You might also like

- Principles of Cash Flow Valuation: An Integrated Market-Based ApproachFrom EverandPrinciples of Cash Flow Valuation: An Integrated Market-Based ApproachRating: 3 out of 5 stars3/5 (3)

- Momo Operating Report 2Q20Document5 pagesMomo Operating Report 2Q20Wong Kai WenNo ratings yet

- Common Size Income Statement ExcelDocument4 pagesCommon Size Income Statement ExceljobsgrandNo ratings yet

- Common Size Income Statement Excel TemplateDocument5 pagesCommon Size Income Statement Excel TemplateStrwbrrsncigNo ratings yet

- Manappuram Finance Investor PresentationDocument43 pagesManappuram Finance Investor PresentationabmahendruNo ratings yet

- Investor Update For December 31, 2016 (Company Update)Document17 pagesInvestor Update For December 31, 2016 (Company Update)Shyam SunderNo ratings yet

- Hemas Holdings PLC (HHL SL: LKR 69.00) : BRS Quarterly Results Snapshot - Q4 FY 19Document4 pagesHemas Holdings PLC (HHL SL: LKR 69.00) : BRS Quarterly Results Snapshot - Q4 FY 19Sudheera IndrajithNo ratings yet

- Analyst Presentation and Fact Sheet - Q4 FY14Document21 pagesAnalyst Presentation and Fact Sheet - Q4 FY14indpubg0611No ratings yet

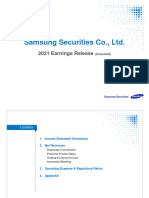

- SamsungSecIR 4Q21 Eng FinalDocument16 pagesSamsungSecIR 4Q21 Eng FinalHardik SharmaNo ratings yet

- Purchases / Average Payables Revenue / Average Total AssetsDocument7 pagesPurchases / Average Payables Revenue / Average Total AssetstannuNo ratings yet

- Ambev Tabelas 4TRI16Document82 pagesAmbev Tabelas 4TRI16Deyverson CostaNo ratings yet

- Ashok Leyland Kotak 050218Document4 pagesAshok Leyland Kotak 050218suprabhattNo ratings yet

- Word Note The Body Shop International PLC 2001: An Introduction To Financial ModelingDocument9 pagesWord Note The Body Shop International PLC 2001: An Introduction To Financial Modelingalka murarka100% (2)

- 637957201521149984_Godrej Consumer Products Result Update - Q1FY23Document4 pages637957201521149984_Godrej Consumer Products Result Update - Q1FY23Prity KumariNo ratings yet

- Greenply Industries Ltd. - Result Presentation Q2H1 FY 2019Document21 pagesGreenply Industries Ltd. - Result Presentation Q2H1 FY 2019Peter MichaleNo ratings yet

- Q3FY21 Result Update Axis Bank: Towards End of Peak Credit Cost CycleDocument12 pagesQ3FY21 Result Update Axis Bank: Towards End of Peak Credit Cost CycleSAGAR VAZIRANINo ratings yet

- ABEV3 TabelasER 1t16yyyyyyyDocument38 pagesABEV3 TabelasER 1t16yyyyyyyitalo.cheiNo ratings yet

- Financial Results Briefing Material For FY2019: April 1, 2018 To March 31, 2019Document30 pagesFinancial Results Briefing Material For FY2019: April 1, 2018 To March 31, 2019choiand1No ratings yet

- Task 1 BigTech TemplateDocument5 pagesTask 1 BigTech Templatedaniyalansari.8425No ratings yet

- Colgate Ratio Analysis WSM 2020 SolvedDocument17 pagesColgate Ratio Analysis WSM 2020 Solvedabi habudinNo ratings yet

- Saito Solar ExcelDocument5 pagesSaito Solar ExcelArjun NairNo ratings yet

- Analyst Presentation and Factsheet - Q4 FY16Document17 pagesAnalyst Presentation and Factsheet - Q4 FY16indpubg0611No ratings yet

- Colgate Financial Model SolvedDocument36 pagesColgate Financial Model SolvedSundara MoorthyNo ratings yet

- 2023-07-27-PH-E-PGOLDDocument6 pages2023-07-27-PH-E-PGOLDexcA1996No ratings yet

- 22 2Q Earning Release of LGEDocument18 pages22 2Q Earning Release of LGEThảo VũNo ratings yet

- ModelDocument103 pagesModelMatheus Augusto Campos PiresNo ratings yet

- Financial Model - Colgate Palmolive (Unsolved Template) : Prepared by Dheeraj Vaidya, CFA, FRMDocument35 pagesFinancial Model - Colgate Palmolive (Unsolved Template) : Prepared by Dheeraj Vaidya, CFA, FRMahmad syaifudinNo ratings yet

- %sales Discount %yoy 18.5% 22.5% 1.8%Document2 pages%sales Discount %yoy 18.5% 22.5% 1.8%Linh NguyenNo ratings yet

