You might also like

- Acctg 201 - Assignment 2Document11 pagesAcctg 201 - Assignment 2sarahbee75% (4)

- Acca106 Midterms ExaminationDocument20 pagesAcca106 Midterms ExaminationNicole Anne Santiago SibuloNo ratings yet

- Dry Cleaning Home Delivery Business PlanDocument39 pagesDry Cleaning Home Delivery Business PlanDivya AggarwalNo ratings yet

- F5 AbcDocument20 pagesF5 AbcMazni HanisahNo ratings yet

- Chapter 3 Solutions Comm 305Document77 pagesChapter 3 Solutions Comm 305Maketh.ManNo ratings yet

- Cost Accounting & Control Midterm ExaminationDocument7 pagesCost Accounting & Control Midterm ExaminationFerb CruzadaNo ratings yet

- Advance Account II MCQ FinalbsisjshDocument33 pagesAdvance Account II MCQ FinalbsisjshPranit Pandit100% (1)

- Final Examination Cost Accounting 2019 FinalDocument6 pagesFinal Examination Cost Accounting 2019 FinalElias DeusNo ratings yet

- Absorption Variable CostingDocument22 pagesAbsorption Variable CostingAaron ArellanoNo ratings yet

- Activity Based Costing Notes and ExerciseDocument6 pagesActivity Based Costing Notes and Exercisefrancis MagobaNo ratings yet

- Intervention ManDocument47 pagesIntervention ManFrederick GbliNo ratings yet

- Meaning of Cost Sheet:: SampleDocument16 pagesMeaning of Cost Sheet:: SampleSunil Shekhar NayakNo ratings yet

- Mid TermDocument7 pagesMid Termpdmallari12No ratings yet

- Tungach LTD Make and Sell A Single Product Demand ForDocument2 pagesTungach LTD Make and Sell A Single Product Demand ForAmit PandeyNo ratings yet

- MGT IssuesDocument22 pagesMGT IssuesaleeshatenetNo ratings yet

- Cost Analysis - Fast Moving Consumer Durables Industry: Group 8Document10 pagesCost Analysis - Fast Moving Consumer Durables Industry: Group 8Saurabh SinghNo ratings yet

- Mas Theories 2018Document18 pagesMas Theories 2018Suzette VillalinoNo ratings yet

- Mas Theories 2018Document18 pagesMas Theories 2018Suzette VillalinoNo ratings yet

- BhaDocument25 pagesBharishu jainNo ratings yet

- ACC103 Assignment January 2019 IntakeDocument8 pagesACC103 Assignment January 2019 IntakeReina TrầnNo ratings yet

- Accounting For Manufacturing OperationsDocument49 pagesAccounting For Manufacturing Operationsgab mNo ratings yet

- 3 Classroom-ExercisesDocument4 pages3 Classroom-ExercisesNikko Bowie PascualNo ratings yet

- Process CostingDocument18 pagesProcess CostingCheliah Mae ImperialNo ratings yet

- Advanced Management Accounting Assignment 20200001Document7 pagesAdvanced Management Accounting Assignment 20200001Sandra K JereNo ratings yet

- (A) Imputed Cost (B) Capitalised Cost (PCC N Ov 09 - 2 Marks)Document2 pages(A) Imputed Cost (B) Capitalised Cost (PCC N Ov 09 - 2 Marks)avtaranNo ratings yet

- Cost Must DoDocument198 pagesCost Must DoVanshika BhedaNo ratings yet

- University of Caloocan City Cost Accounting & Control Midterm ExaminationDocument8 pagesUniversity of Caloocan City Cost Accounting & Control Midterm ExaminationAlexandra Nicole IsaacNo ratings yet

- Acca106 Midterm Exam 1st20212022 KeyDocument28 pagesAcca106 Midterm Exam 1st20212022 KeyNicole Anne Santiago SibuloNo ratings yet

- LQ2 Set B PDFDocument5 pagesLQ2 Set B PDFCharles TuazonNo ratings yet

- BBMC 1113 Management Accounting: Distinguish Between A "Prime Cost" and A "Production Overheads Cost"Document2 pagesBBMC 1113 Management Accounting: Distinguish Between A "Prime Cost" and A "Production Overheads Cost"王宇璇No ratings yet

- Valuation of Inventories: Accounting Standard (AS) 2Document8 pagesValuation of Inventories: Accounting Standard (AS) 2ncxmNo ratings yet

- CA Assignment No. 5 Part 1 ABC and Joint CostingDocument15 pagesCA Assignment No. 5 Part 1 ABC and Joint CostingMethlyNo ratings yet

