You might also like

- Homeowner's Simple Guide to Property Tax Protest: Whats key: Exemptions & Deductions Blind. Disabled. Over 65. Property Rehabilitation. VeteransFrom EverandHomeowner's Simple Guide to Property Tax Protest: Whats key: Exemptions & Deductions Blind. Disabled. Over 65. Property Rehabilitation. VeteransNo ratings yet

- Authoritative Guide On Real Estate Transfer TaxesDocument37 pagesAuthoritative Guide On Real Estate Transfer TaxesJames ReyesNo ratings yet

- pubInfAgenda202101123B4 PDFDocument25 pagespubInfAgenda202101123B4 PDFNancy GarthhNo ratings yet

- MTF Tax Journal November 2021Document15 pagesMTF Tax Journal November 2021Christine Jane RodriguezNo ratings yet

- Bold Venture Appraisal ReportDocument123 pagesBold Venture Appraisal ReportjustinmagdoNo ratings yet

- ESSAY Suggested AnswersDocument5 pagesESSAY Suggested AnswersAe-cha Nae GukNo ratings yet

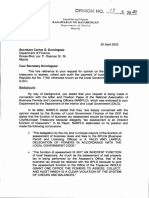

- Opinion No. 17, 2020 - 2Document7 pagesOpinion No. 17, 2020 - 2April Joy AsbocNo ratings yet

- Purpose of Loan & Amount Information of ApplicantDocument5 pagesPurpose of Loan & Amount Information of ApplicantNecky SairahNo ratings yet

- SolutionsDocument16 pagesSolutionsapi-3817072100% (2)

- XX. CIR vs. Fitness by Design, IncDocument11 pagesXX. CIR vs. Fitness by Design, IncStef OcsalevNo ratings yet

- CJHDC v. CBAADocument21 pagesCJHDC v. CBAAErl RoseteNo ratings yet

- Tax Hand Book of KPTCL 16-02-16Document111 pagesTax Hand Book of KPTCL 16-02-16Prasad IyengarNo ratings yet

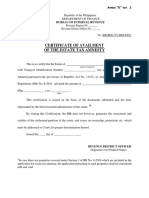

- Certificate of Availment of The Estate Tax Amnesty: Annex "B" Ver. 2Document1 pageCertificate of Availment of The Estate Tax Amnesty: Annex "B" Ver. 2PaulNo ratings yet

- Tax Administration: Bacc 2 Income Taxation Franklin D. Lopez, CPADocument1 pageTax Administration: Bacc 2 Income Taxation Franklin D. Lopez, CPAJaeun SooNo ratings yet

- Certificate of Creditable Tax Withheld at SourceDocument2 pagesCertificate of Creditable Tax Withheld at SourceRhecin Glenale BonalosNo ratings yet

- 16585-1987-Amendment of Transitory Rules On Valuation Of20220425-11-1eaflcrDocument2 pages16585-1987-Amendment of Transitory Rules On Valuation Of20220425-11-1eaflcrbjjwx2h66sNo ratings yet

- 2307 FormDocument3 pages2307 FormK and F Construction Dev't CorpNo ratings yet

- Bir Form 2307 SampleDocument3 pagesBir Form 2307 SampleEliza Cortez Castro50% (2)

- BIR Ruling No. 1397-18Document4 pagesBIR Ruling No. 1397-18SGNo ratings yet

- Instructions For Bidding: State Surplus Property Bid Sheet and AffidavitDocument2 pagesInstructions For Bidding: State Surplus Property Bid Sheet and AffidavitJacob GiffenNo ratings yet

- Philips CertificateDocument3 pagesPhilips CertificateGandaNo ratings yet

- PMR 2307Document1 pagePMR 2307Rheddy RaymundoNo ratings yet

- 2019 Annual BHDocument152 pages2019 Annual BHNicolas GomezNo ratings yet

- BOI Vat-Zero Rating Application & RequirementsDocument3 pagesBOI Vat-Zero Rating Application & RequirementsUnicargo Int'l ForwardingNo ratings yet

- LRA Duty FreeDocument9 pagesLRA Duty FreeRavi KumarNo ratings yet

- Annex B - RMC 103-2019Document2 pagesAnnex B - RMC 103-2019Ra JeNo ratings yet

- Annex B - RMC 103-2019Document2 pagesAnnex B - RMC 103-2019Isaac Dominic MacaranasNo ratings yet

- BIR Certificate of No Outstanding Liability 2019Document1 pageBIR Certificate of No Outstanding Liability 2019jonahpamathiNo ratings yet

- PC Square2307Document3 pagesPC Square2307SirManny ReyesNo ratings yet

- CRS Tax Residency Self Certification Form For Controlling Persons (CRS-CP)Document2 pagesCRS Tax Residency Self Certification Form For Controlling Persons (CRS-CP)Salman ArshadNo ratings yet

- 2019form - RevGIS - NonStock - Updated For Year 2020Document6 pages2019form - RevGIS - NonStock - Updated For Year 2020Joana Saquing100% (1)

- SCI Tax Clearance CertificateDocument1 pageSCI Tax Clearance Certificatekenneth tamalaNo ratings yet

