You might also like

- CFAS - Bank ReconciliationDocument5 pagesCFAS - Bank ReconciliationAltessa Lyn ContigaNo ratings yet

- 1.2 Bank Reconciliation and Proof of CashDocument6 pages1.2 Bank Reconciliation and Proof of CashShally Lao-unNo ratings yet

- Lesson 8 - Bank Reconciliation StatementDocument5 pagesLesson 8 - Bank Reconciliation StatementUnknownymousNo ratings yet

- Bank Reconciliation and Proof of CashDocument2 pagesBank Reconciliation and Proof of CashDarwyn HonaNo ratings yet

- Finals ReviewerDocument6 pagesFinals ReviewerMaliha KansiNo ratings yet

- CA5105 - Bank ReconciliationDocument2 pagesCA5105 - Bank ReconciliationczarliseNo ratings yet

- and Highly Liquid Investment Readily Convertible Into CashDocument3 pagesand Highly Liquid Investment Readily Convertible Into CashGirl Lang AkoNo ratings yet

- C2 Bank ReconciliationDocument22 pagesC2 Bank ReconciliationKenzel lawasNo ratings yet

- Module 2 - Bank ReconciliationDocument21 pagesModule 2 - Bank ReconciliationJennalyn S. GanalonNo ratings yet

- M10 TranscriptDocument3 pagesM10 TranscriptJanna RodriguezNo ratings yet

- Bank ReconciliationDocument12 pagesBank ReconciliationJenny Pearl Dominguez CalizarNo ratings yet

- Accounting Lesson 1 Bank Reconciliation NotesDocument9 pagesAccounting Lesson 1 Bank Reconciliation NotesKabelo SefaliNo ratings yet

- FABM REVIEWER 2nd QUARTERDocument5 pagesFABM REVIEWER 2nd QUARTERMikaella Adriana GoNo ratings yet

- CCEDocument4 pagesCCEせい じよNo ratings yet

- Bank Reconciliation StatementDocument4 pagesBank Reconciliation StatementNishi YadavNo ratings yet

- Notes Chapter 6Document2 pagesNotes Chapter 6syafaNo ratings yet

- IA 1 Module Week 3-4Document8 pagesIA 1 Module Week 3-4Yamit, Angel Marie A.No ratings yet

- Bank Reconciliation StatementDocument4 pagesBank Reconciliation StatementArshad BashirNo ratings yet

- Lesson 5Document22 pagesLesson 5PoonamNo ratings yet

- Chapter 2 Bank ReconciliationDocument15 pagesChapter 2 Bank Reconciliation2021315379No ratings yet

- Bank Reconciliation PDFDocument17 pagesBank Reconciliation PDFJamaica IndacNo ratings yet

- Main IdeasDocument7 pagesMain IdeasIsabel Jost SouribioNo ratings yet

- Bank Reconciliation Statement: Fabm 2 Mr. Denver B. BeguiaDocument19 pagesBank Reconciliation Statement: Fabm 2 Mr. Denver B. BeguiaFelice CastroNo ratings yet

- Bank ReconciliationDocument14 pagesBank ReconciliationKoro SenseiNo ratings yet

- (Studocu) Int Acc Chapter 2 - Valix, Robles, Empleo, MillanDocument4 pages(Studocu) Int Acc Chapter 2 - Valix, Robles, Empleo, MillanHufana, ShelleyNo ratings yet

- 12 Abm123Document3 pages12 Abm123Alex EnriquezNo ratings yet

- Sta Clara - Summary Part 1Document49 pagesSta Clara - Summary Part 1Carms St ClaireNo ratings yet

- Bankasdasd Das AsdDocument9 pagesBankasdasd Das AsdRia AthirahNo ratings yet

- 12 Abm123Document3 pages12 Abm123Alex EnriquezNo ratings yet

- BHT1333 Chapter 6Document6 pagesBHT1333 Chapter 6Weiqin ChanNo ratings yet

- Intermediate AccountingDocument2 pagesIntermediate AccountingKylie CortezNo ratings yet

