You might also like

- Basic Con Trol Sup Erv Iso Ry Cont Ro L Int Erna L Check Int Erna L AuditDocument3 pagesBasic Con Trol Sup Erv Iso Ry Cont Ro L Int Erna L Check Int Erna L AuditKaleem AhmadNo ratings yet

- ESG ChecklistDocument51 pagesESG ChecklistBUDI GINANJARNo ratings yet

- Material ManagementDocument4 pagesMaterial ManagementSimranjeet SinghNo ratings yet

- F&B Controls-BAsic PoliciesDocument7 pagesF&B Controls-BAsic Policiesdafni fernandesNo ratings yet

- Doc3 PDFDocument13 pagesDoc3 PDFibadali2000No ratings yet

- Planta Nivel 1: Horn o DW DW DWDocument1 pagePlanta Nivel 1: Horn o DW DW DWMiguel Angel Gonzalez DiazNo ratings yet

- TAWAL - SUPPLIER PORTAL - DS.030 (v1.0)Document10 pagesTAWAL - SUPPLIER PORTAL - DS.030 (v1.0)nahlaNo ratings yet

- Fluids Lab Buoyant ForceDocument3 pagesFluids Lab Buoyant ForceSandeep BadigantiNo ratings yet

- Ejercicio Delineacion CuencaDocument1 pageEjercicio Delineacion CuencaDiego PullesNo ratings yet

- Recognizing Expenses When Incurred Rather Than When PaidDocument2 pagesRecognizing Expenses When Incurred Rather Than When PaidNath BongalonNo ratings yet

- Pancake: Jump To Navigation Jump To SearchDocument5 pagesPancake: Jump To Navigation Jump To SearchJonahNo ratings yet

- Pusat Pendidikan Dan Pelatihan Industri Sekolah Menengah Kejuruan - Smak Bogor Laboratorium Tempat Uji Kompetensi (Tuk) SmakboDocument1 pagePusat Pendidikan Dan Pelatihan Industri Sekolah Menengah Kejuruan - Smak Bogor Laboratorium Tempat Uji Kompetensi (Tuk) SmakboRahmah WulanNo ratings yet

- En AX22u-4Document2 pagesEn AX22u-4YakupovNo ratings yet

- 10 PPMDocument2 pages10 PPMDamar RukmanaNo ratings yet

- TH 50AS670 EnglishDocument24 pagesTH 50AS670 EnglishDavidNo ratings yet

- Timetable For B.Tech III Yr II Sem Mar 2022 ExamsDocument4 pagesTimetable For B.Tech III Yr II Sem Mar 2022 ExamsHari ChennaNo ratings yet

- Spectra Notes Labor Relations 2016 - Topic 1-4Document49 pagesSpectra Notes Labor Relations 2016 - Topic 1-4Charlie MagneNo ratings yet

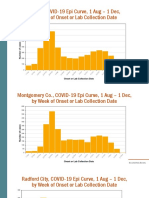

- NRHD, COVID-19 Epi Curve, 1 Aug - 1 Dec, by Week of Onset or Lab Collection DateDocument6 pagesNRHD, COVID-19 Epi Curve, 1 Aug - 1 Dec, by Week of Onset or Lab Collection DatePat ThomasNo ratings yet

- .Co .In/: Ias Prelims Exam 2015Document38 pages.Co .In/: Ias Prelims Exam 2015vgasNo ratings yet

- Img 0003Document3 pagesImg 0003Shayan AbagnaleNo ratings yet

- 2 Oracle Database 12c PLSQL Fundamentals Activity Guide PDFDocument120 pages2 Oracle Database 12c PLSQL Fundamentals Activity Guide PDFTreasureNo ratings yet

- Home - Privacy - Disclaimer - About Us - Report Error - Free Listing - Contact UsDocument3 pagesHome - Privacy - Disclaimer - About Us - Report Error - Free Listing - Contact UsVineet YadavNo ratings yet

- PSAT & Columbus DayDocument3 pagesPSAT & Columbus Dayp998uy9034No ratings yet

- ISPcontract 30012020Document13 pagesISPcontract 30012020Martin MutuaNo ratings yet

- Census Book of KathiharDocument1,020 pagesCensus Book of Kathiharrahul kumarNo ratings yet

- Flying King Air ReprintDocument9 pagesFlying King Air ReprintVinicius AckermannNo ratings yet

- Case Study How Using The Right Raw Materials Can Help You Keep Your Customer Promise - r1Document2 pagesCase Study How Using The Right Raw Materials Can Help You Keep Your Customer Promise - r1Mehedi HasanNo ratings yet

- 徐重QAY800 原理图-17Document1 page徐重QAY800 原理图-17Andre SantosNo ratings yet

- 0BZ Bosa Britalia 10Document1 page0BZ Bosa Britalia 10genesisbarrockNo ratings yet

