You might also like

- Surviving the Aftermath of Covid-19:How Business Can Survive in the New EraFrom EverandSurviving the Aftermath of Covid-19:How Business Can Survive in the New EraNo ratings yet

- IMF Report Summary 2020Document3 pagesIMF Report Summary 2020JOAONo ratings yet

- Executive SummaryDocument2 pagesExecutive SummaryHerry SusantoNo ratings yet

- Executive Summary: Chapter 1: Fiscal Policies To Address The COVID-19 PandemicDocument3 pagesExecutive Summary: Chapter 1: Fiscal Policies To Address The COVID-19 PandemicVdasilva83No ratings yet

- tdr2021ch1 enDocument44 pagestdr2021ch1 envbn7rdkkntNo ratings yet

- Foreword: Economic Outlook, Are The Main Drivers of This DevelDocument2 pagesForeword: Economic Outlook, Are The Main Drivers of This DevelVdasilva83No ratings yet

- World Economic OutlookDocument6 pagesWorld Economic OutlookRudni MedinaNo ratings yet

- Foreword PDFDocument2 pagesForeword PDFTushar DoshiNo ratings yet

- Ch1 PDFDocument26 pagesCh1 PDFrhizelle19No ratings yet

- The Future of Emerging Markets Duttagupta and PazarbasiogluDocument6 pagesThe Future of Emerging Markets Duttagupta and PazarbasiogluMarkoNo ratings yet

- GEP June 2023 ForewordDocument2 pagesGEP June 2023 ForewordKong CreedNo ratings yet

- World Economic Outlook Update: July 2021Document21 pagesWorld Economic Outlook Update: July 2021ctNo ratings yet

- Covid 19Document6 pagesCovid 19Ngọc Thảo NguyễnNo ratings yet

- The Economic Impact of The PandemicDocument5 pagesThe Economic Impact of The Pandemick.agnes12No ratings yet

- Weoeng202006 PDFDocument20 pagesWeoeng202006 PDFAndrewNo ratings yet

- Chapter 6Document20 pagesChapter 6Nikhil ShuklaNo ratings yet

- Tdr2023ch1 enDocument31 pagesTdr2023ch1 enSuhrobNo ratings yet

- An Empirical Evidence of Economic Recovery During The Pandemic Period Into World EconomyDocument10 pagesAn Empirical Evidence of Economic Recovery During The Pandemic Period Into World EconomyIJAR JOURNALNo ratings yet

- Final Exam-ECO720-2112-1&2 VSDocument4 pagesFinal Exam-ECO720-2112-1&2 VSanurag soniNo ratings yet

- World Economic OutlookDocument6 pagesWorld Economic OutlookKEZIAH REVE B. RODRIGUEZNo ratings yet

- جائحة كوروناDocument17 pagesجائحة كوروناMaEstro MoHamedNo ratings yet

- Global Trends 2020-2025 - KearneyDocument25 pagesGlobal Trends 2020-2025 - KearneySuvam ChakrabartyNo ratings yet

- Eafm - 27 May 2020 - 1600Document11 pagesEafm - 27 May 2020 - 1600emon hossainNo ratings yet

- الاستجابة لأزمة كوفيد-19 في بلدان الشرق الأوسط وشمال أفريقياDocument39 pagesالاستجابة لأزمة كوفيد-19 في بلدان الشرق الأوسط وشمال أفريقياsm3977263No ratings yet

- I. Global Economic ReviewDocument2 pagesI. Global Economic ReviewAhmad IshtiaqNo ratings yet

- Global Financial Stability Report - 2020Document43 pagesGlobal Financial Stability Report - 2020Xara ChamorroNo ratings yet

- IMF Fiscal MonitorDocument42 pagesIMF Fiscal MonitorqonijoNo ratings yet

- Economic and Monetary ReviewDocument133 pagesEconomic and Monetary ReviewAravindAgueroNo ratings yet

