You might also like

- Achieving a Sustainable and Efficient Energy Transition in Indonesia: A Power Sector Restructuring Road MapFrom EverandAchieving a Sustainable and Efficient Energy Transition in Indonesia: A Power Sector Restructuring Road MapNo ratings yet

- Lucky Electric Power - RR - 2503 - 10939 - 05-Dec-22Document7 pagesLucky Electric Power - RR - 2503 - 10939 - 05-Dec-22Kristian MacariolaNo ratings yet

- HubcoDocument6 pagesHubcolaiba mujahidNo ratings yet

- HUBCO RR - 2236 - 9714 - 13-Dec-21Document6 pagesHUBCO RR - 2236 - 9714 - 13-Dec-21Kristian MacariolaNo ratings yet

- Gul Ahmed Electric Limited: Rating ReportDocument5 pagesGul Ahmed Electric Limited: Rating ReportKiranNo ratings yet

- Sindh Engro Coal Mining Company: Rating ReportDocument5 pagesSindh Engro Coal Mining Company: Rating ReportHussain SyedNo ratings yet

- Narowal Energy - RR - 1579 - 10334 - 22-Jun-22Document5 pagesNarowal Energy - RR - 1579 - 10334 - 22-Jun-22Kristian MacariolaNo ratings yet

- K-Electric - ICP-11: Rating ReportDocument6 pagesK-Electric - ICP-11: Rating ReportAli RazaNo ratings yet

- RR 2394 12042 05-Sep-23Document5 pagesRR 2394 12042 05-Sep-23Muhammad Abubakar SheikhNo ratings yet

- Pacra Maintains Ratings of Pakistan Refinery Limited: Ress EleaseDocument8 pagesPacra Maintains Ratings of Pakistan Refinery Limited: Ress EleaseSaad SalmanNo ratings yet

- Cleanmax IPP 2 Private LimitedDocument5 pagesCleanmax IPP 2 Private LimitedDhawal VasavadaNo ratings yet

- Rating ReportDocument5 pagesRating Reportl202095No ratings yet

- Rating MBHDocument5 pagesRating MBHHamzaMehmoodBhattiNo ratings yet

- Bulleh Shah Packaging (PVT.) Limited: Rating ReportDocument5 pagesBulleh Shah Packaging (PVT.) Limited: Rating Report057-Kaynat khanNo ratings yet

- Press Release: Raichur Power Corporation LimitedDocument3 pagesPress Release: Raichur Power Corporation LimitedPrasanna Kumar KNo ratings yet

- Document Service V2Document6 pagesDocument Service V2UTSAV DUBEYNo ratings yet

- POWERGRID Infrastructure Investment TrustDocument5 pagesPOWERGRID Infrastructure Investment TrustSamdheepak ThomasNo ratings yet

- Nishat Power - RR - 78 - 10732 - 24-Sep-22Document5 pagesNishat Power - RR - 78 - 10732 - 24-Sep-22Kristian MacariolaNo ratings yet

- CTR Manufacturing Industries Private LimitedDocument7 pagesCTR Manufacturing Industries Private Limitedkrushna.maneNo ratings yet

- Reliance Weaving LTDDocument5 pagesReliance Weaving LTDhhaiderNo ratings yet

- Price Waterhouse & Co Chartered Accountants LLPDocument8 pagesPrice Waterhouse & Co Chartered Accountants LLPSuraj KumarNo ratings yet

- Sundaram Alternate Assets LimitedDocument7 pagesSundaram Alternate Assets LimitedSabSab MukNo ratings yet

- Press Release RACL Geartech LTDDocument4 pagesPress Release RACL Geartech LTDSourav DuttaNo ratings yet

- 4QFY22Document36 pages4QFY22Rajendra AvinashNo ratings yet

- Khulna Power Company LTD-PTDDocument10 pagesKhulna Power Company LTD-PTDnasirNo ratings yet

- Power Finance CorporationDocument32 pagesPower Finance Corporationangshu0020100% (2)

- JSWENERGY - Investor Presentation - 03-May-22 - TickertapeDocument79 pagesJSWENERGY - Investor Presentation - 03-May-22 - TickertapeM j PatelNo ratings yet

- Prayag Polymers Private LimitedDocument4 pagesPrayag Polymers Private Limitednandinimishra6168No ratings yet

- L & W Building Solutions PVT LTDDocument7 pagesL & W Building Solutions PVT LTDhesham zakiNo ratings yet

- LOTTE Kolson (PVT.) Limited: Rating ReportDocument5 pagesLOTTE Kolson (PVT.) Limited: Rating ReportAreeba AmirNo ratings yet

- Fabtech Projects and Engineers LimitedDocument5 pagesFabtech Projects and Engineers LimitedGanoba 444No ratings yet

- Azure Power Thirty Six - R-15102018Document6 pagesAzure Power Thirty Six - R-15102018vinay durgapalNo ratings yet

