You might also like

- Solution Manual for an Introduction to Equilibrium ThermodynamicsFrom EverandSolution Manual for an Introduction to Equilibrium ThermodynamicsNo ratings yet

- (M-2) Process Costing & Material Pricing Sums 3Document24 pages(M-2) Process Costing & Material Pricing Sums 3Yolo GuyNo ratings yet

- Semiconductor Data Book: Characteristics of approx. 10,000 Transistors, FETs, UJTs, Diodes, Rectifiers, Optical Semiconductors, Triacs and SCRsFrom EverandSemiconductor Data Book: Characteristics of approx. 10,000 Transistors, FETs, UJTs, Diodes, Rectifiers, Optical Semiconductors, Triacs and SCRsNo ratings yet

- (M-2) Job, Batch, Operating Costing 4Document13 pages(M-2) Job, Batch, Operating Costing 4Yolo GuyNo ratings yet

- CP2 - Materials Cost - Updated-1Document61 pagesCP2 - Materials Cost - Updated-1esaiinternalauditNo ratings yet

- Consignment AccountingDocument8 pagesConsignment AccountingKHUSHI MEHTANo ratings yet

- Budgeted Statement ExamDocument11 pagesBudgeted Statement ExamNelz KhoNo ratings yet

- VC/unit 5 Unit Produced 3000 15,000 Times 12 Yung FC/month Kasi Total Cost For The Year Hanap FC Per Month 10,000 12 120,000 135,000 TOTAL COSTDocument7 pagesVC/unit 5 Unit Produced 3000 15,000 Times 12 Yung FC/month Kasi Total Cost For The Year Hanap FC Per Month 10,000 12 120,000 135,000 TOTAL COSTArima KouseiNo ratings yet

- AmitabhDewani 364 ACMADocument3 pagesAmitabhDewani 364 ACMAAyush DewaniNo ratings yet

- (M-5) Budgeting 2Document26 pages(M-5) Budgeting 2Yolo GuyNo ratings yet

- Assignment 04Document8 pagesAssignment 04John MilanNo ratings yet

- CGT Case 6Document4 pagesCGT Case 6Wajih RehmanNo ratings yet

- Process Costing and Joint Product and byDocument4 pagesProcess Costing and Joint Product and byGeetika BhattiNo ratings yet

- Cost AnalysisDocument47 pagesCost AnalysisAkarsh BhattNo ratings yet

- Practical Accounting Problems 2 SolutionsDocument9 pagesPractical Accounting Problems 2 SolutionsJimmyChaoNo ratings yet

- Process A Account: 0 0 Normal Loss 200 Opening InventoryDocument33 pagesProcess A Account: 0 0 Normal Loss 200 Opening InventorySimran JainNo ratings yet

- MA CVP SolutionDocument11 pagesMA CVP SolutionAll in ONENo ratings yet

- Day 4 (My)Document11 pagesDay 4 (My)Jhilmil JeswaniNo ratings yet

- Computation of Effective Quantity of Each Chemical Available For Use Particulars Chemical A (KG.) Chemical B (KG.)Document15 pagesComputation of Effective Quantity of Each Chemical Available For Use Particulars Chemical A (KG.) Chemical B (KG.)Parth VijayNo ratings yet

- ACCA107 MIDTERMS OCT 06 2021 PROBLEMS SOLUTION - Sheet3Document12 pagesACCA107 MIDTERMS OCT 06 2021 PROBLEMS SOLUTION - Sheet3Mary Kate OrobiaNo ratings yet

- BREAK EVEN ANALYSIS by FINANCIAL OTABILDocument28 pagesBREAK EVEN ANALYSIS by FINANCIAL OTABILPrincillaNo ratings yet

- MAC2601-SuggestedsolutionOct November2013Document12 pagesMAC2601-SuggestedsolutionOct November2013DINEO PRUDENCE NONGNo ratings yet

- (Mas) Week1 Solutions ManualDocument17 pages(Mas) Week1 Solutions ManualBeef Testosterone100% (1)

- CP9 - Job CostingDocument11 pagesCP9 - Job CostingesaiinternalauditNo ratings yet

- Dia4a GP 7 Acc2533Document9 pagesDia4a GP 7 Acc2533JapyNo ratings yet

- Or Notes (Unit-V)Document14 pagesOr Notes (Unit-V)Vinayak MishraNo ratings yet

- Process CostingDocument11 pagesProcess CostingSujay SinghviNo ratings yet

- Ex. ProcessDocument2 pagesEx. ProcessMeaadNo ratings yet

- Cost Accounting SolutionsDocument3 pagesCost Accounting Solutionsamitdesai1508No ratings yet

- Cost Sheet (M-I)Document17 pagesCost Sheet (M-I)Yolo GuyNo ratings yet

- Or Notes (Unit-V)Document14 pagesOr Notes (Unit-V)Tanya MalviyaNo ratings yet

- Cost and Revenue An in Depth StudyDocument36 pagesCost and Revenue An in Depth StudyJatin Anand0% (1)