- RetentionDocument4 pagesRetentionPrince PierreNo ratings yet

- FABMDocument3 pagesFABMAlex EnriquezNo ratings yet

- Intac Reviewer 2Document10 pagesIntac Reviewer 2rochelle lagmayNo ratings yet

- Chapter 6 CashDocument15 pagesChapter 6 CashTesfamlak MulatuNo ratings yet

- Intermediate AccountingDocument7 pagesIntermediate Accountingjaninasachadelacruz0119No ratings yet

- Bank ReconDocument23 pagesBank ReconAshley LumbaoNo ratings yet

- Chapter 2 & 3 - Bank Recon and Proof of CashDocument3 pagesChapter 2 & 3 - Bank Recon and Proof of CashAvia Chelsy DeangNo ratings yet

- Bank Reconciliation StatementDocument3 pagesBank Reconciliation StatementRealGenius (Carl)No ratings yet

- 1 Updates LoanDocument7 pages1 Updates LoanFor PurposeNo ratings yet

- Green Aesthetic Thesis Defense Presentation - 20240315 - 171147 - 0000Document49 pagesGreen Aesthetic Thesis Defense Presentation - 20240315 - 171147 - 0000joyce jabileNo ratings yet

- L2 Bank ReconciliationDocument3 pagesL2 Bank ReconciliationAshley BrevaNo ratings yet

- ACTBAS2 - Cash HandoutsDocument2 pagesACTBAS2 - Cash HandoutsAliaJustineIlaganNo ratings yet

- Bank Reconciliation-1Document5 pagesBank Reconciliation-1Chin DyNo ratings yet

- Chapter 6 Controlling CashDocument10 pagesChapter 6 Controlling CashyenewNo ratings yet

- Intermidiate Accounting 1Document3 pagesIntermidiate Accounting 1Melka BelmonteNo ratings yet

- Bank ReconciliationDocument41 pagesBank ReconciliationKarl Mendez100% (2)

- Bank ReconciliationDocument24 pagesBank ReconciliationCyrelle MagpantayNo ratings yet

- Key Terms and Chapter Summary-13Document2 pagesKey Terms and Chapter Summary-13onstudy015No ratings yet

- Bank Reconciliation ReviewerDocument2 pagesBank Reconciliation Reviewerfred ferrera jrNo ratings yet

- 00 Quick Notes - Cash and Cash Equivalents PDFDocument6 pages00 Quick Notes - Cash and Cash Equivalents PDFBecky GonzagaNo ratings yet

- Bank Reconciliation Statement Notes-2Document5 pagesBank Reconciliation Statement Notes-2Joel EastNo ratings yet

- Chapter 2-Chapter 5Document17 pagesChapter 2-Chapter 5Jenn sayongNo ratings yet

- Bank Reconciliation: AccountingtoolsDocument1 pageBank Reconciliation: AccountingtoolsQuenie De la CruzNo ratings yet

- Bank Reconciliations Credit Memo PDF FormatDocument8 pagesBank Reconciliations Credit Memo PDF FormatGeorge MockNo ratings yet

- ACC117 - Chapter 7 - Bank Reconciliation StatementDocument24 pagesACC117 - Chapter 7 - Bank Reconciliation StatementIrah NazirahNo ratings yet

- ACC 102 - Bank ReconciliationDocument3 pagesACC 102 - Bank Reconciliationwerter werterNo ratings yet

- Bank Reconciliation StatementDocument12 pagesBank Reconciliation StatementMuhammad BilalNo ratings yet

- Bank ReconciliationDocument5 pagesBank ReconciliationaizaNo ratings yet

- IA 1 - 1 Cash and Cash EquivalentsDocument7 pagesIA 1 - 1 Cash and Cash EquivalentsVJ MacaspacNo ratings yet

- IA 1 - 5 InventoriesDocument8 pagesIA 1 - 5 InventoriesVJ MacaspacNo ratings yet

- IA 1 - 4 ReceivablesDocument9 pagesIA 1 - 4 ReceivablesVJ MacaspacNo ratings yet

- IA 1 - 3 Proof of CashDocument3 pagesIA 1 - 3 Proof of CashVJ MacaspacNo ratings yet

- CCP402Document17 pagesCCP402api-3849444100% (1)

