You might also like

- ICAEW - Accounting 2020 - Chap 4Document78 pagesICAEW - Accounting 2020 - Chap 4TRIEN DINH TIENNo ratings yet

- Question Analysis ICAB Application Level TAXATION-II (Syllabus Weight Based)Document68 pagesQuestion Analysis ICAB Application Level TAXATION-II (Syllabus Weight Based)Optimal Management SolutionNo ratings yet

- Derivatives AFMDocument63 pagesDerivatives AFMSamarth SinghNo ratings yet

- Intution Revision NotesDocument76 pagesIntution Revision NotesPhebin PhilipNo ratings yet

- C02 Sample Questions Feb 2013Document20 pagesC02 Sample Questions Feb 2013Elizabeth Fernandez100% (1)

- Management Accounting: Pilot Paper From December 2011 OnwardsDocument23 pagesManagement Accounting: Pilot Paper From December 2011 OnwardsTaskin Reza KhalidNo ratings yet

- PM Mock QuestionsDocument16 pagesPM Mock QuestionsMuhammad HussnainNo ratings yet

- Icaew Cfab Asr 2019 SyllabusDocument12 pagesIcaew Cfab Asr 2019 SyllabusAnonymous ulFku1vNo ratings yet

- Accounting Final Mock 1 2023Document13 pagesAccounting Final Mock 1 2023diya pNo ratings yet

- 110101131Document667 pages110101131Santha Kannan100% (1)

- ICAEW A&A - ORCHID ME - QsDocument12 pagesICAEW A&A - ORCHID ME - QsJacqueline Kanesha JamesNo ratings yet

- CimaDocument174 pagesCimaroman marian89100% (1)

- Gmap Revised Global Management Accounting PrinciplesDocument84 pagesGmap Revised Global Management Accounting PrinciplesSANG HOANG THANHNo ratings yet

- Pages From BPP CIMA C1 COURSE NOTE 2012 New SyllabusDocument50 pagesPages From BPP CIMA C1 COURSE NOTE 2012 New Syllabusadad9988100% (1)

- ICAEW - MA1 - LECTURE NOTES - For StudentsDocument108 pagesICAEW - MA1 - LECTURE NOTES - For StudentsNga Đào Thị Hằng100% (1)

- CL Suggested Ans - Nov Dec 2019 PDFDocument63 pagesCL Suggested Ans - Nov Dec 2019 PDFMd SelimNo ratings yet

- Sunway University College THE INSTITUTE OF CHARTERED ACCOUNTANTS (ICAEW) Programme 2010Document12 pagesSunway University College THE INSTITUTE OF CHARTERED ACCOUNTANTS (ICAEW) Programme 2010Sunway University100% (1)

- Commercial & Industrial Laws: Nobbodoy PublicationDocument84 pagesCommercial & Industrial Laws: Nobbodoy PublicationRasel UddinNo ratings yet

- Management Information Question Bank 2019Document336 pagesManagement Information Question Bank 2019k20b.lehoangvu100% (1)

- Accounting Chapter 2 MCQ by Nobel Professional AcademyDocument16 pagesAccounting Chapter 2 MCQ by Nobel Professional AcademytafsirmhinNo ratings yet

- Cma Question - r1 - Legal Environment of BusinessDocument12 pagesCma Question - r1 - Legal Environment of BusinessMuhammad Ziaul Haque100% (1)

- CMA MCQ MergedDocument224 pagesCMA MCQ Mergedsaikat karmakarNo ratings yet

- Taxation Sammary Ranjan SirDocument76 pagesTaxation Sammary Ranjan SirWahid100% (2)

- F6 Revision Notes PDFDocument124 pagesF6 Revision Notes PDFЛюба Иванова100% (1)

- I Cap If Rs QuestionsDocument34 pagesI Cap If Rs QuestionsUsmän MïrżäNo ratings yet

- Caf 8 Cma ST PDFDocument656 pagesCaf 8 Cma ST PDFAbdullah DildarNo ratings yet

- f8 RQB 15 Sample PDFDocument98 pagesf8 RQB 15 Sample PDFChandni VariaNo ratings yet

- Exam Form (Application Stage)Document5 pagesExam Form (Application Stage)Akash79No ratings yet

- Syllabus of Knowledge Level For ICABDocument24 pagesSyllabus of Knowledge Level For ICABhridimamalik100% (2)

- P2 September 2014 PaperDocument20 pagesP2 September 2014 PaperAshraf ValappilNo ratings yet

- CAF09 QB 2017 Revised PDFDocument203 pagesCAF09 QB 2017 Revised PDFAsad ZahidNo ratings yet

- Assurance Question Bank 2019 P 192 StudocuDocument193 pagesAssurance Question Bank 2019 P 192 StudocuShahid MahmudNo ratings yet

