You might also like

- Celex 32014L0065 enDocument148 pagesCelex 32014L0065 enMarketsWikiNo ratings yet

- Synthetic Securitisation RegulationDocument24 pagesSynthetic Securitisation Regulationjohn pynchonNo ratings yet

- Celex 02021R2268-20220714 en TXTDocument49 pagesCelex 02021R2268-20220714 en TXTmiguel.anicetoNo ratings yet

- Esma70-708036281-18 Opinion On Portfolio MarginingDocument6 pagesEsma70-708036281-18 Opinion On Portfolio MarginingPrateek GoelNo ratings yet

- Delegated Regulation 2020 447Document3 pagesDelegated Regulation 2020 447john pynchonNo ratings yet

- Brenncke, SSRNDocument87 pagesBrenncke, SSRNMathias BinnekNo ratings yet

- EC Delegated Reg On STS Notification For Synthetic Sec - C (2022) 1892 FinalDocument6 pagesEC Delegated Reg On STS Notification For Synthetic Sec - C (2022) 1892 FinalbenteuxNo ratings yet

- Esma70-151-3076 CP On Gls On Review Evaluation Eu Ccps 0Document36 pagesEsma70-151-3076 CP On Gls On Review Evaluation Eu Ccps 0Oana Dumitrascu MarinoiuNo ratings yet

- European ComissionDocument14 pagesEuropean ComissionurkerNo ratings yet

- Guidelines: On Liquidity Stress Testing in Ucits and AifsDocument21 pagesGuidelines: On Liquidity Stress Testing in Ucits and AifsFabio PolpettiniNo ratings yet

- DOUE - 20190607 - Directive 879-2019 - Amending 54-2019 (BRRD2) - Consolidated VersionDocument207 pagesDOUE - 20190607 - Directive 879-2019 - Amending 54-2019 (BRRD2) - Consolidated VersionAlbert García GarcíaNo ratings yet

- ESMA75-453128700-52 MiCA Consultation Paper - Guidelines On The Qualification of Crypto-Assets As Financial InstrumentsDocument39 pagesESMA75-453128700-52 MiCA Consultation Paper - Guidelines On The Qualification of Crypto-Assets As Financial Instrumentsucenickiservis.tssbNo ratings yet

- Eu Ifrs PDFDocument4 pagesEu Ifrs PDFLeonard BerishaNo ratings yet

- EU - DirectiveDocument8 pagesEU - DirectiveAlfred KizzaNo ratings yet

- GendocDocument15 pagesGendocMaryna PohorielovaNo ratings yet

- CP - Draft RTSs ICT Risk Management Tools Methods Processes and PoliciesDocument87 pagesCP - Draft RTSs ICT Risk Management Tools Methods Processes and PoliciesMirko KovacNo ratings yet

- Celex 32016o0034 en TXTDocument50 pagesCelex 32016o0034 en TXTL E PNo ratings yet

- 1.5 Implementing Regulation - Disclosure Standards - 2019.10.29Document6 pages1.5 Implementing Regulation - Disclosure Standards - 2019.10.29benteuxNo ratings yet

- Text With EEA RelevanceDocument26 pagesText With EEA RelevanceFrancesco LautiziNo ratings yet

- 2016.05 - Ucits ToolboxDocument382 pages2016.05 - Ucits ToolboxJustine991No ratings yet

- Regulation (EU) 2017 1131 On Money Market FundsDocument38 pagesRegulation (EU) 2017 1131 On Money Market FundsjohnNo ratings yet

- Awp Isfp 2020 en PDFDocument42 pagesAwp Isfp 2020 en PDFEdgaras KazkasNo ratings yet

- Eur-Lex - 32016o0034 - en - Eur-LexDocument78 pagesEur-Lex - 32016o0034 - en - Eur-LexL E PNo ratings yet

- EU Benchmark Regulations CELEX - 32016R1011 - EN - TXTDocument65 pagesEU Benchmark Regulations CELEX - 32016R1011 - EN - TXTdpageNo ratings yet

- Commission Implementing Regulation (Eu) 2018-1624Document65 pagesCommission Implementing Regulation (Eu) 2018-1624Mihai NegroiuNo ratings yet

- Eba CP 1699463275Document278 pagesEba CP 1699463275gv47tf9pmyNo ratings yet

- Draft RTS On Shadow Banking EntitiesDocument75 pagesDraft RTS On Shadow Banking EntitiesEirini KoufakiNo ratings yet

