You might also like

- Discrete Time Random Processes: 4.1 (A) UsingDocument16 pagesDiscrete Time Random Processes: 4.1 (A) UsingSudipta GhoshNo ratings yet

- Assignment 1: 1. Example SectionDocument3 pagesAssignment 1: 1. Example SectionYonas D. EbrenNo ratings yet

- Optmization Network For Matrix InversionDocument5 pagesOptmization Network For Matrix InversionSameeraBharadwajaHNo ratings yet

- 6.21, 7.3, 7.4 - 103046Document3 pages6.21, 7.3, 7.4 - 103046shela malaNo ratings yet

- Controls Problems For Qualifying Exam - Spring 2014: Problem 1Document11 pagesControls Problems For Qualifying Exam - Spring 2014: Problem 1MnshNo ratings yet

- Libro Fasshauer Numerico AvanzadoDocument151 pagesLibro Fasshauer Numerico AvanzadoCarlysMendozaamorNo ratings yet

- Haykin, Xue-Neural Networks and Learning Machines 3ed SolnDocument103 pagesHaykin, Xue-Neural Networks and Learning Machines 3ed Solnsticker59253% (17)

- Ch6 Slides Ed3 Feb2021Document63 pagesCh6 Slides Ed3 Feb2021Phuc Hong PhamNo ratings yet

- Complex Eigenvalue and EigenvectorDocument5 pagesComplex Eigenvalue and EigenvectorlostkinNo ratings yet

- Aashikpelokhai and MomoduDocument7 pagesAashikpelokhai and MomoduSandaMohdNo ratings yet

- Spektralna Teorija 1dfDocument64 pagesSpektralna Teorija 1dfEmir BahtijarevicNo ratings yet

- PSA. Part 2Document22 pagesPSA. Part 2SachinNo ratings yet

- Adaptive Predictor Computer ExperimentsDocument9 pagesAdaptive Predictor Computer ExperimentsushapvermaNo ratings yet

- EE 4443/4329 - Control Systems Design Project: Updated:Tuesday, June 15, 2004Document6 pagesEE 4443/4329 - Control Systems Design Project: Updated:Tuesday, June 15, 2004bcooper477No ratings yet

- Chapter 01Document20 pagesChapter 01Engr Kamran JavedNo ratings yet

- MM HA3 SolutionDocument21 pagesMM HA3 SolutionVojvodaAlbertNo ratings yet

- TS PartIIDocument50 pagesTS PartIIأبوسوار هندسةNo ratings yet

- 22 4 Numrcl Detrmntn Eignvl EignvcDocument8 pages22 4 Numrcl Detrmntn Eignvl EignvcDaniel SolhNo ratings yet

- Vectors and Matrices, Problem Set 2Document3 pagesVectors and Matrices, Problem Set 2Edgardo Jose RearioNo ratings yet

- Vectors and Matrices, Problem Set 2Document3 pagesVectors and Matrices, Problem Set 2Roy VeseyNo ratings yet

- 10.1007@s11785 019 00924 ZDocument19 pages10.1007@s11785 019 00924 ZKarwan JwamerNo ratings yet

- TT IimDocument106 pagesTT IimrakeshNo ratings yet

- 630 Rec Part2 Sol PDFDocument9 pages630 Rec Part2 Sol PDFboggled429No ratings yet

- 6.003 Homework 3: ProblemsDocument4 pages6.003 Homework 3: ProblemsIsrael SmithNo ratings yet

- Eigen VectorsDocument8 pagesEigen VectorsRakesh S KNo ratings yet

- Sol6 PDFDocument8 pagesSol6 PDFMichael ARKNo ratings yet

- Discrete Structure Chapter 6-Recurrence RelationDocument38 pagesDiscrete Structure Chapter 6-Recurrence Relationrockers91No ratings yet

- A01 Exam1 - 2013Document8 pagesA01 Exam1 - 2013Talha EtnerNo ratings yet

- Sturm-Liouville Eigenvalue ProblemsDocument7 pagesSturm-Liouville Eigenvalue Problemshammoudeh13No ratings yet

- Practice 6 8Document12 pagesPractice 6 8Marisnelvys CabrejaNo ratings yet

- A Unified Approach For Designing CapacitDocument6 pagesA Unified Approach For Designing CapacitMehmet AKBABANo ratings yet

- Course: Digital Control (CS416) Sheet No.: 1 Date: 27/10/2021 Due: 3/11/2021 Time: 2 HoursDocument7 pagesCourse: Digital Control (CS416) Sheet No.: 1 Date: 27/10/2021 Due: 3/11/2021 Time: 2 HoursAhmed NourNo ratings yet

