You might also like

- SpiceJet - ICICIDocument6 pagesSpiceJet - ICICIKrishna ChennaiNo ratings yet

- Refer To The Data For Rijo Equipment Repair Corp inDocument2 pagesRefer To The Data For Rijo Equipment Repair Corp inMiroslav Gegoski0% (1)

- This Receipt Shall Be Valid For Five (5) Years From The Date of The Permit To UseDocument1 pageThis Receipt Shall Be Valid For Five (5) Years From The Date of The Permit To UseIsabela FINo ratings yet

- Paytm Q4 FY 2023 Revised Earnings Release INRDocument20 pagesPaytm Q4 FY 2023 Revised Earnings Release INRPranav TalrejaNo ratings yet

- DownloadDocument3 pagesDownloadVenkatesh VenkateshNo ratings yet

- Financial Results and Guidance: As of July 29, 2020Document5 pagesFinancial Results and Guidance: As of July 29, 2020Bin WuNo ratings yet

- Dilip Buildcon Q3FY18 - Result Update - Axis Direct - 20022018 - 20!02!2018 - 16Document6 pagesDilip Buildcon Q3FY18 - Result Update - Axis Direct - 20022018 - 20!02!2018 - 16MiteshNo ratings yet

- Gabriel India Investor Presentation Q3 2022Document49 pagesGabriel India Investor Presentation Q3 2022Renato AlvesNo ratings yet

- Block 2Q22 Shareholder LetterDocument34 pagesBlock 2Q22 Shareholder LetterTim MooreNo ratings yet

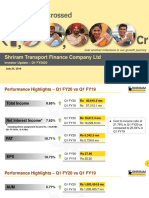

- Shriram Transport Q1 FY20 PresentationDocument18 pagesShriram Transport Q1 FY20 PresentationVenkata Reddy KNo ratings yet

- Relife (Competitive, Financial and User Engagement)Document14 pagesRelife (Competitive, Financial and User Engagement)fitri nurul kamilaNo ratings yet

- S Chand and Company (SCHAND IN) : Q4FY20 Result UpdateDocument6 pagesS Chand and Company (SCHAND IN) : Q4FY20 Result UpdateRaj PrakashNo ratings yet

- ITC AnalysisDocument7 pagesITC AnalysisPRASHANT ARORANo ratings yet

- Money and The MythDocument2 pagesMoney and The MythVanshica SahniNo ratings yet

- TTK Prestige 2022Document3 pagesTTK Prestige 2022aribamirza870No ratings yet

- HCL Tech q2 2021 Investor ReleaseDocument28 pagesHCL Tech q2 2021 Investor ReleasePramod GuptaNo ratings yet

- Paytm Q2 FY24 Earnings Release INRDocument18 pagesPaytm Q2 FY24 Earnings Release INRshaik rafiNo ratings yet

- Earnings Update Q1FY22Document15 pagesEarnings Update Q1FY22sai mohanNo ratings yet

- SHri FY21Document25 pagesSHri FY2153crx1fnocNo ratings yet

- Tax Rate Calculation and WACC for SignifyDocument9 pagesTax Rate Calculation and WACC for SignifyShivam GoelNo ratings yet

- Financial Statement AnalysisDocument23 pagesFinancial Statement AnalysisFeMakes MusicNo ratings yet

- Prodaja Po KvartalimaDocument2 pagesProdaja Po KvartalimaDuško PetrovićNo ratings yet

- Britannia Annual Report Performance and Operations HighlightsDocument17 pagesBritannia Annual Report Performance and Operations HighlightsajthebestNo ratings yet

- Financial Analysis of Asian PaintsDocument7 pagesFinancial Analysis of Asian PaintsMONIKA YADAVNo ratings yet

- Financial Analysis Reveals Asian Paints' Strong GrowthDocument7 pagesFinancial Analysis Reveals Asian Paints' Strong GrowthRohit SinghNo ratings yet

- Punjab Debt Bulletin Dec 2016Document4 pagesPunjab Debt Bulletin Dec 2016Saqib JoyiaNo ratings yet

- Economic Indicators of PakistanDocument4 pagesEconomic Indicators of PakistanhellosaadyNo ratings yet

- SHri 9M FY22Document27 pagesSHri 9M FY2253crx1fnocNo ratings yet

- Shareholder-Letter Block 1Q23Document32 pagesShareholder-Letter Block 1Q23Tim MooreNo ratings yet

- HCL Tech Q1 FY23 Investor ReleaseDocument25 pagesHCL Tech Q1 FY23 Investor ReleasedeepeshNo ratings yet

- HCL Tech Q4 FY22 Investor ReleaseDocument25 pagesHCL Tech Q4 FY22 Investor ReleaseNddd NnbNo ratings yet

- State of Pakistan Economy 1Document22 pagesState of Pakistan Economy 1kqsqNo ratings yet