- Solvency2 Delegated Act 2021 2628 - enDocument9 pagesSolvency2 Delegated Act 2021 2628 - encaziziehNo ratings yet

- Celex 32013R0345 en TXTDocument17 pagesCelex 32013R0345 en TXTakvalexNo ratings yet

- Securities and Futures Ordinance CAP - 571Document397 pagesSecurities and Futures Ordinance CAP - 571KNo ratings yet

- Consultation Paper On RTS On Risk Retention in SecuritisationDocument30 pagesConsultation Paper On RTS On Risk Retention in SecuritisationMardha TillahNo ratings yet

- UK Transposition of The Markets Financial InstrumentsDocument46 pagesUK Transposition of The Markets Financial InstrumentsJoão Gabriel de Oliveira FreitasNo ratings yet

- Celex 32022R1288 en TXT PDFDocument72 pagesCelex 32022R1288 en TXT PDFMicheleNo ratings yet

- 06a - EU AML Regulation - Draft by The CouncilDocument192 pages06a - EU AML Regulation - Draft by The Councildaraksha.passportNo ratings yet

- Celex 32022R1929 en TXTDocument12 pagesCelex 32022R1929 en TXTbenteuxNo ratings yet

- Esma35!43!1906-Esma Opinion Under Article 432 Mifir at CFDDocument6 pagesEsma35!43!1906-Esma Opinion Under Article 432 Mifir at CFDfizzNo ratings yet

- Esma34-45-1272 Guidelines On Marketing CommunicationsDocument13 pagesEsma34-45-1272 Guidelines On Marketing CommunicationsRoscoe CamilleriNo ratings yet

- EBA Report On Crypto AssetsDocument30 pagesEBA Report On Crypto AssetsEmídio MirandaNo ratings yet

- Esma70-156-4596 Mifid II Mifir Annual Report 2021Document20 pagesEsma70-156-4596 Mifid II Mifir Annual Report 2021andres.rafael.carrenoNo ratings yet

- 2016oct - Mifid 2 - Pre and Post Trade TransparencyDocument14 pages2016oct - Mifid 2 - Pre and Post Trade TransparencyPurushottam ChandakNo ratings yet

- Amending RegulationDocument6 pagesAmending RegulationCynical GuyNo ratings yet

- Mi CaDocument380 pagesMi Cawilmer.dazaNo ratings yet

- The Impactof Security Token Offeringstothe Current Regulatory Landscapeandtothe Financial Services MarketDocument68 pagesThe Impactof Security Token Offeringstothe Current Regulatory Landscapeandtothe Financial Services MarketUzma SiddiquiNo ratings yet

- RTS 2 Mifid Reporting FieldsDocument157 pagesRTS 2 Mifid Reporting FieldsHamidul Haque ChishtyNo ratings yet

- AIFMD Exemptions & ScopeDocument3 pagesAIFMD Exemptions & Scopeshubhashish sharmaNo ratings yet

- FSCA Communication 14 of 2023 (RF) - Derivatives Instruments For Pension FundsDocument2 pagesFSCA Communication 14 of 2023 (RF) - Derivatives Instruments For Pension FundsIrfaan CassimNo ratings yet

- Celex 32019R2088 en TXTDocument16 pagesCelex 32019R2088 en TXTPapaplattaNo ratings yet

- Securities Note - 2022 03 08Document67 pagesSecurities Note - 2022 03 08Hyunjin ShinNo ratings yet

- ESMA MIFID II FINAL - Report - On - Guidelines - On - Product - GovernanceDocument55 pagesESMA MIFID II FINAL - Report - On - Guidelines - On - Product - GovernanceRoscoe CamilleriNo ratings yet

- European Banking Authority Opinion On Debt Based Crowdfunding March 2015Document40 pagesEuropean Banking Authority Opinion On Debt Based Crowdfunding March 2015CrowdfundInsiderNo ratings yet

- MiFID II Implementing Regulation (EU) 2017:565Document83 pagesMiFID II Implementing Regulation (EU) 2017:565Maylin SchoutenNo ratings yet

- Esma32-51-370 Qas On Esma Guidelines On ApmsDocument19 pagesEsma32-51-370 Qas On Esma Guidelines On ApmsRishabh MehtaNo ratings yet

- ST 10560 2017 ADD 2 enDocument107 pagesST 10560 2017 ADD 2 enanahh ramakNo ratings yet