- Ketels-Competitiv Upgrading Covid - April 2020Document24 pagesKetels-Competitiv Upgrading Covid - April 2020professionalNo ratings yet

- WORLD ECONOMIC OUTLOOK UPDATE - International Monetary Fund 2021Document11 pagesWORLD ECONOMIC OUTLOOK UPDATE - International Monetary Fund 2021کتابخانه آشنا کتابتونNo ratings yet

- GEP January 2023 ForewordDocument2 pagesGEP January 2023 ForewordDhei MelonNo ratings yet

- Appropriate Policies To Overcome From The Economic Crisis Caused by Covid-19: A Global PerspectiveDocument6 pagesAppropriate Policies To Overcome From The Economic Crisis Caused by Covid-19: A Global Perspectiveemon hossainNo ratings yet

- g20 Report On Strong Sustainable Balanced and Inclusive GrowthDocument24 pagesg20 Report On Strong Sustainable Balanced and Inclusive Growthjohn.tomason29No ratings yet

- Management Discussion and AnalysisDocument36 pagesManagement Discussion and AnalysisVidyashree PNo ratings yet

- Macro - Fiscal Policy AssignmentDocument3 pagesMacro - Fiscal Policy AssignmentAravel Jade Dela CruzNo ratings yet

- ECO720 Group ALP Team 7 - ReportDocument9 pagesECO720 Group ALP Team 7 - ReportRita MaranNo ratings yet

- Budget Overview - of - The - Economy 23Document11 pagesBudget Overview - of - The - Economy 23zubairNo ratings yet

- DBRS Morningstar Changes Trend On Uruguay To Positive, Confirms at BBB (Low)Document11 pagesDBRS Morningstar Changes Trend On Uruguay To Positive, Confirms at BBB (Low)SubrayadoHDNo ratings yet

- Contoh BeritaDocument6 pagesContoh BeritaWindy Marsella ApriliantyNo ratings yet

- WASHINGTON, June 8, 2021 - The Global Economy Is Expected To Expand 5.6%Document3 pagesWASHINGTON, June 8, 2021 - The Global Economy Is Expected To Expand 5.6%Huyền TíttNo ratings yet

- Nurfarhanah Binti Abd Aziz IPE Policy Report - 5521286 6069918 1534314148Document14 pagesNurfarhanah Binti Abd Aziz IPE Policy Report - 5521286 6069918 1534314148Aidah Md SaidNo ratings yet

- 2020, A Global Debt Tidal Wave: April 2020Document5 pages2020, A Global Debt Tidal Wave: April 2020anujNo ratings yet

- Fiscal PolicyDocument7 pagesFiscal PolicySara de la SernaNo ratings yet

- Economic Effects of Covid-19 in Luxembourg First Recovid Working Note With Preliminary EstimatesDocument53 pagesEconomic Effects of Covid-19 in Luxembourg First Recovid Working Note With Preliminary EstimatesShaman WhisperNo ratings yet

- Chief Economists Outlook: Centre For The New Economy and SocietyDocument22 pagesChief Economists Outlook: Centre For The New Economy and SocietycantuscantusNo ratings yet

- Fiscal Sustainability of Assam - 13Document20 pagesFiscal Sustainability of Assam - 13rakesh.rnbdjNo ratings yet

- IMF - United Kingdom - Priazqani RampaditoDocument4 pagesIMF - United Kingdom - Priazqani RampaditoPriazqani RampaditoNo ratings yet

- g20 Minimizing Scarring From The PandemicDocument30 pagesg20 Minimizing Scarring From The PandemicAbdullah BazaNo ratings yet

- Two Major Issues of Fiscal Policy and Potential Harms To The EconomyDocument10 pagesTwo Major Issues of Fiscal Policy and Potential Harms To The Economysue patrickNo ratings yet

- RI - RecoveringandStructuringAfterCOVID19 IssueBrief 202010Document16 pagesRI - RecoveringandStructuringAfterCOVID19 IssueBrief 202010ArgonzNo ratings yet