- Chlorine Files Weekly Water Slide ScheduleDocument1 pageChlorine Files Weekly Water Slide Schedulekirsten_hallNo ratings yet

- South American Rivers: Ci Fi CDocument70 pagesSouth American Rivers: Ci Fi CestarianNo ratings yet

- Paper CuttingDocument1 pagePaper CuttingYogesh SonawaneNo ratings yet

- The Holy Bible, Containing The Old and New Tes-Taments: ... 1775Document3 pagesThe Holy Bible, Containing The Old and New Tes-Taments: ... 1775otumfoba77No ratings yet

- Republic of The Philippines Manila First Division: Supreme CourtDocument4 pagesRepublic of The Philippines Manila First Division: Supreme CourtJames Estrada CastroNo ratings yet

- JKT3 New Construction Project: Submittal FormDocument2 pagesJKT3 New Construction Project: Submittal FormMulya SitanggangNo ratings yet

- Jeni Garisan PDFDocument1 pageJeni Garisan PDFRAJA AZIZU BIN RAJA YUNUS MoeNo ratings yet

- Plaza 125 Greenwich - Amenity S&R Sheet 2 As of 05-16-23Document1 pagePlaza 125 Greenwich - Amenity S&R Sheet 2 As of 05-16-23sanketNo ratings yet

- Sci-Hub - Making Uncommon Knowledge CommonDocument1 pageSci-Hub - Making Uncommon Knowledge CommonhatemaaNo ratings yet

- WWW Acte in AWS Training in HyderabadDocument18 pagesWWW Acte in AWS Training in Hyderabadsophiamerlin1996No ratings yet

- Eaw CatalogDocument20 pagesEaw CatalogalwiNo ratings yet

- BJT Small Signal Configurations Cheat SheetDocument1 pageBJT Small Signal Configurations Cheat SheetAdi SaggarNo ratings yet

- D80190GC20 AgDocument144 pagesD80190GC20 AgRevankar B R ShetNo ratings yet

- Seniority List of Provincial Public Management Assistant Service - Supra GradeDocument2 pagesSeniority List of Provincial Public Management Assistant Service - Supra Gradenpgovlk100% (2)

- Juan Tuno James Pond StatmentDocument1 pageJuan Tuno James Pond Statmentkirsten_hallNo ratings yet

- LZDZ Issue 3 2017 PDFDocument32 pagesLZDZ Issue 3 2017 PDFLEDOMNo ratings yet

- Fauquier Open Space 2-2017Document1 pageFauquier Open Space 2-2017Fauquier Now100% (1)

- Kromatogram HPLC (SMPL)Document2 pagesKromatogram HPLC (SMPL)Sabina ShafaNo ratings yet

- Vocabulary ActivitiesDocument15 pagesVocabulary ActivitiesESTHER AVELLANo ratings yet

- App Drafttrans NPDocument4 pagesApp Drafttrans NPCONDOR C8No ratings yet

- Raiser Candidate PathDocument4 pagesRaiser Candidate PathHasmik GhazaryanNo ratings yet

- Module 1 Revision - ChemistryDocument10 pagesModule 1 Revision - ChemistryIdris MohammedNo ratings yet

- RT 31Document27 pagesRT 31Cali JaveNo ratings yet

- Zacharie AMELI TCHOUALA (frzack@yahooฺcom) has a non-transferable license to use this Student GuideฺDocument324 pagesZacharie AMELI TCHOUALA (frzack@yahooฺcom) has a non-transferable license to use this Student GuideฺNainika KedarisettiNo ratings yet

- LR BLT DD Salur 9 CengkalsewuDocument3 pagesLR BLT DD Salur 9 CengkalsewutopangantengNo ratings yet

- WASA Drainage A3 NewDocument1 pageWASA Drainage A3 Newzeeshn chauhdryNo ratings yet

- 2 Waq FedDocument17 pages2 Waq FedVulebg VukoicNo ratings yet

- PDF Pioneer British Level B1plus Tests CompressDocument64 pagesPDF Pioneer British Level B1plus Tests Compresstramites y fianzas 18No ratings yet

- Bv-Dao TienDocument1 pageBv-Dao TienTùng PhạmNo ratings yet

- Handbook AiAX Coatings EngDocument20 pagesHandbook AiAX Coatings EngfinhasNo ratings yet

- Working Capital BrighamDocument9 pagesWorking Capital BrighamOkasha AliNo ratings yet

- Risk, Return & Opportunity Cost of CapitalDocument19 pagesRisk, Return & Opportunity Cost of CapitalOkasha AliNo ratings yet

- Optimal Capital StructureDocument29 pagesOptimal Capital StructureOkasha AliNo ratings yet

