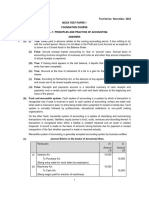

Accounting Notes

Statement of Cash Flows

Statement of Cash Flows:

Operating Activities - activities that generate revenues or expenses in the company š major

line of business.

Receipts Disbursements

- Collections from customers - Payments to suppliers

- Receipts of interest & dividends - Payments to employees

- Other operating receipts - Payments of interest & income tax

- Other operating disbursements

Investing Activities - activities that increase or decrease the long term assets of a business

Receipts Disbursements

- Sale of plant assets - Acquistion of plant assets

- Sale of long term investments - Purchase of long term investments

- Receipts o n loans receivable - Making loans

Financial Activities - activities that obtain the cash needed from investors and creditors to

launch and sustain the business.

Receipts Disbursements

- Issuing of stock - Payment of dividends

- Selling treasury stock - Purchase of treasury stock

- Borrowing money using notes and - Payment of principal amount of debts

bonds payable

Statement of Cash Flows formats:

Direct Method - Format of the operating section of the statement of cash flows lists the

major categories of cash receipts and disbursements.

Indirect Method - Format of the operating section of the statement of cash flows starts with

the net income and then shows the adjustments needed to reconcile the net income

with the cash flows from operating activities.

Page 1

Student Learning Assistance Center, San Antonio College, 2004

Accounting Notes

Statement of Cash Flows

Direct Method Format:

Cash Flow from Operating Activities:

Receipts:

Collections from customers $xxxx

Interest Received xxxx

Dividends Received xxxx

Total Cash Receipts $ xxxxx

Payments:

To suppliers ($xxxx)

To employees ( xxxx)

For Interest ( xxxx)

For Income Tax ( xxxx)

Total Cash Payments ( xxxxx)

Net Cash Flow from Operating Activities $ xxxxx

Cash Flow from Investing Activities:

Acquisition of plant assets ($xxxx)

Loan to another company ( xxxx)

Proceeds from sale of investments xxxx

Proceeds from sale of plant assets xxxx

Collection of loans xxxx

Net Cash Flow from Investing Activites xxxxx

Cash Flow from Financing Activities:

Pro ceeds from issuance of Note Payable $xxxx

Proceeds from issuance of stock xxxx

Payments on Notes Payable ( xxxx)

Dividends Paid ( xxxx)

Purchase of Treasury stock ( xxxx)

Net Cash Flow from Financing Activities ( xxxxx)

Net Increase (Decrease) in Cash $xxxxx

Cash Balance, Beginning of Period xxxxx

Cash Balance, End of Period $xxxxx

Page 2

Student Learning Assistance Center, San Antonio College, 2004

Accounting Notes

Statement of Cash Flows

Direct Method Computations:

Collection from custo mers = Sales + A/R Beg. Bal. - A/R End. Bal.

Payments to suppliers = Cost of Goods Sold + End. Inventory - Beg. Inventory + Beg.

A/P - End. A/P

Payments for operating expenses = Operating Expenses + End. Prepaid Exp. Bal. - Beg.

Prepaid Exp. Bal. + Beg. Accrued Liab. Bal. - End. Accrued Liab. Bal.

Receipt of interest = Interest Revenue + Beg. Interest Receivable Bal. - End. Interest

Receivable Bal.

Receipt of dividends = Dividend Revenue + Beg. Dividend Receivable Bal. - End.

Dividend Receivable Bal.

Payments to employees = Wages Expense + Beg. Wages Payable Bal. - End. Wages

Payable Bal.

Payments for interest = Interest Expense + Beg. Interest Payable Bal. - End. Interest

Payable Bal.

Payments for income taxes = Income Tax Expense + Beg. Income Tax Payable Bal. - End.

Income Tax Payable Bal.

When to add or subtract in the Indirect Method:

Depreciation, Depletion, or Amortization of assets Add

Gains Subtract

Losses Add

Increase in current Assets Subtract

Decrease in current Assets Add

Increase in current Liabilities Add

Decrease in current Liabilities Subtract

Page 3

Student Learning Assistance Center, San Antonio College, 2004

Accounting Notes

Statement of Cash Flows

Indirect Method Format:

Cash Flow from Operating Activities:

Net Income $xxxx

Add (Subtract) items that affect net income

and cash flows differently:

Depreciation, Depletion, Amortization (+) xxxx

Gain on sale of plant asset (-) ( xxxx)

Loss on sale of plant asset (+) xxxx

Decrease in current assets (+) xxxx

Increase in current assets (-) ( xxxx)

Increase in current liabilities (+) xxxx

Decrease in current liabilities (-) ( xxxx)

