You might also like

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Document33 pagesReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB CloydNo ratings yet

- Taxation Law - NIRC Vs TRAINDocument3 pagesTaxation Law - NIRC Vs TRAINGemma F. Tiama100% (2)

- Prelim Take Home ExamDocument11 pagesPrelim Take Home ExamPATATASNo ratings yet

- Public Sector Accounting and Administrative Practices in Nigeria Volume 1From EverandPublic Sector Accounting and Administrative Practices in Nigeria Volume 1No ratings yet

- Expanded Withholding Tax Rates and CodesDocument7 pagesExpanded Withholding Tax Rates and CodesJaemar FajardoNo ratings yet

- WITHHOLDING TAX OBLIGATIONSDocument152 pagesWITHHOLDING TAX OBLIGATIONSemytherese100% (2)

- SGLGB ImplementationDocument47 pagesSGLGB ImplementationDILG Maragondon CaviteNo ratings yet

- Schedules of Alphanumeric Tax CodesDocument3 pagesSchedules of Alphanumeric Tax Codescatherine joy sangilNo ratings yet

- 1601E - August 2008Document3 pages1601E - August 2008lovesresearchNo ratings yet

- Corporation As A TaxpayerDocument27 pagesCorporation As A TaxpayerBSA-2C John Dominic Mia100% (1)

- Trugo, Karluz BT - SW1 - C9Document15 pagesTrugo, Karluz BT - SW1 - C9moreNo ratings yet

- Basic Control Valve and Sizing and SelectionDocument38 pagesBasic Control Valve and Sizing and SelectionNguyen Anh Tung50% (2)

- BIR GlobeDocument4 pagesBIR GlobeRenge TañaNo ratings yet

- Nokia Help PDFDocument101 pagesNokia Help PDFTim GargNo ratings yet

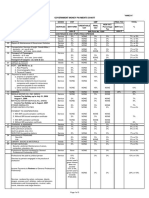

- Government Money Payments Chart - BirDocument3 pagesGovernment Money Payments Chart - BirVan Caz89% (9)

- Withholding Taxes Learning ObjectivesDocument8 pagesWithholding Taxes Learning ObjectivesAce AlquinNo ratings yet

- Catching the Cooperative Tax TrainDocument163 pagesCatching the Cooperative Tax TrainDeirdre Mae Pitpitunge100% (1)

- Abraca Cortina Ovelha-1 PDFDocument13 pagesAbraca Cortina Ovelha-1 PDFMarina Renata Mosella Tenorio100% (7)

- Withholding Tax ATCDocument45 pagesWithholding Tax ATCRandy PaderesNo ratings yet

- Expanded Withholding TaxDocument3 pagesExpanded Withholding TaxCordero TJNo ratings yet

- College of Accounting Education Session on Withholding TaxesDocument16 pagesCollege of Accounting Education Session on Withholding TaxesMitzi WamarNo ratings yet

- Withholding Tax RatesDocument5 pagesWithholding Tax RatesMary Ann castroNo ratings yet

- Withholding Tax Bureau of Internal RevenueDocument10 pagesWithholding Tax Bureau of Internal RevenueFunnyPearl Adal GajuneraNo ratings yet

- Withholding Tax RatesDocument35 pagesWithholding Tax RatesZonia Mae CuidnoNo ratings yet

- A.J. Gen. MerchandisingDocument5 pagesA.J. Gen. MerchandisingErish Jay ManalangNo ratings yet

- Sample 2307 2017Document4 pagesSample 2307 2017jordzNo ratings yet

- Ewt 20082Document384 pagesEwt 20082JonelChavezNo ratings yet

- Table of Creditable Withholding Tax RatesDocument4 pagesTable of Creditable Withholding Tax RatesZandra Mari Dela PenaNo ratings yet

- BIR From 1601E - August 2008Document4 pagesBIR From 1601E - August 2008mba_roxascapiz50% (4)

- Summary of Final Tax Under The Nirc, As Amended Individual Citizen AlienDocument16 pagesSummary of Final Tax Under The Nirc, As Amended Individual Citizen AlienXiaoyu KensameNo ratings yet