- Policymakers Need Steady Hand As Storm Clouds Gather Over Global EconomyDocument11 pagesPolicymakers Need Steady Hand As Storm Clouds Gather Over Global EconomyNúriaNo ratings yet

- ExecsumDocument3 pagesExecsumYar Zar AungNo ratings yet

- Lessons For The Private Equity Industry Amidst Rising Global InflationDocument8 pagesLessons For The Private Equity Industry Amidst Rising Global InflationMarcos LalorNo ratings yet

- Pre Budget Report 2021-2022 Final Revised 19 Jan 21Document43 pagesPre Budget Report 2021-2022 Final Revised 19 Jan 21Anonymous UpWci5No ratings yet

- World Economic Outlook: UpdateDocument16 pagesWorld Economic Outlook: UpdateMihai RadulescuNo ratings yet

- Evaluating The Effects of The Economic Response To COVID 19Document79 pagesEvaluating The Effects of The Economic Response To COVID 19Willian CarvalhoNo ratings yet

- Enspecial Series On Covid19monetary and Financial Policy Responses For Emerging Market and DevelopinDocument5 pagesEnspecial Series On Covid19monetary and Financial Policy Responses For Emerging Market and DevelopinAlip FajarNo ratings yet

- UN - Global Green New DealDocument15 pagesUN - Global Green New DealDJNo ratings yet

- Thinking Aloud: Editor's DeskDocument4 pagesThinking Aloud: Editor's Deskসাদিক মাহবুব ইসলামNo ratings yet

- ExecsumDocument2 pagesExecsumKashf ShabbirNo ratings yet

- Five Ways Retail Has Changed and How Businesses Can Adapt - Articles - ZRHMZWV PDFDocument4 pagesFive Ways Retail Has Changed and How Businesses Can Adapt - Articles - ZRHMZWV PDFAgnes DizonNo ratings yet

- 06 Budgeting Problem 20Document4 pages06 Budgeting Problem 20Agnes DizonNo ratings yet

- Sovereign Risk and Natural Disasters in Emerging MarketsDocument17 pagesSovereign Risk and Natural Disasters in Emerging MarketsAgnes DizonNo ratings yet

- Economic Development and Natural Disasters A Satellite Data AnalysisDocument22 pagesEconomic Development and Natural Disasters A Satellite Data AnalysisAgnes DizonNo ratings yet

- Natural Disasters in Developing CountriesDocument37 pagesNatural Disasters in Developing CountriesAgnes DizonNo ratings yet

- 06 Budgeting Theory 40Document4 pages06 Budgeting Theory 40Agnes DizonNo ratings yet

- Natural DisastersDocument17 pagesNatural DisastersPaul BasaNo ratings yet

- Law On Oblicon Identification 2Document3 pagesLaw On Oblicon Identification 2Agnes DizonNo ratings yet

- Oblicon Multiple Choice 3Document2 pagesOblicon Multiple Choice 3Agnes DizonNo ratings yet

- 1/1 Autonomy of ContractsDocument1 page1/1 Autonomy of ContractsAgnes DizonNo ratings yet

- Pure Capitalism: Communism Mixed Economy SocialismDocument2 pagesPure Capitalism: Communism Mixed Economy SocialismAgnes DizonNo ratings yet

- 1/1 IntimidationDocument1 page1/1 IntimidationAgnes DizonNo ratings yet

- FalseDocument2 pagesFalseAgnes DizonNo ratings yet

- Which of The Following Is Not An Ordering Cost?Document2 pagesWhich of The Following Is Not An Ordering Cost?Agnes DizonNo ratings yet

- Relatively Elastic Supply Relatively Inelastic SupplyDocument3 pagesRelatively Elastic Supply Relatively Inelastic SupplyAgnes DizonNo ratings yet

- Heat, Light, and Power Commercial Expenses: Variable Factory OverheadDocument2 pagesHeat, Light, and Power Commercial Expenses: Variable Factory OverheadAgnes DizonNo ratings yet