- Financial ResultsDocument56 pagesFinancial ResultsoverkillNo ratings yet

- KNR Constructions: Execution Momentum To SustainDocument12 pagesKNR Constructions: Execution Momentum To SustainRishabh RanaNo ratings yet

- HCL Tech q3 2019 Investor ReleaseDocument23 pagesHCL Tech q3 2019 Investor ReleaseVarun SidanaNo ratings yet

- 2022 Ogdensburg City Budget SummaryDocument8 pages2022 Ogdensburg City Budget SummaryAshley MarieNo ratings yet

- DownloadDocument22 pagesDownloadAshwani KesharwaniNo ratings yet

- EdgeReport YESBANK ConcallAnalysis 30-04-2022 233Document2 pagesEdgeReport YESBANK ConcallAnalysis 30-04-2022 233prashant_natureNo ratings yet

- S Chand and Company (SCHAND IN) : Q3FY20 Result UpdateDocument6 pagesS Chand and Company (SCHAND IN) : Q3FY20 Result UpdateanjugaduNo ratings yet

- HCL Tech Q3 FY22 Investor ReleaseDocument28 pagesHCL Tech Q3 FY22 Investor Releaseashokdb2kNo ratings yet

- AUBANK ConcallAnalysis 19 01 2023 548Document2 pagesAUBANK ConcallAnalysis 19 01 2023 548Muni AwasthiNo ratings yet

- Investor Release For December 31, 2016 (Company Update)Document10 pagesInvestor Release For December 31, 2016 (Company Update)Shyam SunderNo ratings yet

- PC - Engineers India 4Q21Document8 pagesPC - Engineers India 4Q21Sandesh ShettyNo ratings yet

- Economics Evaluation SpreadsheetDocument4 pagesEconomics Evaluation SpreadsheetTemitope BelloNo ratings yet

- Infosys LTD 774.60: Nse: InfyDocument5 pagesInfosys LTD 774.60: Nse: InfybezirksvorNo ratings yet

- Dharamsi Morarjee Presentation Feb 2022Document8 pagesDharamsi Morarjee Presentation Feb 2022Puneet367No ratings yet

- Mutual Fund Industry Factbook 1668362398Document134 pagesMutual Fund Industry Factbook 1668362398Hitesh GuptaaNo ratings yet

- Q223 HP Inc Earnings SummaryDocument1 pageQ223 HP Inc Earnings Summarynicolas SpritzerNo ratings yet

- NESTLE 2017-18 Annual Report AnalysisDocument6 pagesNESTLE 2017-18 Annual Report AnalysisAamil Rafi KhanNo ratings yet

- Bangladesh National Budget Review 2018-19Document45 pagesBangladesh National Budget Review 2018-19Shamim Parvez DurjoyNo ratings yet

- BOB Result-FY 2022Document6 pagesBOB Result-FY 2022Ashutosh JaiswalNo ratings yet

- Golden Stocks PortfolioDocument6 pagesGolden Stocks PortfoliocompangelNo ratings yet

- Pakistan 2022Document2 pagesPakistan 2022Burhan UddinNo ratings yet

- WIPRO 2021-22 Annual Report AnalysisDocument60 pagesWIPRO 2021-22 Annual Report AnalysisShanmuganayagam RNo ratings yet

- Asumsi: Kamar Laku Selama 26 Hari Dari 30 Hari: - I0 + I1/ (1+r) + I2/ (1+r) 2 + I3/ (1+r) 3 + .+ In/ (1+r) NDocument4 pagesAsumsi: Kamar Laku Selama 26 Hari Dari 30 Hari: - I0 + I1/ (1+r) + I2/ (1+r) 2 + I3/ (1+r) 3 + .+ In/ (1+r) NAdis IsmailNo ratings yet

- UNION BUDGET 2023 ANALYSIS OF DIRECT TAX PROPOSALSDocument54 pagesUNION BUDGET 2023 ANALYSIS OF DIRECT TAX PROPOSALSCharul ChhajerNo ratings yet

- Vedanta Financial AnalysisDocument4 pagesVedanta Financial AnalysisShikhar AroraNo ratings yet

- India: 2022 Annual Research: Key HighlightsDocument2 pagesIndia: 2022 Annual Research: Key Highlightsbeautyera2023No ratings yet

- From The Desk of Business Head and CIO - January 2019: Mr. Prateek AgrawalDocument4 pagesFrom The Desk of Business Head and CIO - January 2019: Mr. Prateek AgrawalAshwin HasyagarNo ratings yet

- Dalmia Cement (DALCEM) : Higher Expenditure Dents MarginDocument6 pagesDalmia Cement (DALCEM) : Higher Expenditure Dents Marginjass200910No ratings yet

- Irving Budget Update 2010-07-07Document22 pagesIrving Budget Update 2010-07-07Irving BlogNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific-Seventh EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific-Seventh EditionNo ratings yet