- Withholding TaxDocument20 pagesWithholding TaxAngela CanayaNo ratings yet

- Passive Income Rc/Ra/Nrc Nra-ETB Nra - Netb DC RFC NRFCDocument10 pagesPassive Income Rc/Ra/Nrc Nra-ETB Nra - Netb DC RFC NRFCBARBEKS 202021No ratings yet

- BIR Form 2307 Tax CodesDocument16 pagesBIR Form 2307 Tax CodesAnalyn Velasco Matibag100% (1)

- WT Tax RatesDocument2 pagesWT Tax RatesericbacsalNo ratings yet

- Uganda Tax Guide: Income, VAT, Excise, Stamp Duty RatesDocument9 pagesUganda Tax Guide: Income, VAT, Excise, Stamp Duty RatesJeff QueiroNo ratings yet

- Schedules of Alphanumeric Tax CodesDocument5 pagesSchedules of Alphanumeric Tax CodesKatherine YuNo ratings yet

- HumRes TaxDocument3 pagesHumRes TaxJob Noel BernardoNo ratings yet

- 2307Document3 pages2307Anonymous yCFuth7BL80% (1)

- 2307Document5 pages2307jblopez66No ratings yet

- W14 Module 12withholding TaxesDocument7 pagesW14 Module 12withholding Taxescamille ducutNo ratings yet

- Midterm Assignment No. 3Document3 pagesMidterm Assignment No. 3XaxxyNo ratings yet

- Types of Income and Corresponding Tax RatesDocument13 pagesTypes of Income and Corresponding Tax RatesJessa Belle EubionNo ratings yet

- BIR Form No. 1601E - Guidelines and InstructionsDocument4 pagesBIR Form No. 1601E - Guidelines and InstructionsJinefer ButohanNo ratings yet

- Graduated - Tax Base Is Net Income 8% - Tax Base Is Gross IncomeDocument9 pagesGraduated - Tax Base Is Net Income 8% - Tax Base Is Gross IncomeFrancis Kyle Cagalingan SubidoNo ratings yet

- Tax Rates for Individuals, Capital Gains, Passive Income and Corporations from 2018-2022Document9 pagesTax Rates for Individuals, Capital Gains, Passive Income and Corporations from 2018-2022Kyle SubidoNo ratings yet

- FinalDocument2 pagesFinalJessica FordNo ratings yet

- BIR Form 1601E Guidelines for Alphanumeric Tax CodesDocument3 pagesBIR Form 1601E Guidelines for Alphanumeric Tax CodesGuia CatolicoNo ratings yet

- RC Nirc, Ra, Nra-Etb Nra-Netb: Taxpayer Tax Base Source of Taxable IncomeDocument7 pagesRC Nirc, Ra, Nra-Etb Nra-Netb: Taxpayer Tax Base Source of Taxable IncomeGwyneth GloriaNo ratings yet

- RMO No. 3-2004 PDFDocument4 pagesRMO No. 3-2004 PDFlantern san juanNo ratings yet

- Tax Rates For CWT (Expanded) PDFDocument2 pagesTax Rates For CWT (Expanded) PDFRoseAnnFloriaNo ratings yet

- BIR Form No. 1601E - Guidelines and InstructionsDocument3 pagesBIR Form No. 1601E - Guidelines and Instructionsivy contrerasNo ratings yet

- Taxation - Botswana (TX - Bwa) : Applied SkillsDocument20 pagesTaxation - Botswana (TX - Bwa) : Applied Skillsgajendra.naiduNo ratings yet

- EWTDocument12 pagesEWTdawngarcia1797No ratings yet

- Quiz 1: Tax 3 Final Period QuizzesDocument10 pagesQuiz 1: Tax 3 Final Period QuizzesJhun bondocNo ratings yet

- Revenue Memorandum Order No. 3-2004Document4 pagesRevenue Memorandum Order No. 3-2004HarryNo ratings yet

- Taxation Law 1 Taxation Law 1 Atty. Vicente V. Cañoneo Atty. Vicente V. CañoneoDocument3 pagesTaxation Law 1 Taxation Law 1 Atty. Vicente V. Cañoneo Atty. Vicente V. CañoneoHannah Beatriz Cabral0% (1)

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Commercial Bank Revenues World Summary: Market Values & Financials by CountryFrom EverandCommercial Bank Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Securities Brokerage Revenues World Summary: Market Values & Financials by CountryFrom EverandSecurities Brokerage Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesFrom EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNo ratings yet