- معايير Ch 2 InventoriesDocument11 pagesمعايير Ch 2 InventoriesHamza MahmoudNo ratings yet

- Mas 02 - Variable Absorption Costing & BudgetingDocument11 pagesMas 02 - Variable Absorption Costing & BudgetingCriane DomineusNo ratings yet

- Cost ManagementDocument5 pagesCost Managementels emsNo ratings yet

- Accounting Standard (AS) 2 Valuation of InventoriesDocument6 pagesAccounting Standard (AS) 2 Valuation of InventoriesRajNo ratings yet

- LMSDocument4 pagesLMSJohn Carlo LorenzoNo ratings yet

- Chapt Vii. Depreciation DisposalsDocument61 pagesChapt Vii. Depreciation DisposalsAlty StelleNo ratings yet

- Part A: Managerial Accounting Assessment - ACC720 - March 2020Document4 pagesPart A: Managerial Accounting Assessment - ACC720 - March 2020Helmy YusoffNo ratings yet

- Cagayan State University - AndrewsDocument4 pagesCagayan State University - AndrewsWynie AreolaNo ratings yet

- Acc 213 3e Q2Document6 pagesAcc 213 3e Q2Rogel Dolino67% (3)

- Cost Accounting - Quiz 1Document5 pagesCost Accounting - Quiz 1alexissosing.cpaNo ratings yet

- As 02Document14 pagesAs 02Dipak UgaleNo ratings yet

- KA SET A Cost PrelimsDocument16 pagesKA SET A Cost PrelimsGeozelle BenitoNo ratings yet

- PM Sunway Test July-Sept 2023 PTDocument11 pagesPM Sunway Test July-Sept 2023 PTFarahAin FainNo ratings yet

- Answer Key Bacostmx-3tay2021-Finals Quiz 2Document8 pagesAnswer Key Bacostmx-3tay2021-Finals Quiz 2Marjorie Nepomuceno100% (1)

- SCM Assignment Activity Sept 20 2020 Answer Key PDF FreeDocument5 pagesSCM Assignment Activity Sept 20 2020 Answer Key PDF FreeChizu ChizuNo ratings yet

- @cahelp23 - Inter Costing Must Do List Nov2021Document120 pages@cahelp23 - Inter Costing Must Do List Nov2021bnanduriNo ratings yet

- Lecture 1Document7 pagesLecture 1HarusiNo ratings yet

- Asi Mba 162 4 Sma 140917Document6 pagesAsi Mba 162 4 Sma 140917Danah Dela RosaNo ratings yet

- Saint Theresa College of Tandag, Inc. Tandag City Strategic Cost Management - Summer Class Dit 1Document4 pagesSaint Theresa College of Tandag, Inc. Tandag City Strategic Cost Management - Summer Class Dit 1Esheikell ChenNo ratings yet

- Intermediate Group II Test Papers (Revised July 2009)Document55 pagesIntermediate Group II Test Papers (Revised July 2009)Sumit AroraNo ratings yet

- BAJA SAEINDIA Cost Guidelines 2021Document4 pagesBAJA SAEINDIA Cost Guidelines 2021Siva DanusNo ratings yet

- III Job Order CostingDocument66 pagesIII Job Order CostingJoshuaGuerrero0% (1)

- Handout 4 - Job Order Costing PDFDocument11 pagesHandout 4 - Job Order Costing PDFKurt CaneroNo ratings yet

- Cost AccountingDocument9 pagesCost AccountingCyndy VillapandoNo ratings yet

- Principles of Cost AccountingDocument28 pagesPrinciples of Cost AccountingNin WaramNo ratings yet

- Practical Guide To Production Planning & Control [Revised Edition]From EverandPractical Guide To Production Planning & Control [Revised Edition]Rating: 1 out of 5 stars1/5 (1)

- A Study of the Supply Chain and Financial Parameters of a Small BusinessFrom EverandA Study of the Supply Chain and Financial Parameters of a Small BusinessNo ratings yet

- Beyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkFrom EverandBeyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkNo ratings yet

- Make It! The Engineering Manufacturing Solution: Engineering the Manufacturing SolutionFrom EverandMake It! The Engineering Manufacturing Solution: Engineering the Manufacturing SolutionNo ratings yet

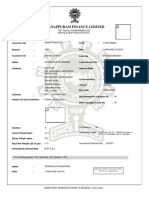

- Manappuram Finance Limited: SR - NoDocument5 pagesManappuram Finance Limited: SR - NoKiran GolwadNo ratings yet

- Manappuram Finance Limited: SR - NoDocument5 pagesManappuram Finance Limited: SR - NoKiran GolwadNo ratings yet

