You might also like

- An Overview of Auditing the CIS EnvironmentDocument14 pagesAn Overview of Auditing the CIS EnvironmentRana LinNo ratings yet

- Chapter 20 The Computer EnvironmentDocument13 pagesChapter 20 The Computer EnvironmentClar Aaron Bautista100% (1)

- Auditing Theory - 090: Cis Environment & Completing An Audit CMP The Computer EnvironmentDocument7 pagesAuditing Theory - 090: Cis Environment & Completing An Audit CMP The Computer EnvironmentLeny Joy DupoNo ratings yet

- Auditing in A CIS EnvironmentDocument15 pagesAuditing in A CIS EnvironmentJollybelleann Marcos100% (2)

- Auditing in a CIS EnvironmentDocument10 pagesAuditing in a CIS Environmentbobo ka0% (1)

- Chapter 6: Auditing in A Computer Information Systems (Cis) or Information Technology (It) EnvironmentDocument29 pagesChapter 6: Auditing in A Computer Information Systems (Cis) or Information Technology (It) EnvironmentLeny Joy DupoNo ratings yet

- Chapter 12 Multiple-Choice Questions on Auditing IT SystemsDocument12 pagesChapter 12 Multiple-Choice Questions on Auditing IT SystemsJohn Rey EnriquezNo ratings yet

- Auditing Computerized EnvironmentsDocument9 pagesAuditing Computerized EnvironmentsAngela Miles Dizon100% (1)

- Audit Specialized Industries Under 40 CharactersDocument61 pagesAudit Specialized Industries Under 40 CharactersCrizza Demecillo100% (2)

- Unit I: Audit of Investment PropertyDocument11 pagesUnit I: Audit of Investment PropertyAnn SarmientoNo ratings yet

- 10.1. Cis Environment: Meaning of CIS AuditDocument13 pages10.1. Cis Environment: Meaning of CIS AuditShubham BhatiaNo ratings yet

- Defining Specialized Industries and Auditing RequirementsDocument2 pagesDefining Specialized Industries and Auditing RequirementsPaupauNo ratings yet

- Audit 4 - Audit in Specialized IndustryDocument7 pagesAudit 4 - Audit in Specialized IndustryPaupauNo ratings yet

- IT Auditing 4th Edition Test BankDocument39 pagesIT Auditing 4th Edition Test BankMelanie SamsonaNo ratings yet

- ANSWER Key Quiz 5 Auditing CISDocument7 pagesANSWER Key Quiz 5 Auditing CISQuendrick SurbanNo ratings yet

- Quiz # 6 Reviewer Auditing Computer Information SystemsDocument5 pagesQuiz # 6 Reviewer Auditing Computer Information SystemsJohn Lexter MacalberNo ratings yet

- Aud. in Cis Env. Final Exam 2nd Sem Ay2017-18 (Sam)Document9 pagesAud. in Cis Env. Final Exam 2nd Sem Ay2017-18 (Sam)Uy SamuelNo ratings yet

- At 04 Auditing in A Cis EnvironmentDocument16 pagesAt 04 Auditing in A Cis Environmentcarl fuerzasNo ratings yet

- Audit Theory Case AnalysisDocument2 pagesAudit Theory Case AnalysisSheila Mary GregorioNo ratings yet

- Lesson 1 Overview of IT AuditDocument42 pagesLesson 1 Overview of IT AuditMCDABCNo ratings yet

- CPA review auditing in a CIS environmentDocument12 pagesCPA review auditing in a CIS environmentJohn Carlo Cruz67% (3)

- AUD CIS CH 1-6Document25 pagesAUD CIS CH 1-6Bela BellsNo ratings yet

- Quiz 2 AuditingDocument4 pagesQuiz 2 AuditingCrissa Mae Falsis100% (1)

- Audit Expenditure Cycle TestsDocument19 pagesAudit Expenditure Cycle TestsKaren PortiaNo ratings yet

- Auditing Standards and Practices Council: Philippine Auditing Practice Statement 1009 Computer-Assisted Audit TechniquesDocument25 pagesAuditing Standards and Practices Council: Philippine Auditing Practice Statement 1009 Computer-Assisted Audit TechniquesDaphne0% (1)

- Pas 29 Financial Reporting in Hyperinflationary EconomiesDocument2 pagesPas 29 Financial Reporting in Hyperinflationary EconomiesLlyana paula SuyuNo ratings yet

- Audit of Specialized IndustriesDocument7 pagesAudit of Specialized IndustriesCatherine Bercasio Dela CruzNo ratings yet

