You might also like

- Topic 5-Time Value of Money ApplicationDocument38 pagesTopic 5-Time Value of Money ApplicationPhuong VuongNo ratings yet

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- Time Value of Money Ch6 - HandoutsDocument32 pagesTime Value of Money Ch6 - HandoutsMd. Atiqul Hoque NiloyNo ratings yet

- 1.3 Time Value of MoneyDocument27 pages1.3 Time Value of Moneyafiman1725No ratings yet

- Time Value Ch6Document37 pagesTime Value Ch6anower.hosen61No ratings yet

- TVM CALCULATIONS AND CONCEPTSDocument8 pagesTVM CALCULATIONS AND CONCEPTSHassleBustNo ratings yet

- Lecture 2 Time Value of MoneyDocument52 pagesLecture 2 Time Value of MoneyMuhammad YahyaNo ratings yet

- Chapter 2 Time Value of MoneyDocument50 pagesChapter 2 Time Value of MoneyAMER KHALIQUENo ratings yet

- The Mechanics of Valuation (Time Value Money)Document5 pagesThe Mechanics of Valuation (Time Value Money)AnaadilNo ratings yet

- Time Value of Money: Future Value Present Value Annuities Rates of Return AmortizationDocument19 pagesTime Value of Money: Future Value Present Value Annuities Rates of Return AmortizationkarmabitesNo ratings yet

- Time Value of Money ExplainedDocument37 pagesTime Value of Money Explainedansary75No ratings yet

- FinanceDocument95 pagesFinancereda gadNo ratings yet

- Lec 04 Time Value of MoneyDocument24 pagesLec 04 Time Value of MoneyOptimistic EyeNo ratings yet

- Economic Evaluation of Investment Proposals: NPV, IRR, Annuity CalculationsDocument44 pagesEconomic Evaluation of Investment Proposals: NPV, IRR, Annuity CalculationsCarbon_AdilNo ratings yet

- Time Value of Money Concepts ExplainedDocument15 pagesTime Value of Money Concepts Explainedfaizy24No ratings yet

- FM Unit 4 Lecture Notes - Time Value of MoneyDocument4 pagesFM Unit 4 Lecture Notes - Time Value of MoneyDebbie DebzNo ratings yet

- Introduction To Business Finance (Fin201) : Time Value of MoneyDocument55 pagesIntroduction To Business Finance (Fin201) : Time Value of MoneyAhsan KamranNo ratings yet

- Time Value of Money: - Future Value - Present Value - Annuities - Rate of Return - AmortizationDocument132 pagesTime Value of Money: - Future Value - Present Value - Annuities - Rate of Return - AmortizationMohamed HosnyNo ratings yet

- Basic Practical Examples: Simple Interest Compound Interest. PrincipalDocument10 pagesBasic Practical Examples: Simple Interest Compound Interest. PrincipalArvie Angeles AlferezNo ratings yet

- Time Value of Money ExplainedDocument34 pagesTime Value of Money ExplainedMd. Rezwan Hossain Sakib 1711977630No ratings yet

- Time Value of Money: Future Value Present ValueDocument58 pagesTime Value of Money: Future Value Present ValueeyraNo ratings yet

- Finance: Dr. Suhaib AnagrehDocument113 pagesFinance: Dr. Suhaib AnagrehRabeea AsifNo ratings yet

- FM Ch3 Time Value of MoneyDocument30 pagesFM Ch3 Time Value of Moneytemesgen yohannesNo ratings yet

- Time Value of Money: Future Value Present Value Annuities Rates of Return AmortizationDocument55 pagesTime Value of Money: Future Value Present Value Annuities Rates of Return Amortizationfaheem qureshiNo ratings yet

- Time Value of Money: Future Value Present Value Annuities Rates of Return AmortizationDocument55 pagesTime Value of Money: Future Value Present Value Annuities Rates of Return Amortizationwaqas farooqNo ratings yet

- Topik 5 - Time Value of MoneyDocument35 pagesTopik 5 - Time Value of MoneyHaryadi WidodoNo ratings yet

- Time Value of MoneyDocument52 pagesTime Value of MoneyANKIT AGARWALNo ratings yet

- 05 Lecture - The Time Value of Money PDFDocument26 pages05 Lecture - The Time Value of Money PDFjgutierrez_castro7724No ratings yet

- The Time Value of MoneyDocument75 pagesThe Time Value of MoneySanchit AroraNo ratings yet

- Chapter 5 NoteDocument62 pagesChapter 5 NoteFatimah HamadNo ratings yet

- TVM Chapter 5 Key ConceptsDocument60 pagesTVM Chapter 5 Key Conceptslinda zyongweNo ratings yet

- Chapter 5: How To Value Bonds and StocksDocument16 pagesChapter 5: How To Value Bonds and StocksmajorkonigNo ratings yet

