You might also like

- Financial Statement Analysis: Business Strategy & Competitive AdvantageFrom EverandFinancial Statement Analysis: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Chapter 07 Futures and OptiDocument68 pagesChapter 07 Futures and OptiLia100% (1)

- Fundamental Analysis Black BookDocument46 pagesFundamental Analysis Black Bookwagha25% (4)

- Michael Porter's Value Chain: Unlock your company's competitive advantageFrom EverandMichael Porter's Value Chain: Unlock your company's competitive advantageRating: 4 out of 5 stars4/5 (1)

- CFA RC Equity Research Report EssentialsDocument3 pagesCFA RC Equity Research Report EssentialsSahil GoyalNo ratings yet

- KKR Overview and Organizational SummaryDocument73 pagesKKR Overview and Organizational SummaryRavi Chaurasia100% (3)

- Fundamental vs Technical Analysis Key DifferencesDocument12 pagesFundamental vs Technical Analysis Key DifferencesShakti ShuklaNo ratings yet

- ListDocument8 pagesListLuis RodríguezNo ratings yet

- Monetary EconomicsDocument14 pagesMonetary EconomicsMarco Antonio Tumiri López0% (3)

- Commercial Account FormDocument19 pagesCommercial Account FormSimonNo ratings yet

- Financial Statement Analysis, Balance Sheet, Income Statement, Retained Earnings StatementDocument51 pagesFinancial Statement Analysis, Balance Sheet, Income Statement, Retained Earnings StatementMara LacsamanaNo ratings yet

- Fundamental Analysis of ICICI BankDocument79 pagesFundamental Analysis of ICICI BanksantumandalNo ratings yet

- Unit 3Document21 pagesUnit 3InduSaran AttadaNo ratings yet

- Fundamental Analysis Principles, Types, and How To Use It $$$$$Document8 pagesFundamental Analysis Principles, Types, and How To Use It $$$$$ACC200 MNo ratings yet

- Company AnalysisDocument84 pagesCompany AnalysisShantnu SoodNo ratings yet

- Fundamental AnalysisDocument7 pagesFundamental AnalysisJyothi Kruthi PanduriNo ratings yet

- Fundamental Analysis Black BookDocument50 pagesFundamental Analysis Black Bookwagha100% (1)

- IUJ Math Aptitude Test - Sample 4Document7 pagesIUJ Math Aptitude Test - Sample 4Tigist TayeNo ratings yet

- Business ValuationDocument16 pagesBusiness Valuationsangya01No ratings yet

- RHB Account Terms and ConditionsDocument29 pagesRHB Account Terms and ConditionsLeong Liang TingNo ratings yet

- Fundamental Analysis of TATA MOTORSDocument4 pagesFundamental Analysis of TATA MOTORSNikher Verma100% (1)

- Fundamental Analysis: Stock Trading Analysis/IndicatorsDocument5 pagesFundamental Analysis: Stock Trading Analysis/IndicatorsAngie LeeNo ratings yet

- Equity Research - An Investment Advisory Service (Fundamental Analysis Approach)Document5 pagesEquity Research - An Investment Advisory Service (Fundamental Analysis Approach)rockyrrNo ratings yet

- Fundamental Analysis of ICICI BankDocument70 pagesFundamental Analysis of ICICI BankAnonymous TduRDX9JMh0% (1)

- WEALTH MANAGEMENT PROJECTDocument24 pagesWEALTH MANAGEMENT PROJECTshrishtiNo ratings yet

- Chapter Five Security Analysis and ValuationDocument66 pagesChapter Five Security Analysis and ValuationKume MezgebuNo ratings yet

- Strategy Consulting GuideDocument13 pagesStrategy Consulting Guideujjwal sethNo ratings yet

- Strategy and Consulting Domain: Gd-Pi Preparation CompendiumDocument13 pagesStrategy and Consulting Domain: Gd-Pi Preparation Compendiumujjwal sethNo ratings yet

- Equity ValuationDocument17 pagesEquity ValuationAadesh MunotNo ratings yet

- Business Valuation: Economic ConditionsDocument10 pagesBusiness Valuation: Economic ConditionscuteheenaNo ratings yet

