You might also like

- Boosting Productivity in Kazakhstan with Micro-Level Tools: Analysis and Policy LessonsFrom EverandBoosting Productivity in Kazakhstan with Micro-Level Tools: Analysis and Policy LessonsNo ratings yet

- FullReport AES2021Document108 pagesFullReport AES2021clement3176No ratings yet

- Report On NIA Q2 2021Document24 pagesReport On NIA Q2 2021sarah jane lomaNo ratings yet

- The State of The Economy - DR Salami UpdatedDocument21 pagesThe State of The Economy - DR Salami UpdatedEfosa AigbeNo ratings yet

- Dabur India's strong domestic volume growth lifts revenues 18Document9 pagesDabur India's strong domestic volume growth lifts revenues 18Raghavendra Pratap SinghNo ratings yet

- Q2Fy21 GDP: Investments Fared Better Than Consumption FY21E GDP Retained at - 5% To - 7%Document5 pagesQ2Fy21 GDP: Investments Fared Better Than Consumption FY21E GDP Retained at - 5% To - 7%Raghvendra N DhootNo ratings yet

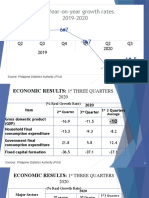

- The Stories Numbers Tell: Understanding Key Economic IndicatorsDocument22 pagesThe Stories Numbers Tell: Understanding Key Economic IndicatorsreiiNo ratings yet

- EricssonDocument47 pagesEricssonRafa BorgesNo ratings yet

- Vietnam Startup Report Highlights Rising Trends and Investor OptimismDocument34 pagesVietnam Startup Report Highlights Rising Trends and Investor OptimismTrần Thủy VânNo ratings yet

- GDP 2021 EngDocument18 pagesGDP 2021 EngMunkhchimeg PurevNo ratings yet

- V-Guard Q1 FY20 Earnings Presentation Highlights Strong GrowthDocument21 pagesV-Guard Q1 FY20 Earnings Presentation Highlights Strong GrowthSelva ThanarajNo ratings yet

- Q1 FY2019 Performance Review HighlightsDocument20 pagesQ1 FY2019 Performance Review HighlightsRAHUL PANDEYNo ratings yet

- Fibank Albania Annual Report 2019 083685f7fdDocument141 pagesFibank Albania Annual Report 2019 083685f7fdKarolina MusagalliuNo ratings yet

- Total Factor Productivity For Major Industries - 2022Document15 pagesTotal Factor Productivity For Major Industries - 2022Novica SupicNo ratings yet

- HCL Tech Q1 FY23 Investor ReleaseDocument25 pagesHCL Tech Q1 FY23 Investor ReleasedeepeshNo ratings yet

- GDP growth plunges to 5% lowest in 25 quartersDocument2 pagesGDP growth plunges to 5% lowest in 25 quartersSanjoySahaNo ratings yet

- GDP Report Q1 2021Document99 pagesGDP Report Q1 2021idrisngrNo ratings yet

- Business Outlook Brighter in The Second Quarter of 2005Document13 pagesBusiness Outlook Brighter in The Second Quarter of 2005raloreto7251No ratings yet

- Echap09 Vol2Document21 pagesEchap09 Vol2Abhinav VohraNo ratings yet

- Kantar Worldpanel Division FMCG Monitor Full Year 2020 EN FinalDocument10 pagesKantar Worldpanel Division FMCG Monitor Full Year 2020 EN FinalvinhtamledangNo ratings yet

- V-Guard-Industries - Q4 FY21-Results-PresentationDocument17 pagesV-Guard-Industries - Q4 FY21-Results-PresentationanooppattazhyNo ratings yet

- Lombard Fy19Document21 pagesLombard Fy19Sriram RajaramNo ratings yet

- Sub: Investor UpdateDocument29 pagesSub: Investor UpdateSHANKAR JADHAVNo ratings yet

- NESG Manufacturing Policy Brief May 2021Document11 pagesNESG Manufacturing Policy Brief May 2021uchenna joel iconNo ratings yet

- 1Q20 Naver Eng 0521Document11 pages1Q20 Naver Eng 0521Insight Viet NamNo ratings yet

- Viet Nam Market Pulse - Shared by WorldLine Technology-1Document21 pagesViet Nam Market Pulse - Shared by WorldLine Technology-1CHIÊM HÀNo ratings yet