- Process Costing 1Document32 pagesProcess Costing 1errNo ratings yet

- Process Costing Quiz Spoiled UnitsDocument3 pagesProcess Costing Quiz Spoiled UnitsRafael Capunpon VallejosNo ratings yet

- Problem 2-14 Product Cost Sunk Cost Direct LaborDocument8 pagesProblem 2-14 Product Cost Sunk Cost Direct LaborarijitmajeeNo ratings yet

- CostingDocument4 pagesCostingPaulNo ratings yet

- Cutting Dept.: Perusahaan Menggunakan Asumsi Arus Biaya FIFO. Tidak Ada Kerusakan/kehilangan/tambahan Unit DiprosesDocument3 pagesCutting Dept.: Perusahaan Menggunakan Asumsi Arus Biaya FIFO. Tidak Ada Kerusakan/kehilangan/tambahan Unit DiprosesYoelPurba FlashNo ratings yet

- Econmics Concepts With Formula or and UseDocument6 pagesEconmics Concepts With Formula or and UseLuis QuinonesNo ratings yet

- Process CostingDocument5 pagesProcess Costingideasim31996No ratings yet

- A Annual Consumption 0 Cost of Placing Order C Carrying Cost Per UnitDocument8 pagesA Annual Consumption 0 Cost of Placing Order C Carrying Cost Per UnitJaimin PatelNo ratings yet

- Practice Question On Absorption Abc MethodsDocument5 pagesPractice Question On Absorption Abc MethodsAshraf MahabubNo ratings yet

- Varoon FX23031 MA Assignment 3Document4 pagesVaroon FX23031 MA Assignment 3Varoon RNo ratings yet

- Correction TD 5 Nov 2022Document14 pagesCorrection TD 5 Nov 2022chaima smatiNo ratings yet

- The Costs of ProductionDocument23 pagesThe Costs of ProductionJothi BasuNo ratings yet

- Cost Accounting MCQs End TermDocument7 pagesCost Accounting MCQs End TermVineesha GurnaniNo ratings yet

- 1 RO-Quotation For ACDC Solar - 25C EVI Heat Pumpair Conditioner-Victor 07.11.2022Document2 pages1 RO-Quotation For ACDC Solar - 25C EVI Heat Pumpair Conditioner-Victor 07.11.2022oanaNo ratings yet

- Cost & Management AccountingDocument3 pagesCost & Management AccountingAnurag AwasthiNo ratings yet

- (MICROECO) Lesson 4 CostDocument26 pages(MICROECO) Lesson 4 CostCollege Sophomore 2301No ratings yet

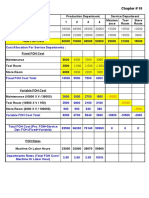

- Chapter # 10Document2 pagesChapter # 10kqandeelNo ratings yet

- Name:: Course: F5 Faculty: Miss Urooj Istaqlal Date: 27 Jan 2021 Class IDDocument5 pagesName:: Course: F5 Faculty: Miss Urooj Istaqlal Date: 27 Jan 2021 Class IDMuhammad AdilNo ratings yet

- Variances Working Sheet CDocument12 pagesVariances Working Sheet CHitesh YadavNo ratings yet

- COSMAN2 Final ExamDocument18 pagesCOSMAN2 Final ExamRIZLE SOGRADIELNo ratings yet

- Materials Price Variance (AP - SP) X AQDocument8 pagesMaterials Price Variance (AP - SP) X AQRIZLE SOGRADIELNo ratings yet

- 3 Nov Cost-Volume - Profit Analysis - QusetionsDocument44 pages3 Nov Cost-Volume - Profit Analysis - QusetionsAbhinavNo ratings yet

- AFAR First Preboard 93 - SolutionsDocument12 pagesAFAR First Preboard 93 - SolutionsEpfie SanchesNo ratings yet

- WK 4 Solutions To Thread Practice ProblemsDocument3 pagesWK 4 Solutions To Thread Practice Problemsmasta4ulskilzNo ratings yet

- Assignment 2 - CMADocument9 pagesAssignment 2 - CMAVivek SharanNo ratings yet

- CVP AnalysisDocument19 pagesCVP Analysissharjeelraja876No ratings yet

- F F A, I %, N P 200,000 F A, 6 %, 20: Methods of Financing and EnterpriseDocument13 pagesF F A, I %, N P 200,000 F A, 6 %, 20: Methods of Financing and Enterprisejung biNo ratings yet

- Pet Products Flow of Production Physical Units DM CCDocument2 pagesPet Products Flow of Production Physical Units DM CCAngelica RoseNo ratings yet

- (M-5) Budgeting 2Document26 pages(M-5) Budgeting 2Yolo GuyNo ratings yet

- Cost Sheet (M-I)Document17 pagesCost Sheet (M-I)Yolo GuyNo ratings yet

- (M-4) - Marginal Costing & CVP Analysis Formulas 2Document2 pages(M-4) - Marginal Costing & CVP Analysis Formulas 2Yolo GuyNo ratings yet

- EVS Module 3Document37 pagesEVS Module 3Yolo GuyNo ratings yet

- EVS Module 4Document71 pagesEVS Module 4Yolo GuyNo ratings yet

- Business Accountancy Module 1Document49 pagesBusiness Accountancy Module 1Yolo Guy100% (1)

