You might also like

- Cabin Operations Safety Best Practices Guide: Buy OnlineDocument25 pagesCabin Operations Safety Best Practices Guide: Buy OnlineLuis HernandezNo ratings yet

- Ancient Egypt and Kush: Holt McdougalDocument45 pagesAncient Egypt and Kush: Holt McdougalLuis Hernandez100% (1)

- Sindi and Wahab in 18th CenturyDocument9 pagesSindi and Wahab in 18th CenturyMujahid Asaadullah AbdullahNo ratings yet

- Efe and Ife Matrix: Institute of Business and TechnologyDocument10 pagesEfe and Ife Matrix: Institute of Business and TechnologyAsim Baig100% (2)

- Valuation Methods and Shareholder Value CreationFrom EverandValuation Methods and Shareholder Value CreationRating: 4.5 out of 5 stars4.5/5 (3)

- From Philo To Plotinus AftermanDocument21 pagesFrom Philo To Plotinus AftermanRaphael888No ratings yet

- Theories of International InvestmentDocument2 pagesTheories of International InvestmentSamish DhakalNo ratings yet

- Fusion Implementing Offerings Using Functional Setup Manager PDFDocument51 pagesFusion Implementing Offerings Using Functional Setup Manager PDFSrinivasa Rao Asuru0% (1)

- 5 Perfo Per Tof Bel NorDocument23 pages5 Perfo Per Tof Bel NorLuis HernandezNo ratings yet

- Plaza 66 Tower 2 Structural Design ChallengesDocument13 pagesPlaza 66 Tower 2 Structural Design ChallengessrvshNo ratings yet

- DC 7 BrochureDocument4 pagesDC 7 Brochures_a_r_r_yNo ratings yet

- Annual Report PSCDocument27 pagesAnnual Report PSCEmoxie X - Stabyielz100% (1)

- Functional DesignDocument17 pagesFunctional DesignRajivSharmaNo ratings yet

- The Economic Outlook For The U.S. and The Construction IndustryDocument23 pagesThe Economic Outlook For The U.S. and The Construction IndustryLuis Eduardo NaranjoNo ratings yet

- Class 9Document4 pagesClass 9vroommNo ratings yet

- Spicejet LTD.: October 22 October 22, 2010Document37 pagesSpicejet LTD.: October 22 October 22, 2010sunilpachisiaNo ratings yet

- Airtran Airways - 2009: A. Case AbstractDocument13 pagesAirtran Airways - 2009: A. Case AbstractShayan RehmanNo ratings yet

- Cost Awareness - TrainingDocument39 pagesCost Awareness - TrainingtongsabaiNo ratings yet

- APM Automotive Holdings Berhad: Riding On Motor Sector's Growth Cycle - 29/7/2010Document7 pagesAPM Automotive Holdings Berhad: Riding On Motor Sector's Growth Cycle - 29/7/2010Rhb InvestNo ratings yet

- Veto SwitchgearsDocument44 pagesVeto Switchgearssingh66222No ratings yet

- Tofas Turk Otomobil Fabri 02 25 2024Document6 pagesTofas Turk Otomobil Fabri 02 25 2024Mehmet Emre AYDEMİRNo ratings yet

- MediaRing AR04Document68 pagesMediaRing AR04Karan Henrik PonnuduraiNo ratings yet

- Sampa Video SpreadsheetDocument4 pagesSampa Video SpreadsheetVarsha ShirsatNo ratings yet

- Drug Discovery & Development For The World Market From India: How RealDocument20 pagesDrug Discovery & Development For The World Market From India: How RealRicky TiwariNo ratings yet

- GP PetroleumsDocument44 pagesGP Petroleumssingh66222No ratings yet

- Runoff Ratio MethodDocument5 pagesRunoff Ratio Methodmaria sol fernandezNo ratings yet

- Annual Review of HSE PerformanceDocument20 pagesAnnual Review of HSE PerformanceRakawy Bin RakNo ratings yet

- Misr Chemical Industries - 10 January 2012Document25 pagesMisr Chemical Industries - 10 January 2012Mona ElShazlyNo ratings yet

- Final PPT 4 April JetBlueDocument43 pagesFinal PPT 4 April JetBlueNii Ben100% (1)