- We TubeDocument38 pagesWe TubeGaurav ChikhalikarNo ratings yet

- Valuation of BusinessDocument9 pagesValuation of BusinessShiv SharmaNo ratings yet

- SAPM - Security AnalysisDocument7 pagesSAPM - Security AnalysisTyson Texeira100% (1)

- Fundamental of ValuationDocument39 pagesFundamental of Valuationkristeen1211No ratings yet

- Business ValuationDocument5 pagesBusiness ValuationPulkitAgrawalNo ratings yet

- What Is Vertical IntegrationDocument5 pagesWhat Is Vertical IntegrationNyadroh Clement MchammondsNo ratings yet

- RC Equity Research Report Essentials CFA InstituteDocument3 pagesRC Equity Research Report Essentials CFA InstitutetheakjNo ratings yet

- Reading 24 - Equity Valuation - Applications and ProcessesDocument5 pagesReading 24 - Equity Valuation - Applications and ProcessesJuan MatiasNo ratings yet

- Reviewer FMDocument8 pagesReviewer FMTHRISHIA ANN SOLIVANo ratings yet

- Fundamental AnalysisDocument4 pagesFundamental Analysisgabby209No ratings yet

- Fundamental Analysis of FMCG Companies. (New)Document67 pagesFundamental Analysis of FMCG Companies. (New)AKKI REDDYNo ratings yet

- Comparative IT Company ValuationDocument5 pagesComparative IT Company ValuationVarsha BhatiaNo ratings yet

- BBA5 Fundamental Analysis of Investment ManagementDocument7 pagesBBA5 Fundamental Analysis of Investment Managementgorang GehaniNo ratings yet

- Strategy - Chapter 3: Can A Firm Develop Strategies That Influence Industry Structure in Order To Moderate Competition?Document8 pagesStrategy - Chapter 3: Can A Firm Develop Strategies That Influence Industry Structure in Order To Moderate Competition?Tang WillyNo ratings yet

- Fundamental AnalysisDocument6 pagesFundamental Analysisumasahithi91No ratings yet

- Executive SummaryDocument63 pagesExecutive SummarymaisamNo ratings yet

- Strategy Is A Pattern of Activities That Seeks To Achieve The Objectives ofDocument5 pagesStrategy Is A Pattern of Activities That Seeks To Achieve The Objectives ofPriya NairNo ratings yet

- Fundamental Analysis 12Document5 pagesFundamental Analysis 12Pranay KolarkarNo ratings yet

- Product Management Unit IIIDocument32 pagesProduct Management Unit IIIKevinNo ratings yet

- MDI GDPI Prep - StrategyDocument10 pagesMDI GDPI Prep - StrategyDevavrat SinghNo ratings yet

- Presented by - Snibdhatambe, 11 Shreeti Daddha, 09 (Bvimsr)Document39 pagesPresented by - Snibdhatambe, 11 Shreeti Daddha, 09 (Bvimsr)Daddha ShreetiNo ratings yet

- Fundamental Analysis - WikipediaDocument21 pagesFundamental Analysis - WikipediaNaman JindalNo ratings yet

- The Industry AnalysisDocument6 pagesThe Industry AnalysisNicoleNo ratings yet

- Strategic Management Concepts ExplainedDocument9 pagesStrategic Management Concepts ExplainedAnil KumarNo ratings yet

- What Is Fundamental AnalysisDocument13 pagesWhat Is Fundamental AnalysisvishnucnkNo ratings yet

- Fundamental AnalysisDocument8 pagesFundamental AnalysisNiño Rey LopezNo ratings yet

- Chapter 6 Comparable Companies AnalysisDocument46 pagesChapter 6 Comparable Companies AnalysisLAMOUCHI RIMNo ratings yet

- AbcdDocument3 pagesAbcdAshwin NairNo ratings yet

- Marketing Management AssignmentDocument32 pagesMarketing Management Assignmentwerksew tsegayeNo ratings yet

- Reviewer Compre 1Document30 pagesReviewer Compre 1Dexter AlcantaraNo ratings yet

- Efficient Market Hypothesis AssingmentDocument5 pagesEfficient Market Hypothesis AssingmentJohn P ReddenNo ratings yet