- Draft Delegated Regulation - Ares (2023) 4009405Document11 pagesDraft Delegated Regulation - Ares (2023) 4009405Sîrbu VladNo ratings yet

- FI COMPASS - Manual - Ex Ante Quick Reference GuideDocument48 pagesFI COMPASS - Manual - Ex Ante Quick Reference GuideGeorge GuranNo ratings yet

- Esma Guide LinesDocument69 pagesEsma Guide Linessimha1177No ratings yet

- Decisions: (Recast)Document4 pagesDecisions: (Recast)Andreea BuicuNo ratings yet

- The Mifid 2 GuideDocument30 pagesThe Mifid 2 GuideNeeraj KumarNo ratings yet

- 2014-549 - Consultation Paper Mifid II - MifirDocument311 pages2014-549 - Consultation Paper Mifid II - MifirMarketsWikiNo ratings yet

- What Is SIMBOX?Document6 pagesWhat Is SIMBOX?Ayoub ZahraouiNo ratings yet

- Research Methods For Architecture Ebook - Lucas, Ray - Kindle StoreDocument1 pageResearch Methods For Architecture Ebook - Lucas, Ray - Kindle StoreMohammed ShriamNo ratings yet

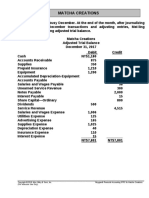

- MC4 Matcha Creations: (For Instructor Use Only)Document2 pagesMC4 Matcha Creations: (For Instructor Use Only)Reza eka PutraNo ratings yet

- List of PEREgistered On DLTDocument4,812 pagesList of PEREgistered On DLTVishalChaturvediNo ratings yet

- 2010 - Howaldt y Schwarz - Social Innovation-Concepts, Research Fields and International - LibroDocument82 pages2010 - Howaldt y Schwarz - Social Innovation-Concepts, Research Fields and International - Librovallejo13No ratings yet

- Webank'S Supply Chain Finance Solution: Confidential & ProprietaryDocument15 pagesWebank'S Supply Chain Finance Solution: Confidential & ProprietaryimuesNo ratings yet

- Ebook Business Law and The Regulation of Business 11Th Edition Mann Test Bank Full Chapter PDFDocument37 pagesEbook Business Law and The Regulation of Business 11Th Edition Mann Test Bank Full Chapter PDFelizabethclarkrigzatobmc100% (10)

- 13 - Project Procurement Management-Online v1Document41 pages13 - Project Procurement Management-Online v1Afrina M.Kom.No ratings yet

- Tenant Verification Form PDFDocument2 pagesTenant Verification Form PDFmohit kumarNo ratings yet

- BIT 4206 ICT in Business and Society-1Document85 pagesBIT 4206 ICT in Business and Society-1James MuthuriNo ratings yet

- SIP Report Atharva SableDocument68 pagesSIP Report Atharva Sable7s72p3nswtNo ratings yet

- Business Management Case Study: Ducal Aspirateurs: Instructions To CandidatesDocument5 pagesBusiness Management Case Study: Ducal Aspirateurs: Instructions To CandidatesJuan Antonio Limo DulantoNo ratings yet

- Bs in Business Administration Marketing Management: St. Nicolas College of Business and TechnologyDocument6 pagesBs in Business Administration Marketing Management: St. Nicolas College of Business and TechnologyMaria Charise TongolNo ratings yet

- LISTENING Countries in The WorldDocument6 pagesLISTENING Countries in The WorldVân KhánhNo ratings yet

- Approved Sponsorship LetterDocument2 pagesApproved Sponsorship LetterFelix Raphael MintuNo ratings yet

- Pt. Patco Elektronik Teknologi Standard Operating Procedure PurchasingDocument8 pagesPt. Patco Elektronik Teknologi Standard Operating Procedure Purchasingmochammad iqbal100% (1)

- Market Segmentation Strategic Analysis and Positioning ToolDocument4 pagesMarket Segmentation Strategic Analysis and Positioning ToolshadrickNo ratings yet

- Research On Fastrack WatchesDocument23 pagesResearch On Fastrack Watcheskk_kamal40% (5)

- Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002. byDocument56 pagesSecuritisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002. bykannangksNo ratings yet

- GPOA (PR Consultant)Document7 pagesGPOA (PR Consultant)Jeydrew TVNo ratings yet

- FLIPKART Research ReportDocument18 pagesFLIPKART Research ReportHabib RahmanNo ratings yet

