You might also like

- Audit Program Cash and Bank BalancesDocument4 pagesAudit Program Cash and Bank BalancesGrace Unay100% (1)

- T A T I: Investing Cycle Learning ObjectivesDocument15 pagesT A T I: Investing Cycle Learning ObjectivesAngelo PayawalNo ratings yet

- DocxDocument15 pagesDocxjhouvanNo ratings yet

- 358763050Document15 pages358763050kristelle0marisseNo ratings yet

- Audit GKJDocument24 pagesAudit GKJtutuaman603No ratings yet

- Auditing Lecture Notes 04172022Document16 pagesAuditing Lecture Notes 04172022Abegail Cadacio100% (2)

- 09 - Cash and Bank BalancesDocument4 pages09 - Cash and Bank BalancesAqib SheikhNo ratings yet

- Chapter 20 - Answer PDFDocument10 pagesChapter 20 - Answer PDFjhienellNo ratings yet

- Stock Audit PresentationDocument27 pagesStock Audit PresentationShan BsmaniNo ratings yet

- Audit Assets & LiabilitiesDocument7 pagesAudit Assets & LiabilitiesHenry MapaNo ratings yet

- Verifying Trade PayablesDocument14 pagesVerifying Trade PayablesRuwan GunarathnaNo ratings yet

- Audit Investment FinancialsDocument3 pagesAudit Investment FinancialsHannah Tudio100% (1)

- 08 - Advances, Deposits, Prepayments and Other ReceivablesDocument4 pages08 - Advances, Deposits, Prepayments and Other ReceivablesAqib SheikhNo ratings yet

- Audit Program-Fixed AssetsDocument7 pagesAudit Program-Fixed AssetsNaomiNo ratings yet

- Substantive Testing For Deposit LiabilitiesDocument3 pagesSubstantive Testing For Deposit LiabilitiesChristian PerezNo ratings yet

- WP Asset B - Trade ReceivablesDocument15 pagesWP Asset B - Trade ReceivablesDikdikNo ratings yet

- 19l (12-00) Develop The Audit Program - RevenuesDocument2 pages19l (12-00) Develop The Audit Program - RevenuesAnh Tuấn TrầnNo ratings yet

- WEEK 5 ACCT444 Group Project 14-34Document6 pagesWEEK 5 ACCT444 Group Project 14-34Spencer Nath100% (2)

- Statutory Audit ChecklistDocument4 pagesStatutory Audit ChecklistAreeba FatimaNo ratings yet

- Audit AssertionsDocument5 pagesAudit AssertionsJazzyNo ratings yet

- Audit of Capital and ReservesDocument24 pagesAudit of Capital and Reserveseequals mcsquaredNo ratings yet

- Audit Plan For CashDocument5 pagesAudit Plan For CashDiana PrinceNo ratings yet

- 05 - Long Term Loans and AdvancesDocument5 pages05 - Long Term Loans and AdvancesAqib SheikhNo ratings yet

- Auditing and Assurance Services 4Th Edition Louwers Solutions Manual Full Chapter PDFDocument50 pagesAuditing and Assurance Services 4Th Edition Louwers Solutions Manual Full Chapter PDFstephenthanh1huo100% (12)

- Audit Procedures and Objectives for Key AccountsDocument121 pagesAudit Procedures and Objectives for Key AccountsabdellaNo ratings yet

- Manufacturing Procedures AuditDocument32 pagesManufacturing Procedures AuditVera Magdalena HutaurukNo ratings yet

- Prepaymentsand ReceivablesDocument3 pagesPrepaymentsand ReceivablesAsim JavedNo ratings yet

- Audit Program For Other IncomeDocument3 pagesAudit Program For Other IncomeCollins O.71% (7)

- 6th Sessiom - Audit of Investment STUDENTDocument17 pages6th Sessiom - Audit of Investment STUDENTNIMOTHI LASENo ratings yet