- Monthly Bulletin July 2023 EnglishDocument13 pagesMonthly Bulletin July 2023 EnglishNirmal MenonNo ratings yet

- Sme Report - FinalDocument14 pagesSme Report - FinalAKSHATA NEOLENo ratings yet

- Pidilite Industries (PIDIND) : High Raw Material Prices Hit MarginDocument10 pagesPidilite Industries (PIDIND) : High Raw Material Prices Hit MarginSiddhant SinghNo ratings yet

- Malaysian Economic Development 1Q2011 (BNM)Document9 pagesMalaysian Economic Development 1Q2011 (BNM)Anuar HishamNo ratings yet

- Africa Day Presentation VDefDocument30 pagesAfrica Day Presentation VDefBernard BiboumNo ratings yet

- DABUR INDIA LIMITED INVESTOR COMMUNICATION Q1 FY20 HIGHLIGHTSDocument23 pagesDABUR INDIA LIMITED INVESTOR COMMUNICATION Q1 FY20 HIGHLIGHTSarti guptaNo ratings yet

- Retail Industry Retail Industry Retail IndustryDocument8 pagesRetail Industry Retail Industry Retail IndustryTanmay PokaleNo ratings yet

- ICICI Bank Investor Presentation On Performance Review Q4 2020Document85 pagesICICI Bank Investor Presentation On Performance Review Q4 2020shubham moonNo ratings yet

- Economic Indicators DashboardDocument22 pagesEconomic Indicators Dashboardthulani sibandaNo ratings yet

- V Guard Industries Q3 FY22 Results PresentationDocument17 pagesV Guard Industries Q3 FY22 Results PresentationRATHINo ratings yet

- Press Presentation q1 Fy21Document13 pagesPress Presentation q1 Fy21Pharma researchNo ratings yet

- Q4 Fy21 GDPDocument7 pagesQ4 Fy21 GDPsksaha1976No ratings yet

- Philippine Economic Updates May 2023Document2 pagesPhilippine Economic Updates May 2023regina.bumatayNo ratings yet

- MIDA Newsletter December 2020 FINALDocument28 pagesMIDA Newsletter December 2020 FINALbicarahidup98No ratings yet

- Orange Reports Solid FY22 Results With Revenue Growth and EBITDAaL Beat#FY_2022Document30 pagesOrange Reports Solid FY22 Results With Revenue Growth and EBITDAaL Beat#FY_2022Umar MasaudNo ratings yet

- Wipro LTD (WIPRO) : Growth and Margin Visibility Improving..Document13 pagesWipro LTD (WIPRO) : Growth and Margin Visibility Improving..ashok yadavNo ratings yet

- 2021 First Half Year Results: Underlying Performance GAAP MeasuresDocument23 pages2021 First Half Year Results: Underlying Performance GAAP MeasuresTHU TAO DUONG THANHNo ratings yet

- KBSV - Macro Outlook 2Q - 2019Document16 pagesKBSV - Macro Outlook 2Q - 2019LinhNo ratings yet

- Talk Shop Asia - As of 24 Nov 2020Document9 pagesTalk Shop Asia - As of 24 Nov 2020Jonathan AguilarNo ratings yet

- ABB Reports Solid Q1 2022 Results Despite UncertaintiesDocument13 pagesABB Reports Solid Q1 2022 Results Despite UncertaintiesMATHU MOHANNo ratings yet

- Business confidence rises for Q1 and Q2 2019Document13 pagesBusiness confidence rises for Q1 and Q2 2019Rommel LoretoNo ratings yet

- Qb23q3 en Ch2Document5 pagesQb23q3 en Ch2milvibesupplyNo ratings yet

- Industry Infrastructure Growth Recovery IIPDocument48 pagesIndustry Infrastructure Growth Recovery IIPsudip dhuriNo ratings yet

- Kendrion, 2019 Q2Document18 pagesKendrion, 2019 Q2Jasper Laarmans Teixeira de MattosNo ratings yet

- July 2022 CPI ReportDocument5 pagesJuly 2022 CPI ReportBernewsAdminNo ratings yet

- HCL Tech Q4 FY22 Investor ReleaseDocument25 pagesHCL Tech Q4 FY22 Investor ReleaseNddd NnbNo ratings yet

- MAPI Shares Fall as PPKM Extension Hampers RevenueDocument6 pagesMAPI Shares Fall as PPKM Extension Hampers RevenuePutu Chantika Putri DhammayantiNo ratings yet