- Auditing in Specialized Industries (Notes)Document10 pagesAuditing in Specialized Industries (Notes)Jene LmNo ratings yet

- CIS - It Environment ReviewerDocument28 pagesCIS - It Environment RevieweraceNo ratings yet

- Psa 401Document5 pagesPsa 401novyNo ratings yet

- Tandem Activity GE Allowable DeductionsDocument6 pagesTandem Activity GE Allowable DeductionsErin CruzNo ratings yet

- Profe03 - Chapter 1 Business Combinations Recognition and MeasurementDocument19 pagesProfe03 - Chapter 1 Business Combinations Recognition and MeasurementSteffany Roque100% (1)

- Audit of Liabilities ProceduresDocument9 pagesAudit of Liabilities Procedureskara albueraNo ratings yet

- CHAPTER 7 - Solman CONSOLIDATED FS PART 4 - ACCTG FOR BUS. COMBINATIONSDocument20 pagesCHAPTER 7 - Solman CONSOLIDATED FS PART 4 - ACCTG FOR BUS. COMBINATIONSJeeramel TorresNo ratings yet

- Lecture 2 Auditing IT Governance ControlsDocument63 pagesLecture 2 Auditing IT Governance ControlsAldwin CalambaNo ratings yet

- PAPS 1001: Computer Information Systems Environment - Stand-Alone Personal ComputersDocument8 pagesPAPS 1001: Computer Information Systems Environment - Stand-Alone Personal ComputersJomaica AmadorNo ratings yet

- Chapter 22 Auditing in A CIS Environment - pptx990626434Document25 pagesChapter 22 Auditing in A CIS Environment - pptx990626434Clar Aaron Bautista67% (3)

- 6 - Lecture - The 8 Es in AuditingDocument11 pages6 - Lecture - The 8 Es in AuditingKris MendezNo ratings yet

- Bcsvillaluz: Advanced Financial Accounting & Reporting (Afar) Financial Accounting & Reporting (Far)Document5 pagesBcsvillaluz: Advanced Financial Accounting & Reporting (Afar) Financial Accounting & Reporting (Far)nickoloco100% (1)

- Auditing in a Computerized EnvironmentDocument15 pagesAuditing in a Computerized EnvironmentLawrenceValdezNo ratings yet

- Chapter 11 Intagible AssetsDocument5 pagesChapter 11 Intagible Assetsmaria isabellaNo ratings yet

- Chapter 7: Auditing in A Computerized Environment (No 85)Document22 pagesChapter 7: Auditing in A Computerized Environment (No 85)JIL Masapang Victoria ChapterNo ratings yet

- Auditing in CIS EnvironmentDocument36 pagesAuditing in CIS EnvironmentMei Chien Yap89% (9)

- Ass 2 in AuditingDocument5 pagesAss 2 in Auditingarnel gallarteNo ratings yet

- Information Technology Auditing 3rd Edition James HallDocument9 pagesInformation Technology Auditing 3rd Edition James HallHiraya ManawariNo ratings yet

- Quiz Chapter 1 Business Combinations Part 1Document6 pagesQuiz Chapter 1 Business Combinations Part 1Kaye L. Dela CruzNo ratings yet

- Accounting For Business Combinations First Grading ExaminationDocument18 pagesAccounting For Business Combinations First Grading ExaminationNhel AlvaroNo ratings yet

- Audit Approach in CIS EnvironmentsDocument30 pagesAudit Approach in CIS EnvironmentsMiles SantosNo ratings yet

- Auditing CIS Environment Chap 1Document2 pagesAuditing CIS Environment Chap 1Michelle AnnNo ratings yet

- Aviation: Chapter 1 - The Airline Industry Chapter 2 - Accounting and Auditing in An Airline EnvironmentDocument15 pagesAviation: Chapter 1 - The Airline Industry Chapter 2 - Accounting and Auditing in An Airline EnvironmentJessa Gay Cartagena TorresNo ratings yet

- editedQUIZ CHAPTER-6 FINANCIAL-ASSETSDocument3 pageseditedQUIZ CHAPTER-6 FINANCIAL-ASSETSanna mariaNo ratings yet

- Assurance Engagement QuizDocument7 pagesAssurance Engagement Quizdave excelleNo ratings yet

- Summative Assessment 2 ITDocument9 pagesSummative Assessment 2 ITJoana Trinidad100% (1)

- Auditing Concept Problems Cash and Cash EquivalentDocument7 pagesAuditing Concept Problems Cash and Cash EquivalentJoanah TayamenNo ratings yet