- Audit of Stock-in-Trade at Ahmad Hassan Textile MillsDocument5 pagesAudit of Stock-in-Trade at Ahmad Hassan Textile MillsAqib SheikhNo ratings yet

- TOPIC 5: AUDIT OF FINANCIAL STATEMENTS: Verification of Balance Sheet ItemsDocument34 pagesTOPIC 5: AUDIT OF FINANCIAL STATEMENTS: Verification of Balance Sheet ItemsIan100% (1)

- Audit of ReceivablesDocument30 pagesAudit of ReceivablesJay LloydNo ratings yet

- Audit Cash Equivalents Assertions ProceduresDocument7 pagesAudit Cash Equivalents Assertions Proceduresnicole bancoroNo ratings yet

- CA IPCC Auditing Suggested Answer Nov 2015Document12 pagesCA IPCC Auditing Suggested Answer Nov 2015Siva Narayana Phani MouliNo ratings yet

- Qa Audit of Receivables and SalesDocument7 pagesQa Audit of Receivables and SalesAsniah M. RatabanNo ratings yet

- Scope of Internal Audit - RDocument4 pagesScope of Internal Audit - RHarshadaNo ratings yet

- Audit of LiabilitiesDocument5 pagesAudit of LiabilitiesLea VillamorNo ratings yet

- Audit Cash Investments TitleDocument7 pagesAudit Cash Investments TitleIulia BurtoiuNo ratings yet

- Obtaining Audit Evidence on AssertionsDocument7 pagesObtaining Audit Evidence on AssertionsJesebel AmbalesNo ratings yet

- Nature, Objectives and Scope of AuditDocument20 pagesNature, Objectives and Scope of Auditbinu75% (4)

- Management of A Public Accounting Firm: Professional FeesDocument18 pagesManagement of A Public Accounting Firm: Professional FeesLaiza Mechelle Roxas MacaraigNo ratings yet

- GOTTAGETITDocument20 pagesGOTTAGETITHadia KhanNo ratings yet

- 1 Cash and Equivalent Audit ProgramDocument7 pages1 Cash and Equivalent Audit ProgramScribdTranslationsNo ratings yet

- Audit Evidence VouchingDocument8 pagesAudit Evidence VouchingGyanesh DoshiNo ratings yet

- Substantive Test OF Shareholders' EquityDocument46 pagesSubstantive Test OF Shareholders' EquityAldrin John TungolNo ratings yet

- 2024 - For Merge1Document17 pages2024 - For Merge1tigistdesalegn2021No ratings yet

- Cma Inter Audit - Marathon Notes Relevant For June and Dec 23Document64 pagesCma Inter Audit - Marathon Notes Relevant For June and Dec 23Sarfaraz ShaikhNo ratings yet

- CH01 - Nature of Specialized IndustriesDocument2 pagesCH01 - Nature of Specialized IndustriesJerikaye Marie ZafeNo ratings yet

- Gathering and Evaluating EvidenceDocument9 pagesGathering and Evaluating EvidenceLynne PetersNo ratings yet

- Vouching of Telephone ExpensesDocument11 pagesVouching of Telephone Expensesadeelfeb100% (1)

- Internal Controls For The Accounting Function (Contd.) : 1.examples of Accounting SubsystemsDocument31 pagesInternal Controls For The Accounting Function (Contd.) : 1.examples of Accounting Subsystemsraina mattNo ratings yet

- Audit Objectives and Financial Statements Assertions for Cash and Accounts ReceivableDocument63 pagesAudit Objectives and Financial Statements Assertions for Cash and Accounts ReceivableSarah Hashem100% (1)

- Audit of CashDocument25 pagesAudit of CashCHRISTINE TABULOGNo ratings yet

- Audit Icai FullDocument720 pagesAudit Icai Fullnsaiakshaya16No ratings yet

- Nature, Objective and Scope of Audit: Learning OutcomesDocument46 pagesNature, Objective and Scope of Audit: Learning OutcomesAniketNo ratings yet