Net Cash Flow from Operating Activities $ xxxx

Cash Flow from Investing Activities:

$ xxxx

Same format as direct method

(xxxx)

Net Cash Flow from Investing Activities xxxx

Cash Flow from Financing Activities

$ xxxx

Same format as direct method

( xxxx)

Net Cash Flow from Financing Activities xxxx

Net increase (decrease) in cash $ xxxx

Cash Balance, Beginning of the period xxxx

Cash Balance, End of the period $ xxxx

Page 4

Student Learning Assistance Center, San Antonio College, 2004

You might also like

- Accounting and Finance Formulas: A Simple IntroductionFrom EverandAccounting and Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- 1-Cash Flow StatementDocument21 pages1-Cash Flow StatementOvais Zia100% (1)

- Cfas Millan 2020 Answer KeyDocument193 pagesCfas Millan 2020 Answer KeyPEBIDA, DAVERLY N.No ratings yet

- Cash Flow Statement Examples As Per Direct Method: Report Name Sap Report T-CodeDocument6 pagesCash Flow Statement Examples As Per Direct Method: Report Name Sap Report T-Codejainendra100% (1)

- AssignmentDocument8 pagesAssignmentNegil Patrick DolorNo ratings yet

- Property Finals CasesDocument9 pagesProperty Finals CasesMegan MateoNo ratings yet

- Cash Flow StatementDocument19 pagesCash Flow StatementCharu100% (1)

- Module 4 Statement of Cash Flows 1Document9 pagesModule 4 Statement of Cash Flows 1Kimberly BalontongNo ratings yet

- 408 Tax Case BriefDocument256 pages408 Tax Case BriefIsabel Luchie GuimaryNo ratings yet

- Accounting Process Quizzer PDFDocument6 pagesAccounting Process Quizzer PDFDaniel Laurence Salazar Itable100% (1)

- RMC 39-2007 (Agency Fee)Document6 pagesRMC 39-2007 (Agency Fee)rmdelmandoNo ratings yet

- Lesson 10 Bank Reconciliation StatementDocument22 pagesLesson 10 Bank Reconciliation StatementGelai Batad100% (1)

- More Statement of Cash Flow Exercises-1Document8 pagesMore Statement of Cash Flow Exercises-1Juliana CaroNo ratings yet

- Ias 7 Cash Flow Statement ContinuedDocument8 pagesIas 7 Cash Flow Statement ContinuedMichael Bwire100% (1)

- Cash Flow StatementDocument16 pagesCash Flow StatementSagnik Sharangi100% (1)

- L11-Statement of Cash FlowsDocument33 pagesL11-Statement of Cash FlowsSYAMIMI ANUARNo ratings yet

- 2020 Sem 1 ACC10007 Discussion Questions (And Solutions) - Topic 3Document6 pages2020 Sem 1 ACC10007 Discussion Questions (And Solutions) - Topic 3Renee WongNo ratings yet

- The Statement: Statements and The Annual ReportDocument58 pagesThe Statement: Statements and The Annual Reportsaad107100% (1)

- Topic 7 MFRS 107 Statement of Cash FlowsDocument21 pagesTopic 7 MFRS 107 Statement of Cash Flowsaisyahinafaryanis14No ratings yet

- Cash Flow AccountingDocument17 pagesCash Flow AccountingPrabir Kumer RoyNo ratings yet

- Ias 7 Statement of Cashflows (F2)Document7 pagesIas 7 Statement of Cashflows (F2)Tawanda Tatenda Herbert100% (1)

- Lesson 04 - Cash Flow StatementDocument5 pagesLesson 04 - Cash Flow Statementpulitha kodituwakkuNo ratings yet

- Cashflow ExampleDocument6 pagesCashflow ExamplecoolyouhiNo ratings yet

- HANDOUT 2 Cash Flow AnalysisDocument2 pagesHANDOUT 2 Cash Flow AnalysisJayson Bautista RicoNo ratings yet

- Chapter 22 - Statement of Cash FlowsDocument17 pagesChapter 22 - Statement of Cash Flowsprasad guthiNo ratings yet

- F1 Chapter 4 PDFDocument20 pagesF1 Chapter 4 PDFAchiek JamesNo ratings yet

- Cash Flow StatementDocument5 pagesCash Flow StatementDebaditya SenguptaNo ratings yet

- Accounting & Financial Systems (Lecture 7)Document20 pagesAccounting & Financial Systems (Lecture 7)Right Karl-Maccoy HattohNo ratings yet

- تلخيص لغة تانيه 20233Document4 pagesتلخيص لغة تانيه 20233magdy kamelNo ratings yet

- Chapter 18 Cash Flow StatementsDocument11 pagesChapter 18 Cash Flow StatementstyresekupajrNo ratings yet