- EVS Module 5Document32 pagesEVS Module 5Yolo GuyNo ratings yet

- Behavioral Science - Case StudyDocument3 pagesBehavioral Science - Case StudyYolo GuyNo ratings yet

- MRTP and Competition Act 2002Document12 pagesMRTP and Competition Act 2002Yolo GuyNo ratings yet

- My Bank StatementDocument3 pagesMy Bank StatementAnji DudigamNo ratings yet

- 108 Questions & Answers On Mutu - Yadnya InvestmentsDocument202 pages108 Questions & Answers On Mutu - Yadnya Investmentsk praNo ratings yet

- 2013-14 - Agha Jahanzeb - Trade-Off Theory, Pecking Order Theory and Market Timing Theory A Comprehensive Review of Capital Structure Theories-94Document8 pages2013-14 - Agha Jahanzeb - Trade-Off Theory, Pecking Order Theory and Market Timing Theory A Comprehensive Review of Capital Structure Theories-94Nicol Escobar HerreraNo ratings yet

- GFM Stacking OrderDocument1 pageGFM Stacking Orderapi-3822695No ratings yet

- BRIC Investing ReportDocument12 pagesBRIC Investing ReportSonia CorrealeNo ratings yet

- Test Bank For Finance Applications and Theory 4th Edition Marcia Cornett Troy Adair John NofsingerDocument43 pagesTest Bank For Finance Applications and Theory 4th Edition Marcia Cornett Troy Adair John Nofsingerjennifervaughnpzcygfixrs100% (21)

- (MB0053) International Business ManagementDocument14 pages(MB0053) International Business ManagementAjay KumarNo ratings yet

- The Development of Financial Markets in The Philippines and Its Interaction With Monetary Policy and Financial StabilityDocument27 pagesThe Development of Financial Markets in The Philippines and Its Interaction With Monetary Policy and Financial Stabilitylei dcNo ratings yet

- Performance Analysis of Top 5 Banks in India HDFC Sbi Icici Axis Idbi by SatishpgoyalDocument72 pagesPerformance Analysis of Top 5 Banks in India HDFC Sbi Icici Axis Idbi by SatishpgoyalSatish P.Goyal71% (17)

- Gold Price Suppression: The Hidden TruthDocument2 pagesGold Price Suppression: The Hidden TruthRon RobinsNo ratings yet

- BOKU Billing and Payments ProcessDocument11 pagesBOKU Billing and Payments ProcessAfc DeetweeNo ratings yet

- Case Semi FinalDocument5 pagesCase Semi FinalHanna CruzNo ratings yet

- IftDocument3 pagesIftNavneet SinghNo ratings yet

- Stock Market Awareness Among School Students in Selected DistrictsDocument10 pagesStock Market Awareness Among School Students in Selected DistrictsnandhinislvrjNo ratings yet

- Capital BudgetingDocument65 pagesCapital Budgetingarjunmba119624No ratings yet

- Sergei Fedotov: 20912 - Introduction To Financial MathematicsDocument27 pagesSergei Fedotov: 20912 - Introduction To Financial MathematicsaqszaqszNo ratings yet

- Sample Final Solutions PDFDocument10 pagesSample Final Solutions PDFrealdmanNo ratings yet

- High Probability Setups - Phantom PDFDocument1 pageHigh Probability Setups - Phantom PDFSteven Hard100% (1)

- Foriegn Exchange MarketDocument22 pagesForiegn Exchange MarketDebopam BanerjeeNo ratings yet

- Assignment: Fin 441 Bank ManagementDocument11 pagesAssignment: Fin 441 Bank ManagementNazir Ahmed ZihadNo ratings yet

- "Trade Finance": A Summer Training Project Report OnDocument5 pages"Trade Finance": A Summer Training Project Report OnSudarshan RaviNo ratings yet

- Nism Viii Equity Derivative Short NotesDocument24 pagesNism Viii Equity Derivative Short Notesshivamsahu890No ratings yet

- Syllabus Course 1: Global Financial Markets and AssetsDocument12 pagesSyllabus Course 1: Global Financial Markets and AssetsFerNo ratings yet

- Acctg Principles and ConceptsDocument25 pagesAcctg Principles and ConceptsAdelyn Dizon50% (2)

- IAMv3 Individual Sample Reports PDFDocument23 pagesIAMv3 Individual Sample Reports PDFAnonymous xv5fUs4AvNo ratings yet

- Cushman & Wakefield - International Investment Atlas - 2014 MarchDocument28 pagesCushman & Wakefield - International Investment Atlas - 2014 MarchRidi YusfandrikNo ratings yet

- GBM Round Table Seminars PresentationDocument40 pagesGBM Round Table Seminars PresentationUpendra ChoudharyNo ratings yet

- Financial MarketDocument83 pagesFinancial Marketkembobwana100% (1)

- Chapter 5Document10 pagesChapter 5Patrick Earl T. PintacNo ratings yet

- Investment Decision Criteria (PAF)Document32 pagesInvestment Decision Criteria (PAF)VinayGolchhaNo ratings yet