- A Method For Numerical Integration: by C. B. HaselgroveDocument15 pagesA Method For Numerical Integration: by C. B. HaselgroveAbid MullaNo ratings yet

- Schwarz-Christoffel Transformation On A Half Plane: Abdualah Ibrahim SultanDocument5 pagesSchwarz-Christoffel Transformation On A Half Plane: Abdualah Ibrahim Sultanwww.irjes.comNo ratings yet

- Review of Properties of Eigenvalues and EigenvectorsDocument11 pagesReview of Properties of Eigenvalues and EigenvectorsLaxman Naidu NNo ratings yet

- Computer Exercises in Adaptive FiltersDocument11 pagesComputer Exercises in Adaptive FiltersushapvermaNo ratings yet

- Midsem Regular MFDS 22-12-2019 Answer Key PDFDocument5 pagesMidsem Regular MFDS 22-12-2019 Answer Key PDFBalwant SinghNo ratings yet

- Eigenvalues and Eigenvectors: NG Tin Yau (PHD)Document38 pagesEigenvalues and Eigenvectors: NG Tin Yau (PHD)Lam WongNo ratings yet

- GEM 802 Chapter 1Document52 pagesGEM 802 Chapter 1Leah Ann ManuelNo ratings yet

- Quantum Harmonic Oscillator, A Computational ApproachDocument6 pagesQuantum Harmonic Oscillator, A Computational ApproachIOSRjournalNo ratings yet

- Real Analysis Problem SolutionDocument6 pagesReal Analysis Problem SolutionAparajeeta GuhaNo ratings yet

- LA EigenvaluesDocument27 pagesLA EigenvaluesMuhammad HamdanNo ratings yet

- EM May 2021Document3 pagesEM May 2021Shivam YadavNo ratings yet

- Homework02 Withsolutions 1 PDFDocument5 pagesHomework02 Withsolutions 1 PDFVarmenUchihaNo ratings yet

- Matlab Tutorial of Modelling of A Slider Crank MechanismDocument14 pagesMatlab Tutorial of Modelling of A Slider Crank MechanismTrolldaddyNo ratings yet

- Appendix: University of California, BerkeleyDocument14 pagesAppendix: University of California, BerkeleycNo ratings yet

- 2.2.1 A Solution Method: 2.3 Row Operations and Equivalent SystemsDocument139 pages2.2.1 A Solution Method: 2.3 Row Operations and Equivalent SystemsDaniel DadaNo ratings yet

- Evaluating Some Yule-Walker Methods With The Maximum-Likelihood Estimator For The Spectral ARMA ModelDocument10 pagesEvaluating Some Yule-Walker Methods With The Maximum-Likelihood Estimator For The Spectral ARMA ModelAdrian Jose Costa OspinoNo ratings yet

- 172 421 1 SMDocument10 pages172 421 1 SMJogo da VelhaNo ratings yet

- QM1 Problem Set 1 Solutions - Mike SaelimDocument5 pagesQM1 Problem Set 1 Solutions - Mike SaelimryzesyaaNo ratings yet

- Degree in Data Science and Engineering Group 96/196 Linear Algebra. Test 2. December 9, 2020Document4 pagesDegree in Data Science and Engineering Group 96/196 Linear Algebra. Test 2. December 9, 2020Beatriz IzquierdoNo ratings yet

- KLT ExampleDocument5 pagesKLT ExampledeepuNo ratings yet

- Numerical Solution Methods: 3.1.1 Matrices and Vectors in FortranDocument9 pagesNumerical Solution Methods: 3.1.1 Matrices and Vectors in FortranLucas SantosNo ratings yet

- hw8 Solns PDFDocument7 pageshw8 Solns PDFDon QuixoteNo ratings yet

- My Thirds em ReportDocument21 pagesMy Thirds em ReportMassDuttNo ratings yet

- ME 361-EigenvaluesDocument22 pagesME 361-EigenvaluesYigit YAMANNo ratings yet

- Cubic Spline AssignmentDocument12 pagesCubic Spline AssignmentFarhan EllahiNo ratings yet

- Tutorial 4: Determinants and Linear TransformationsDocument5 pagesTutorial 4: Determinants and Linear TransformationsJustin Del CampoNo ratings yet

- Difference Equations in Normed Spaces: Stability and OscillationsFrom EverandDifference Equations in Normed Spaces: Stability and OscillationsNo ratings yet

