You might also like

- E Newsletter September 2013Document13 pagesE Newsletter September 2013sd naikNo ratings yet

- Landmark Cases 439Document17 pagesLandmark Cases 439Anand Kumar KediaNo ratings yet

- Brains Trust PPT - MR Gautam DoshiDocument31 pagesBrains Trust PPT - MR Gautam DoshiIshanNo ratings yet

- Summary of Case Laws of Direct TaxDocument14 pagesSummary of Case Laws of Direct TaxAvaniJainNo ratings yet

- Session Paper - 6 (Questions & Answers), For Overall Discussion On Principles of Taxation of CLDocument3 pagesSession Paper - 6 (Questions & Answers), For Overall Discussion On Principles of Taxation of CLProgga MehnazNo ratings yet

- Dividend Under Companies Act 2013Document12 pagesDividend Under Companies Act 2013Abhinay KumarNo ratings yet

- ITAT Ruling Excludes Oman Investment from Section 14A DisallowanceDocument43 pagesITAT Ruling Excludes Oman Investment from Section 14A DisallowanceTrisha MajumdarNo ratings yet

- Income Tax Appellate Tribunal - Mumbai: Suresh Industries P.LTD, Mumbai Vs Assessee On 13 September, 2012Document5 pagesIncome Tax Appellate Tribunal - Mumbai: Suresh Industries P.LTD, Mumbai Vs Assessee On 13 September, 2012Puneet kumarNo ratings yet

- Factoring Charges Not Interest for TDSDocument3 pagesFactoring Charges Not Interest for TDSSaksham ShrivastavNo ratings yet

- ELP Indirect Tax Newsletter November 2022Document6 pagesELP Indirect Tax Newsletter November 2022ELP LawNo ratings yet

- Deemed Dividend-A Detailed Analysis of Section 2 (22) (E) and Its Legal ImplicationsDocument6 pagesDeemed Dividend-A Detailed Analysis of Section 2 (22) (E) and Its Legal ImplicationsSindhuja BhaskaraNo ratings yet

- Refund Forms For Centre and StateDocument20 pagesRefund Forms For Centre and StateShail MehtaNo ratings yet

- Form B VXL Realtors Pvt. Ltd.Document8 pagesForm B VXL Realtors Pvt. Ltd.Vikram Singh BaidNo ratings yet

- Issues in Tax Audit ReportDocument70 pagesIssues in Tax Audit ReportPankaj ShahNo ratings yet

- COMPANY LAW AND TAX LIABILITYDocument7 pagesCOMPANY LAW AND TAX LIABILITYavinashNo ratings yet

- TS 333 ITAT 2013DEL TS 333 ITAT 2013DEL SPX India PVT LTDDocument5 pagesTS 333 ITAT 2013DEL TS 333 ITAT 2013DEL SPX India PVT LTDbharath289No ratings yet

- DT CASE STUDY SERIES FOR FINAL STUDENTs - SET 5Document10 pagesDT CASE STUDY SERIES FOR FINAL STUDENTs - SET 5tusharjaipur7No ratings yet

- Consolidated Digest of Case Laws Jan 2013 March 2013Document179 pagesConsolidated Digest of Case Laws Jan 2013 March 2013Ankit DamaniNo ratings yet

- Cir 174 06 2022 CGSTDocument5 pagesCir 174 06 2022 CGSTNM JHANWAR & ASSOCIATESNo ratings yet

- PDF - 28-09-23 07-02-29Document18 pagesPDF - 28-09-23 07-02-29jalodarahardik786No ratings yet

- Tax Deductions Allowed for Bad Debts and Plant Shifting ChargesDocument9 pagesTax Deductions Allowed for Bad Debts and Plant Shifting ChargesByomkesh PandaNo ratings yet

- DT New Case LawDocument32 pagesDT New Case LawJohn WilliamNo ratings yet

- Weekly Updates 16th Apr 2023 To 22nd Apr 2023Document7 pagesWeekly Updates 16th Apr 2023 To 22nd Apr 2023Swathi JainNo ratings yet

- CIT v. MKJ Enterprises Ltd.-Cal HCDocument2 pagesCIT v. MKJ Enterprises Ltd.-Cal HCSaksham ShrivastavNo ratings yet

- CA Final Case Laws SummaryDocument7 pagesCA Final Case Laws SummaryAnamika Chauhan VermaNo ratings yet

- Delhi ITAT (Bar) Reports - December 2020Document23 pagesDelhi ITAT (Bar) Reports - December 2020PARVATI KUMARINo ratings yet

- Income Taxation DigestDocument17 pagesIncome Taxation DigestSitty MangNo ratings yet

- Direct Tax-Chit FundDocument27 pagesDirect Tax-Chit FundAbirami VasudevanNo ratings yet