- Shell AnalysisDocument21 pagesShell AnalysisOkasha AliNo ratings yet

- ContentDocument1 pageContentOkasha AliNo ratings yet

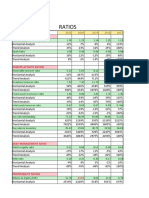

- Liquidity RatiosDocument10 pagesLiquidity RatiosOkasha AliNo ratings yet

- FRM Final ProjectDocument5 pagesFRM Final ProjectOkasha AliNo ratings yet

- ICMO 2024 Form ConstructionDocument2 pagesICMO 2024 Form Constructionjonathankarta.hdkNo ratings yet

- Pengaruh Threat Emotions, Kepercayaan Merek Dan Harga Terhadap Keputusan Pembelian Produk Susu Anlene ActifitDocument10 pagesPengaruh Threat Emotions, Kepercayaan Merek Dan Harga Terhadap Keputusan Pembelian Produk Susu Anlene ActifitDiwan HYNo ratings yet

- Definition of WagesDocument8 pagesDefinition of WagesCorolla SedanNo ratings yet

- Ruka CompleteDocument121 pagesRuka CompletePhelix O DaniyanNo ratings yet

- 2223-Article Text-10843-1-10-20230721Document17 pages2223-Article Text-10843-1-10-20230721aptvirtualkpknlmksNo ratings yet

- Ma Security Company Profile 2Document6 pagesMa Security Company Profile 2api-233290339No ratings yet

- Annual Report 2014Document249 pagesAnnual Report 2014BETTY ELIZABETH JUI�A QUILACHAMINNo ratings yet

- HR Demand and SupplyDocument29 pagesHR Demand and SupplyYasser AbdallaNo ratings yet

- A) Maximum and Minimum PricesDocument4 pagesA) Maximum and Minimum PricesNicole MpehlaNo ratings yet

- E - General Terms and Conditions For Cloud ServicesDocument10 pagesE - General Terms and Conditions For Cloud ServicesUlysse TpnNo ratings yet

- Marketing Function and How It Interacts With Other Function. NGHI - (09!06!2021)Document7 pagesMarketing Function and How It Interacts With Other Function. NGHI - (09!06!2021)Lê NghiNo ratings yet

- TSmunt BM 711 Ch2 HandoutDocument3 pagesTSmunt BM 711 Ch2 HandoutShelbyNo ratings yet

- PP Presentation Q 15 ADocument8 pagesPP Presentation Q 15 ARita LakhsmiNo ratings yet

- HR PRACTICES Marriott - 23027 - RMDocument13 pagesHR PRACTICES Marriott - 23027 - RMMahak Sharma100% (1)

- Isilon Product FamilyDocument7 pagesIsilon Product FamilyrejnanNo ratings yet

- Lokesh Punj Cvdec2018Document11 pagesLokesh Punj Cvdec2018LOKESH PUNJNo ratings yet

- Engineering EconomicspreboardDocument2 pagesEngineering EconomicspreboardNUCUP Marco V.No ratings yet

- EFFECT OF SUSTAINABLE PROCUREMENT PRACTICES ON OPERATIONAL PERFORMANCE - CASE STUDY GHANA GRID COMPANY LIMITED (GRIDCo)Document69 pagesEFFECT OF SUSTAINABLE PROCUREMENT PRACTICES ON OPERATIONAL PERFORMANCE - CASE STUDY GHANA GRID COMPANY LIMITED (GRIDCo)Korkor Nartey100% (1)

- PM REFX IntegrationDocument3 pagesPM REFX IntegrationVuppala VenkataramanaNo ratings yet

- MDP Cust Exp Session 3Document10 pagesMDP Cust Exp Session 3Leo Bogosi MotlogelwNo ratings yet

- Chapter 1-Introduction To Accounting and Business: True/FalseDocument3 pagesChapter 1-Introduction To Accounting and Business: True/FalseChloe Gabriel Evangeline ChaseNo ratings yet

- 19llb082 - Banking Law Project - 6th SemDocument25 pages19llb082 - Banking Law Project - 6th Semashirbad sahooNo ratings yet

- Checklist - FF (New) (Blad) - NvoccDocument1 pageChecklist - FF (New) (Blad) - NvoccUnicargo Int'l ForwardingNo ratings yet

- ITC Financial Result Q4 FY2023 SfsDocument6 pagesITC Financial Result Q4 FY2023 Sfsaanchal prasadNo ratings yet

- The Governance ContinuumDocument3 pagesThe Governance Continuumnathan_lawler4416No ratings yet

- Practice of ArchitectureDocument13 pagesPractice of ArchitectureLaurence Caraang CabatanNo ratings yet

- Selecta Fortified MilkDocument40 pagesSelecta Fortified MilkRochelle TyNo ratings yet

- PACEDocument5 pagesPACEJoanne DawangNo ratings yet

- Manual For Discounting Oil and Gas IncomeDocument9 pagesManual For Discounting Oil and Gas IncomeCarlota BellésNo ratings yet

- India 2023 Agrifood Investment ReportDocument34 pagesIndia 2023 Agrifood Investment ReportANKUSH SINHANo ratings yet