- LIberty Power Tech - RR - 74 - 10861 - 10-Nov-22Document5 pagesLIberty Power Tech - RR - 74 - 10861 - 10-Nov-22Kristian MacariolaNo ratings yet

- Summer - Internship - Report - Project - Apprais - NaveenDocument89 pagesSummer - Internship - Report - Project - Apprais - NaveenNaveen GuptaNo ratings yet

- Khaadi - 14 Dec 21Document5 pagesKhaadi - 14 Dec 21Anum ShamimNo ratings yet

- Agrocel Industries Private LimitedDocument7 pagesAgrocel Industries Private LimitedNitin KumarNo ratings yet

- Press Release: Refer Annexure For DetailsDocument5 pagesPress Release: Refer Annexure For Detailslalit rawatNo ratings yet

- 22.3 Build or Buy Decision QASPL AJMCDocument23 pages22.3 Build or Buy Decision QASPL AJMCAli Zain ParharNo ratings yet

- Powergrid SipDocument62 pagesPowergrid SipmonNo ratings yet

- RR 1664 9107 1Document5 pagesRR 1664 9107 1Saifullah SaifiNo ratings yet

- Abhishek ReportDocument62 pagesAbhishek ReportAshokNo ratings yet

- Business Profile:: Power Finance Corporation LimitedDocument6 pagesBusiness Profile:: Power Finance Corporation LimitedBarkha SinghalNo ratings yet

- Preface: NTPC Limited Capacity Addition Programme - Project ManagementDocument69 pagesPreface: NTPC Limited Capacity Addition Programme - Project ManagementbhagyashreNo ratings yet

- PNC Challakere (Karnataka) Highways Private LimitedDocument4 pagesPNC Challakere (Karnataka) Highways Private LimitedSrujan ReddyNo ratings yet

- AR Summit 2016-17 PDFDocument184 pagesAR Summit 2016-17 PDFSumaiya RahmanNo ratings yet

- SGS Tekniks Manufacturing PVT LTDDocument7 pagesSGS Tekniks Manufacturing PVT LTDgcgary87No ratings yet

- SMC Power Generation LTD.: Summary of Rated InstrumentsDocument7 pagesSMC Power Generation LTD.: Summary of Rated Instrumentspiyush upadhyayNo ratings yet

- Anuh Pharma LimitedDocument7 pagesAnuh Pharma Limitedadhyan kashyapNo ratings yet

- JSWEL Corporate Investor Presentation February 2023Document63 pagesJSWEL Corporate Investor Presentation February 2023Sutirtha DasNo ratings yet

- Research Report of Masood Roomi FabricDocument5 pagesResearch Report of Masood Roomi FabricWaqas AkramNo ratings yet

- Tungabhadra Solar Parks Private LimitedDocument8 pagesTungabhadra Solar Parks Private Limitedtarunbajaj1107No ratings yet

- Prateek Wires (P) LTD - R - 08102020Document6 pagesPrateek Wires (P) LTD - R - 08102020DarshanNo ratings yet

- PFC Ar2019 2024122020Document368 pagesPFC Ar2019 2024122020Dhyan MothukuriNo ratings yet

- Si Project ReportDocument32 pagesSi Project ReportShivani NegiNo ratings yet

- Onshore Construction Company Private LimitedDocument7 pagesOnshore Construction Company Private Limitedhesham zakiNo ratings yet

- 575-600-Case StudyDocument26 pages575-600-Case StudyHina FatimaNo ratings yet

- RR 2269 11061 18-Jan-23Document5 pagesRR 2269 11061 18-Jan-23khurramsadiq888No ratings yet

- Power Finance CorpDocument10 pagesPower Finance CorpdevrajkinjalNo ratings yet

- Pharmagen Limited: Rating ReportDocument5 pagesPharmagen Limited: Rating ReportMuhammad Ahmed MirzaNo ratings yet

- Rcncwoblcs: Pragnes H DarjiDocument118 pagesRcncwoblcs: Pragnes H Darjivirupakshudu kodiyalaNo ratings yet

- Order_2023-133RCDocument64 pagesOrder_2023-133RCKristian MacariolaNo ratings yet

- Nishat Power LTDDocument43 pagesNishat Power LTDKristian MacariolaNo ratings yet

- Narowal Energy - RR - 1579 - 10334 - 22-Jun-22Document5 pagesNarowal Energy - RR - 1579 - 10334 - 22-Jun-22Kristian MacariolaNo ratings yet

- Nishat Power - RR - 78 - 10732 - 24-Sep-22Document5 pagesNishat Power - RR - 78 - 10732 - 24-Sep-22Kristian MacariolaNo ratings yet

- LIberty Power Tech - RR - 74 - 10861 - 10-Nov-22Document5 pagesLIberty Power Tech - RR - 74 - 10861 - 10-Nov-22Kristian MacariolaNo ratings yet

- TRF-308 Huaneng Upfront Coal Determination 31-03-2015 4385-87Document19 pagesTRF-308 Huaneng Upfront Coal Determination 31-03-2015 4385-87Kristian MacariolaNo ratings yet