- Rahul Patil Audit Misrepresentations SuppressionsDocument4 pagesRahul Patil Audit Misrepresentations SuppressionsA PanickarNo ratings yet

- Income Tax Tribunal Order on NSEL Trading LossesDocument63 pagesIncome Tax Tribunal Order on NSEL Trading LossesCA Prakash Chandra BhandariNo ratings yet

- Page 1 of 4Document4 pagesPage 1 of 4Sunil ShahNo ratings yet

- 31400sm DTL Finalnew Vol3 May Nov14 Cp1Document6 pages31400sm DTL Finalnew Vol3 May Nov14 Cp1sunitadklNo ratings yet

- Direct Tax Notes SummaryDocument224 pagesDirect Tax Notes SummaryPreeti Ray100% (1)

- Bar On Direct Demand Against Deductee - Jus in Re Bar On Direct Demand Against Deductee - Jus in ReDocument3 pagesBar On Direct Demand Against Deductee - Jus in Re Bar On Direct Demand Against Deductee - Jus in Reabc defNo ratings yet

- Direct Tax Case LawDocument17 pagesDirect Tax Case Lawsathish_61288@yahooNo ratings yet

- 1652426740-447 & 8168 HCL Comnet Systems & Services LTDDocument7 pages1652426740-447 & 8168 HCL Comnet Systems & Services LTDArulnidhi Ramanathan SeshanNo ratings yet

- Tax Audit ReportDocument28 pagesTax Audit Reportsmith sethisNo ratings yet

- Circular CGST 131 NewDocument5 pagesCircular CGST 131 NewSanjeev BorgohainNo ratings yet

- Aino Communique Mar 23 113th EditionDocument13 pagesAino Communique Mar 23 113th EditionSwathi JainNo ratings yet

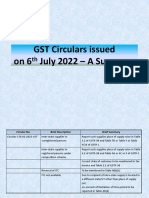

- GST Circulars Issued On 6th July - A SummaryDocument8 pagesGST Circulars Issued On 6th July - A SummaryVijaya ChandNo ratings yet

- NoteDocument3 pagesNoteNeelesh KhandelwalNo ratings yet

- Monthly Digest Dec 2013Document134 pagesMonthly Digest Dec 2013innvolNo ratings yet

- Of of of The For TheirDocument7 pagesOf of of The For TheirKatherine MakalintalNo ratings yet

- 484b6 Impact Wrong Type of Tax Paid and Wrong Claim of ItcDocument5 pages484b6 Impact Wrong Type of Tax Paid and Wrong Claim of Itc15211 alok AnandNo ratings yet

- FN File RequisitionDocument20 pagesFN File RequisitionMayur JadejaNo ratings yet

- आयकर अपीलीय अिधकरण " यायपीठ पुणे म । (Through Virtual Court)Document8 pagesआयकर अपीलीय अिधकरण " यायपीठ पुणे म । (Through Virtual Court)Saksham ShrivastavNo ratings yet

- TDS Year of Receipt 26asDocument8 pagesTDS Year of Receipt 26asDr G D PadmahshaliNo ratings yet

- Red 228358Document2 pagesRed 228358Prabhati AssestNo ratings yet

- Ito New Delhi Vs M S Paragon XT New Delhi On 14 March 2019Document29 pagesIto New Delhi Vs M S Paragon XT New Delhi On 14 March 2019ashish poddarNo ratings yet

- High Court Digest PDFDocument410 pagesHigh Court Digest PDFAnukul DasNo ratings yet

- Abb FZ LLC - Bangalore ItatDocument23 pagesAbb FZ LLC - Bangalore Itatbharath289No ratings yet

- 6.case Study On Input Tax Credit Under GSTDocument17 pages6.case Study On Input Tax Credit Under GSTSUNIL PUJARINo ratings yet

- Swram HRDocument15 pagesSwram HRRAJORAJI CO.No ratings yet

- Tax Deducted at Source ExplainedDocument31 pagesTax Deducted at Source ExplainedShaleenPatniNo ratings yet

- Letter Template-1Document21 pagesLetter Template-1QwertyNo ratings yet

- Ca Final Advanced ManagementDocument114 pagesCa Final Advanced ManagementMohammed IrfanNo ratings yet

- Address: of The of The Employee 2021-2022Document3 pagesAddress: of The of The Employee 2021-2022Dipak PArmarNo ratings yet

- Ca Final New Case Laws Notification CircularsDocument9 pagesCa Final New Case Laws Notification Circularsbedidanish900No ratings yet

- Dell International Services India PVT LTD Vs The IIL2022040522170528204COM311728Document30 pagesDell International Services India PVT LTD Vs The IIL2022040522170528204COM311728Rıtesha DasNo ratings yet