- Internal Control of Fixed Assets: A Controller and Auditor's GuideFrom EverandInternal Control of Fixed Assets: A Controller and Auditor's GuideRating: 4 out of 5 stars4/5 (1)

- Engagement Essentials: Preparation, Compilation, and Review of Financial StatementsFrom EverandEngagement Essentials: Preparation, Compilation, and Review of Financial StatementsNo ratings yet

- Bookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursFrom EverandBookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursNo ratings yet

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- Sarbanes Financial ReportingDocument3 pagesSarbanes Financial ReportingDivine GraceNo ratings yet

- BSSOXFinancial Reporting Control MatrixDocument4 pagesBSSOXFinancial Reporting Control MatrixDivine GraceNo ratings yet

- APPLE Procurement-Non InventoryDocument3 pagesAPPLE Procurement-Non InventoryDivine GraceNo ratings yet

- BSSOXPurchasing&Payables Control MatrixDocument2 pagesBSSOXPurchasing&Payables Control MatrixDivine GraceNo ratings yet

- JII Internal Audit Check Disbursement ControlsDocument1 pageJII Internal Audit Check Disbursement ControlsDivine GraceNo ratings yet

- Audit of Internal ControlDocument160 pagesAudit of Internal ControlRavi K P KumarNo ratings yet

- Assessmentof ICover Financial ReportingDocument21 pagesAssessmentof ICover Financial ReportingDivine GraceNo ratings yet

- K12 Cash Disbursements&RelatedDocument52 pagesK12 Cash Disbursements&RelatedDivine GraceNo ratings yet

- Audit AP managementDocument9 pagesAudit AP managementDivine GraceNo ratings yet

- Audit of Disbursements and PayrollDocument2 pagesAudit of Disbursements and PayrollDivine GraceNo ratings yet

- ICMatrix Purchaseto PayDocument5 pagesICMatrix Purchaseto PayDivine GraceNo ratings yet

- Ap QuestionnaireDocument3 pagesAp QuestionnaireDivine GraceNo ratings yet

- Revenue Recognition Audit Guide Objectives ProceduresDocument6 pagesRevenue Recognition Audit Guide Objectives ProceduresDaniela BulardaNo ratings yet

- SOx 404 Purchasing APDocument2 pagesSOx 404 Purchasing APDivine GraceNo ratings yet

- Banking Prepaid Accrued ExpensesDocument3 pagesBanking Prepaid Accrued ExpensesDivine GraceNo ratings yet

- The 3 Laws of PerformanceDocument8 pagesThe 3 Laws of PerformanceDivine GraceNo ratings yet

- Ilog MariaDocument4 pagesIlog MariaDivine GraceNo ratings yet

- Basel Operational RiskDocument30 pagesBasel Operational RiskAleksandr RazumovskiyNo ratings yet

- The 3 Laws of PerformanceDocument8 pagesThe 3 Laws of PerformanceDivine GraceNo ratings yet

- Advanced Accounting 12th Edition Hoyle Solutions Manual Full Chapter PDFDocument41 pagesAdvanced Accounting 12th Edition Hoyle Solutions Manual Full Chapter PDFanwalteru32x100% (14)

- Enhanced NSBI Book Value Calculator v2Document8 pagesEnhanced NSBI Book Value Calculator v2jahjahNo ratings yet

- Exhibitor List ItalyDocument35 pagesExhibitor List ItalyTruck Trailer & Tyre ExpoNo ratings yet

- Payback PeriodDocument32 pagesPayback Periodarif SazaliNo ratings yet

- TYBFM A 36 Vignesh Khandelwal Black BookDocument74 pagesTYBFM A 36 Vignesh Khandelwal Black Bookpreet doshiNo ratings yet

