You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (346)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 2.0-Multiple Timeframe AnalysisDocument6 pages2.0-Multiple Timeframe AnalysisOntiretse Ngwako100% (1)

- Arab Region Fintech GuideDocument54 pagesArab Region Fintech GuideHisham DaelNo ratings yet

- IWPA Members Address ListDocument188 pagesIWPA Members Address ListGayathri Rupin75% (8)

- Checklist For Piling WorksDocument8 pagesChecklist For Piling WorksAaronNo ratings yet

- Geography Book 2Document40 pagesGeography Book 2elise limNo ratings yet

- Kurt Weyland - The Rise of Latin America S Two Lefts Insights From Rentier State TheoryDocument20 pagesKurt Weyland - The Rise of Latin America S Two Lefts Insights From Rentier State TheorycacoNo ratings yet

- Inventories NotesDocument7 pagesInventories NotesJessel Ann MontecilloNo ratings yet

- Success Magazine Jan 2014Document92 pagesSuccess Magazine Jan 2014GuillermoSurracoNo ratings yet

- Full Download Test Bank For International Management Culture Strategy and Behavior 11th Edition Fred Luthans Jonathan Doh PDF Full ChapterDocument36 pagesFull Download Test Bank For International Management Culture Strategy and Behavior 11th Edition Fred Luthans Jonathan Doh PDF Full Chapterrusmaactinalf9bf5j100% (15)

- Bcoe 142 PDFDocument4 pagesBcoe 142 PDFShiv KumarNo ratings yet

- Cases PMF 11thed GitmannDocument61 pagesCases PMF 11thed GitmannJohn Carlos WeeNo ratings yet

- VIDYA SAGAR Analysis-CA Final LAW For Dec - 2021Document6 pagesVIDYA SAGAR Analysis-CA Final LAW For Dec - 2021Ranjit BhogesaraNo ratings yet

- Chapter 2Document17 pagesChapter 2Amanuel GenetNo ratings yet

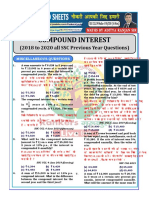

- Compound Interest: (2018 To 2020 All SSC Previous Year Questions)Document17 pagesCompound Interest: (2018 To 2020 All SSC Previous Year Questions)HakjsNo ratings yet

- LOI - Petroleum FZCDocument2 pagesLOI - Petroleum FZCMohamed Mehdi OuakdiNo ratings yet

- Project-Management Solved MCQs (Set-5)Document8 pagesProject-Management Solved MCQs (Set-5)MiressaBeJiNo ratings yet

- Examples and ProblemsDocument4 pagesExamples and ProblemsPaul AounNo ratings yet

- SIMBIZ Annual Report ExerciseDocument13 pagesSIMBIZ Annual Report ExerciseViona Putri WijayaNo ratings yet

- Ncert Booklist: S.No. Subject Class Book EditionDocument1 pageNcert Booklist: S.No. Subject Class Book EditionBhartendu ShakyaNo ratings yet

- Soa - Converge SampleDocument1 pageSoa - Converge SampleFulbert Eli MendozaNo ratings yet

- MM439: Iron and Steel Making: Course ContentsDocument11 pagesMM439: Iron and Steel Making: Course Contentsmanish pandeNo ratings yet

- Industrial Engineering & Management: India 'S Saddlery and Harness Sector: Exports and Its ChallengesDocument4 pagesIndustrial Engineering & Management: India 'S Saddlery and Harness Sector: Exports and Its ChallengesTanveerNo ratings yet

- OpenDocs Service InvoiceDocument1 pageOpenDocs Service Invoicemiranda criggerNo ratings yet

- History of Economic Thought 12 PDFDocument9 pagesHistory of Economic Thought 12 PDFPrema SelvarajNo ratings yet

- Drager Paslite Ba SetDocument4 pagesDrager Paslite Ba SetSUNIL MISHRANo ratings yet

- ICICI SmartKid Brochure FinalDocument23 pagesICICI SmartKid Brochure FinalNiharika AnandNo ratings yet

- Business Law A2 Mai Huong (Recovered)Document6 pagesBusiness Law A2 Mai Huong (Recovered)Mai HươngNo ratings yet

- F Fukuyama End of History and The WorldDocument8 pagesF Fukuyama End of History and The WorldAleezay ChaudhryNo ratings yet

- Financial Planning Tools: WK04-LAS2-BF-II-12Document37 pagesFinancial Planning Tools: WK04-LAS2-BF-II-12Benj Jamieson DuagNo ratings yet

- Midterm Examination - MAS REVIEWDocument7 pagesMidterm Examination - MAS REVIEWFrancis MateosNo ratings yet