- Pa Rev 1220asDocument2 pagesPa Rev 1220asVikram rajputNo ratings yet

- Leida Mae Bumanlag Refresher B Answers To 2019 Bar Examination On TaxationDocument13 pagesLeida Mae Bumanlag Refresher B Answers To 2019 Bar Examination On TaxationLei BumanlagNo ratings yet

- Zimbabwe Revenue AuthorityDocument5 pagesZimbabwe Revenue AuthorityAlton MadyaraNo ratings yet

- J.R.a. Philippines, Inc. vs. Commissioner of Internal RevenueDocument6 pagesJ.R.a. Philippines, Inc. vs. Commissioner of Internal Revenuevince005No ratings yet

- GBCI 10k-22Document126 pagesGBCI 10k-22hamesNo ratings yet

- Form 11Document44 pagesForm 11gilbert.belciugNo ratings yet

- Bir Form 2307 SampleDocument3 pagesBir Form 2307 SampleErick Echual75% (4)

- Notice of Assessment 2021 04 01 17 31 56 853329Document4 pagesNotice of Assessment 2021 04 01 17 31 56 85332969j8mpp2scNo ratings yet

- Bir05 PDFDocument3 pagesBir05 PDFBarangay LumbangNo ratings yet

- 11 CIR vs. Next MobileDocument20 pages11 CIR vs. Next MobileDianne LingalNo ratings yet

- Income Tax Declaration User Manual: Fc&A Services - Taxation TeamDocument6 pagesIncome Tax Declaration User Manual: Fc&A Services - Taxation TeammikekikNo ratings yet

- Kiryas Joel Bond Preliminary StatementDocument88 pagesKiryas Joel Bond Preliminary StatementJohn N. AllegroNo ratings yet

- Microsoft Vs CIRDocument1 pageMicrosoft Vs CIRKaren Mae ServanNo ratings yet

- Ar VMW 2021Document160 pagesAr VMW 2021gvinothkumargvkNo ratings yet

- Tax1-BIR Ruling 13-2004 (Headquarters Exempt)Document4 pagesTax1-BIR Ruling 13-2004 (Headquarters Exempt)SuiNo ratings yet

- CTHartford01b POSDocument345 pagesCTHartford01b POSrealhartfordNo ratings yet

- Singh, Jashanpreet Tax PDF 2020 SignedDocument20 pagesSingh, Jashanpreet Tax PDF 2020 SignedJashan Dere AalaNo ratings yet

- 2016 Revenue Bond Prospectus McGowin Park Improvement DistrictDocument244 pages2016 Revenue Bond Prospectus McGowin Park Improvement DistrictMike Leahy100% (1)

- American Rescue Plan Act of 2021 - An AnalysisDocument37 pagesAmerican Rescue Plan Act of 2021 - An Analysisanthony jassoNo ratings yet

- Government Accounting: Accounting For Non-Profit OrganizationsDocument21 pagesGovernment Accounting: Accounting For Non-Profit OrganizationsRowena GarnierNo ratings yet

- RMC No. 121-2020 Annex ADocument1 pageRMC No. 121-2020 Annex Aveloxenergy.taxcompspecialistNo ratings yet

- 01-Uptown ServicesDocument2 pages01-Uptown ServicesMarina ButlayNo ratings yet

- Bio Restorative BKDocument56 pagesBio Restorative BKtriguy_2010No ratings yet

- 2307Document2 pages2307Nephy Bersales Taberara67% (3)

- FBT Form 1603Document2 pagesFBT Form 1603Cb SingsonNo ratings yet

- J.K. Lasser's Your Income Tax 2019: For Preparing Your 2018 Tax ReturnFrom EverandJ.K. Lasser's Your Income Tax 2019: For Preparing Your 2018 Tax ReturnNo ratings yet

- Four Lakes Task Force Three Year ReportDocument4 pagesFour Lakes Task Force Three Year ReportIsabelle PasciollaNo ratings yet

- San Antonio Police Department Police Report On The Arrest of Daniel Pentkowski.Document2 pagesSan Antonio Police Department Police Report On The Arrest of Daniel Pentkowski.David ClarkNo ratings yet

- San Antonio City Attorney LetterDocument2 pagesSan Antonio City Attorney LetterDavid ClarkNo ratings yet

- Daniel Pentkowski Booking RecordDocument1 pageDaniel Pentkowski Booking RecordDavid ClarkNo ratings yet

- Litter Disposal Fee AmendmentDocument5 pagesLitter Disposal Fee AmendmentIsabelle PasciollaNo ratings yet

- Midland Flood Reduction PlanDocument2 pagesMidland Flood Reduction PlanIsabelle PasciollaNo ratings yet

- Midland Flood Reduction PlanDocument2 pagesMidland Flood Reduction PlanIsabelle PasciollaNo ratings yet

- Congressman Kildee's Flood Mitigation LetterDocument1 pageCongressman Kildee's Flood Mitigation LetterIsabelle PasciollaNo ratings yet

- 2022 Drinking Water ReportDocument4 pages2022 Drinking Water ReportIsabelle PasciollaNo ratings yet