- SFM Theory Booklet PDFDocument132 pagesSFM Theory Booklet PDFManoj VenkatNo ratings yet

- Objective Questions PDFDocument118 pagesObjective Questions PDFFahad Khan TareenNo ratings yet

- Icag New Syllabus 2024Document98 pagesIcag New Syllabus 2024ekadanu CAGL100% (1)

- MA RC September 2019-August 2020 As at 12 March 2019 FinalDocument238 pagesMA RC September 2019-August 2020 As at 12 March 2019 FinalOlha LNo ratings yet

- PAC All CAF Subjects Mock QP With Solutions Compiled by Saboor AhmadDocument132 pagesPAC All CAF Subjects Mock QP With Solutions Compiled by Saboor AhmadHadeed HafeezNo ratings yet

- Business Planning Insurance 2020 Question Bank SampleDocument50 pagesBusiness Planning Insurance 2020 Question Bank SampleIsavic Alsina100% (1)

- Tareq Ahmed (Faisal) M.J.Abedin & CoDocument49 pagesTareq Ahmed (Faisal) M.J.Abedin & Cotusher pepolNo ratings yet

- ACCA FIA - Accountant in Business (AB) - Teaching Slides - 2019Document1,007 pagesACCA FIA - Accountant in Business (AB) - Teaching Slides - 2019Vimala RavishankarNo ratings yet

- ICAEW Principal of Tax Question Bank 2024 Final 1Document226 pagesICAEW Principal of Tax Question Bank 2024 Final 1k20b.lehoangvuNo ratings yet

- PM Book - FinalDocument372 pagesPM Book - FinalThu Hà Phan ThịNo ratings yet

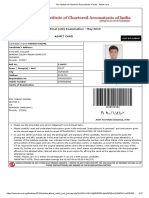

- CA Admit Card May-19Document15 pagesCA Admit Card May-19NEERNo ratings yet

- All AFM Technical Articles 2021Document139 pagesAll AFM Technical Articles 2021Ashfaq Ul Haq OniNo ratings yet

- Buet Question of 2015-2016 (L-2 T-1) - CeDocument18 pagesBuet Question of 2015-2016 (L-2 T-1) - CePicasso Debnath0% (1)

- Auditing BitsDocument48 pagesAuditing BitskalyanikamineniNo ratings yet

- f7 Mock QuestionDocument20 pagesf7 Mock Questionnoor ul anumNo ratings yet

- ICAEW AssuranceDocument156 pagesICAEW AssuranceThành Vinh NguyễnNo ratings yet

- December 2002 ACCA Paper 2.5 QuestionsDocument11 pagesDecember 2002 ACCA Paper 2.5 QuestionsUlanda2No ratings yet

- Management Information PDFDocument366 pagesManagement Information PDFmamun ahmed100% (1)

- Assurance 1Document247 pagesAssurance 1phuongthaosally10xNo ratings yet

- Ifrss Learning and Assessment Programme: Diego MiguitaDocument1 pageIfrss Learning and Assessment Programme: Diego MiguitaVinte UmNo ratings yet

- 2021 COAF 4201 GroupsDocument16 pages2021 COAF 4201 GroupsTawanda Tatenda HerbertNo ratings yet

- اسئلة اقتصادية باللغة الانجليزيةDocument5 pagesاسئلة اقتصادية باللغة الانجليزيةMoun DirNo ratings yet

- Bai Tap CMQT clc59Document20 pagesBai Tap CMQT clc59Hải AnhNo ratings yet

- AIS16Exercises SCDocument6 pagesAIS16Exercises SCSarah GherdaouiNo ratings yet

- Mock - Quiz - Intermediate Accounting IDocument2 pagesMock - Quiz - Intermediate Accounting IАйбар КарабековNo ratings yet

- 4 Property Plant Equipment Classification Acquisition Govt Grant and Borrowing CostDocument11 pages4 Property Plant Equipment Classification Acquisition Govt Grant and Borrowing CostElvie PepitoNo ratings yet

- Bai Tap CMQT clc59Document21 pagesBai Tap CMQT clc59Hằng LêNo ratings yet

- International Accounting Doupnik 4th Edition Test BankDocument4 pagesInternational Accounting Doupnik 4th Edition Test BankmanhkieraebyzNo ratings yet

- 10 FixedAsset 21 FixedAsset InitSettingsDocument32 pages10 FixedAsset 21 FixedAsset InitSettingsCrazy TechNo ratings yet

- PRINCIPLES OF ACCOUNTING Summary NotesDocument4 pagesPRINCIPLES OF ACCOUNTING Summary NotesKeyah NkonghoNo ratings yet

- Jawaban Perhitungan Dan Akumulasi BiayaDocument7 pagesJawaban Perhitungan Dan Akumulasi BiayaEka OematanNo ratings yet