- Module 1 - Understanding ExpensesDocument14 pagesModule 1 - Understanding Expensesjudith magsinoNo ratings yet

- 2.edited FM Capital BudgetingDocument72 pages2.edited FM Capital BudgetingbelovedbijithNo ratings yet

- FIN254 Report On Ratio Analyis and Intrepretaion of RAK Ceramics Bangladesh LimitedDocument27 pagesFIN254 Report On Ratio Analyis and Intrepretaion of RAK Ceramics Bangladesh LimitedAbdullah Al SakibNo ratings yet

- MCQDocument5 pagesMCQRazin Gajiwala100% (2)

- Financial Management - Compilation of Financial RatiosDocument6 pagesFinancial Management - Compilation of Financial RatiosIce AlojaNo ratings yet

- Chapter 9 - Pas 1 Statement of Comprehensive IncomeDocument26 pagesChapter 9 - Pas 1 Statement of Comprehensive IncomeMarriel Fate CullanoNo ratings yet

- RWJ - FCF11e - Chap - 16-Financial LeverageDocument50 pagesRWJ - FCF11e - Chap - 16-Financial LeverageCẩm TiênNo ratings yet

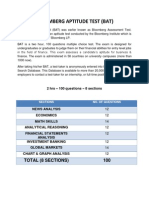

- Bloomberg Aptitude Test (BAT)Document10 pagesBloomberg Aptitude Test (BAT)Shivgan Joshi100% (1)

- Tutorial 3 QDocument2 pagesTutorial 3 QBraham Rahul Ram JamnadasNo ratings yet

- Causes of Difference in Profit of Cost and Financial AccountingDocument4 pagesCauses of Difference in Profit of Cost and Financial Accountingvivek kumarNo ratings yet

- NIC Consolidated 31 December 2021 - EnglishDocument9 pagesNIC Consolidated 31 December 2021 - Englishsam davidNo ratings yet

- ACC501 Mod 1 Case Financial StatementsDocument12 pagesACC501 Mod 1 Case Financial StatementsNoble S WolfeNo ratings yet

- Yeats Valves and Controls IncDocument16 pagesYeats Valves and Controls IncStackwell IndiaNo ratings yet

- AF210: Financial Accounting: School of Accounting and FinanceDocument11 pagesAF210: Financial Accounting: School of Accounting and FinanceShikhaNo ratings yet

- CH 19 Hull OFOD9 TH Editionbr 1Document33 pagesCH 19 Hull OFOD9 TH Editionbr 1Willem VincentNo ratings yet

- Dey's Important Questions of Accounting For Debentures Based On CBSE SQP For Term-II Exam-2022 (Extracted From Exam Handbook 2022 Term-II)Document5 pagesDey's Important Questions of Accounting For Debentures Based On CBSE SQP For Term-II Exam-2022 (Extracted From Exam Handbook 2022 Term-II)RiNo ratings yet

- Topic 5 Answer Key and SolutionsDocument6 pagesTopic 5 Answer Key and SolutionscykenNo ratings yet

- Intermediate Accounting 3 1. Chapter 4: Share-Based Payments (Part 2)Document5 pagesIntermediate Accounting 3 1. Chapter 4: Share-Based Payments (Part 2)happy240823100% (1)

- Introducing Arrowroot Real Estate's First AcquisitionDocument2 pagesIntroducing Arrowroot Real Estate's First AcquisitionPR.comNo ratings yet

- Visa Inc Fiscal 2022 Annual ReportDocument143 pagesVisa Inc Fiscal 2022 Annual ReportPankaj GoyalNo ratings yet

- Intercompany Sales Problem Solving Exercises (Test Bank)Document2 pagesIntercompany Sales Problem Solving Exercises (Test Bank)Kristine Esplana Toralde100% (1)

- Analysis of Working Capital Management Ankush NanavatiDocument85 pagesAnalysis of Working Capital Management Ankush Nanavatisachindixit46No ratings yet

- 3.2 ExercisesDocument6 pages3.2 ExercisesGeorgios MilitsisNo ratings yet

- Yilendwe ExcelDocument4 pagesYilendwe Excelsanjay gautamNo ratings yet

- 123 - AS Question Bank by Rahul MalkanDocument182 pages123 - AS Question Bank by Rahul MalkanPooja GuptaNo ratings yet

- FM GA2 FinalDocument15 pagesFM GA2 FinalTulsi GovaniNo ratings yet

- ACC 557 Week 1 Chapter 1Document11 pagesACC 557 Week 1 Chapter 1acurashah100% (1)

- Class 12 Accounts Notes Chapter 3 Studyguide360 - 2Document17 pagesClass 12 Accounts Notes Chapter 3 Studyguide360 - 2Ali ssNo ratings yet

- Demand and Market Struture For LPG in Zambia 2019 1Document88 pagesDemand and Market Struture For LPG in Zambia 2019 1Lubilo MateNo ratings yet

- Cost of Credit FormulaDocument3 pagesCost of Credit FormulaShin YaeNo ratings yet