You might also like

- Walt Disney Yen FinancingDocument10 pagesWalt Disney Yen FinancingAndy100% (3)

- Account Statement - 2022 09 01 - 2023 01 31 - en GB - A9250cDocument7 pagesAccount Statement - 2022 09 01 - 2023 01 31 - en GB - A9250cRosca ConstantinNo ratings yet

- Summary of Project Assumptions: Construction CostsDocument5 pagesSummary of Project Assumptions: Construction CostsjowacocoNo ratings yet

- E NEWSLETTER May 2013Document9 pagesE NEWSLETTER May 2013sd naikNo ratings yet

- Refund Forms For Centre and StateDocument20 pagesRefund Forms For Centre and StateShail MehtaNo ratings yet

- TDS Year of Receipt 26asDocument8 pagesTDS Year of Receipt 26asDr G D PadmahshaliNo ratings yet

- Show Cause NoticeDocument8 pagesShow Cause NoticeinfoNo ratings yet

- Nation: MarketDocument9 pagesNation: MarketDebashis MitraNo ratings yet

- Shree Karthik Papers Ltdvs Deputy Commissionerof Income TDocument4 pagesShree Karthik Papers Ltdvs Deputy Commissionerof Income TKaran GannaNo ratings yet

- Cir 174 06 2022 CGSTDocument5 pagesCir 174 06 2022 CGSTNM JHANWAR & ASSOCIATESNo ratings yet

- Brains Trust PPT - MR Gautam DoshiDocument31 pagesBrains Trust PPT - MR Gautam DoshiIshanNo ratings yet

- TapanDocument6 pagesTapanDebashis MitraNo ratings yet

- Eturns: This Chapter Will Equip You ToDocument52 pagesEturns: This Chapter Will Equip You ToShowkat MalikNo ratings yet

- GST Returns: BackgroundDocument3 pagesGST Returns: BackgroundPrakash PalanisamyNo ratings yet

- 0bba0 GSTR 9 Booklet HiregangeDocument113 pages0bba0 GSTR 9 Booklet HiregangeAMIT SHARMANo ratings yet

- AssessmentDocument3 pagesAssessmentSWETCHCHA MISKANo ratings yet

- AAAJT1833E - Issue Letter - 1049437802 (1) - 06022023Document2 pagesAAAJT1833E - Issue Letter - 1049437802 (1) - 06022023Basavaraj KorishettarNo ratings yet

- GST LatestAmendments Issues 01072023Document85 pagesGST LatestAmendments Issues 01072023Selvakumar MuthurajNo ratings yet

- Perfetti Van Melle IndiaDocument18 pagesPerfetti Van Melle IndiaramitkatyalNo ratings yet

- Eturns: After Studying This Chapter, You Will Be Able ToDocument70 pagesEturns: After Studying This Chapter, You Will Be Able ToChandan ganapathi HcNo ratings yet

- CA Ashish Chaudhary 1Document30 pagesCA Ashish Chaudhary 1sonapakhi nandyNo ratings yet

- Bhati Axa Life InsuranceDocument40 pagesBhati Axa Life InsuranceshashankNo ratings yet

- TS 333 ITAT 2013DEL TS 333 ITAT 2013DEL SPX India PVT LTDDocument5 pagesTS 333 ITAT 2013DEL TS 333 ITAT 2013DEL SPX India PVT LTDbharath289No ratings yet

- Aino Communique 111th Edition Jan 2023 PDFDocument14 pagesAino Communique 111th Edition Jan 2023 PDFSwathi JainNo ratings yet

- 15 04 16 Case2Document26 pages15 04 16 Case2tamanna.vkacaNo ratings yet

- Form 27 Dec 2022Document3 pagesForm 27 Dec 2022srinivasgateNo ratings yet

- ShowfileDocument4 pagesShowfileMkNo ratings yet

- Circular No.60Document4 pagesCircular No.60Hr legaladviserNo ratings yet

- Annexure-X - Waiver of SCN & PenaltyDocument3 pagesAnnexure-X - Waiver of SCN & Penaltyvishnuprakash1990No ratings yet

- GSTR ReturnDocument136 pagesGSTR Returnyoyorikee0% (1)

- 1652426740-447 & 8168 HCL Comnet Systems & Services LTDDocument7 pages1652426740-447 & 8168 HCL Comnet Systems & Services LTDArulnidhi Ramanathan SeshanNo ratings yet

- DRC03Document2 pagesDRC03sumitsharmaNo ratings yet

- Priyanka Tungidwar - 21036Document1 pagePriyanka Tungidwar - 21036Anonymous 5l219Y7Iu1No ratings yet