- Basic Pre-Contractual Information: Name and Address of N26 Bank GMBH, Sucursal en EspañaDocument6 pagesBasic Pre-Contractual Information: Name and Address of N26 Bank GMBH, Sucursal en EspañaJosué BoteroNo ratings yet

- MHI-05-D11 - CompressedDocument4 pagesMHI-05-D11 - CompressedDr. Amit JainNo ratings yet

- Slip Gaji (3)Document2 pagesSlip Gaji (3)Olele Olala50% (2)

- GiftDocument6 pagesGiftalive2flirtNo ratings yet

- Print - Udyam Registration CertificateDocument3 pagesPrint - Udyam Registration Certificatemanwanimuki12No ratings yet

- 大萧条:历史与经验Document54 pages大萧条:历史与经验吴宙航No ratings yet

- Std. X Ch. 3 Money and Credit WS (21 - 22)Document3 pagesStd. X Ch. 3 Money and Credit WS (21 - 22)YASHVI MODINo ratings yet

- Case Study 3: Fountain Pens LimitedDocument3 pagesCase Study 3: Fountain Pens Limitedtanya singh100% (1)

- This Study Resource WasDocument2 pagesThis Study Resource WasAron Rabino ManaloNo ratings yet

- $100M Leads: How to Get Strangers to Want to Buy Your StuffFrom Everand$100M Leads: How to Get Strangers to Want to Buy Your StuffRating: 5 out of 5 stars5/5 (17)

- Obviously Awesome: How to Nail Product Positioning so Customers Get It, Buy It, Love ItFrom EverandObviously Awesome: How to Nail Product Positioning so Customers Get It, Buy It, Love ItRating: 4.5 out of 5 stars4.5/5 (151)

- Summary: Traction: Get a Grip on Your Business: by Gino Wickman: Key Takeaways, Summary, and AnalysisFrom EverandSummary: Traction: Get a Grip on Your Business: by Gino Wickman: Key Takeaways, Summary, and AnalysisRating: 5 out of 5 stars5/5 (10)

- $100M Offers: How to Make Offers So Good People Feel Stupid Saying NoFrom Everand$100M Offers: How to Make Offers So Good People Feel Stupid Saying NoRating: 5 out of 5 stars5/5 (21)

- Fascinate: How to Make Your Brand Impossible to ResistFrom EverandFascinate: How to Make Your Brand Impossible to ResistRating: 5 out of 5 stars5/5 (1)

- Ca$hvertising: How to Use More than 100 Secrets of Ad-Agency Psychology to Make Big Money Selling Anything to AnyoneFrom EverandCa$hvertising: How to Use More than 100 Secrets of Ad-Agency Psychology to Make Big Money Selling Anything to AnyoneRating: 5 out of 5 stars5/5 (114)

- Pre-Suasion: Channeling Attention for ChangeFrom EverandPre-Suasion: Channeling Attention for ChangeRating: 4.5 out of 5 stars4.5/5 (277)

- ChatGPT Millionaire 2024 - Bot-Driven Side Hustles, Prompt Engineering Shortcut Secrets, and Automated Income Streams that Print Money While You Sleep. The Ultimate Beginner’s Guide for AI BusinessFrom EverandChatGPT Millionaire 2024 - Bot-Driven Side Hustles, Prompt Engineering Shortcut Secrets, and Automated Income Streams that Print Money While You Sleep. The Ultimate Beginner’s Guide for AI BusinessNo ratings yet

- The Catalyst: How to Change Anyone's MindFrom EverandThe Catalyst: How to Change Anyone's MindRating: 4.5 out of 5 stars4.5/5 (273)

- How to Read People: The Complete Psychology Guide to Analyzing People, Reading Body Language, and Persuading, Manipulating and Understanding How to Influence Human BehaviorFrom EverandHow to Read People: The Complete Psychology Guide to Analyzing People, Reading Body Language, and Persuading, Manipulating and Understanding How to Influence Human BehaviorRating: 4.5 out of 5 stars4.5/5 (33)

- Dealers of Lightning: Xerox PARC and the Dawn of the Computer AgeFrom EverandDealers of Lightning: Xerox PARC and the Dawn of the Computer AgeRating: 4 out of 5 stars4/5 (88)

- How to Get a Meeting with Anyone: The Untapped Selling Power of Contact MarketingFrom EverandHow to Get a Meeting with Anyone: The Untapped Selling Power of Contact MarketingRating: 4.5 out of 5 stars4.5/5 (28)