- Judge Note 138Document83 pagesJudge Note 138Balakrishna GM Gowda50% (2)

- 4 5850544239464682122Document14 pages4 5850544239464682122gemedakebede7No ratings yet

- Banking Case StudiesDocument7 pagesBanking Case StudiesNeeta SharmaNo ratings yet

- Banking and Insurance X PDFDocument196 pagesBanking and Insurance X PDFSahida ParveenNo ratings yet

- QuickBooks SyllabusDocument10 pagesQuickBooks SyllabusNot Going to Argue Jesus is KingNo ratings yet

- Educational Interpreter PoliciesDocument4 pagesEducational Interpreter Policiesapi-356743732No ratings yet

- Negotiable Instruments Law ............................................. 2Document16 pagesNegotiable Instruments Law ............................................. 2Claudine ArrabisNo ratings yet

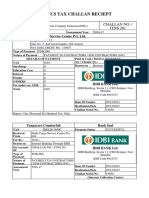

- TDS Challan Nov 15Document243 pagesTDS Challan Nov 15sunilNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument39 pages© The Institute of Chartered Accountants of IndiaGowriNo ratings yet

- HESCO Intern-Ship ReportDocument34 pagesHESCO Intern-Ship ReportHumair Uddin100% (3)

- Austin & Katy Van Wyk: Epicicity!Document2 pagesAustin & Katy Van Wyk: Epicicity!katylinvwNo ratings yet

- SOP - Finance and Accounting DepartmentDocument52 pagesSOP - Finance and Accounting Departmentcoffee Dust100% (20)

- Gov - Uscourts.ca7.14-1682.28.17 RedactedDocument90 pagesGov - Uscourts.ca7.14-1682.28.17 RedactedJ Doe100% (1)

- First Division G.R. NO. 136202, January 25, 2007: Supreme Court of The PhilippinesDocument13 pagesFirst Division G.R. NO. 136202, January 25, 2007: Supreme Court of The PhilippinesGlenelyn AzurinNo ratings yet

- Kunci Jawaban Sistem Informasi AkuntansiDocument63 pagesKunci Jawaban Sistem Informasi AkuntansiAlamsyahHermawan50% (2)

- CustomAccountStatement07 02 2024Document3 pagesCustomAccountStatement07 02 2024bsen51642No ratings yet

- CH 11Document33 pagesCH 11kalidindi_kc_krishnaNo ratings yet

- Keown8 ch17Document30 pagesKeown8 ch17samir249No ratings yet

- SWIFT HandbookDocument121 pagesSWIFT HandbookRichard JoyeNo ratings yet

- Current and Savings Account User Manual 1 PDFDocument772 pagesCurrent and Savings Account User Manual 1 PDFthandayuthapani sundarNo ratings yet

- Internship Report On MCB Bank LTDDocument66 pagesInternship Report On MCB Bank LTDbbaahmad89No ratings yet

- Accounting For Single Entry and Incomplete Records PDFDocument18 pagesAccounting For Single Entry and Incomplete Records PDFCj BarrettoNo ratings yet

- MCIA - Mexico Handbook PDFDocument326 pagesMCIA - Mexico Handbook PDFbillludley_15No ratings yet

- NEGO Week 5 (July 5 and 6)Document3 pagesNEGO Week 5 (July 5 and 6)larcia025No ratings yet

- Tikona Sep 2023Document3 pagesTikona Sep 2023Lalit JainNo ratings yet

- (Formerly Doeacc Centre Calicut) : Code Module Name Duration (29 Feb 2012) (30 May 2012)Document7 pages(Formerly Doeacc Centre Calicut) : Code Module Name Duration (29 Feb 2012) (30 May 2012)vineetsudevNo ratings yet

- Edi Patit Paban Das DetailsDocument11 pagesEdi Patit Paban Das DetailsAnik ChowdhuryNo ratings yet

- Special Penal Laws 2014Document16 pagesSpecial Penal Laws 2014Martin Martel50% (2)

- Albrecht, Albrecht, & Albrecht: Fraud Against OrganizationsDocument18 pagesAlbrecht, Albrecht, & Albrecht: Fraud Against OrganizationsFatimaIjazNo ratings yet