- Audit ReportDocument3 pagesAudit ReportCrystal Jenn BalabaNo ratings yet

- Chapter 5 Advanced AccountingDocument47 pagesChapter 5 Advanced Accountingthescribd94No ratings yet

- Examinable DocumentsDocument3 pagesExaminable DocumentsKim SoonNo ratings yet

- Financial Management 101Document14 pagesFinancial Management 101mushtaq72No ratings yet

- Financial Plan: A. AssumptionsDocument20 pagesFinancial Plan: A. AssumptionsNahiyan MuakhkherNo ratings yet

- Edi Mandor Ari Po 23 00001.vendorDocument1 pageEdi Mandor Ari Po 23 00001.vendorTaufiq Miftahul HudaNo ratings yet

- Nurmala Ahmar - STIE Perbanas Surabaya JMV Mulyadi - Universitas PancasilaDocument12 pagesNurmala Ahmar - STIE Perbanas Surabaya JMV Mulyadi - Universitas PancasilaHafidh NazmiNo ratings yet

- MCQ With AnsDocument68 pagesMCQ With AnsRosemarie Cruz0% (2)

- CV InglesDocument3 pagesCV InglesHernan PNo ratings yet

- CAF 1 IA Autumn 2020Document5 pagesCAF 1 IA Autumn 2020Qasim Hafeez KhokharNo ratings yet

- Ifrs 16 SimulationDocument7 pagesIfrs 16 SimulationSuryadi100% (1)

- Lembar JWB PD ANGKASADocument53 pagesLembar JWB PD ANGKASAernyNo ratings yet

- Chapter 2 Fair Value Measurement IFRS 13Document21 pagesChapter 2 Fair Value Measurement IFRS 13johnegnNo ratings yet

- Acc AnalysisDocument3 pagesAcc AnalysisMd Sifat KhanNo ratings yet

- Luca Pacioli BiographyDocument6 pagesLuca Pacioli BiographyDavid PazmiñoNo ratings yet

- Chapter 1 Test QuestionsDocument3 pagesChapter 1 Test QuestionsRocel NavajaNo ratings yet

- Auditing Questions and AnswerDocument13 pagesAuditing Questions and AnsweryaregalNo ratings yet

- Modal VerbsDocument5 pagesModal VerbsYoha CorreaNo ratings yet

- Group Activity 1Document10 pagesGroup Activity 1Winshei Cagulada0% (1)

- Master UCBDocument18 pagesMaster UCBS KulkarniNo ratings yet

- Reviewer For AccountingDocument7 pagesReviewer For AccountingRoesell Anne EspeletaNo ratings yet

- Management Advisory Services - ReviewDocument14 pagesManagement Advisory Services - ReviewTeofel John Alvizo PantaleonNo ratings yet

- Far Set2 A Basic Reviewer For Financial Accounting and Reporting 1Document6 pagesFar Set2 A Basic Reviewer For Financial Accounting and Reporting 1AShley NIcole0% (1)

- 18bc147k ACA AssignmentDocument22 pages18bc147k ACA AssignmentSuchitraNo ratings yet

- Blank Accounting FormsDocument21 pagesBlank Accounting FormsAdam Zakri100% (1)

- AMITY Business School: Cost Accounting Nupur AgarwalDocument41 pagesAMITY Business School: Cost Accounting Nupur AgarwalNupur AgarwalNo ratings yet

- The Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceFrom EverandThe Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceRating: 4 out of 5 stars4/5 (1)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- Venture Deals: Be Smarter Than Your Lawyer and Venture CapitalistFrom EverandVenture Deals: Be Smarter Than Your Lawyer and Venture CapitalistRating: 4 out of 5 stars4/5 (32)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- The Value of a Whale: On the Illusions of Green CapitalismFrom EverandThe Value of a Whale: On the Illusions of Green CapitalismRating: 5 out of 5 stars5/5 (2)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 5 out of 5 stars5/5 (2)

- Corporate Finance Formulas: A Simple IntroductionFrom EverandCorporate Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsFrom EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNo ratings yet

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 3.5 out of 5 stars3.5/5 (8)

- Risk Management: Concepts and Guidance, Fifth EditionFrom EverandRisk Management: Concepts and Guidance, Fifth EditionRating: 4.5 out of 5 stars4.5/5 (10)

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamFrom EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamNo ratings yet

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (8)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Built, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursFrom EverandBuilt, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursRating: 5 out of 5 stars5/5 (13)

- Data Analysis for Corporate Finance: Building financial models using SQL, Python, and MS PowerBIFrom EverandData Analysis for Corporate Finance: Building financial models using SQL, Python, and MS PowerBINo ratings yet

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (35)