- Key Highlights:: Particulars Q4 FY21 Q4 FY20 Shift FY21 FY20 FY20 ShiftDocument3 pagesKey Highlights:: Particulars Q4 FY21 Q4 FY20 Shift FY21 FY20 FY20 Shiftkashyappathak01No ratings yet

- HDFC Life Presentation - Q1 FY21 FinalDocument59 pagesHDFC Life Presentation - Q1 FY21 FinaljhopadlpNo ratings yet

- IRDA Annual Copy 2023-24Document96 pagesIRDA Annual Copy 2023-24Anjali BawaNo ratings yet

- Er 23q1Document134 pagesEr 23q1Rhoda LawNo ratings yet

- q2 Results-2020 tcm1350-553657 1 deDocument25 pagesq2 Results-2020 tcm1350-553657 1 deDiana KilelNo ratings yet

- 2021 Budget Highlights v1Document30 pages2021 Budget Highlights v1alexander amoakoNo ratings yet

- Infosys Revenue Up 7.9% YoYDocument11 pagesInfosys Revenue Up 7.9% YoYanjugaduNo ratings yet

- Green Behavior and Financial Performance: Impact On The Malaysian Fashion IndustryDocument14 pagesGreen Behavior and Financial Performance: Impact On The Malaysian Fashion IndustryGol HoNo ratings yet

- BondsDocument1 pageBondsK60 Nguyễn Thúy HoàNo ratings yet

- Singapore Economy at a GlanceDocument5 pagesSingapore Economy at a GlanceK60 Nguyễn Thúy HoàNo ratings yet

- Bút ngữ tiếng Anh trung cấp 2 - Writing testDocument6 pagesBút ngữ tiếng Anh trung cấp 2 - Writing testK60 Nguyễn Thúy HoàNo ratings yet

- OME 752 Supply Chain Management 1Document2 pagesOME 752 Supply Chain Management 1sheelasweetyNo ratings yet

- New 1st Semester English (MCO-01,04,05,21) M.com AssignmentDocument8 pagesNew 1st Semester English (MCO-01,04,05,21) M.com AssignmentRajni KumariNo ratings yet

- Strategic Analysis of Reliance Industries LTD.: Guide - Dr. Neeraj SinghalDocument20 pagesStrategic Analysis of Reliance Industries LTD.: Guide - Dr. Neeraj SinghalPRITHIKA DASGUPTA 19212441No ratings yet

- Course Syllabus Outline OBLI 2nd SEM AY 2021 2022 For The ClassDocument8 pagesCourse Syllabus Outline OBLI 2nd SEM AY 2021 2022 For The ClassJULLIAN PAOLO UMALINo ratings yet

- Pooya, A., Mehran, A.K. and Ghouzhdi, S.G., 2020.Document19 pagesPooya, A., Mehran, A.K. and Ghouzhdi, S.G., 2020.Eduardo CastañedaNo ratings yet

- Operations and services strategy assignmentDocument7 pagesOperations and services strategy assignmentShivam JadhavNo ratings yet

- Strategies for Customer Relationship ManagementDocument26 pagesStrategies for Customer Relationship Managementprince100% (3)

- Datesheet Ims SeptemberDocument2 pagesDatesheet Ims SeptemberOm PratapNo ratings yet

- DocJuris Contract Playbook Model v4.5 - Service AgreementDocument24 pagesDocJuris Contract Playbook Model v4.5 - Service AgreementvicentesuzukiNo ratings yet

- Nigerian Price Control Act 1977Document41 pagesNigerian Price Control Act 1977AhmadNo ratings yet

- Department of Business Administration: Assignment OnDocument13 pagesDepartment of Business Administration: Assignment OnRubyat SharminNo ratings yet

- HSRP Online Appointment Transaction Receipt Rosmerta Safety Systems PVT - LTDDocument1 pageHSRP Online Appointment Transaction Receipt Rosmerta Safety Systems PVT - LTDTaj HackersNo ratings yet

- Sustainable Supply Chain Management: A Review of Literature and Implications For Future ResearchDocument49 pagesSustainable Supply Chain Management: A Review of Literature and Implications For Future ResearchShashi BhushanNo ratings yet

- Janome Memory 10000 Craft Sewing Machine Instruction Manual Pt2Document112 pagesJanome Memory 10000 Craft Sewing Machine Instruction Manual Pt2iliiexpugnansNo ratings yet

- Measuring Media Coverage EffectivelyDocument9 pagesMeasuring Media Coverage EffectivelyAsif KhanNo ratings yet