- Scientific Advertising: "Master of Effective Advertising"From EverandScientific Advertising: "Master of Effective Advertising"Rating: 4.5 out of 5 stars4.5/5 (163)

- How To Win Customers And Keep Them For Life: An Action-Ready Blueprint for Achieving the Winner's Edge!From EverandHow To Win Customers And Keep Them For Life: An Action-Ready Blueprint for Achieving the Winner's Edge!Rating: 4.5 out of 5 stars4.5/5 (23)

- Marketing Made Simple: A Step-by-Step StoryBrand Guide for Any BusinessFrom EverandMarketing Made Simple: A Step-by-Step StoryBrand Guide for Any BusinessRating: 5 out of 5 stars5/5 (203)

- Blue Ocean Strategy, Expanded Edition: How to Create Uncontested Market Space and Make the Competition IrrelevantFrom EverandBlue Ocean Strategy, Expanded Edition: How to Create Uncontested Market Space and Make the Competition IrrelevantRating: 4 out of 5 stars4/5 (387)

- Understanding Digital Marketing: Marketing Strategies for Engaging the Digital GenerationFrom EverandUnderstanding Digital Marketing: Marketing Strategies for Engaging the Digital GenerationRating: 4 out of 5 stars4/5 (22)

- Create Once, Distribute Forever: How Great Creators Spread Their Ideas and How You Can TooFrom EverandCreate Once, Distribute Forever: How Great Creators Spread Their Ideas and How You Can TooNo ratings yet

- Brand Identity Breakthrough: How to Craft Your Company's Unique Story to Make Your Products IrresistibleFrom EverandBrand Identity Breakthrough: How to Craft Your Company's Unique Story to Make Your Products IrresistibleRating: 4.5 out of 5 stars4.5/5 (48)

- Summary: Range: Why Generalists Triumph in a Specialized World by David Epstein: Key Takeaways, Summary & Analysis IncludedFrom EverandSummary: Range: Why Generalists Triumph in a Specialized World by David Epstein: Key Takeaways, Summary & Analysis IncludedRating: 4.5 out of 5 stars4.5/5 (6)

- Jab, Jab, Jab, Right Hook: How to Tell Your Story in a Noisy Social WorldFrom EverandJab, Jab, Jab, Right Hook: How to Tell Your Story in a Noisy Social WorldRating: 4.5 out of 5 stars4.5/5 (18)

- Summary: The 1-Page Marketing Plan: Get New Customers, Make More Money, And Stand Out From The Crowd by Allan Dib: Key Takeaways, Summary & AnalysisFrom EverandSummary: The 1-Page Marketing Plan: Get New Customers, Make More Money, And Stand Out From The Crowd by Allan Dib: Key Takeaways, Summary & AnalysisRating: 5 out of 5 stars5/5 (7)

- Yes!: 50 Scientifically Proven Ways to Be PersuasiveFrom EverandYes!: 50 Scientifically Proven Ways to Be PersuasiveRating: 4 out of 5 stars4/5 (153)

- Invisible Influence: The Hidden Forces that Shape BehaviorFrom EverandInvisible Influence: The Hidden Forces that Shape BehaviorRating: 4.5 out of 5 stars4.5/5 (131)

- Launch: An Internet Millionaire's Secret Formula to Sell Almost Anything Online, Build a Business You Love, and Live the Life of Your DreamsFrom EverandLaunch: An Internet Millionaire's Secret Formula to Sell Almost Anything Online, Build a Business You Love, and Live the Life of Your DreamsRating: 4.5 out of 5 stars4.5/5 (123)

- The Lean Product Playbook: How to Innovate with Minimum Viable Products and Rapid Customer FeedbackFrom EverandThe Lean Product Playbook: How to Innovate with Minimum Viable Products and Rapid Customer FeedbackRating: 4.5 out of 5 stars4.5/5 (81)

- Summary: $100M Leads: How to Get Strangers to Want to Buy Your Stuff by Alex Hormozi: Key Takeaways, Summary & Analysis IncludedFrom EverandSummary: $100M Leads: How to Get Strangers to Want to Buy Your Stuff by Alex Hormozi: Key Takeaways, Summary & Analysis IncludedRating: 3 out of 5 stars3/5 (6)

- The Power of Why: Breaking Out In a Competitive MarketplaceFrom EverandThe Power of Why: Breaking Out In a Competitive MarketplaceRating: 4 out of 5 stars4/5 (5)