- Advanced Accounting 13th Edition Beams Test Bank Full Chapter PDFDocument59 pagesAdvanced Accounting 13th Edition Beams Test Bank Full Chapter PDFanwalteru32x100% (13)

- SS CT DEC 2021 TITLEDocument4 pagesSS CT DEC 2021 TITLEsharifah nurshahira sakinaNo ratings yet

- FDNACCT - Quiz #1 - Solutions To PS - Set ADocument2 pagesFDNACCT - Quiz #1 - Solutions To PS - Set AleshamunsayNo ratings yet

- FAR - March-April-2021Document8 pagesFAR - March-April-2021Towhidul IslamNo ratings yet

- Foreign Currency Transactions and Translations ExplainedDocument4 pagesForeign Currency Transactions and Translations ExplainedKrizia Mae Flores100% (1)

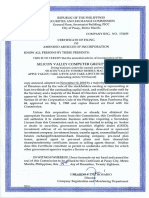

- SEC Amended Articles of Incorporation for Silicon Valley Computer GroupDocument20 pagesSEC Amended Articles of Incorporation for Silicon Valley Computer GroupSir AronNo ratings yet

- SCF WorksheetDocument19 pagesSCF WorksheetAngelo Gian CoNo ratings yet

- Account GPDocument22 pagesAccount GPNurul SyuhadaNo ratings yet

- MS-44J (Working Capital Management)Document13 pagesMS-44J (Working Capital Management)juleslovefenNo ratings yet

- Chapter 06: Dividend Decision: ................ Md. Jobayair Ibna Rafiq.............Document62 pagesChapter 06: Dividend Decision: ................ Md. Jobayair Ibna Rafiq.............Mohammad Salim Hossain0% (1)

- Sap Functionality For Accounting of Prepaid ExpensesDocument3 pagesSap Functionality For Accounting of Prepaid ExpensesVanshika Narang100% (1)

- Financial Projections-TextDocument5 pagesFinancial Projections-TextFarid UddinNo ratings yet

- Ie00b5bmr087 - 01 01 2023Document3 pagesIe00b5bmr087 - 01 01 2023Tanasa AlinNo ratings yet

- Acc466 Test 2 July2022 - Question (PW)Document9 pagesAcc466 Test 2 July2022 - Question (PW)nur hadhirahNo ratings yet

- Accounting and Finance MCQsDocument50 pagesAccounting and Finance MCQsSathish Kumar MagapuNo ratings yet

- Closing Entries (Accounting)Document3 pagesClosing Entries (Accounting)Sachi LoreigneNo ratings yet

- UCU 104 Lesson 6Document19 pagesUCU 104 Lesson 6Matt HeavenNo ratings yet

- Nov 2019 Paper 2A Questions EngDocument10 pagesNov 2019 Paper 2A Questions EngTerry MaNo ratings yet

- College Accounting A Contemporary Approach 3rd Edition Haddock Price Farina ISBN Solution ManualDocument22 pagesCollege Accounting A Contemporary Approach 3rd Edition Haddock Price Farina ISBN Solution Manualdonald100% (24)

- BC 304 PI Past PapersDocument29 pagesBC 304 PI Past PapersBilal AhmadNo ratings yet

- Solution Manual For Case Studies in Finance 8th BrunerDocument13 pagesSolution Manual For Case Studies in Finance 8th BrunerDerekWrightjcio100% (33)

- Question Paper Accountancy Class 12Document12 pagesQuestion Paper Accountancy Class 12SunitaNo ratings yet

- BBK 2017 H1-Results-V6-TwinDocument1 pageBBK 2017 H1-Results-V6-TwinManil UniqueNo ratings yet

- Net Economic Value Added From Year To Year: Group 7Document17 pagesNet Economic Value Added From Year To Year: Group 7James Ryan AlzonaNo ratings yet

- Disclosures Under Regulation 29 (2) of SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011Document9 pagesDisclosures Under Regulation 29 (2) of SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011Contra Value BetsNo ratings yet