- Porter's Five Forces That Shape IndustryDocument8 pagesPorter's Five Forces That Shape IndustryLaong laanNo ratings yet

- Chapter 5Document9 pagesChapter 5NadineNo ratings yet

- What Is 'Fundamental Analysis': Intrinsic Value Macroeconomic Factors Current PriceDocument9 pagesWhat Is 'Fundamental Analysis': Intrinsic Value Macroeconomic Factors Current Pricedhwani100% (1)

- Financial Statement Analysis Study Resource for CIMA & ACCA Students: CIMA Study ResourcesFrom EverandFinancial Statement Analysis Study Resource for CIMA & ACCA Students: CIMA Study ResourcesNo ratings yet

- The Pros and Cons of GrexitDocument4 pagesThe Pros and Cons of GrexitTanay ChitreNo ratings yet

- Chapter 1636Document30 pagesChapter 1636MJ39No ratings yet

- Snapshot Ed General Presentation DisclosuresDocument20 pagesSnapshot Ed General Presentation DisclosuresAsad MuhammadNo ratings yet

- Assigment Financial ManagementDocument5 pagesAssigment Financial ManagementMuhammad A IsmaielNo ratings yet

- Chapter 1 Evolution and Fundamental of BusinessDocument211 pagesChapter 1 Evolution and Fundamental of BusinessDr. Nidhi KumariNo ratings yet

- Booking 1062381456Document2 pagesBooking 1062381456Deni SetiawanNo ratings yet

- Intermediate Accounting IFRS Edition: Kieso, Weygandt, WarfieldDocument20 pagesIntermediate Accounting IFRS Edition: Kieso, Weygandt, Warfielddystopian au.No ratings yet

- Musharaka Accounting AgendaDocument32 pagesMusharaka Accounting AgendamohamedNo ratings yet

- Chapter 1 Textbook NotesDocument16 pagesChapter 1 Textbook NotesAhmed SohailNo ratings yet

- 22 2Q Earning Release of LGEDocument18 pages22 2Q Earning Release of LGEThảo VũNo ratings yet

- Circular No. 102-2012-TT-BTC - Per-Diem For Overseas Business Trip - ENGDocument20 pagesCircular No. 102-2012-TT-BTC - Per-Diem For Overseas Business Trip - ENGLê Đình ChinhNo ratings yet

- Mobile Services: Your Account Summary This Month'S ChargesDocument2 pagesMobile Services: Your Account Summary This Month'S ChargesShahidNo ratings yet

- Makalah Bahasa Inggris-1Document8 pagesMakalah Bahasa Inggris-1NajwaNo ratings yet

- Acct Statement - XX6419 - 08112022Document26 pagesAcct Statement - XX6419 - 08112022AartiNo ratings yet

- Investing in Fixed Income SecuritiesDocument16 pagesInvesting in Fixed Income Securitiescao cao100% (1)

- Account Management Agreement - Agreed Form 18mar11-1Document17 pagesAccount Management Agreement - Agreed Form 18mar11-1UltimanoticiasNo ratings yet

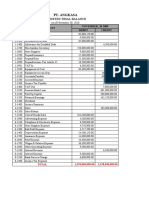

- Kerja Kelompok PT Angkasa BDocument28 pagesKerja Kelompok PT Angkasa BElisa EndrianiiNo ratings yet

- Gov't Assistance, Subsidies, & Impacts on BusinessDocument12 pagesGov't Assistance, Subsidies, & Impacts on BusinessHassaan UmerNo ratings yet

- Pro Forma Balance Sheet Template: Company NameDocument5 pagesPro Forma Balance Sheet Template: Company NamePhương ĐinhNo ratings yet

- Accounts - Module 2 Books and Trial BalanceDocument18 pagesAccounts - Module 2 Books and Trial Balance9986212378No ratings yet

- IS Milan New Student Fees 23 24Document1 pageIS Milan New Student Fees 23 24Bharani DhanasekarNo ratings yet

- Cigicon 2015 BrochureDocument2 pagesCigicon 2015 Brochuredrjas007No ratings yet

- Financial Management Test 1 - DistanceDocument2 pagesFinancial Management Test 1 - DistancePdoneeverNo ratings yet