You might also like

- CalypsoTraining PDFDocument399 pagesCalypsoTraining PDFanubhav92% (13)

- Accounting For Special TransactionsDocument43 pagesAccounting For Special Transactionsjohnpenielmontales0% (1)

- Capra Breadth Internal Indicators For Winning Swing and Posistion Trading ManualDocument58 pagesCapra Breadth Internal Indicators For Winning Swing and Posistion Trading ManualVarun VasurendranNo ratings yet

- Consumer Behaviour Towards Mutual FundDocument119 pagesConsumer Behaviour Towards Mutual FundChandan SrivastavaNo ratings yet

- Shrader OptionsManualDocument11 pagesShrader OptionsManualOm Prakash100% (2)

- Module III. Business Combination - Subsequent To Date of AcquisitionDocument5 pagesModule III. Business Combination - Subsequent To Date of AcquisitionAldrin Zolina0% (4)

- Prelim Quiz - Business CombinationDocument4 pagesPrelim Quiz - Business CombinationJeane Mae BooNo ratings yet

- Lesson 1 - Cash and Cash EquivalentsDocument2 pagesLesson 1 - Cash and Cash EquivalentsPol Moises Gregory Clamor88% (16)

- Law On SalesDocument81 pagesLaw On SalesJhanelle Marquez50% (2)

- Accounting For Special TransactionsDocument43 pagesAccounting For Special TransactionsNezer VergaraNo ratings yet

- Consolidated-Financial-Statements-80%-Owned-SubsidiaryDocument10 pagesConsolidated-Financial-Statements-80%-Owned-SubsidiaryBetty SantiagoNo ratings yet

- A Comparative Study On Banking Sector Mutual Funds - NetworthDocument10 pagesA Comparative Study On Banking Sector Mutual Funds - NetworthLOGIC SYSTEMSNo ratings yet

- Fxtradermagazine 1 EgDocument61 pagesFxtradermagazine 1 EgDoncov EngenyNo ratings yet

- More Cash Flow ExercisesDocument4 pagesMore Cash Flow ExercisesLorenzodeLunaNo ratings yet

- Buscom 8Document11 pagesBuscom 8dmangiginNo ratings yet

- Buscom 7Document9 pagesBuscom 7dmangiginNo ratings yet

- Cash Flow 1Document3 pagesCash Flow 1Percy JacksonNo ratings yet

- Advance AssigmentDocument3 pagesAdvance AssigmentAdugna MegenasaNo ratings yet

- Partnership Formation ReviewDocument3 pagesPartnership Formation ReviewRafael Capunpon VallejosNo ratings yet

- Cash FlowsDocument6 pagesCash FlowsZaheer AhmadNo ratings yet

- The Following Data Relate To The Prima Company 1 Exhibit: Unlock Answers Here Solutiondone - OnlineDocument1 pageThe Following Data Relate To The Prima Company 1 Exhibit: Unlock Answers Here Solutiondone - OnlineAmit PandeyNo ratings yet

- Assignment AdvDocument4 pagesAssignment AdvTilahun GirmaNo ratings yet

- Acct 3101 Chapter 05Document13 pagesAcct 3101 Chapter 05Arief RachmanNo ratings yet

- Brief Exercises - Cash FlowDocument4 pagesBrief Exercises - Cash FlowHannah JoyNo ratings yet

- 1 To 111 Thories 1 57Document34 pages1 To 111 Thories 1 57Jyasmine Aura V. AgustinNo ratings yet

- ACCT336 Chapter23 SolutionsDocument7 pagesACCT336 Chapter23 SolutionskareemrawwadNo ratings yet

- Financial MGTDocument2 pagesFinancial MGTSohail Liaqat AliNo ratings yet

- Questions On Chapter FourDocument2 pagesQuestions On Chapter Fourbrook butaNo ratings yet

- Balance Sheet and Cash Flow AnalysisDocument8 pagesBalance Sheet and Cash Flow AnalysisAntonios FahedNo ratings yet

- Financial Management, MBA511, Section: 01 Chapter 3: ProblemsDocument2 pagesFinancial Management, MBA511, Section: 01 Chapter 3: ProblemsShakilNo ratings yet

- Mid-Term - Financial Accounting For Managers July 2010...Document4 pagesMid-Term - Financial Accounting For Managers July 2010...ApoorvNo ratings yet