- Oblicon Multiple Choice 1Document2 pagesOblicon Multiple Choice 1Agnes DizonNo ratings yet

- Costacc Quiz 3Document2 pagesCostacc Quiz 3Agnes DizonNo ratings yet

- Cost MCQ AnsDocument2 pagesCost MCQ AnsAgnes DizonNo ratings yet

- Oblicon Multiple Choice 2Document3 pagesOblicon Multiple Choice 2Agnes DizonNo ratings yet

- Costacc Quiz 1Document2 pagesCostacc Quiz 1Agnes DizonNo ratings yet

- Costacc Quiz 2Document2 pagesCostacc Quiz 2Agnes DizonNo ratings yet

- The Method For Allocating Service Department Costs That Requires The Least Clerical Work IsDocument2 pagesThe Method For Allocating Service Department Costs That Requires The Least Clerical Work IsAgnes DizonNo ratings yet

- 005-Method Statement For FencingDocument6 pages005-Method Statement For FencingEng AliNo ratings yet

- Glossaryof TermsDocument11 pagesGlossaryof Termsjan clyde codasNo ratings yet

- Quiz 2 AbcDocument15 pagesQuiz 2 AbcMa. Lou Erika BALITENo ratings yet

- New Delhi Institute of Management: PGDM 2020-22 Semester-III Paper 2 (Set-B)Document2 pagesNew Delhi Institute of Management: PGDM 2020-22 Semester-III Paper 2 (Set-B)bhushanNo ratings yet

- 1 Session - Overfiew of FSADocument45 pages1 Session - Overfiew of FSAAbhishek SwarnkarNo ratings yet

- RLB Profile Nov'19 PDFDocument16 pagesRLB Profile Nov'19 PDFGoli Boy dot comNo ratings yet

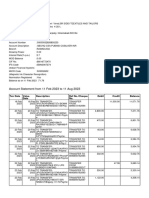

- Account Statement From 11 Feb 2023 To 11 Aug 2023Document8 pagesAccount Statement From 11 Feb 2023 To 11 Aug 2023vinodbommadeniNo ratings yet

- UNIT IV Material ManagementDocument3 pagesUNIT IV Material ManagementHIMANSHU DARGANNo ratings yet

- ALERT LIST (Asof 24october2023) - EnglishDocument14 pagesALERT LIST (Asof 24october2023) - EnglishLuqman MohammadNo ratings yet

- Instrument of Transfer SampleDocument1 pageInstrument of Transfer Samplehazel_tm0% (1)

- Pemenang Lomba Karya Ilmiah Stabilitas Sistem Keuangan 2021Document2 pagesPemenang Lomba Karya Ilmiah Stabilitas Sistem Keuangan 2021Rezha Nursina YuniNo ratings yet

- "A Study On The Financial Performance of Hindustan Unilever Limited"Document60 pages"A Study On The Financial Performance of Hindustan Unilever Limited"career pathNo ratings yet

- FILE - 20211108 - 150658 - Unit 4 - Supplementary ExercisesDocument4 pagesFILE - 20211108 - 150658 - Unit 4 - Supplementary ExercisesNguyen T. Tú AnhNo ratings yet

- Lesson 05 - Fiscal Policy and StabilizationDocument48 pagesLesson 05 - Fiscal Policy and StabilizationMetoo ChyNo ratings yet

- 2021 OctDocument64 pages2021 OctAhm Ferdous100% (1)

- Supplier Business Plan 1Document10 pagesSupplier Business Plan 1Bipana SapkotaNo ratings yet

- 500 WordsDocument2 pages500 WordsKristyl Ivy PingolNo ratings yet

- Characteristics of Competitive Markets The Mode... - Chegg - ComhhDocument3 pagesCharacteristics of Competitive Markets The Mode... - Chegg - ComhhBLESSEDNo ratings yet

- Asian RegionalismDocument18 pagesAsian RegionalismJewdaly Lagasca Costales60% (10)