- Wedding Card-1 PDFDocument4 pagesWedding Card-1 PDFVenky VenkyNo ratings yet

- Resume 1Document2 pagesResume 1Venky VenkyNo ratings yet

- Dismissal Order Singamaneni, Harsha Vardhan (206765)Document2 pagesDismissal Order Singamaneni, Harsha Vardhan (206765)Venky VenkyNo ratings yet

- Water Softener Quotation for Rs. 81315Document1 pageWater Softener Quotation for Rs. 81315Venky VenkyNo ratings yet

- Resume 1Document2 pagesResume 1Venky VenkyNo ratings yet

- Resume35 PDFDocument2 pagesResume35 PDFVenky VenkyNo ratings yet

- Kadechur Banashankar - Latest - UpdatedDocument4 pagesKadechur Banashankar - Latest - UpdatedVenky VenkyNo ratings yet

- Time Series Week2 SessionFlowDocument21 pagesTime Series Week2 SessionFlowVenky VenkyNo ratings yet

- Preventing Corruption in Public Finance Management: A Practical GuideDocument46 pagesPreventing Corruption in Public Finance Management: A Practical GuideBernardo EncinasNo ratings yet

- W4-Module Income Tax On CorporationDocument18 pagesW4-Module Income Tax On CorporationShiela TanglaoNo ratings yet

- Chapt-5 Exclude From Gross IncomeDocument4 pagesChapt-5 Exclude From Gross IncomehumnarviosNo ratings yet

- TCS employee payslip April 2014Document1 pageTCS employee payslip April 2014BalajiNo ratings yet

- Itr VDocument1 pageItr VcachandhiranNo ratings yet

- Bharat Sanchar Nigam Limited: Telephone Bill Name and Address of The CustomerDocument1 pageBharat Sanchar Nigam Limited: Telephone Bill Name and Address of The CustomerVijaya ChandNo ratings yet

- IEPDocument50 pagesIEPK.muniNo ratings yet

- Gross IncomeDocument33 pagesGross IncomeRey ViloriaNo ratings yet

- CA Inter DT Revision LecturesDocument119 pagesCA Inter DT Revision LecturesJerrin JoseNo ratings yet

- DT-Revision Chart (Ec.263 - 264) by CA Vijay SardaDocument1 pageDT-Revision Chart (Ec.263 - 264) by CA Vijay Sardapooja4040100% (1)

- MSA 2 - Taxation NotesDocument19 pagesMSA 2 - Taxation NotesadilfarooqaNo ratings yet

- Succession and Estate Tax ConceptsDocument3 pagesSuccession and Estate Tax ConceptsKim Cristian MaañoNo ratings yet

- Income Tax Syllabus Rev. August 4 2022Document23 pagesIncome Tax Syllabus Rev. August 4 2022Nezer VergaraNo ratings yet

- Year Long BillDocument3 pagesYear Long BillKewal GuglaniNo ratings yet

- TDS on Final Dividend 2021-22Document24 pagesTDS on Final Dividend 2021-22ajeshtnNo ratings yet

- Chap 6 Relief and RebateDocument15 pagesChap 6 Relief and RebateKelvin OngNo ratings yet

- Assignment-KMBN FM02-III-Shaleen Suneja-2022-23Document2 pagesAssignment-KMBN FM02-III-Shaleen Suneja-2022-23Vivek SharmaNo ratings yet

- Transfer and Business Tax 2014 Ballada PDFDocument26 pagesTransfer and Business Tax 2014 Ballada PDFCamzwell Kleinne HalyieNo ratings yet

- EFFORTS BY-Ravleen Kaur Roll No-01391101818Document8 pagesEFFORTS BY-Ravleen Kaur Roll No-01391101818Harleen KaurNo ratings yet

- Historical Development of Taxing System in IndiaDocument17 pagesHistorical Development of Taxing System in IndiasenthamilanNo ratings yet

- Invoice for medical suppliesDocument1 pageInvoice for medical suppliesIramNo ratings yet

- Summary PEFA Report-2020Document40 pagesSummary PEFA Report-2020Victor ShabaniNo ratings yet

- What is Finance? Understanding the Key ConceptsDocument19 pagesWhat is Finance? Understanding the Key ConceptsArmilyn Jean CastonesNo ratings yet

- Payslip For March 2023 - TORM ARAWA (Closed Payroll) : Torm A/S Torm A/SDocument1 pagePayslip For March 2023 - TORM ARAWA (Closed Payroll) : Torm A/S Torm A/SRodelio TomasNo ratings yet

- PUBLIC FINANCE PrivatizationDocument16 pagesPUBLIC FINANCE PrivatizationZek Ruzaini100% (1)

- Preliminary Assessment NoticeDocument3 pagesPreliminary Assessment NoticeHanabishi RekkaNo ratings yet

- Form 16 TDS CertificateDocument2 pagesForm 16 TDS CertificateRanjeet RajputNo ratings yet

- August 2022 Payslip for Sean Derrick BlancoDocument1 pageAugust 2022 Payslip for Sean Derrick BlancoSean Derrick BlancoNo ratings yet