- AKM 1 Bab 3Document5 pagesAKM 1 Bab 3alesha nindyaNo ratings yet

- Cash Flow Statement1Document2 pagesCash Flow Statement1Mila Mercado0% (1)

- Assignment 3 Lump-Sump LiquidationDocument1 pageAssignment 3 Lump-Sump LiquidationchxrlttxNo ratings yet

- Cash Flow StatementDocument2 pagesCash Flow StatementMila MercadoNo ratings yet

- Review Accounting NotesDocument9 pagesReview Accounting NotesJasin LujayaNo ratings yet

- 03 Course Notes On Statement of Cash Flows-2 PDFDocument4 pages03 Course Notes On Statement of Cash Flows-2 PDFMaxin TanNo ratings yet

- Solutions - CH 5Document4 pagesSolutions - CH 5Khánh AnNo ratings yet

- 111Document7 pages111haerudinsaniNo ratings yet

- FIN 220, Ch3, Selected Problems 2Document3 pagesFIN 220, Ch3, Selected Problems 23ooobd1234No ratings yet

- FINMAN Cash-Flow-Analysis-Practice-Problem-2Document2 pagesFINMAN Cash-Flow-Analysis-Practice-Problem-2stel mariNo ratings yet

- ABC Manufacturing Entity Sole Trader Has Provided You With TheDocument1 pageABC Manufacturing Entity Sole Trader Has Provided You With TheMiroslav GegoskiNo ratings yet

- Presented Here Is The Total Column of The Governmental FundsDocument1 pagePresented Here Is The Total Column of The Governmental Fundstrilocksp SinghNo ratings yet

- Winterschid Company 2008 year-end trial balance and financial statementsDocument6 pagesWinterschid Company 2008 year-end trial balance and financial statementsJa Mi LahNo ratings yet

- Cebu Cpar Practical Accounting 1 Cash Flow - UmDocument9 pagesCebu Cpar Practical Accounting 1 Cash Flow - UmJomarNo ratings yet

- Akm3 Week-10Document5 pagesAkm3 Week-10pizzaanutriaNo ratings yet

- EXERCISE 5-5 (30-35 Minutes) Uhura Company Balance Sheet ...Document4 pagesEXERCISE 5-5 (30-35 Minutes) Uhura Company Balance Sheet ...Thùy Dương ĐồngNo ratings yet

- Assign 1 FA2 SP 23Document2 pagesAssign 1 FA2 SP 23AbdulNo ratings yet

- Solutiondone 2-157Document1 pageSolutiondone 2-157trilocksp SinghNo ratings yet

- Problem 3,5,&8Document4 pagesProblem 3,5,&8Mark CalapatanNo ratings yet

- Tugas 4 - Mukhlasin S 142170091Document10 pagesTugas 4 - Mukhlasin S 142170091Mukhlasin SyaifullahNo ratings yet

- Key Chapter 2Document11 pagesKey Chapter 2JinAe NaNo ratings yet

- Financial Statement Analysis Tools for ACC C 204Document18 pagesFinancial Statement Analysis Tools for ACC C 204Hannah JoyNo ratings yet

- Accounting ExerciseDocument6 pagesAccounting Exercisenourhan hegazyNo ratings yet

- Bryant Ritchie Trisnodjojo - 041911333021 - AKM 3 Week 10Document4 pagesBryant Ritchie Trisnodjojo - 041911333021 - AKM 3 Week 10Goji iiiNo ratings yet

- Exhibit 7.1: Financial Statement AnalysisDocument2 pagesExhibit 7.1: Financial Statement AnalysisYean SoramyNo ratings yet

- F.reporting - Final Exams PreparationsDocument54 pagesF.reporting - Final Exams PreparationsAbuu lsmailNo ratings yet

- Accounting Warren 23rd Edition Solutions ManualDocument54 pagesAccounting Warren 23rd Edition Solutions Manualbrennadrusillas7zNo ratings yet

- 2010 06 24 - 172141 - P3 3aDocument4 pages2010 06 24 - 172141 - P3 3aVivian0% (1)

- Statement of Cash Flows - ProblemsDocument2 pagesStatement of Cash Flows - ProblemsMiladanica Barcelona BarracaNo ratings yet