- Sampa Video Solution Harvard Case Solution 1Document10 pagesSampa Video Solution Harvard Case Solution 1Héctor SilvaNo ratings yet

- Boeing Current Market Outlook 2009 To 2028Document30 pagesBoeing Current Market Outlook 2009 To 2028Jijoo Jacob VargheseNo ratings yet

- Asset Management Companies: Date: 20 February, 2020Document34 pagesAsset Management Companies: Date: 20 February, 2020Ikp IkpNo ratings yet

- Crude Oil SourDocument48 pagesCrude Oil SourhkaruvathilNo ratings yet

- Whirlpool Europe Spreadsheet Supplement TVI 1Document6 pagesWhirlpool Europe Spreadsheet Supplement TVI 1Mousumi GuhaNo ratings yet

- Lrdi V101017Document11 pagesLrdi V101017ANAMIKA SHARMANo ratings yet

- Piaggio Group 2010-2013: Investor DayDocument11 pagesPiaggio Group 2010-2013: Investor DayAlok MishraNo ratings yet

- Analysis of Finacial Statemtent.: Submitted To: Sir Yousuf AbdiDocument14 pagesAnalysis of Finacial Statemtent.: Submitted To: Sir Yousuf Abdidara001No ratings yet

- Annualreport1d10 PDFDocument99 pagesAnnualreport1d10 PDFnat1asha-1No ratings yet

- Motherson Sumi Systems LTD.: May 22, 2015 Volume No. 1 Issue No. 19Document7 pagesMotherson Sumi Systems LTD.: May 22, 2015 Volume No. 1 Issue No. 19nitishNo ratings yet

- Apollo Global Management - APO - Stock Price - Live Quote - Historical Chart 2022 FebDocument6 pagesApollo Global Management - APO - Stock Price - Live Quote - Historical Chart 2022 FebhelloNo ratings yet

- Basic Assumptions: Particulars ($000) 2001 2002 E 2003 EDocument7 pagesBasic Assumptions: Particulars ($000) 2001 2002 E 2003 EMuskan ValbaniNo ratings yet

- A Project On "Economic Value Added" in Kirloskar Oil Engines LTDDocument19 pagesA Project On "Economic Value Added" in Kirloskar Oil Engines LTDPrayag GokhaleNo ratings yet

- Airfinance Journal Roundtable Summit: The Future of Engine TechnologyDocument37 pagesAirfinance Journal Roundtable Summit: The Future of Engine TechnologyliuhkNo ratings yet

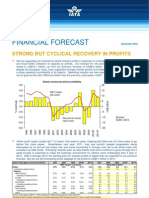

- Financial Forecast: Strong But Cyclical Recovery in ProfitsDocument4 pagesFinancial Forecast: Strong But Cyclical Recovery in ProfitsDaniel WongNo ratings yet

- Case Study - LÓrealDocument4 pagesCase Study - LÓrealAndrea BrozosNo ratings yet

- LIT FactsheetDocument2 pagesLIT FactsheetAlex MilarNo ratings yet

- Case Prepared By: Corey Daigle, Seth Fraser, and Megan ForemanDocument42 pagesCase Prepared By: Corey Daigle, Seth Fraser, and Megan ForemanChanrithy SokNo ratings yet

- Stock Buyback: Presented by Pushan Sharma Ruchi Gupta Sashank ShahDocument26 pagesStock Buyback: Presented by Pushan Sharma Ruchi Gupta Sashank Shahruchi070186No ratings yet

- Yemen: Aidfortrade at A Glance 2017Document2 pagesYemen: Aidfortrade at A Glance 2017Rami Al-SabriNo ratings yet

- Market OutlookDocument31 pagesMarket OutlookwilmerNo ratings yet

- C1 Sampa VideoDocument2 pagesC1 Sampa VideoBharadwaja ReddyNo ratings yet

- XAT 2011 Question Paper and Ans KeyDocument32 pagesXAT 2011 Question Paper and Ans Keyvikram_bansal_5No ratings yet

- 9h Tata SteelDocument11 pages9h Tata SteelManan AgarwalNo ratings yet

- Amy Kakuk, Beth Theriault, and Jessica BourgoinDocument47 pagesAmy Kakuk, Beth Theriault, and Jessica BourgoinmarioNo ratings yet