- ACT 1202 Quiz No. 1 - AUDITING AND ASSURANCE PRINCIPLESDocument21 pagesACT 1202 Quiz No. 1 - AUDITING AND ASSURANCE PRINCIPLESJimbo ManalastasNo ratings yet

- Introduction To Audit and Assurance in Specialized IndustriesDocument15 pagesIntroduction To Audit and Assurance in Specialized IndustriesJohann VillegasNo ratings yet

- CHAPTER 26: COMPUTER ENVIRONMENTSDocument3 pagesCHAPTER 26: COMPUTER ENVIRONMENTSClang SantiagoNo ratings yet

- Applications of Computers in Accounting: - State The MeaningDocument17 pagesApplications of Computers in Accounting: - State The MeaningSonia SNo ratings yet

- Operating System Definition: It Is A Software That Works As An Interface Between A User andDocument8 pagesOperating System Definition: It Is A Software That Works As An Interface Between A User andmuraryNo ratings yet

- ICT ModuleDocument46 pagesICT Modulegiven kalukanguNo ratings yet

- LossesDocument4 pagesLossesNoroNo ratings yet

- Tax1 SummaryDocument8 pagesTax1 SummarychimchimcoliNo ratings yet

- CHAP 26. Internal and Government Financial Auditing and Operational AuditinDocument16 pagesCHAP 26. Internal and Government Financial Auditing and Operational AuditinNoroNo ratings yet

- Gross IncomeDocument4 pagesGross IncomeNoroNo ratings yet

- Concept of IncomeDocument3 pagesConcept of IncomeNoroNo ratings yet

- CHAP 4.professional EthicsDocument29 pagesCHAP 4.professional EthicsNoroNo ratings yet

- CHAP 8. Audit Planning and Analytical ProceduresDocument24 pagesCHAP 8. Audit Planning and Analytical ProceduresNoroNo ratings yet

- Management Accounting Environment (Final)Document3 pagesManagement Accounting Environment (Final)NoroNo ratings yet

- Prophet' S BiographyDocument5 pagesProphet' S BiographyNoroNo ratings yet

- Business Plan Marketing Plan 1.1 The ProductDocument9 pagesBusiness Plan Marketing Plan 1.1 The ProductNoroNo ratings yet

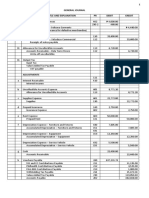

- GJS, TBS, and FSsDocument15 pagesGJS, TBS, and FSsNoro100% (1)

- Prof. Charlou BautistaDocument2 pagesProf. Charlou BautistaNoroNo ratings yet

- CHAP 10. Internal Control and Control RiskDocument27 pagesCHAP 10. Internal Control and Control RiskNoro100% (1)

- UntitledDocument11 pagesUntitledNoroNo ratings yet

- AssetsDocument17 pagesAssetsChloeNo ratings yet

- 2technical PlanDocument6 pages2technical PlanNoroNo ratings yet

- CWTSNST41Document2 pagesCWTSNST41NoroNo ratings yet

- GJS, TBS, and FSsDocument15 pagesGJS, TBS, and FSsNoro100% (1)

- Growing Internet Business in MSUDocument7 pagesGrowing Internet Business in MSUNoroNo ratings yet

- SPECIAL JOURNALS (Final)Document8 pagesSPECIAL JOURNALS (Final)NoroNo ratings yet

- Test Bank - Chapter 3 Job Order CostingDocument36 pagesTest Bank - Chapter 3 Job Order CostingAiko E. Lara81% (21)

- ReadingsDocument4 pagesReadingsNoroNo ratings yet

- CWTSNST41Document2 pagesCWTSNST41NoroNo ratings yet

- Lecture 2. Supply and DemandDocument51 pagesLecture 2. Supply and DemandNoroNo ratings yet

- SPECIAL JOURNALS (Final)Document8 pagesSPECIAL JOURNALS (Final)NoroNo ratings yet

- Lecture 2. Supply and DemandDocument51 pagesLecture 2. Supply and DemandNoroNo ratings yet

- AssetsDocument17 pagesAssetsChloeNo ratings yet

- Sales Contract EssentialsDocument90 pagesSales Contract EssentialsNoro100% (1)

- I. Nature and Form of The Contract Sources of The Law On SalesDocument20 pagesI. Nature and Form of The Contract Sources of The Law On SalesNoroNo ratings yet