- Do You Know GST - July 2022Document17 pagesDo You Know GST - July 2022CA Ranjan MehtaNo ratings yet

- Return Formats (Sahaj Return - FORM GST RET-2) (Quarterly) (Including Amendment)Document30 pagesReturn Formats (Sahaj Return - FORM GST RET-2) (Quarterly) (Including Amendment)ch7utiyapa9No ratings yet

- Dcw-Circular-07 10 2021Document12 pagesDcw-Circular-07 10 2021Kombaiah PandianNo ratings yet

- Gateway Technolabs P LTDDocument4 pagesGateway Technolabs P LTDDayavanti Nilesh RanaNo ratings yet

- Attachment 1Document2 pagesAttachment 1khabrilaalNo ratings yet

- Aino Communique Mar 23 113th EditionDocument13 pagesAino Communique Mar 23 113th EditionSwathi JainNo ratings yet

- Circular CGST 131 NewDocument5 pagesCircular CGST 131 NewSanjeev BorgohainNo ratings yet

- आयकर अपीलीय अिधकरण " यायपीठ पुणे म । (Through Virtual Court)Document8 pagesआयकर अपीलीय अिधकरण " यायपीठ पुणे म । (Through Virtual Court)Saksham ShrivastavNo ratings yet

- 2002 83 ITD 151 Delhi SB 2002 77 TTJ 387 Delhi SB 01 08 2002highlightedDocument12 pages2002 83 ITD 151 Delhi SB 2002 77 TTJ 387 Delhi SB 01 08 2002highlightedSnigdha MazumdarNo ratings yet

- 3a Notices Ysk Amar SubDocument1,066 pages3a Notices Ysk Amar SubKrishna ReddyNo ratings yet

- Form GST ASMT - 11 - NNNNNDocument2 pagesForm GST ASMT - 11 - NNNNNGovindNo ratings yet

- Page 1 of 4Document4 pagesPage 1 of 4Sunil ShahNo ratings yet

- Roll No C 17 Prakash Ochwanni Sem XDocument10 pagesRoll No C 17 Prakash Ochwanni Sem XPRAKASH OCHWANINo ratings yet

- Step by Step Compliances Under RCM: How Composition Dealer Will Be Affected by RCM?Document7 pagesStep by Step Compliances Under RCM: How Composition Dealer Will Be Affected by RCM?arpit jainNo ratings yet

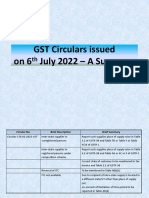

- GST Circulars Issued On 6th July - A SummaryDocument8 pagesGST Circulars Issued On 6th July - A SummaryVijaya ChandNo ratings yet

- Shri Vedavyas Co Operative Credit Society LTD Vs Income Tax Officer 6aeaa3c543bd92250fef9d363c6aa9 DocumentDocument8 pagesShri Vedavyas Co Operative Credit Society LTD Vs Income Tax Officer 6aeaa3c543bd92250fef9d363c6aa9 Documentbharath289No ratings yet

- Return Formats (Sugam Return - FORM GST RET-3) (Quarterly) (Including Amendment)Document32 pagesReturn Formats (Sugam Return - FORM GST RET-3) (Quarterly) (Including Amendment)Puneet PrajapatiNo ratings yet

- 2023 152 Taxmann Com 312 Bombay 14 07 2023 Bombay Dyeing Manufacturing Co LTD VsDocument1 page2023 152 Taxmann Com 312 Bombay 14 07 2023 Bombay Dyeing Manufacturing Co LTD VsSricharan RNo ratings yet

- Returns GSTDocument25 pagesReturns GSTRahul RockzzNo ratings yet

- Value of SupplyDocument16 pagesValue of Supplyhariom bajpaiNo ratings yet

- Appeal SummaryDocument49 pagesAppeal Summarymaapitambraenterprises700No ratings yet

- 1588756021-1693-Allegis Servicses Final PrintDocument9 pages1588756021-1693-Allegis Servicses Final PrintDehradun MootNo ratings yet

- Tax ProjectDocument19 pagesTax Projectsanskarbarekar789No ratings yet

- UntitledDocument5 pagesUntitledharsh hgNo ratings yet

- AACCK3258R - Demand Notice Us 156 - 1052866885 (1) - 16052023Document1 pageAACCK3258R - Demand Notice Us 156 - 1052866885 (1) - 16052023Hitesh DhingraNo ratings yet

- OIO AarkeyTrad 57 13Document20 pagesOIO AarkeyTrad 57 13jitendraktNo ratings yet