- Pan Card Application Form Updated 2017 With Aadhaar DetailsDocument2 pagesPan Card Application Form Updated 2017 With Aadhaar DetailsManasib AshrafNo ratings yet

- Enrollment FormDocument1 pageEnrollment Formsd naikNo ratings yet

- Activity Code13 PagesDocument13 pagesActivity Code13 Pagessd naikNo ratings yet

- GOODS SOLD ON MRP BASIS IS EXEMPTED FROM SERVICE TAX Circular No.173 - 8 - 2013 - ST, Dated 07-10-2013Document1 pageGOODS SOLD ON MRP BASIS IS EXEMPTED FROM SERVICE TAX Circular No.173 - 8 - 2013 - ST, Dated 07-10-2013phani raja kumarNo ratings yet

- TeplateDocument8 pagesTeplatejigyasha oarmarNo ratings yet

- Electronic Payment SystemDocument14 pagesElectronic Payment SystemToppers of WorldsNo ratings yet

- First InvestmentsDocument4 pagesFirst InvestmentsNitin Kumar0% (1)

- Fee Receipt: Student InformationDocument1 pageFee Receipt: Student InformationAVNEESH SINGHANIA100% (1)

- Advantages and Disadvantages of GSTDocument5 pagesAdvantages and Disadvantages of GSTKshitiz TiwariNo ratings yet

- US Internal Revenue Service: I1040a - 2001Document64 pagesUS Internal Revenue Service: I1040a - 2001IRSNo ratings yet

- Indian Income Tax Return Acknowledgement SummaryDocument1 pageIndian Income Tax Return Acknowledgement SummaryGanesh DasaraNo ratings yet

- 4 Income Tax Tables Final PDFDocument8 pages4 Income Tax Tables Final PDFwilliam091090No ratings yet

- University of Petroleum & Energy StudiesDocument1 pageUniversity of Petroleum & Energy Studiespintu ramNo ratings yet

- Savant FrameworkDocument41 pagesSavant FrameworkফেরদৌসআলমNo ratings yet

- Solina - 2ndyr - 1sttermDocument1 pageSolina - 2ndyr - 1sttermEduard Keandrei Yap SolinaNo ratings yet

- View Invoice - AppleDocument1 pageView Invoice - AppleCamelia BarbuNo ratings yet

- Appendix 24 - QUARTERLY REPORT OF REVENUE AND OTHER RECEIPTSDocument1 pageAppendix 24 - QUARTERLY REPORT OF REVENUE AND OTHER RECEIPTSPau PerezNo ratings yet

- CUNY Standard Verification WorksheetDocument3 pagesCUNY Standard Verification Worksheethicu0No ratings yet

- CHAPTER 10 ALLOWABLE DEDUCTIONSDocument17 pagesCHAPTER 10 ALLOWABLE DEDUCTIONSKyle BacaniNo ratings yet

- Proforma InvoiceDocument1 pageProforma InvoiceNaveen KumarNo ratings yet

- Taxation of Business Entities 2018 Edition 9th Edition Spilker Solutions ManualDocument31 pagesTaxation of Business Entities 2018 Edition 9th Edition Spilker Solutions Manuallongchadudz100% (26)

- SSC CGL 2023 Maths Chapterwise CompilationDocument207 pagesSSC CGL 2023 Maths Chapterwise CompilationBharatNo ratings yet

- Taxation IiDocument3 pagesTaxation IiRyNo ratings yet

- Ripple CryptocurrencyDocument5 pagesRipple CryptocurrencyRipple Coin NewsNo ratings yet

- Frank Sciame & Richard AndersonDocument3 pagesFrank Sciame & Richard AndersondfreedlanderNo ratings yet

- Accomplishment of ElectricianDocument17 pagesAccomplishment of ElectricianRichard Tañada RosalesNo ratings yet

- Airtel 3G Postpaid Plans ComparisonDocument9 pagesAirtel 3G Postpaid Plans ComparisonSandeep Singh MehraNo ratings yet

- Income and Business TaxDocument43 pagesIncome and Business TaxMathew EstradaNo ratings yet

- Invoice DCLDocument1 pageInvoice DCLYaseenNo ratings yet

- Domain Renewal Invoice for The Skills AcademyDocument1 pageDomain Renewal Invoice for The Skills AcademyPrabal Frank NandwaniNo ratings yet

- ElectricityDocument1 pageElectricityDarge GmentizaNo ratings yet

- RAGA BenefitsDocument1 pageRAGA BenefitsCBS This MorningNo ratings yet

- Discharge Voucher ULIP End V6.1 RevisedDocument3 pagesDischarge Voucher ULIP End V6.1 Revisedsunny0908No ratings yet

- 10 CIR v. Toledo Power CompanyDocument47 pages10 CIR v. Toledo Power Companyada mae santoniaNo ratings yet