- Financial and Managerial Accounting Group AssignmentDocument9 pagesFinancial and Managerial Accounting Group AssignmentDagmawit NegussieNo ratings yet

- Module 2 Homework Answer KeyDocument5 pagesModule 2 Homework Answer KeyMrinmay kunduNo ratings yet

- Extra Applications - Lecture Week 2Document5 pagesExtra Applications - Lecture Week 2Muhammad HusseinNo ratings yet

- Problem Set 6 BS CS 6Document3 pagesProblem Set 6 BS CS 6Rubab MirzaNo ratings yet

- Statement of Cash Flows and Financial Position AnalysisDocument5 pagesStatement of Cash Flows and Financial Position AnalysisFiyo DarmawanNo ratings yet

- Mannie Company worksheet data adjustmentsDocument17 pagesMannie Company worksheet data adjustmentsVy Pham Nguyen KhanhNo ratings yet

- The Boston Institute of Finance Mutual Fund Advisor Course: Series 6 and Series 63 Test PrepFrom EverandThe Boston Institute of Finance Mutual Fund Advisor Course: Series 6 and Series 63 Test PrepNo ratings yet

- What Is Mental HealthDocument3 pagesWhat Is Mental HealthHusnul KhatimahNo ratings yet

- Jurnal CohesionDocument17 pagesJurnal CohesionAri andreNo ratings yet

- Booklet 1 CORRECTION OF ERRORS CASHDocument17 pagesBooklet 1 CORRECTION OF ERRORS CASHnaddieNo ratings yet

- Booklet 2 RECEIVABLES INVENTORYDocument25 pagesBooklet 2 RECEIVABLES INVENTORYnaddieNo ratings yet

- Defining mental health and exploring stigma in childrenDocument13 pagesDefining mental health and exploring stigma in childrenUsman Ahmad TijjaniNo ratings yet

- Introduction To Research: July 2016Document25 pagesIntroduction To Research: July 2016Subash DangalNo ratings yet

- Unlocking of Chakras - The Whispers of The SoulDocument4 pagesUnlocking of Chakras - The Whispers of The SoulnaddieNo ratings yet

- Oaisis HotelDocument11 pagesOaisis HotelnaddieNo ratings yet

- Improving Mental Health Through ExerciseDocument6 pagesImproving Mental Health Through ExercisenaddieNo ratings yet

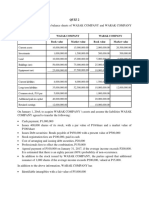

- Wasak and Warak balance sheets acquisition quizDocument3 pagesWasak and Warak balance sheets acquisition quiznaddieNo ratings yet

- JPIA Got Talent Score Sheet DANCINGDocument1 pageJPIA Got Talent Score Sheet DANCINGnaddieNo ratings yet

- Jpia Got Talent Score Sheet Art MakingDocument2 pagesJpia Got Talent Score Sheet Art MakingnaddieNo ratings yet

- Stat CompileDocument115 pagesStat CompilenaddieNo ratings yet

- Jpia Got Talent Score Sheet Art MakingDocument2 pagesJpia Got Talent Score Sheet Art MakingnaddieNo ratings yet

- Alg DesignDocument59 pagesAlg DesignnaddieNo ratings yet

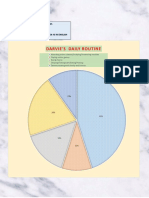

- Darvie'S Daily Routine: Darvie Jr. L. Ramos 7-Ruby Performance Task #3 in EnglishDocument2 pagesDarvie'S Daily Routine: Darvie Jr. L. Ramos 7-Ruby Performance Task #3 in EnglishnaddieNo ratings yet

- FindingsDocument1 pageFindingsnaddieNo ratings yet

- JPIA Got Talent Score Sheet SINGINGDocument1 pageJPIA Got Talent Score Sheet SINGINGnaddieNo ratings yet

- AssumptionDocument1 pageAssumptionnaddieNo ratings yet

- RRLDocument7 pagesRRLnaddieNo ratings yet

- 5 Ways To Protect Your Mental Health During Quarantine: Keep A RoutineDocument1 page5 Ways To Protect Your Mental Health During Quarantine: Keep A RoutinenaddieNo ratings yet

- RECOMMENDATIONDocument1 pageRECOMMENDATIONnaddieNo ratings yet

- The Normal DistributionDocument36 pagesThe Normal DistributionnaddieNo ratings yet