- Adobe Scan Nov 27, 2023-CompressedDocument7 pagesAdobe Scan Nov 27, 2023-Compressedswainsachidananda1950No ratings yet

- Gstr-2A: TH TH THDocument1 pageGstr-2A: TH TH THTejaswi J DamerlaNo ratings yet

- Integra Engineering India LTDDocument9 pagesIntegra Engineering India LTDByomkesh PandaNo ratings yet

- Amount Owed by The Business AccountingDocument3 pagesAmount Owed by The Business Accountingelsana philipNo ratings yet

- Classification of Riba: (A) Riba-un-Nasiyah or Riba-al-Jahiliya (B) Riba-al-Fadl or Riba-al-BaiDocument25 pagesClassification of Riba: (A) Riba-un-Nasiyah or Riba-al-Jahiliya (B) Riba-al-Fadl or Riba-al-Baiatifkhan890572267% (3)

- Financial Statement Analysis - Jollibee and MaxDocument21 pagesFinancial Statement Analysis - Jollibee and MaxRemNo ratings yet

- General Mathematics: Second Quarter Module 3: Simple and General AnnuitiesDocument15 pagesGeneral Mathematics: Second Quarter Module 3: Simple and General AnnuitiesJelrose SumalpongNo ratings yet

- The 2013 Capital Requirements Directive IV and Capital Requirements Regulation: Implications and Institutional EffectsDocument49 pagesThe 2013 Capital Requirements Directive IV and Capital Requirements Regulation: Implications and Institutional EffectsbobmezzNo ratings yet

- Emerging Markets Strategy DashboardsDocument26 pagesEmerging Markets Strategy DashboardsqeneibwrNo ratings yet

- Ch-5 MONEYDocument6 pagesCh-5 MONEYYoshita ShahNo ratings yet

- 2016 Nomura Summer Internship ProgramDocument25 pages2016 Nomura Summer Internship ProgramTing-An KuoNo ratings yet

- Sap Guide 2 0 1Document13 pagesSap Guide 2 0 1api-359265393No ratings yet

- Adobe Scan Feb 11, 2024Document20 pagesAdobe Scan Feb 11, 2024DEVIL RDXNo ratings yet

- Deepak Eduworld PVT LTD: Receipt AmountDocument22 pagesDeepak Eduworld PVT LTD: Receipt AmountSupriya BoseNo ratings yet

- Winter 2007 Midterm With SolutionsDocument13 pagesWinter 2007 Midterm With Solutionsupload55No ratings yet

- Notes On Mishkin Chapter 8 (Econ 353, Tesfatsion)Document10 pagesNotes On Mishkin Chapter 8 (Econ 353, Tesfatsion)Karthikeyan PandiarasuNo ratings yet

- Jul-21 Company Name Claim Buddy Numbers From Ir Base Year Below (In Consistent Units) This YearDocument32 pagesJul-21 Company Name Claim Buddy Numbers From Ir Base Year Below (In Consistent Units) This YearProtyay ChakrabortyNo ratings yet

- Working Capital ManagementDocument8 pagesWorking Capital ManagementNickNo ratings yet

- Cash System and Procedure Part 1Document8 pagesCash System and Procedure Part 1Rohit BhaduNo ratings yet

- Brooks Financial mgmt14 PPT ch08Document85 pagesBrooks Financial mgmt14 PPT ch08Jake AbatayoNo ratings yet

- Chap 009Document20 pagesChap 009Ela PelariNo ratings yet

- Monetary PolicyDocument10 pagesMonetary PolicyAshish MisraNo ratings yet

- Ch. 31 Forecasting and Managing Cash FlowsDocument4 pagesCh. 31 Forecasting and Managing Cash FlowsRosina KaneNo ratings yet

- Gul OzerolDocument74 pagesGul OzerolMimma afrinNo ratings yet

- Chapter 9 Interest and DepreciationDocument24 pagesChapter 9 Interest and Depreciationluca.castelvetere04No ratings yet

- 1 - Decentralization-Responsibility AccountingDocument40 pages1 - Decentralization-Responsibility AccountingZedie Leigh VioletaNo ratings yet

- 4002CBS Glossary English To Samoan 6-5-16 2Document51 pages4002CBS Glossary English To Samoan 6-5-16 2Angie Milford (Teph)No ratings yet

- Chapter 10 Part A and Part B ReviewDocument9 pagesChapter 10 Part A and Part B ReviewNhi HoNo ratings yet

- Liquidation ReportDocument3 pagesLiquidation Reportkabataansulong2023No ratings yet

- Soal Un Bahasa InggrisDocument7 pagesSoal Un Bahasa InggrisFauzi AzhariNo ratings yet