- FDDP Opt-Out Charge CalculationDocument2 pagesFDDP Opt-Out Charge CalculationIsabelle PasciollaNo ratings yet

- City of Midland Rules and Regulations For Disposal of RefuseDocument9 pagesCity of Midland Rules and Regulations For Disposal of RefuseIsabelle PasciollaNo ratings yet

- Midland County ESA May 2023 Ballot ProposalDocument6 pagesMidland County ESA May 2023 Ballot ProposalIsabelle PasciollaNo ratings yet

- Lincoln Park Residences MapDocument1 pageLincoln Park Residences MapIsabelle PasciollaNo ratings yet

- Book of Mormon: Scripture Stories Coloring BookDocument22 pagesBook of Mormon: Scripture Stories Coloring BookJEJESILZANo ratings yet

- The Juilliard School Admission Music Technology CenterDocument2 pagesThe Juilliard School Admission Music Technology CenterBismarck MartínezNo ratings yet

- AtsikhataDocument6 pagesAtsikhataKaran Upadhyay100% (1)

- Court TranscriptDocument13 pagesCourt Transcriptrea balag-oyNo ratings yet

- Document 1Document3 pagesDocument 1Micky YnopiaNo ratings yet

- Only Daughter: Sandra CisnerosDocument2 pagesOnly Daughter: Sandra CisnerosUzhe ChávezNo ratings yet

- Filipino-Social ThinkersDocument2 pagesFilipino-Social ThinkersadhrianneNo ratings yet

- Street Art From The Underground: After Pei Protests N.Y.U. Plan, Supermarket Site Is New FocusDocument28 pagesStreet Art From The Underground: After Pei Protests N.Y.U. Plan, Supermarket Site Is New FocusTroy MastersNo ratings yet

- Sop QC 04Document3 pagesSop QC 04MNuamanNo ratings yet

- EF3e Int Filetest 010a Answer SheetDocument1 pageEF3e Int Filetest 010a Answer SheetRomanNo ratings yet

- Economics in Education: Freddie C. Gallardo Discussant Ma. Janelyn T. Fundal ProfessorDocument14 pagesEconomics in Education: Freddie C. Gallardo Discussant Ma. Janelyn T. Fundal ProfessorDebbie May Ferolino Yelo-QuiandoNo ratings yet

- Intentional InjuriesDocument29 pagesIntentional InjuriesGilvert A. PanganibanNo ratings yet

- Azure Ea Us - Bif - Sow Template Fy15Document5 pagesAzure Ea Us - Bif - Sow Template Fy15SergeyNo ratings yet

- 1Document4 pages1vikram270693No ratings yet

- Uttar Pradesh TourismDocument32 pagesUttar Pradesh TourismAnone AngelicNo ratings yet

- Kusnandar - InsideDocument159 pagesKusnandar - InsideKusnandarNo ratings yet

- The Correlation Between Poverty and Reading SuccessDocument18 pagesThe Correlation Between Poverty and Reading SuccessocledachingchingNo ratings yet

- 50 bt Mức độ nhận biết - phần 1Document4 pages50 bt Mức độ nhận biết - phần 1Mai BùiNo ratings yet

- IMNPD AssignmentDocument49 pagesIMNPD AssignmentSreePrakash100% (3)

- Module 3 READINGS IN PHILIPPINE HISTORY Wala Pa NahomanDocument4 pagesModule 3 READINGS IN PHILIPPINE HISTORY Wala Pa NahomanJerson Dela CernaNo ratings yet

- Moot Proposition GJC 2023Document9 pagesMoot Proposition GJC 2023Prasun Ojha 83No ratings yet

- 2018 Management Accounting Ibm2 PrepDocument9 pages2018 Management Accounting Ibm2 PrepВероника КулякNo ratings yet

- SATIP-Q-006-03 Foamed Asphalt Stabilization REV1Document2 pagesSATIP-Q-006-03 Foamed Asphalt Stabilization REV1Abdul HannanNo ratings yet

- Narrative (Successful Chef)Document2 pagesNarrative (Successful Chef)Melissa RosilaNo ratings yet

- Perceptions of Borders and Human Migration: The Human (In) Security of Shan Migrant Workers in ThailandDocument90 pagesPerceptions of Borders and Human Migration: The Human (In) Security of Shan Migrant Workers in ThailandPugh JuttaNo ratings yet

- Speed Up Your BSNL BroadBand (Guide)Document13 pagesSpeed Up Your BSNL BroadBand (Guide)Hemant AroraNo ratings yet

- Cyborg Urbanization - Matthew GandyDocument24 pagesCyborg Urbanization - Matthew GandyAngeles Maqueira YamasakiNo ratings yet

- 5 Species Interactions, Ecological Succession, Population ControlDocument8 pages5 Species Interactions, Ecological Succession, Population ControlAnn ShawNo ratings yet

- Architect's Letter To Village of La GrangeDocument13 pagesArchitect's Letter To Village of La GrangeDavid GiulianiNo ratings yet

- Drug and AlchoholDocument1 pageDrug and AlchoholBIREN SHAHNo ratings yet