- Lecture 3rd Time Value of MoneyDocument26 pagesLecture 3rd Time Value of MoneyBahrawar saidNo ratings yet

- Time Value of Money: Future Value Present Value Annuities Rates of Return AmortizationDocument56 pagesTime Value of Money: Future Value Present Value Annuities Rates of Return Amortizationsii raiiNo ratings yet

- Unit 2 TVMDocument24 pagesUnit 2 TVMZaheer Ahmed Swati100% (1)

- CH 4 - The Meaning of Interest RatesDocument46 pagesCH 4 - The Meaning of Interest RatesAysha KamalNo ratings yet

- TOPIC 4 - Time Value of Money ConceptDocument28 pagesTOPIC 4 - Time Value of Money ConceptKhánh AnNo ratings yet

- L1 R1 HY NotesDocument4 pagesL1 R1 HY NotesboscoNo ratings yet

- Time Value of Money FundamentalsDocument61 pagesTime Value of Money FundamentalsLimNo ratings yet

- Session 20-22Document39 pagesSession 20-22Muhammad Ubaid UllahNo ratings yet

- FM - Lecture 2 - Time Value of Money PDFDocument82 pagesFM - Lecture 2 - Time Value of Money PDFMi ThưNo ratings yet

- Ch#5 Time Value of MoneyDocument43 pagesCh#5 Time Value of MoneyRafeh AkramNo ratings yet

- Time Value of Money Concepts ExplainedDocument22 pagesTime Value of Money Concepts ExplainedmedrekNo ratings yet

- Time Value of Money Notes Loan ArmotisationDocument12 pagesTime Value of Money Notes Loan ArmotisationVimbai ChituraNo ratings yet

- Time Value of Money ConceptsDocument44 pagesTime Value of Money ConceptsAniket Roy AnikNo ratings yet

- Time Value of Money: The Language of Finance The Most Important LessonDocument36 pagesTime Value of Money: The Language of Finance The Most Important LessonRahmatullah MardanviNo ratings yet

- Time Value of Money Concepts ExplainedDocument9 pagesTime Value of Money Concepts ExplainedBenita BijuNo ratings yet

- 02 How To Calculate Present ValuesDocument5 pages02 How To Calculate Present ValuesMộng Nghi TôNo ratings yet

- Chapter 2 - How To Calculate Present ValuesDocument36 pagesChapter 2 - How To Calculate Present ValuesDeok NguyenNo ratings yet

- Time Value of Money: Future Value Present Value Annuities Rates of Return AmortizationDocument43 pagesTime Value of Money: Future Value Present Value Annuities Rates of Return AmortizationAsif Islam SamannoyNo ratings yet

- Chapter 15 Investment, Time, and Capital Markets: Teaching NotesDocument65 pagesChapter 15 Investment, Time, and Capital Markets: Teaching NotesMohit ChetwaniNo ratings yet

- MBA - RELOSA - DANILO - C - Time Value of MoneyDocument39 pagesMBA - RELOSA - DANILO - C - Time Value of MoneyDan RelosaNo ratings yet

- TVM Lecture 3Document42 pagesTVM Lecture 380tekNo ratings yet

- Time Value of MoneyDocument25 pagesTime Value of MoneyAbhinav RajvermaNo ratings yet

- Chapter 6 Time Value of MoneyDocument39 pagesChapter 6 Time Value of Moneyjhogonnath.saha.65No ratings yet

- Time Value of MoneyDocument18 pagesTime Value of MoneyLatasha AdhiakriNo ratings yet

- FinQuiz - Curriculum Note, Study Session 2-3, Reading 5-12 - QuantDocument85 pagesFinQuiz - Curriculum Note, Study Session 2-3, Reading 5-12 - QuantNattKoon100% (1)

- Finquiz - Curriculum Note Study Session 2 Reading 5Document7 pagesFinquiz - Curriculum Note Study Session 2 Reading 5api-289145400No ratings yet

- 302time Value of MoneyDocument69 pages302time Value of MoneypujaadiNo ratings yet

- Ask Chuck - ITM Case StudyDocument3 pagesAsk Chuck - ITM Case StudyKhánh AnNo ratings yet

- TOPIC 4 - Time Value of Money ConceptDocument28 pagesTOPIC 4 - Time Value of Money ConceptKhánh AnNo ratings yet

- 2023 - Tutorial 1 - FMADocument1 page2023 - Tutorial 1 - FMAKhánh AnNo ratings yet

- TOPIC 1 - Overview of Financial ManagementDocument32 pagesTOPIC 1 - Overview of Financial ManagementKhánh AnNo ratings yet

- Unit 2 Vitamins - Essence of HealthDocument7 pagesUnit 2 Vitamins - Essence of HealthKhánh AnNo ratings yet