- Cash Flow Statement FormateDocument3 pagesCash Flow Statement FormatesatyaNo ratings yet

- Cash FlowDocument6 pagesCash FlowKhaneik KingNo ratings yet

- Dac 511: Corporate Financial Reporting & Analysis Group 5 Cash Flow AnalysisDocument44 pagesDac 511: Corporate Financial Reporting & Analysis Group 5 Cash Flow AnalysisJan Dave Ogatis100% (1)

- Accounting Principles: Second Canadian EditionDocument38 pagesAccounting Principles: Second Canadian EditionErik Lorenz PalomaresNo ratings yet

- Statement of Cash FlowsDocument3 pagesStatement of Cash FlowsEricka DelgadoNo ratings yet

- Cash Flow Statement 1220159910575245 9Document17 pagesCash Flow Statement 1220159910575245 9duyphung1234No ratings yet

- Chapter 11 Lecture 2018Document62 pagesChapter 11 Lecture 2018Johnny Sins100% (1)

- Cash Flow Statement NotesDocument6 pagesCash Flow Statement NotesChe DivineNo ratings yet

- Cashflow StatementsDocument4 pagesCashflow Statementsfaith bakasaNo ratings yet

- Pre Reading Material For Session 17 FA (Cash Flow)Document10 pagesPre Reading Material For Session 17 FA (Cash Flow)Rohit Roy100% (1)

- Cash Flow Statement Format Indirect MethodDocument2 pagesCash Flow Statement Format Indirect Methodkashifaslam022No ratings yet

- Cash Flow Notes 1Document2 pagesCash Flow Notes 1Kevin JoyNo ratings yet

- Group BDocument37 pagesGroup BHashen BandaraNo ratings yet

- Cashflow StatementDocument16 pagesCashflow StatementJames NdegwaNo ratings yet

- Cash Flow StatementDocument20 pagesCash Flow StatementPrasad BhanageNo ratings yet

- The Cashflow StatementDocument17 pagesThe Cashflow StatementNdumiso MsizaNo ratings yet

- Cash Flow StatementDocument21 pagesCash Flow StatementMacky RobentaNo ratings yet

- Cash Flow Statement - Indirect MethodDocument5 pagesCash Flow Statement - Indirect MethodBimal KrishnaNo ratings yet

- Cash Flow Statements6Document28 pagesCash Flow Statements6kimuli FreddieNo ratings yet

- Statement of Cash FlowDocument6 pagesStatement of Cash FlowNhel AlvaroNo ratings yet

- Module 3Document22 pagesModule 3ANGEL ROBIN RCBSNo ratings yet

- Cash Flow StatementDocument4 pagesCash Flow StatementRathore NitinNo ratings yet

- Financial Statement AnalysisDocument46 pagesFinancial Statement AnalysisMusom BBANo ratings yet

- CH 16Document57 pagesCH 16Liony KalaloNo ratings yet

- Cash Flow StatementDocument16 pagesCash Flow StatementAjay KareNo ratings yet

- FABM2 - Q1 - V2a Page 59 69Document11 pagesFABM2 - Q1 - V2a Page 59 69joiNo ratings yet

- Statement of Cash FlowDocument19 pagesStatement of Cash FlowSHARMAINE JOY FULGARNo ratings yet

- Dr. Ajay Dwivedi Professor Department of Financial StudiesDocument16 pagesDr. Ajay Dwivedi Professor Department of Financial StudiesKaran Pratap Singh100% (1)

- FinmanDocument62 pagesFinmanJohana Mae DamoleNo ratings yet

- Cash Flow Statement - Lecture 6-8Document41 pagesCash Flow Statement - Lecture 6-8SHIVA THAVANI100% (1)

- IAS - 7 Statement of Cash FlowsDocument29 pagesIAS - 7 Statement of Cash FlowsKəmalə AslanzadəNo ratings yet

- CFS - Accountancy - Grade 12 - Session 10Document62 pagesCFS - Accountancy - Grade 12 - Session 10Nirav Sheth100% (1)

- Cash Flow StatementDocument22 pagesCash Flow StatementThe ONE GUYNo ratings yet

- Cash FlowDocument5 pagesCash FlowSirdar MukodzaniNo ratings yet

- Cash Flow Statement in A NutshellDocument2 pagesCash Flow Statement in A NutshellJuan SalazarNo ratings yet

- Cash Flow Statement Format 2021Document5 pagesCash Flow Statement Format 2021VV MusicNo ratings yet

- FABM 2 Lesson 1 2 3 4 5 SummaryDocument16 pagesFABM 2 Lesson 1 2 3 4 5 SummaryGelai BatadNo ratings yet