- Tarc Acc t4Document2 pagesTarc Acc t4Shirley VunNo ratings yet

- Cbse Ix-X Social Science 2022-23 PisDocument52 pagesCbse Ix-X Social Science 2022-23 PisAditi JaniNo ratings yet

- Road Maintenance in Nepal - Most Neglected Aspect - The Himalayan TimesDocument3 pagesRoad Maintenance in Nepal - Most Neglected Aspect - The Himalayan TimesShambhu SahNo ratings yet

- 56148917999019339Document2 pages56148917999019339gajendraNo ratings yet

- Plastic Storage ContainerDocument1 pagePlastic Storage ContainerSanjhanaNo ratings yet

- International Trade Barriers: By: Sugandh MittalDocument7 pagesInternational Trade Barriers: By: Sugandh MittalnoorNo ratings yet

- Chap 4 Managing in The Global ArenaDocument13 pagesChap 4 Managing in The Global Arenaamer DanounNo ratings yet

- Lecture 1-3Document3 pagesLecture 1-3Riot SkinNo ratings yet

- Project 4Document16 pagesProject 4Jai GauravNo ratings yet

- WazirX Competitive LandscapeDocument7 pagesWazirX Competitive Landscapevenkatesh.iyer1989No ratings yet

- Collection Disbursement ReportDocument6 pagesCollection Disbursement Reportmkmohit991No ratings yet

- Stonewalled: My Fight for Truth Against the Forces of Obstruction, Intimidation, and Harassment in Obama's WashingtonFrom EverandStonewalled: My Fight for Truth Against the Forces of Obstruction, Intimidation, and Harassment in Obama's WashingtonRating: 4.5 out of 5 stars4.5/5 (21)

- The Courage to Be Free: Florida's Blueprint for America's RevivalFrom EverandThe Courage to Be Free: Florida's Blueprint for America's RevivalNo ratings yet

- The Smear: How Shady Political Operatives and Fake News Control What You See, What You Think, and How You VoteFrom EverandThe Smear: How Shady Political Operatives and Fake News Control What You See, What You Think, and How You VoteRating: 4.5 out of 5 stars4.5/5 (16)

- The Russia Hoax: The Illicit Scheme to Clear Hillary Clinton and Frame Donald TrumpFrom EverandThe Russia Hoax: The Illicit Scheme to Clear Hillary Clinton and Frame Donald TrumpRating: 4.5 out of 5 stars4.5/5 (11)

- Thomas Jefferson: Author of AmericaFrom EverandThomas Jefferson: Author of AmericaRating: 4 out of 5 stars4/5 (107)

- Modern Warriors: Real Stories from Real HeroesFrom EverandModern Warriors: Real Stories from Real HeroesRating: 3.5 out of 5 stars3.5/5 (3)

- Commander In Chief: FDR's Battle with Churchill, 1943From EverandCommander In Chief: FDR's Battle with Churchill, 1943Rating: 4 out of 5 stars4/5 (16)

- Nine Black Robes: Inside the Supreme Court's Drive to the Right and Its Historic ConsequencesFrom EverandNine Black Robes: Inside the Supreme Court's Drive to the Right and Its Historic ConsequencesNo ratings yet

- Crimes and Cover-ups in American Politics: 1776-1963From EverandCrimes and Cover-ups in American Politics: 1776-1963Rating: 4.5 out of 5 stars4.5/5 (26)

- Game Change: Obama and the Clintons, McCain and Palin, and the Race of a LifetimeFrom EverandGame Change: Obama and the Clintons, McCain and Palin, and the Race of a LifetimeRating: 4 out of 5 stars4/5 (572)

- The Shadow War: Inside Russia's and China's Secret Operations to Defeat AmericaFrom EverandThe Shadow War: Inside Russia's and China's Secret Operations to Defeat AmericaRating: 4.5 out of 5 stars4.5/5 (12)

