You might also like

- Wells Fargo Everyday CheckingDocument6 pagesWells Fargo Everyday CheckingAnny LorenzoNo ratings yet

- hw1 AnsDocument7 pageshw1 AnsMingyanNo ratings yet

- Actuarial Notation: AnnuitiesDocument12 pagesActuarial Notation: AnnuitiesCallum Thain BlackNo ratings yet

- Anual 1Document18 pagesAnual 1Gussyck Agus PsicologistaNo ratings yet

- ICSE ROBOMATE MATH - Compressed-1-17Document17 pagesICSE ROBOMATE MATH - Compressed-1-17Suvadip SanyalNo ratings yet

- Financial Management 1Document20 pagesFinancial Management 1Sriram_VNo ratings yet

- Simple and Compound Interest: Concept of Time and Value OfmoneyDocument11 pagesSimple and Compound Interest: Concept of Time and Value OfmoneyUnzila AtiqNo ratings yet

- General Mathematics 2nd Quarter LectureDocument9 pagesGeneral Mathematics 2nd Quarter LectureSakamoto MiraiNo ratings yet

- Simple Debt AmortizationDocument4 pagesSimple Debt AmortizationAmer IbrahimNo ratings yet

- AnnuityDocument52 pagesAnnuityGoldey Fetalvero MalabananNo ratings yet

- Afb Formula + Qs ShortDocument112 pagesAfb Formula + Qs ShortGursharan BrarNo ratings yet

- Banking Extra PracticeDocument17 pagesBanking Extra PracticeSubham PatiNo ratings yet

- Maths Chap 2 BankingDocument13 pagesMaths Chap 2 BankingBikramjit MajumdarNo ratings yet

- Nvrwx5ura - g11 2q 4m 1-4d - Simple and Compound InterestDocument24 pagesNvrwx5ura - g11 2q 4m 1-4d - Simple and Compound InterestZoe Caga-ananNo ratings yet

- FINANCIAL MANAGEMENT Assgn No.1Document10 pagesFINANCIAL MANAGEMENT Assgn No.1Sachin ChaudharyNo ratings yet

- Lecture 2 Financial ArithmeticDocument23 pagesLecture 2 Financial ArithmeticmaxNo ratings yet

- Compound InterestDocument20 pagesCompound InterestKarla Anexine ValenciaNo ratings yet

- Money Amp Amp BankingDocument15 pagesMoney Amp Amp BankingMaxim IgoshinNo ratings yet

- Unit 3 Financial MathDocument13 pagesUnit 3 Financial Math0805640No ratings yet

- What's More: Quarter 2 - Module 7: Deferred AnnuityDocument4 pagesWhat's More: Quarter 2 - Module 7: Deferred AnnuityChelsea NicoleNo ratings yet

- The Role of Time Value of Money in Project AppraisalDocument15 pagesThe Role of Time Value of Money in Project AppraisalsilvanokanuNo ratings yet

- Chapter 5 BASIC LT FINANCIAL CONCEPTDocument3 pagesChapter 5 BASIC LT FINANCIAL CONCEPTAiron Bendaña50% (2)

- Solutions To End-Of-Chapter ProblemsDocument24 pagesSolutions To End-Of-Chapter ProblemsNabila AhmedNo ratings yet

- Math 11 Gen Math Q2-Week 3Document20 pagesMath 11 Gen Math Q2-Week 3Eloisa MadrilenoNo ratings yet

- QMB Interest (English)Document7 pagesQMB Interest (English)nokulungahlatshwayo40No ratings yet

- Eco Lec 9-13Document5 pagesEco Lec 9-13Lorman MaylasNo ratings yet

- Skinning FundsDocument12 pagesSkinning FundsNehemia T MasiyaziNo ratings yet

- Time Value of Money-1Document70 pagesTime Value of Money-1Archana SinghNo ratings yet

- Calculating Different Types of AnnuitiesDocument5 pagesCalculating Different Types of Annuitiesjc casordNo ratings yet

- Midterm RevisionDocument27 pagesMidterm RevisionTrang CaoNo ratings yet

- The Time Value of Money - Annuities and Other TopicsDocument78 pagesThe Time Value of Money - Annuities and Other TopicsTaqiya NadiyaNo ratings yet