- AMOREPACIFIC GROUP 3Q20 EN VFDocument7 pagesAMOREPACIFIC GROUP 3Q20 EN VFbui dinh thaoNo ratings yet

- Docshare - Tips - Sampa Video Solution Harvard Case Solution PDFDocument10 pagesDocshare - Tips - Sampa Video Solution Harvard Case Solution PDFnimarNo ratings yet

- Ind-Swift LabsDocument44 pagesInd-Swift Labssingh66222No ratings yet

- Assignment 1 - AirlineDocument16 pagesAssignment 1 - AirlineArthur GodderisNo ratings yet

- Fidelity Asian Bonds Fact Sheet PDFDocument3 pagesFidelity Asian Bonds Fact Sheet PDFSebastian BauschNo ratings yet

- Aviation Strategy in The Last DecadeDocument24 pagesAviation Strategy in The Last DecadeFilippo CapitanioNo ratings yet

- Trend Analysis of Noon Sugar Mills LTDDocument10 pagesTrend Analysis of Noon Sugar Mills LTDJawwad KhanNo ratings yet

- JBM Auto (Q2FY21 Result Update)Document7 pagesJBM Auto (Q2FY21 Result Update)krippuNo ratings yet

- Case Prepared By: Corey Daigle, Seth Fraser, and Megan ForemanDocument42 pagesCase Prepared By: Corey Daigle, Seth Fraser, and Megan ForemanPrashant NarulaNo ratings yet

- Apple WaccDocument3 pagesApple WaccMaira Ahmad0% (2)

- Ratio Analysis: Pakistan State OilDocument19 pagesRatio Analysis: Pakistan State OilMUHAMMAD MUDASSAR TAHIR NCBA&ENo ratings yet

- Financial Analysis of Fauji Cement LTDDocument27 pagesFinancial Analysis of Fauji Cement LTDMBA...KIDNo ratings yet

- Financial Crisis: Project Designed by Subhayu Das (IILM BS) KOLDocument14 pagesFinancial Crisis: Project Designed by Subhayu Das (IILM BS) KOLshuvayumicrobioNo ratings yet

- Corporate Finance ProjectDocument7 pagesCorporate Finance ProjectAbhinav Akash SinghNo ratings yet

- EDCP Presentation BY SS, SAILDocument40 pagesEDCP Presentation BY SS, SAILLove DeepNo ratings yet

- Using Aspect-Oriented Programming for Trustworthy Software DevelopmentFrom EverandUsing Aspect-Oriented Programming for Trustworthy Software DevelopmentRating: 3 out of 5 stars3/5 (1)

- ADM Notre DameDocument25 pagesADM Notre DameLuis HernandezNo ratings yet

- Agha Rahim - Defense AttachmentDocument30 pagesAgha Rahim - Defense AttachmentLuis HernandezNo ratings yet

- Va-Spa-703-1 v2 B Tuupi Efb Rakenduste KasDocument4 pagesVa-Spa-703-1 v2 B Tuupi Efb Rakenduste KasLuis HernandezNo ratings yet

- Sphi/Cix Chiclayo, Peru: Komla 1A (Koml1A) Rnav Arrival (RWY 19)Document24 pagesSphi/Cix Chiclayo, Peru: Komla 1A (Koml1A) Rnav Arrival (RWY 19)Luis HernandezNo ratings yet

- APS MCC Competencies PosterDocument1 pageAPS MCC Competencies PosterLuis HernandezNo ratings yet

- Electronic Flight Bag (Efb) Policy and Guidance: Peter Skaves, Federal Aviation Administration, Washington, DCDocument11 pagesElectronic Flight Bag (Efb) Policy and Guidance: Peter Skaves, Federal Aviation Administration, Washington, DCLuis HernandezNo ratings yet

- Aircraft Performance Database DH8DDocument1 pageAircraft Performance Database DH8DLuis HernandezNo ratings yet

- AUPRTA Rev3 - TabletDocument116 pagesAUPRTA Rev3 - TabletLuis HernandezNo ratings yet

- "History Is More or Less Bunk." - Henry Ford Rats Multiply So Quickly That in 18 Months, Two Rats Could Have Over One Million DescendantsDocument104 pages"History Is More or Less Bunk." - Henry Ford Rats Multiply So Quickly That in 18 Months, Two Rats Could Have Over One Million DescendantsLuis HernandezNo ratings yet