- Osotspa Public Company Limited: Q4'18 and FY18 Management Discussion & AnalysisDocument7 pagesOsotspa Public Company Limited: Q4'18 and FY18 Management Discussion & AnalysisEcho WackoNo ratings yet

- Beginner EBay DCFDocument14 pagesBeginner EBay DCFQazi Mohd TahaNo ratings yet

- Apollo Hospitals Enterprise Limited NSEI APOLLOHOSP FinancialsDocument40 pagesApollo Hospitals Enterprise Limited NSEI APOLLOHOSP Financialsakumar4uNo ratings yet

- Ratio Analysis of Colgate PalmoliveDocument19 pagesRatio Analysis of Colgate Palmolivewan nur anisahNo ratings yet

- V-Guard-Industries - Q4 FY21-Results-PresentationDocument17 pagesV-Guard-Industries - Q4 FY21-Results-PresentationanooppattazhyNo ratings yet

- 22 3Q Earning Release of LGEDocument18 pages22 3Q Earning Release of LGEIgnacio ElliotNo ratings yet

- Pag BankDocument24 pagesPag Bankandre.torresNo ratings yet

- Financial Analysis: ITC Ltd. Ticker: ITC: Prepared By: EdualphaDocument13 pagesFinancial Analysis: ITC Ltd. Ticker: ITC: Prepared By: EdualphaParas LodayaNo ratings yet

- Class Exercise Fashion Company Three Statements Model - CompletedDocument16 pagesClass Exercise Fashion Company Three Statements Model - CompletedbobNo ratings yet

- Copy of Data Analytics in Excel_WorkbookDocument88 pagesCopy of Data Analytics in Excel_Workbookjeenmarie2017No ratings yet

- Dixon InvestorPresentationJan2022Document12 pagesDixon InvestorPresentationJan2022raguramrNo ratings yet

- Financial-Model CaseDocument20 pagesFinancial-Model CasecoukslyneNo ratings yet

- Investors - Presentation - 11-02-2021 Low MarginDocument32 pagesInvestors - Presentation - 11-02-2021 Low Marginravi.youNo ratings yet

- Quarterly Update Q4FY20: Visaka Industries LTDDocument10 pagesQuarterly Update Q4FY20: Visaka Industries LTDsherwinmitraNo ratings yet

- JFC 1Q21 earnings dragged by one-off tax adjustment below estimatesDocument10 pagesJFC 1Q21 earnings dragged by one-off tax adjustment below estimatesJajahinaNo ratings yet

- Revised ModelDocument27 pagesRevised ModelAnonymous 0CbF7xaNo ratings yet

- Lenovo Intergration Plan Annual 2004 PresentationDocument26 pagesLenovo Intergration Plan Annual 2004 PresentationKelvin Lim Wei LiangNo ratings yet

- Ratio Analysis Model - Colgate PalmoliveDocument18 pagesRatio Analysis Model - Colgate PalmoliveAkshataNo ratings yet

- IIFL Wealth Q4 and FY21 Performance Update SummaryDocument21 pagesIIFL Wealth Q4 and FY21 Performance Update SummaryRohan RautelaNo ratings yet

- Tech Mahindra Valuation Report FY21 Equity Inv CIA3Document5 pagesTech Mahindra Valuation Report FY21 Equity Inv CIA3safwan hosainNo ratings yet

- Gymboree LBO Model ComDocument7 pagesGymboree LBO Model ComrolandsudhofNo ratings yet

- StoneCo ER 2Q23Document28 pagesStoneCo ER 2Q23Andre TorresNo ratings yet

- Keppel Pacific Oak US REIT Financial StatementsDocument155 pagesKeppel Pacific Oak US REIT Financial StatementsAakashNo ratings yet

- 2022.07.24 - DCF Tutorial Answer KeyDocument18 pages2022.07.24 - DCF Tutorial Answer KeySrikanth ReddyNo ratings yet

- Evercore Partners 8.6.13 PDFDocument6 pagesEvercore Partners 8.6.13 PDFChad Thayer VNo ratings yet

- Q1FY22 Result Update City Union Bank LTD: Beat On Operational Front Due To Lower Credit CostDocument12 pagesQ1FY22 Result Update City Union Bank LTD: Beat On Operational Front Due To Lower Credit Costforgi mistyNo ratings yet

- Financial Model - Colgate Palmolive (Solved) : Prepared by Dheeraj Vaidya, CFA, FRMDocument27 pagesFinancial Model - Colgate Palmolive (Solved) : Prepared by Dheeraj Vaidya, CFA, FRMMehmet Isbilen100% (1)

- Top Glove 140618Document5 pagesTop Glove 140618Joseph CampbellNo ratings yet

- Hgs Q4 & Full Year Fy2018 Financials & Fact Sheet: Hinduja Global Solutions LimitedDocument6 pagesHgs Q4 & Full Year Fy2018 Financials & Fact Sheet: Hinduja Global Solutions LimitedChirag LaxmanNo ratings yet

- STORAENSO RESULTS Key Figures 2018Document11 pagesSTORAENSO RESULTS Key Figures 2018Paula Tapiero MorenoNo ratings yet