- Pawn Shop Revenues World Summary: Market Values & Financials by CountryFrom EverandPawn Shop Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Easychair Preprint: Shakti Chaturvedi, Nisha Goyal and Raghava Reddy VaraprasadDocument24 pagesEasychair Preprint: Shakti Chaturvedi, Nisha Goyal and Raghava Reddy VaraprasadSneha Elizabeth VivianNo ratings yet

- Study of HRM Practices in Public SectorDocument82 pagesStudy of HRM Practices in Public SectorvishalNo ratings yet

- Message From The Chairman: Section On International and Comparative AdministrationDocument12 pagesMessage From The Chairman: Section On International and Comparative AdministrationBrittany KeeganNo ratings yet

- Unit 1.3 Practice TestDocument16 pagesUnit 1.3 Practice TestYoann DanionNo ratings yet

- Alabama Tenants HandbookDocument26 pagesAlabama Tenants HandbookzorthogNo ratings yet

- S141 Advanced DSP-based Servo Motion ControllerDocument8 pagesS141 Advanced DSP-based Servo Motion ControllersharkeraNo ratings yet

- BIR - RMC.064-16.Tax Treatment Non-Stock Non ProfitDocument11 pagesBIR - RMC.064-16.Tax Treatment Non-Stock Non ProfitKTGNo ratings yet

- G.R. No. 201302 Hygienic Packaging Corporation, Petitioner Nutri-Asia, Inc., Doing Business Under The Name and Style of Ufc Philippines (FORMERLY NUTRI-ASIA, INC.), Respondent Decision Leonen, J.Document5 pagesG.R. No. 201302 Hygienic Packaging Corporation, Petitioner Nutri-Asia, Inc., Doing Business Under The Name and Style of Ufc Philippines (FORMERLY NUTRI-ASIA, INC.), Respondent Decision Leonen, J.SK Fairview Barangay BaguioNo ratings yet

- Exam PaperDocument2 pagesExam PapersanggariNo ratings yet

- Navigator Cisco Product Rental StockDocument6 pagesNavigator Cisco Product Rental StockSatish KumarNo ratings yet

- Client Data Sector Wise BangaloreDocument264 pagesClient Data Sector Wise BangaloreOindrilaNo ratings yet

- Working Capital ManagmentDocument7 pagesWorking Capital ManagmentMarie ElliottNo ratings yet

- Welcome To SBI - Application Form PrintDocument1 pageWelcome To SBI - Application Form PrintmoneythindNo ratings yet

- STD 2 ComputerDocument12 pagesSTD 2 ComputertayyabaNo ratings yet

- The List, Stack, and Queue Adts Abstract Data Type (Adt)Document17 pagesThe List, Stack, and Queue Adts Abstract Data Type (Adt)Jennelyn SusonNo ratings yet

- 1536-Centrifugial (SPUN), FittingsDocument23 pages1536-Centrifugial (SPUN), FittingsshahidNo ratings yet

- The Effective Length of Columns in MultiDocument12 pagesThe Effective Length of Columns in MulticoolkaisyNo ratings yet

- Analog To Digital Converters (ADC) : A Literature Review: and Sanjeet K. SinhaDocument9 pagesAnalog To Digital Converters (ADC) : A Literature Review: and Sanjeet K. SinhaRyu- MikaNo ratings yet

- Biosafety and Lab Waste GuideDocument4 pagesBiosafety and Lab Waste Guidebhramar bNo ratings yet

- Class 11 Constitutional Law Model QuestionDocument3 pagesClass 11 Constitutional Law Model QuestionanuNo ratings yet

- ml350p g8.Document57 pagesml350p g8.Aboubacar N'dji CoulibalyNo ratings yet

- TS Dry StonerDocument6 pagesTS Dry StonerChong Chan YauNo ratings yet

- LogProcessing-TEICH v2Document23 pagesLogProcessing-TEICH v2slides courseNo ratings yet

- R.J. Reynolds Internation FinancingDocument2 pagesR.J. Reynolds Internation FinancingUmair ShaikhNo ratings yet

- Chapter 3Document2 pagesChapter 3RoAnne Pa Rin100% (1)

- Tut 1Document5 pagesTut 1foranangelqwertyNo ratings yet