- CAS2 RevisedDocument4 pagesCAS2 RevisedBHUSHAN DahaleNo ratings yet

- Ogl 347901676355685668 PDFDocument5 pagesOgl 347901676355685668 PDFBHUSHAN DahaleNo ratings yet

- Manappuram Finance Limited: SR - NoDocument5 pagesManappuram Finance Limited: SR - NoKiran GolwadNo ratings yet

- Assignment No 5 Economics PerspectiveDocument3 pagesAssignment No 5 Economics PerspectiveheyNo ratings yet

- Course OL TaxationDocument3 pagesCourse OL TaxationSayed Mukhtar HedayatNo ratings yet

- Lecture 3 Job Order CostingDocument20 pagesLecture 3 Job Order CostingTheresa RoqueNo ratings yet

- Declarations-: (Signature & Stamp of The Buyer)Document3 pagesDeclarations-: (Signature & Stamp of The Buyer)akakakshanNo ratings yet

- SBR Mock 1 Sep 23 TGDocument7 pagesSBR Mock 1 Sep 23 TGAkshita BhartiyaNo ratings yet

- Unit-III Time Study (Work Measurement) Time Study: DefinitionsDocument15 pagesUnit-III Time Study (Work Measurement) Time Study: DefinitionsAbhishek AruaNo ratings yet

- Analisis Penentuan Harga Jual Apartemen - CompressDocument14 pagesAnalisis Penentuan Harga Jual Apartemen - Compressriko andreanNo ratings yet

- RIPARODocument1 pageRIPAROPEA CHRISTINE AZURIASNo ratings yet

- SbaDocument4 pagesSbaahyenn cabello100% (1)

- Chapter 1 Mcqs On Income Tax Rates and Basic Concept of Income TaxDocument27 pagesChapter 1 Mcqs On Income Tax Rates and Basic Concept of Income TaxSatheesh KannaNo ratings yet

- Module 5-Variable and Absorption CostingDocument13 pagesModule 5-Variable and Absorption CostingAna ValenovaNo ratings yet

- Audit of Shareholders' Equity - July 22, 2021Document35 pagesAudit of Shareholders' Equity - July 22, 2021Kathrina RoxasNo ratings yet

- Statement of Realization and LiquidationDocument2 pagesStatement of Realization and LiquidationSherilyn BunagNo ratings yet

- Limni CoDocument3 pagesLimni CoDavid Jung ThapaNo ratings yet

- Portfolio Theory and The Capital Asset Pricing Model: Answers To Problem SetsDocument18 pagesPortfolio Theory and The Capital Asset Pricing Model: Answers To Problem SetsShyamal VermaNo ratings yet

- IDCloudHost - Invoice #158341 PDFDocument2 pagesIDCloudHost - Invoice #158341 PDFQorthonyNo ratings yet

- Excise Tax SummaryDocument40 pagesExcise Tax SummaryHeva AbsalonNo ratings yet

- Global Strategic AlliancesDocument40 pagesGlobal Strategic AlliancesDhruv AroraNo ratings yet

- Invoice - 2021-01-05T150251.353Document1 pageInvoice - 2021-01-05T150251.353mib_santoshNo ratings yet

- Assignment 2 GuidanceDocument4 pagesAssignment 2 GuidanceNguyễn AnNo ratings yet

- Belay Tayure Fruit and Vegetables Business PlanDocument24 pagesBelay Tayure Fruit and Vegetables Business Plangemechu75% (8)

- Chapter 2 PDFDocument11 pagesChapter 2 PDFTú NguyễnNo ratings yet

- Chapter 3Document11 pagesChapter 3Arun Kumar SatapathyNo ratings yet

- Evidencia 3: Ensayo "Free Trade Agreement (FTA) : Advantages and Disadvantages"Document4 pagesEvidencia 3: Ensayo "Free Trade Agreement (FTA) : Advantages and Disadvantages"jesus david franco barriosNo ratings yet

- Ghana Investment Promotion Centre (Gipc) Act 865Document19 pagesGhana Investment Promotion Centre (Gipc) Act 865JeffreyNo ratings yet

- Google Finance Investment TrackerDocument13 pagesGoogle Finance Investment TrackerSwaraj NayseNo ratings yet

- Indian Public Finance Statistics 2017-18Document101 pagesIndian Public Finance Statistics 2017-18Priyansh ShrivastavNo ratings yet

- Index Dashboard: Broad Market IndicesDocument2 pagesIndex Dashboard: Broad Market IndicesVagaram ChowdharyNo ratings yet

![Practical Guide To Production Planning & Control [Revised Edition]](https://imgv2-2-f.scribdassets.com/img/word_document/235162742/149x198/2a816df8c8/1709920378?v=1)