- Colgate Financial Model SolvedDocument30 pagesColgate Financial Model Solvedrsfgfgn fhhsdzfgvNo ratings yet

- FIN 3512 Fall 2019 Quiz #1 9.18.2019 To UploadDocument3 pagesFIN 3512 Fall 2019 Quiz #1 9.18.2019 To UploadgNo ratings yet

- CSS Ratio AnalysisDocument9 pagesCSS Ratio AnalysisMasood Ahmad AadamNo ratings yet

- RQDocument3 pagesRQKathlyn Joyce SumangNo ratings yet

- Corporate Finance MCQ QuestionsDocument10 pagesCorporate Finance MCQ QuestionsGanesh GaneshNo ratings yet

- Corporate finance quizDocument43 pagesCorporate finance quizPriyanka MahajanNo ratings yet

- Working Capital Policy Sums For FSADocument3 pagesWorking Capital Policy Sums For FSAAbhishek ThakurNo ratings yet

- 2233 - EN TNG Financial Statements 31-12-2015Document42 pages2233 - EN TNG Financial Statements 31-12-2015Nhật Linh LêNo ratings yet

- Case - Ohio Rubber Works Inc PDFDocument3 pagesCase - Ohio Rubber Works Inc PDFRaviSinghNo ratings yet

- GABRIEL - Investor Presentation - 05-EDocument48 pagesGABRIEL - Investor Presentation - 05-ETradingideas2456No ratings yet

- Project On Financial Analysis Between Tata Motors and Ashok LeylanDocument23 pagesProject On Financial Analysis Between Tata Motors and Ashok LeylannafisurNo ratings yet

- Working Capital Management of Odisha PowerDocument66 pagesWorking Capital Management of Odisha PowerPrateek Anand33% (3)

- Kevin Project - OushadhiDocument88 pagesKevin Project - OushadhiRojith Abraham CheruvazhakunnelNo ratings yet

- Butler Lumber Company Funding AnalysisDocument2 pagesButler Lumber Company Funding AnalysisDucNo ratings yet

- Executive Summary: Butler Lumber CompanyDocument3 pagesExecutive Summary: Butler Lumber CompanyVaishali GuptaNo ratings yet

- Business FundamentalsDocument24 pagesBusiness FundamentalsB112NITESH KUMAR SAHUNo ratings yet

- MCQ On Financial ManagementDocument23 pagesMCQ On Financial Managementsvparo0% (1)

- Textile Project ReportDocument116 pagesTextile Project ReportVikash Singh Gautam100% (1)

- Ch. 5 Financial AnalysisDocument34 pagesCh. 5 Financial AnalysisfauziyahNo ratings yet

- Unit EX1.2 - Corporate Finance and Financial StrategyDocument22 pagesUnit EX1.2 - Corporate Finance and Financial StrategyFamily MagroNo ratings yet

- Working Capital at Zuari Cement: Working Capital Management Is One of The Key Areas of Financial DecisionDocument5 pagesWorking Capital at Zuari Cement: Working Capital Management Is One of The Key Areas of Financial DecisionVardhan BujjiNo ratings yet

- Name: - Date: - QuizDocument4 pagesName: - Date: - QuizKatrine Clarisse BlanquiscoNo ratings yet

- Lesson 1: Overview of Financial ManagementDocument33 pagesLesson 1: Overview of Financial ManagementPhilip Denver NoromorNo ratings yet

- PPTDocument35 pagesPPTShivam ChauhanNo ratings yet

- Principles of Managerial Finance: Chapter 11Document54 pagesPrinciples of Managerial Finance: Chapter 11Crystal Nedd100% (3)

- Accounting Info+Financial StatementsDocument31 pagesAccounting Info+Financial StatementsSage WilliamsNo ratings yet

- Project Report On Grape Squash ManufacturingDocument13 pagesProject Report On Grape Squash ManufacturingPhanisreeNo ratings yet

- SYNOPSIS ON A STUDY OF WORKING CAPITAL MANAGEMENT OF AN ORGANISATION Khushboo DagaDocument10 pagesSYNOPSIS ON A STUDY OF WORKING CAPITAL MANAGEMENT OF AN ORGANISATION Khushboo DagaKhushboo DagaNo ratings yet

- Working Capital Management: Delivered By: Dr. Shakeel Iqbal AwanDocument48 pagesWorking Capital Management: Delivered By: Dr. Shakeel Iqbal AwanMuhammad Abdul Wajid RaiNo ratings yet

- Chapter 3 Financial Statement Taxes and CashflowDocument33 pagesChapter 3 Financial Statement Taxes and CashflowlovejkbsNo ratings yet

- Solution Manual For Case Studies in Finance 8th BrunerDocument13 pagesSolution Manual For Case Studies in Finance 8th BrunerDerekWrightjcio100% (33)

- "SRK Industries": A Study Analysis of Working Capital Management"Document71 pages"SRK Industries": A Study Analysis of Working Capital Management"Suhas IngaleNo ratings yet