesProject ForexRitesh koliNo ratings yet

- Exam Assigment of IFMDocument9 pagesExam Assigment of IFMPunita KumariNo ratings yet

- Internal FinanceDocument7 pagesInternal Financeakhlaqur rahmanNo ratings yet

- Exchange Rate Bài 3Document15 pagesExchange Rate Bài 3Giang ChauNo ratings yet

- IBF NotesDocument35 pagesIBF NotesAsad Shah100% (1)

- FX Market ReflectionDocument1 pageFX Market ReflectionHella Mae RambunayNo ratings yet

- Final Assignment Forex MarketDocument6 pagesFinal Assignment Forex MarketUrvish Tushar DalalNo ratings yet

- FIN542 Group Assignment 1Document5 pagesFIN542 Group Assignment 1Syukri SalimNo ratings yet

- Fixed vs Floating Exchange Rates: A GuideDocument6 pagesFixed vs Floating Exchange Rates: A GuideThinaThinaNo ratings yet

- Exchange Rate Determination Challenges LimitationsDocument5 pagesExchange Rate Determination Challenges LimitationsSakshi LodhaNo ratings yet

- International Business Assignment: BY: Neetika Jalan 08D1678 Bba "B"Document17 pagesInternational Business Assignment: BY: Neetika Jalan 08D1678 Bba "B"jayesh611No ratings yet

- FM Asg# 2 - 2010Document12 pagesFM Asg# 2 - 2010zakavisionNo ratings yet

- An easy approach to the forex trading: An introductory guide on the Forex Trading and the most effective strategies to work in the currency marketFrom EverandAn easy approach to the forex trading: An introductory guide on the Forex Trading and the most effective strategies to work in the currency marketRating: 5 out of 5 stars5/5 (2)

- Changing Dimensions of Business in IndiaDocument136 pagesChanging Dimensions of Business in Indiarajat_singla100% (1)

- W4 - The Effectiveness of FOREX Interventions in Four Latin American CountriesDocument17 pagesW4 - The Effectiveness of FOREX Interventions in Four Latin American Countriesjonathan melgarejo sanchezNo ratings yet

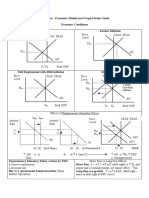

- AP Macroeconomic Models and Graphs Study GuideDocument23 pagesAP Macroeconomic Models and Graphs Study GuideGabriel Jimenez100% (7)

- Tenets of Effective Monetary Policy in The Philippines: Jasmin E. DacioDocument14 pagesTenets of Effective Monetary Policy in The Philippines: Jasmin E. DacioEmeldinand Padilla MotasNo ratings yet

- I. Economic Environment (1) I: The Philippines WT/TPR/S/59Document15 pagesI. Economic Environment (1) I: The Philippines WT/TPR/S/59Roselyn MonsayNo ratings yet

- RBI Credit Policy (Rough)Document15 pagesRBI Credit Policy (Rough)Nidhi NavneetNo ratings yet

- Mause 2019 PoliticalEconomyDocument14 pagesMause 2019 PoliticalEconomySTEPHEN NEIL CASTAÑONo ratings yet

- Investigative Reporting: 2nd Place - Haggai Matsiko and Ian Katusiime, The IndependentDocument5 pagesInvestigative Reporting: 2nd Place - Haggai Matsiko and Ian Katusiime, The IndependentAfrican Centre for Media ExcellenceNo ratings yet

- Mec 004Document11 pagesMec 004Money Mantras100% (1)

- Contempo ModuleDocument123 pagesContempo ModuledennchesNo ratings yet

- Ensayos Sobre Politica Monetaria Inflacionaria y Politica EconomiaDocument127 pagesEnsayos Sobre Politica Monetaria Inflacionaria y Politica EconomiacocoNo ratings yet

- Internship Report 2019 Bop KarorDocument25 pagesInternship Report 2019 Bop KarorArham khanNo ratings yet

- The Dovish MR DudleyDocument8 pagesThe Dovish MR DudleyTaylor CottamNo ratings yet

- Monetary Policy Guide for StudentsDocument15 pagesMonetary Policy Guide for StudentsThamilnila GowthamNo ratings yet

- Monetary Instruments in The Philippines: Focus On Open Market OperationsDocument14 pagesMonetary Instruments in The Philippines: Focus On Open Market OperationsApple CruzNo ratings yet

- Fed Dec ProjectionsDocument17 pagesFed Dec ProjectionsTim MooreNo ratings yet

- RBI HIKES REPO RATE BY 50 BPS TO 5.9Document16 pagesRBI HIKES REPO RATE BY 50 BPS TO 5.9Surath KrishnaNo ratings yet

- Madagascar 2013Document15 pagesMadagascar 2013HayZara MadagascarNo ratings yet

- Money MarketDocument19 pagesMoney Marketramesh.kNo ratings yet

- Macro Final Cheat SheetDocument2 pagesMacro Final Cheat SheetChristine Son100% (1)

- TestsDocument5 pagesTestsDenzel GotoNo ratings yet

- Report On The Work Of The Government: 摘自China Daily,更多英语资料整理请关注微博@夏天英语乐园 Qq群:667495173Document31 pagesReport On The Work Of The Government: 摘自China Daily,更多英语资料整理请关注微博@夏天英语乐园 Qq群:667495173Jian HuangNo ratings yet

- Predictability of Monetary PolDocument84 pagesPredictability of Monetary PolSt MelisaNo ratings yet

- Bilateral Screening: Chapter 17: Presentation of MontenegroDocument13 pagesBilateral Screening: Chapter 17: Presentation of MontenegroAngus DoijNo ratings yet

- Central Bank - WikipediaDocument143 pagesCentral Bank - WikipediaDaxesh BhoiNo ratings yet

- C18 - Slides: Paul KrugmanDocument35 pagesC18 - Slides: Paul Krugmandua.fatma.1892No ratings yet

- Monetary Fiscal Policy MCQsDocument17 pagesMonetary Fiscal Policy MCQsrohanNo ratings yet

- Tabel Marimi UK-EURDocument2 pagesTabel Marimi UK-EURmariela2mNo ratings yet

- Makerere University Business SchoolDocument6 pagesMakerere University Business SchoolCeacer Julio SsekatawaNo ratings yet