- TrueNoord in Aircraft Commerce May 2017Document10 pagesTrueNoord in Aircraft Commerce May 2017Luis HernandezNo ratings yet

- Europe: Aircraft Analysis Aircraft Analysis & Fleet PlanningDocument1 pageEurope: Aircraft Analysis Aircraft Analysis & Fleet PlanningLuis HernandezNo ratings yet

- Bounce Recovery - Rejected Landing: Tool KitDocument3 pagesBounce Recovery - Rejected Landing: Tool KitLuis HernandezNo ratings yet

- Runway Excursions: Tool KitDocument4 pagesRunway Excursions: Tool KitLuis HernandezNo ratings yet

- Terrain-Avoidance (Pull-Up) Maneuver: Tool KitDocument4 pagesTerrain-Avoidance (Pull-Up) Maneuver: Tool KitLuis HernandezNo ratings yet

- Carob-Tree As CO2 Sink in The Carbon MarketDocument5 pagesCarob-Tree As CO2 Sink in The Carbon MarketFayssal KartobiNo ratings yet

- Essay Rough Draft 19Document9 pagesEssay Rough Draft 19api-549246767No ratings yet

- Dialogue Au Restaurant, Clients Et ServeurDocument9 pagesDialogue Au Restaurant, Clients Et ServeurbanuNo ratings yet

- Science7 - q1 - Mod3 - Distinguishing Mixtures From Substances - v5Document25 pagesScience7 - q1 - Mod3 - Distinguishing Mixtures From Substances - v5Bella BalendresNo ratings yet

- ReadmeDocument3 pagesReadmedhgdhdjhsNo ratings yet

- Duavent Drug Study - CunadoDocument3 pagesDuavent Drug Study - CunadoLexa Moreene Cu�adoNo ratings yet

- School of Mathematics 2021 Semester 1 MAT1841 Continuous Mathematics For Computer Science Assignment 1Document2 pagesSchool of Mathematics 2021 Semester 1 MAT1841 Continuous Mathematics For Computer Science Assignment 1STEM Education Vung TauNo ratings yet

- Hdfs Default XML ParametersDocument14 pagesHdfs Default XML ParametersVinod BihalNo ratings yet

- Activity # 1 (DRRR)Document2 pagesActivity # 1 (DRRR)Juliana Xyrelle FutalanNo ratings yet

- DPSD ProjectDocument30 pagesDPSD ProjectSri NidhiNo ratings yet

- Gods Omnipresence in The World On Possible MeaninDocument20 pagesGods Omnipresence in The World On Possible MeaninJoan Amanci Casas MuñozNo ratings yet

- 74HC00D 74HC00D 74HC00D 74HC00D: CMOS Digital Integrated Circuits Silicon MonolithicDocument8 pages74HC00D 74HC00D 74HC00D 74HC00D: CMOS Digital Integrated Circuits Silicon MonolithicAssistec TecNo ratings yet

- Proceeding of Rasce 2015Document245 pagesProceeding of Rasce 2015Alex ChristopherNo ratings yet

- Emea 119948060Document31 pagesEmea 119948060ASHUTOSH MISHRANo ratings yet

- Chapter13 PDFDocument34 pagesChapter13 PDFAnastasia BulavinovNo ratings yet

- UTP Student Industrial ReportDocument50 pagesUTP Student Industrial ReportAnwar HalimNo ratings yet

- Introduction-: Microprocessor 68000Document13 pagesIntroduction-: Microprocessor 68000margyaNo ratings yet

- LetrasDocument9 pagesLetrasMaricielo Angeline Vilca QuispeNo ratings yet

- Application Activity Based Costing (Abc) System As An Alternative For Improving Accuracy of Production CostDocument19 pagesApplication Activity Based Costing (Abc) System As An Alternative For Improving Accuracy of Production CostM Agus SudrajatNo ratings yet

- Marketing FinalDocument15 pagesMarketing FinalveronicaNo ratings yet

- Ito Na Talaga Yung FinalDocument22 pagesIto Na Talaga Yung FinalJonas Gian Miguel MadarangNo ratings yet

- BNF Pos - StockmockDocument14 pagesBNF Pos - StockmockSatish KumarNo ratings yet

- The JHipster Mini Book 2Document129 pagesThe JHipster Mini Book 2tyulist100% (1)