- Lesson 19Document45 pagesLesson 19nabila qayyumNo ratings yet

- Green Field TownshipsDocument8 pagesGreen Field Townshipssharad yadavNo ratings yet

- Luckscout Ultimate Wealth System: The Ultimate Guide Toward Wealth and Financial FreedomDocument36 pagesLuckscout Ultimate Wealth System: The Ultimate Guide Toward Wealth and Financial FreedomSamuel AnemeNo ratings yet

- Technical Analysis For Beginners (The Ultimate Guide) - New Trader UDocument1 pageTechnical Analysis For Beginners (The Ultimate Guide) - New Trader UPuneet RajNo ratings yet

- Capital Budgeting Techniques ExplainedDocument35 pagesCapital Budgeting Techniques ExplainedGaurav gusaiNo ratings yet

- Afar 10Document8 pagesAfar 10RENZEL MAGBITANGNo ratings yet

- VAC - Financial LiteracyDocument17 pagesVAC - Financial Literacypatelrajat454454No ratings yet

- BASEL Norms MCQDocument15 pagesBASEL Norms MCQBiswajit Das100% (1)

- Multi 0 PageDocument266 pagesMulti 0 PageNatali GolubNo ratings yet

- Insurance Question BankDocument58 pagesInsurance Question BankGaneshNo ratings yet

- 02 Time Value of Money - GRCDocument11 pages02 Time Value of Money - GRCGabrielle VizcarraNo ratings yet

- Baskin, J., 1989, An Empirical Investigation of The Pecking Order Hypothesis, Financial Management, Spring, 26-35Document11 pagesBaskin, J., 1989, An Empirical Investigation of The Pecking Order Hypothesis, Financial Management, Spring, 26-35Eva DivaNo ratings yet

- United States District Court Southern District of New YorkDocument85 pagesUnited States District Court Southern District of New YorkfleckaleckaNo ratings yet

- ISJ033Document66 pagesISJ0332imediaNo ratings yet

- Awkum SlipDocument1 pageAwkum SlipAbdul Aziz0% (1)

- Jiwaji University, Gwalior: Master of Commerce INDocument36 pagesJiwaji University, Gwalior: Master of Commerce INPratiksha SaxenaNo ratings yet

- Balance Transfer From Last Month Salary Amount in Hand OthersDocument3 pagesBalance Transfer From Last Month Salary Amount in Hand OthersJithin RoyNo ratings yet

- ITAT Hearing on Transfer Pricing AdjustmentDocument29 pagesITAT Hearing on Transfer Pricing Adjustmentbharath289No ratings yet

- Perspectives Paper Challenges To Market ValueDocument10 pagesPerspectives Paper Challenges To Market ValueRuben Gonzalez CortesNo ratings yet

- Capital BudgetingDocument22 pagesCapital BudgetingBradNo ratings yet

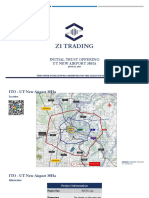

- ITO - UT New Airport 38Ha Land InvestmentDocument10 pagesITO - UT New Airport 38Ha Land InvestmentPaul KitNo ratings yet

- Q: What Do You Think Is Wrong With The First Question I Asked in The Application Questions? How Does This Impact Your Answer, If at All?Document1 pageQ: What Do You Think Is Wrong With The First Question I Asked in The Application Questions? How Does This Impact Your Answer, If at All?PratikNo ratings yet

- Chapter 7: Intercompany Profit Transactions - Bonds: Advanced AccountingDocument14 pagesChapter 7: Intercompany Profit Transactions - Bonds: Advanced AccountingDivya rezkyNo ratings yet

- Financial Asset at Fair Value Problem 21-1 (IFRS) : Solution 21-1 Answer CDocument15 pagesFinancial Asset at Fair Value Problem 21-1 (IFRS) : Solution 21-1 Answer CEngel QuimsonNo ratings yet

- Asset and Liability ManagementDocument8 pagesAsset and Liability ManagementPriyanka YadavNo ratings yet

- Impact of Venture Capital On Indian EconomyDocument5 pagesImpact of Venture Capital On Indian EconomylenovoNo ratings yet

- Financial Statements and RatiosDocument27 pagesFinancial Statements and RatiosIoana MariucaNo ratings yet

- SEBI's Informal Guidance On Investment Conditions For AIFs - Vinod Kothari ConsultantsDocument4 pagesSEBI's Informal Guidance On Investment Conditions For AIFs - Vinod Kothari ConsultantsRajesh AroraNo ratings yet

- Real Estate Portfolio Valuation Model v3.4Document11 pagesReal Estate Portfolio Valuation Model v3.4daniellehynes69No ratings yet

- JP Morgan BacheletDocument4 pagesJP Morgan BacheletDiario ElMostrador.clNo ratings yet