- Time Value of MoneyDocument24 pagesTime Value of MoneyShoaib Ahmed (Lecturer-EE)No ratings yet

- Time Value of MoneyDocument55 pagesTime Value of MoneySayoni GhoshNo ratings yet

- Lesson 11 9.2 Compound Interest Future ValueDocument7 pagesLesson 11 9.2 Compound Interest Future ValueSandro SerdiñaNo ratings yet

- Purana 66666666Document1 pagePurana 66666666APKNo ratings yet

- Assignment On Math Solution: Submitted ToDocument11 pagesAssignment On Math Solution: Submitted ToJoy ChowdhuryNo ratings yet

- FM AnswersDocument4 pagesFM AnswersGamer zoneNo ratings yet

- BA 2802 - Principles of Finance Solutions To Problems For Recitation #2Document10 pagesBA 2802 - Principles of Finance Solutions To Problems For Recitation #2Eda Nur EvginNo ratings yet

- Lec11 Amortized Loans Homework SolutionsDocument3 pagesLec11 Amortized Loans Homework SolutionsJerickson MauricioNo ratings yet

- FM I Chapter 3Document12 pagesFM I Chapter 3mearghaile4No ratings yet

- Week 012-Presentation Key Concepts of Simple and Compound Interests, and Simple and General Annuities - Part 002Document18 pagesWeek 012-Presentation Key Concepts of Simple and Compound Interests, and Simple and General Annuities - Part 002Alleona EmbolodeNo ratings yet

- CFVG - IDBV - 1 - Time Value of Money ExerciseDocument6 pagesCFVG - IDBV - 1 - Time Value of Money ExerciseThu Thủy ĐỗNo ratings yet

- Module 02 TimeValueofMoneyDocument6 pagesModule 02 TimeValueofMoneyjean barrettoNo ratings yet

- Concept of Compound Interest.Document32 pagesConcept of Compound Interest.ScribdTranslationsNo ratings yet

- Mortgage and AmmortizationDocument10 pagesMortgage and AmmortizationMisty BartolomeNo ratings yet

- Sanchez, Gian Emmanuelle R. CE21S2 Compound Interest More Than One Period Per Year Group 2Document4 pagesSanchez, Gian Emmanuelle R. CE21S2 Compound Interest More Than One Period Per Year Group 2Gian SanchezNo ratings yet

- Engineering Economy LectureDocument16 pagesEngineering Economy LectureEphraim RamosNo ratings yet

- Fin118 Unit 9Document25 pagesFin118 Unit 9ayadi_ezer6795No ratings yet

- Time Value of MoneyDocument29 pagesTime Value of Moneyrohan angelNo ratings yet

- 8B Financial Mathematics (B)Document17 pages8B Financial Mathematics (B)enn ennNo ratings yet

- 1 Business Mathemetics - AFB Module-ADocument22 pages1 Business Mathemetics - AFB Module-Awaste mailNo ratings yet

- General Mathematics, Quarter 2, Week 4Document8 pagesGeneral Mathematics, Quarter 2, Week 4Jehl T DuranNo ratings yet

- CH 2Document35 pagesCH 2Mick MalickNo ratings yet

- Genmath Q2 W1-8Document60 pagesGenmath Q2 W1-8lui yangyangNo ratings yet

- S.I and C.IDocument16 pagesS.I and C.IMumtazAhmad100% (1)

- Financial Mathematics Lecture Notes Fina PDFDocument71 pagesFinancial Mathematics Lecture Notes Fina PDFTram HoNo ratings yet

- Chapter 3 Time Value of Money PDFDocument16 pagesChapter 3 Time Value of Money PDFmuluken walelgnNo ratings yet

- 06 - Time Value of Money - 2Document77 pages06 - Time Value of Money - 2Salsabila AufaNo ratings yet

- Chapter 4. The Time Value of Money and Discounted Cash Flow AnalysisDocument15 pagesChapter 4. The Time Value of Money and Discounted Cash Flow Analysisw4termel0n33No ratings yet

- Time Value SolnDocument34 pagesTime Value SolnAlim Ahmed Ansari100% (1)

- Deffered AnnuityDocument23 pagesDeffered AnnuityBryanHarold BrooNo ratings yet

- Unit Test-3 (Types of Plan)Document3 pagesUnit Test-3 (Types of Plan)Gemini PatelNo ratings yet