- Assessment (L4) : Case Analysis: Managerial EconomicsDocument4 pagesAssessment (L4) : Case Analysis: Managerial EconomicsRocel DomingoNo ratings yet

- Chapter 11 - Foundations of Organizational Design-1-1Document21 pagesChapter 11 - Foundations of Organizational Design-1-1Labiba IbnatNo ratings yet

- Call For Papers - ICAFI 2023Document2 pagesCall For Papers - ICAFI 2023Alcido JuanihaNo ratings yet

- La La Land SongbookDocument74 pagesLa La Land SongbookNickNo ratings yet

- SM Manpower AustraliaDocument37 pagesSM Manpower Australiadhwani malde100% (1)

- Britinnia Cheese: A Class Assignment ReportDocument15 pagesBritinnia Cheese: A Class Assignment ReportAshwani RaiNo ratings yet

- Base Sim Game How To Play GuideDocument7 pagesBase Sim Game How To Play GuideFrancisco BaezaNo ratings yet

- Animal Production TLE Summative AssessmentDocument7 pagesAnimal Production TLE Summative AssessmentHoney Grace CaballesNo ratings yet

- I1 Personal Best WB AnswersDocument6 pagesI1 Personal Best WB Answersliliane ramosNo ratings yet

- DP Clean Tech BrochureDocument16 pagesDP Clean Tech BrochurebhasinbNo ratings yet

- Prequalification Checklist Form: ANNEX-D (Returnable Form) Infrastructure Services: ContractorsDocument2 pagesPrequalification Checklist Form: ANNEX-D (Returnable Form) Infrastructure Services: ContractorsJavier ContrerasNo ratings yet

- Aolved: Question BankDocument25 pagesAolved: Question BankMehul Jindal100% (2)

- Module - 3 Trial Balance QuestionsDocument7 pagesModule - 3 Trial Balance QuestionsMuskan Rathi 5100No ratings yet

- Class Notes 11 - Fractions & Percentages Practice QuestionsDocument11 pagesClass Notes 11 - Fractions & Percentages Practice Questions4H Boodram ArvindaNo ratings yet

- Public RelationDocument14 pagesPublic RelationWahyu RinaNo ratings yet

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantFrom EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantRating: 4.5 out of 5 stars4.5/5 (146)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (12)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- Financial Accounting For Dummies: 2nd EditionFrom EverandFinancial Accounting For Dummies: 2nd EditionRating: 5 out of 5 stars5/5 (10)

- Profit First for Therapists: A Simple Framework for Financial FreedomFrom EverandProfit First for Therapists: A Simple Framework for Financial FreedomNo ratings yet

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetFrom EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetNo ratings yet

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- Business Valuation: Private Equity & Financial Modeling 3 Books In 1: 27 Ways To Become A Successful Entrepreneur & Sell Your Business For BillionsFrom EverandBusiness Valuation: Private Equity & Financial Modeling 3 Books In 1: 27 Ways To Become A Successful Entrepreneur & Sell Your Business For BillionsNo ratings yet

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyFrom EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyRating: 5 out of 5 stars5/5 (1)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsFrom EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsNo ratings yet

- Basic Accounting: Service Business Study GuideFrom EverandBasic Accounting: Service Business Study GuideRating: 5 out of 5 stars5/5 (2)

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsFrom EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsRating: 4 out of 5 stars4/5 (7)

- Emprender un Negocio: Paso a Paso Para PrincipiantesFrom EverandEmprender un Negocio: Paso a Paso Para PrincipiantesRating: 3 out of 5 stars3/5 (1)

- NLP:The Essential Handbook for Business: The Essential Handbook for Business: Communication Techniques to Build Relationships, Influence Others, and Achieve Your GoalsFrom EverandNLP:The Essential Handbook for Business: The Essential Handbook for Business: Communication Techniques to Build Relationships, Influence Others, and Achieve Your GoalsRating: 4.5 out of 5 stars4.5/5 (4)

- Bookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesFrom EverandBookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesRating: 4.5 out of 5 stars4.5/5 (30)

- The Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyFrom EverandThe Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyRating: 4 out of 5 stars4/5 (4)

- Full Charge Bookkeeping, For the Beginner, Intermediate & Advanced BookkeeperFrom EverandFull Charge Bookkeeping, For the Beginner, Intermediate & Advanced BookkeeperRating: 5 out of 5 stars5/5 (3)