- Advanced Numerical and Semi-Analytical Methods for Differential EquationsFrom EverandAdvanced Numerical and Semi-Analytical Methods for Differential EquationsNo ratings yet

- Exercise A: Confine Space AssessmentDocument7 pagesExercise A: Confine Space AssessmentMohammad Sohel100% (1)

- Service Bulletin: SubjectDocument6 pagesService Bulletin: SubjectWaitylla DiasNo ratings yet

- Soalan Sebenar Sejarah STPM Penggal 2 PDFDocument1 pageSoalan Sebenar Sejarah STPM Penggal 2 PDFFatins FilzaNo ratings yet

- Fs Project ReportDocument50 pagesFs Project Reportfizzy thingsNo ratings yet

- Facial RecognitionDocument5 pagesFacial RecognitionPeterNo ratings yet

- The Cybersecurity Sorcery Cube Scatter Quizlet - Gonzalez Garcia GabrielDocument3 pagesThe Cybersecurity Sorcery Cube Scatter Quizlet - Gonzalez Garcia GabrielSharon AlvarezNo ratings yet

- Final Project Template V2 1Document46 pagesFinal Project Template V2 1HUY NGUYEN QUOCNo ratings yet

- 7.2kV Current Transformer - WH3Document2 pages7.2kV Current Transformer - WH3Sandhi YudiyantoNo ratings yet

- Series Al5000 Light Tower: Operation/Service & Parts ManualDocument64 pagesSeries Al5000 Light Tower: Operation/Service & Parts ManualJovanNo ratings yet

- Teachers Program - Six SectionsDocument44 pagesTeachers Program - Six SectionsAce Dela Cruz EnriquezNo ratings yet

- Sundaram ClaytonDocument207 pagesSundaram ClaytonReTHINK INDIANo ratings yet

- VerilatorDocument224 pagesVerilatorGolnaz KorkianNo ratings yet

- Indian Institute of Technology: Delhi Summary Sheet Consumable StoresDocument2 pagesIndian Institute of Technology: Delhi Summary Sheet Consumable StoresSumit SinghNo ratings yet

- SBC10 v2 X Rev0 1Document2 pagesSBC10 v2 X Rev0 1okebNo ratings yet

- NAVEEN Final Project 2Document83 pagesNAVEEN Final Project 2syed bismillahNo ratings yet

- Research in MathDocument6 pagesResearch in MathJohn David YuNo ratings yet

- Reliability and Its Application in TQMDocument15 pagesReliability and Its Application in TQMVijay Anand50% (2)

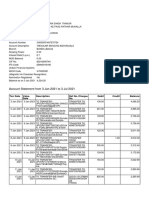

- Account Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument8 pagesAccount Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSanatan ThakurNo ratings yet

- Ecrin 4.0 - Petro BlogDocument4 pagesEcrin 4.0 - Petro BlogReynold AvgNo ratings yet

- SGV Series: Storage Filling PumpDocument2 pagesSGV Series: Storage Filling PumpAnupam MehraNo ratings yet

- Spun Pipe RCC Pipe Hume PipeDocument1 pageSpun Pipe RCC Pipe Hume PipeAbhiishek SinghNo ratings yet

- Ibs Kota Bharu 1 30/06/22Document7 pagesIbs Kota Bharu 1 30/06/22Nik Suraya IbrahimNo ratings yet

- Analytics-Based Investigation & Automated Response With AWS + Splunk Security SolutionsDocument37 pagesAnalytics-Based Investigation & Automated Response With AWS + Splunk Security SolutionsWesly SibagariangNo ratings yet

- Logistics ManagementDocument2 pagesLogistics ManagementJohn Paul BarotNo ratings yet

- Catamsia 9.0 Cara InstallDocument2 pagesCatamsia 9.0 Cara InstalljohnsonNo ratings yet

- All Worksheets MYSQLDocument33 pagesAll Worksheets MYSQLSample1No ratings yet

- Compressor House Unit-3Document199 pagesCompressor House Unit-3Priyanka BasuNo ratings yet

- Income Tax Calulator With Functions and Robus Validation: PFC - Assignment - Part 1Document4 pagesIncome Tax Calulator With Functions and Robus Validation: PFC - Assignment - Part 1tran nguyenNo ratings yet

- CAAM-Drone Requirement 2020Document6 pagesCAAM-Drone Requirement 2020nasser4858No ratings yet

- Construction Planning and SchedulingDocument70 pagesConstruction Planning and SchedulingDessalegn AyenewNo ratings yet