- Prova Do 2º Ano Present Continuous 3º BiDocument2 pagesProva Do 2º Ano Present Continuous 3º BiRaphael RodriguesNo ratings yet

- Ibs JLN Maktab, KL SC 1 31/01/23Document1 pageIbs JLN Maktab, KL SC 1 31/01/23faezahNo ratings yet

- Q2. Business and Consumer LoansDocument22 pagesQ2. Business and Consumer LoansCassy RabangNo ratings yet

- Bank Statement 1 Fusionn 1 PDFDocument6 pagesBank Statement 1 Fusionn 1 PDFBenny BerniceNo ratings yet

- Account Statement UnlockedDocument12 pagesAccount Statement UnlockedDeepeNo ratings yet

- 100+ Netflix Hits 3.02.2024Document6 pages100+ Netflix Hits 3.02.2024mestt3739No ratings yet

- Creditreport 1561319714905 PDFDocument38 pagesCreditreport 1561319714905 PDFMustaffa ShabazzNo ratings yet

- CIBIL Score 737: Raj Roshan KumarDocument3 pagesCIBIL Score 737: Raj Roshan Kumarrajroshang6No ratings yet

- EPS Pension Calculator NewDocument7 pagesEPS Pension Calculator NewpswaminathanNo ratings yet

- Annual StatementDocument1 pageAnnual StatementFerdee FerdNo ratings yet

- PPF - Short NotesDocument1 pagePPF - Short NotesPoorani SundaresanNo ratings yet

- City Union BankDocument1 pageCity Union BankRaja RajaNo ratings yet

- EMI Calculator - Prepayment OptionDocument15 pagesEMI Calculator - Prepayment OptionPrateekSorteNo ratings yet

- Ibs Bachok SC 1 28/02/23Document4 pagesIbs Bachok SC 1 28/02/23Sabariah MansoorNo ratings yet

- Cyber Boost Proclamation No 907 2015 Public Servants Pension AmendmentDocument8 pagesCyber Boost Proclamation No 907 2015 Public Servants Pension AmendmentaddisNo ratings yet

- Lecture-11 Compound Interest)Document2 pagesLecture-11 Compound Interest)Aditya SahaNo ratings yet

- This Is A System-Generated Statement. Hence, It Does Not Require Any SignatureDocument16 pagesThis Is A System-Generated Statement. Hence, It Does Not Require Any SignatureVinod DharavathNo ratings yet

- PDF Document 28B77D7A8A5D 1Document4 pagesPDF Document 28B77D7A8A5D 1Dan ZinoNo ratings yet

- FA19-BCS-152 Suleman SohailDocument5 pagesFA19-BCS-152 Suleman SohailNew Age Electronics OfficialNo ratings yet

- F D Bond GeneraterDocument1 pageF D Bond GeneraterJayprakash VermaNo ratings yet

- Ty WVTPG6 FP 8 X SUBeDocument6 pagesTy WVTPG6 FP 8 X SUBeashish marwahNo ratings yet

- Statement May 23 XXXXXXXX6585Document4 pagesStatement May 23 XXXXXXXX6585Simanta GamerNo ratings yet

- Account Statement 01 May 2023-21 Aug 2023Document10 pagesAccount Statement 01 May 2023-21 Aug 2023PRONAB MAJHINo ratings yet

- Varo Bank StatementDocument2 pagesVaro Bank StatementlexxyNo ratings yet

- Highlights of Proposed Ability-To-Repay RulesDocument3 pagesHighlights of Proposed Ability-To-Repay RulesForeclosure FraudNo ratings yet

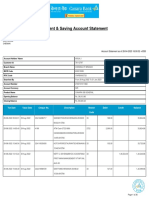

- Current & Saving Account Statement: Arun J Plot No 366 13Th Street Astalakshmi Nagar 3Rd Main RD Alapakkam ChennaiDocument26 pagesCurrent & Saving Account Statement: Arun J Plot No 366 13Th Street Astalakshmi Nagar 3Rd Main RD Alapakkam ChennaiArun Jayaprakash NarayananNo ratings yet

- 7819 10122023120043 UnlockedDocument2 pages7819 10122023120043 Unlockedsubham1hewNo ratings yet