- Chapter 4: Accruals & DeferralsDocument4 pagesChapter 4: Accruals & DeferralsnaddieNo ratings yet

- Statement of Changes in Equity and Income StatementDocument1 pageStatement of Changes in Equity and Income StatementnaddieNo ratings yet

- Purposive Communication Book Reading Report " (Bette and Joan: The Divine Feud) " Author: Shaun ConsidineDocument1 pagePurposive Communication Book Reading Report " (Bette and Joan: The Divine Feud) " Author: Shaun ConsidinenaddieNo ratings yet

- Human Lives Were Lost Due To A Disregard of Proper Building Codes and Legally-Mandated Work Safety StandardsDocument2 pagesHuman Lives Were Lost Due To A Disregard of Proper Building Codes and Legally-Mandated Work Safety StandardsnaddieNo ratings yet

- Chapter 6 - BfarDocument10 pagesChapter 6 - BfarnaddieNo ratings yet

- SoS MidTerm ReportDocument17 pagesSoS MidTerm ReportDheeraj Kumar ReddyNo ratings yet

- Analysis of Bfsi Industry in India: Prepared by Devansh VermaDocument4 pagesAnalysis of Bfsi Industry in India: Prepared by Devansh VermaDevansh VermaNo ratings yet

- 251 0405Document23 pages251 0405api-27548664No ratings yet

- Rahul Singh 119Document13 pagesRahul Singh 119Jerry SinghNo ratings yet

- Financial Health RatiosDocument29 pagesFinancial Health Ratiosmushiechan888No ratings yet

- Imu600 Final July 2022Document3 pagesImu600 Final July 2022fathul dzarifNo ratings yet

- RDRBDocument7 pagesRDRBaspentrades1No ratings yet

- PRESENTATION ON Finincial Statement FinalDocument28 pagesPRESENTATION ON Finincial Statement FinalNollecy Takudzwa Bere100% (2)

- E-mini Stock Index Futures: An IntroductionDocument13 pagesE-mini Stock Index Futures: An IntroductionEric MarlowNo ratings yet

- M/S Champalal K .Vardhan & Co Executive Summary: ProfileDocument21 pagesM/S Champalal K .Vardhan & Co Executive Summary: ProfileVishmita Vanage100% (1)

- HeikinAshi CandleStick Formulae For MetaStockDocument5 pagesHeikinAshi CandleStick Formulae For MetaStockKhaled Hammad AhmedNo ratings yet

- Tutorial 3 PFPDocument6 pagesTutorial 3 PFPWinjie PangNo ratings yet

- Indian Salon Hair and Skin Products Industry ReportDocument24 pagesIndian Salon Hair and Skin Products Industry ReportReevolv Advisory Services Private LimitedNo ratings yet

- Credit Risk and Credit Derivatives: Characteristics and Risk ManagementDocument34 pagesCredit Risk and Credit Derivatives: Characteristics and Risk ManagementNajze AleksandrovaNo ratings yet

- Annex 17 New Financial Advisers Remuneration and Incentive RegulationsDocument7 pagesAnnex 17 New Financial Advisers Remuneration and Incentive RegulationstrishitalalaNo ratings yet

- JP Morgan BacheletDocument4 pagesJP Morgan BacheletDiario ElMostrador.clNo ratings yet

- Insurance Question BankDocument58 pagesInsurance Question BankGaneshNo ratings yet

- Liquidity ManagementDocument13 pagesLiquidity ManagementUpomaAhmedNo ratings yet

- The Wall Street Journal 10 June 2023Document58 pagesThe Wall Street Journal 10 June 2023Raden Angga Widitama PutraNo ratings yet

- CANSLIM Bear Market TMLsDocument18 pagesCANSLIM Bear Market TMLsYS FongNo ratings yet

- E120 Fall14 HW6Document2 pagesE120 Fall14 HW6kimball_536238392No ratings yet

- Fundamental Equity Analysis - SPI Index - The Top 100 Companies of The Swiss Performance IndexDocument205 pagesFundamental Equity Analysis - SPI Index - The Top 100 Companies of The Swiss Performance IndexQ.M.S Advisors LLCNo ratings yet

- Debt Vs EquityDocument27 pagesDebt Vs EquitynisakardryNo ratings yet