- The Great Gasbag: An A–Z Study Guide to Surviving Trump WorldFrom EverandThe Great Gasbag: An A–Z Study Guide to Surviving Trump WorldRating: 3.5 out of 5 stars3.5/5 (9)

- The Quiet Man: The Indispensable Presidency of George H.W. BushFrom EverandThe Quiet Man: The Indispensable Presidency of George H.W. BushRating: 4 out of 5 stars4/5 (1)

- An Ordinary Man: The Surprising Life and Historic Presidency of Gerald R. FordFrom EverandAn Ordinary Man: The Surprising Life and Historic Presidency of Gerald R. FordRating: 4 out of 5 stars4/5 (5)

- Power Grab: The Liberal Scheme to Undermine Trump, the GOP, and Our RepublicFrom EverandPower Grab: The Liberal Scheme to Undermine Trump, the GOP, and Our RepublicNo ratings yet

- Witch Hunt: The Story of the Greatest Mass Delusion in American Political HistoryFrom EverandWitch Hunt: The Story of the Greatest Mass Delusion in American Political HistoryRating: 4 out of 5 stars4/5 (6)

- The Red and the Blue: The 1990s and the Birth of Political TribalismFrom EverandThe Red and the Blue: The 1990s and the Birth of Political TribalismRating: 4 out of 5 stars4/5 (29)

- We've Got Issues: How You Can Stand Strong for America's Soul and SanityFrom EverandWe've Got Issues: How You Can Stand Strong for America's Soul and SanityNo ratings yet

- Socialism 101: From the Bolsheviks and Karl Marx to Universal Healthcare and the Democratic Socialists, Everything You Need to Know about SocialismFrom EverandSocialism 101: From the Bolsheviks and Karl Marx to Universal Healthcare and the Democratic Socialists, Everything You Need to Know about SocialismRating: 4.5 out of 5 stars4.5/5 (42)

- The Deep State: How an Army of Bureaucrats Protected Barack Obama and Is Working to Destroy the Trump AgendaFrom EverandThe Deep State: How an Army of Bureaucrats Protected Barack Obama and Is Working to Destroy the Trump AgendaRating: 4.5 out of 5 stars4.5/5 (4)

- The Magnificent Medills: The McCormick-Patterson Dynasty: America's Royal Family of Journalism During a Century of Turbulent SplendorFrom EverandThe Magnificent Medills: The McCormick-Patterson Dynasty: America's Royal Family of Journalism During a Century of Turbulent SplendorNo ratings yet

- Confidence Men: Wall Street, Washington, and the Education of a PresidentFrom EverandConfidence Men: Wall Street, Washington, and the Education of a PresidentRating: 3.5 out of 5 stars3.5/5 (52)

- Hatemonger: Stephen Miller, Donald Trump, and the White Nationalist AgendaFrom EverandHatemonger: Stephen Miller, Donald Trump, and the White Nationalist AgendaRating: 4 out of 5 stars4/5 (5)

- Camelot's Court: Inside the Kennedy White HouseFrom EverandCamelot's Court: Inside the Kennedy White HouseRating: 4 out of 5 stars4/5 (17)

- A Short History of the United States: From the Arrival of Native American Tribes to the Obama PresidencyFrom EverandA Short History of the United States: From the Arrival of Native American Tribes to the Obama PresidencyRating: 3.5 out of 5 stars3.5/5 (19)

- Reading the Constitution: Why I Chose Pragmatism, not TextualismFrom EverandReading the Constitution: Why I Chose Pragmatism, not TextualismNo ratings yet

- The Science of Liberty: Democracy, Reason, and the Laws of NatureFrom EverandThe Science of Liberty: Democracy, Reason, and the Laws of NatureNo ratings yet

- The Last Republicans: Inside the Extraordinary Relationship Between George H.W. Bush and George W. BushFrom EverandThe Last Republicans: Inside the Extraordinary Relationship Between George H.W. Bush and George W. BushRating: 4 out of 5 stars4/5 (6)