- EJ895747Document24 pagesEJ895747Gelai BatadNo ratings yet

- PDF 20230111 082828 0000Document7 pagesPDF 20230111 082828 0000Gelai BatadNo ratings yet

- Review Problems Without AnswersDocument2 pagesReview Problems Without AnswersGelai BatadNo ratings yet

- Review Problems With AnswersDocument5 pagesReview Problems With AnswersGelai BatadNo ratings yet

- Quiz 9 FABM 2 Income Taxation WO Answers 1Document1 pageQuiz 9 FABM 2 Income Taxation WO Answers 1Gelai BatadNo ratings yet

- APA MLA and Chicago Style Research Paper FormattingDocument2 pagesAPA MLA and Chicago Style Research Paper FormattingGelai BatadNo ratings yet

- Lesson 11 Income and Business TaxationDocument51 pagesLesson 11 Income and Business TaxationGelai BatadNo ratings yet

- Slide - BudgetingDocument7 pagesSlide - BudgetingSofia ArissaNo ratings yet

- Tugas Hutang Jangka Panjang - Nur Vina 2011070599Document3 pagesTugas Hutang Jangka Panjang - Nur Vina 2011070599muhammad fadillahNo ratings yet

- Assets Would Have Increased P55,000Document4 pagesAssets Would Have Increased P55,000Louise100% (1)

- Cash Flow Statement Disclosures A Study of Banking Companies in Bangladesh.Document18 pagesCash Flow Statement Disclosures A Study of Banking Companies in Bangladesh.MD. REZAYA RABBINo ratings yet

- Fundamentals of Finance: Ignacio Lezaun English Edition 2021Document27 pagesFundamentals of Finance: Ignacio Lezaun English Edition 2021Elias Macher CarpenaNo ratings yet

- What Is LeasingDocument9 pagesWhat Is LeasingHassan KianiNo ratings yet

- Unit 6: As 27: Financial Reporting of Interests in Joint VenturesDocument28 pagesUnit 6: As 27: Financial Reporting of Interests in Joint Venturesvikash1905No ratings yet

- A. The Constitution and The Income Tax: Federal Income Tax Professor Morrison Fall 2003 CHAPTER 1: IntroductionDocument67 pagesA. The Constitution and The Income Tax: Federal Income Tax Professor Morrison Fall 2003 CHAPTER 1: IntroductioncjleopNo ratings yet

- Case2 MarriottDocument10 pagesCase2 Marriott石曉儒No ratings yet

- Chapter - 1 Introduction To AccountingDocument3 pagesChapter - 1 Introduction To AccountingAnna Olivia MarieNo ratings yet

- 93 Codex Alimentarius CommissionDocument165 pages93 Codex Alimentarius Commissioncpinto39No ratings yet

- Afa 5Document5 pagesAfa 5akash raymondNo ratings yet

- Mariosoft Pos Quotation Final v2 John Nicko LabanaDocument1 pageMariosoft Pos Quotation Final v2 John Nicko LabanaJoy Francia Mae RamosNo ratings yet

- Forbes & Manhattan Coal Corp. Management's Discussion and Analysis For The Three Months Ended May 31, 2012Document30 pagesForbes & Manhattan Coal Corp. Management's Discussion and Analysis For The Three Months Ended May 31, 2012Shankar JhaNo ratings yet

- 12a Isc 858 AccountsDocument18 pages12a Isc 858 AccountsA.c. GuptaNo ratings yet

- Case Digest:Quisumbing Vs GarciaDocument27 pagesCase Digest:Quisumbing Vs GarciaRon Poblete0% (1)

- Uniwide First Quarter 2006 ReportDocument39 pagesUniwide First Quarter 2006 ReportKeith LameraNo ratings yet

- Problems CompiledDocument67 pagesProblems CompiledRosh ClementeNo ratings yet

- MTP 14 28 Answers 1701406110Document11 pagesMTP 14 28 Answers 1701406110aim.cristiano1210No ratings yet

- Sfas 109-EeDocument132 pagesSfas 109-EekyougiNo ratings yet

- Tax and The Taxpayer by Lord TemplemanDocument9 pagesTax and The Taxpayer by Lord TemplemannarkooNo ratings yet

- Rice Company Was Incorporated On January 1Document6 pagesRice Company Was Incorporated On January 1Marjorie PalmaNo ratings yet

- Chapter-9 Analysis of Financial Statements: Section A: One Mark Questions I. Fill in The BlanksDocument10 pagesChapter-9 Analysis of Financial Statements: Section A: One Mark Questions I. Fill in The BlanksAlton D'silvaNo ratings yet

- Reporting The Statement of Cash Flows: QuestionsDocument58 pagesReporting The Statement of Cash Flows: QuestionsMohamed AfzalNo ratings yet