- Pylon CTFDocument7 pagesPylon CTFAleNoAutoPlzNo ratings yet

- Rolando Remy Rivas Diaz: She Went To The Store To Buy A New PhoneDocument2 pagesRolando Remy Rivas Diaz: She Went To The Store To Buy A New PhoneRENZO ALEJANDRO ISMODES LIRANo ratings yet

- Software Engineering Part 1 50 MCQ CEXAMINDIA (1) - UnlockedDocument7 pagesSoftware Engineering Part 1 50 MCQ CEXAMINDIA (1) - UnlockedAditya SharmaNo ratings yet

- E Library ProjectDocument87 pagesE Library ProjectNil WangduNo ratings yet

- EE 260 Lecture 2: Introduction To ArduinoDocument22 pagesEE 260 Lecture 2: Introduction To ArduinoindrahermawanNo ratings yet

- InkZone Perfect: Fast, Affordable Ink Key PresettingDocument2 pagesInkZone Perfect: Fast, Affordable Ink Key PresettingTheJuankyNo ratings yet

- 18CS0501 PPSDocument21 pages18CS0501 PPSKausalya SrinivasNo ratings yet

- Powerware Release 24062002 PW9305-80 kVADocument2 pagesPowerware Release 24062002 PW9305-80 kVARizwan JamilNo ratings yet

- Chapter Three Source Coding: 1-Sampling TheoremDocument19 pagesChapter Three Source Coding: 1-Sampling Theoremعلو الدوريNo ratings yet

- Assignment 2Document8 pagesAssignment 2baknidoknuNo ratings yet

- IELM 511: Information System Design: Part 1. ISD For Well Structured Data - Relational and Other DBMSDocument32 pagesIELM 511: Information System Design: Part 1. ISD For Well Structured Data - Relational and Other DBMSSarita MoreNo ratings yet

- CS: Examination Form: 1.study Group?Document4 pagesCS: Examination Form: 1.study Group?Munteanu DorinNo ratings yet

- Charles Petzold - Programming Windows (6th Edition, Win8)Document294 pagesCharles Petzold - Programming Windows (6th Edition, Win8)Gapesh KumarNo ratings yet

- PX-4226A-A: Owner's ManualDocument38 pagesPX-4226A-A: Owner's ManualFaizall SahbudinNo ratings yet

- ISR 4331 BackupDocument4 pagesISR 4331 BackupPrathvi R SinghNo ratings yet

- Manual NETLink-PRO 5Document67 pagesManual NETLink-PRO 5Carlos Salamanca FartoNo ratings yet

- Integrated Flood Analysis System (IFAS)Document2 pagesIntegrated Flood Analysis System (IFAS)Umer MalikNo ratings yet

- CCTV Service Contracts Provide Peace of MindDocument2 pagesCCTV Service Contracts Provide Peace of MindSaliya DasanayakeNo ratings yet

- Circuitpro PM 2.1 Ab v1.0 EngDocument316 pagesCircuitpro PM 2.1 Ab v1.0 Engmphysics2023No ratings yet

- Computer Science 1Document61 pagesComputer Science 1deepanjal shresthaNo ratings yet

- Ebook PDF Calculus For Biology and Medicine 4th Edition PDFDocument41 pagesEbook PDF Calculus For Biology and Medicine 4th Edition PDFkelly.thomas740100% (29)

- Owners Manual: Aacd #3Document22 pagesOwners Manual: Aacd #3carlos pachecoNo ratings yet

- 2.8M GMAIL ComboDocument5 pages2.8M GMAIL ComboMichael HenryNo ratings yet

- Model 3002: Alpha-Beta Survey MeterDocument1 pageModel 3002: Alpha-Beta Survey MeterAlaa Al HabeesNo ratings yet

- Z50 BrochureDocument2 pagesZ50 Brochureraul100% (1)

- FUNCTIONSDocument16 pagesFUNCTIONSHero KardeşlerNo ratings yet

- Nokia Siemens Networks SGSN SG7.0 Cause DescriptionDocument81 pagesNokia Siemens Networks SGSN SG7.0 Cause DescriptionBibiana TamayoNo ratings yet

- Quick Start Guide Betonwin III EN REL - 1.0Document39 pagesQuick Start Guide Betonwin III EN REL - 1.0Abdullah0% (1)

- ICT and Higher Educational System in NigeriaDocument5 pagesICT and Higher Educational System in NigeriankemoviaNo ratings yet

- Stock Market Analysis and PredictionDocument16 pagesStock Market Analysis and PredictionIndra Kishor Chaudhary AvaiduwaiNo ratings yet