You might also like

- Igl Gas Bill - IndiaDocument1 pageIgl Gas Bill - Indiasouravdubey1909No ratings yet

- FAR - Shiv ChemicalDocument3 pagesFAR - Shiv Chemicalgroup6 cgstauditNo ratings yet

- 76124bos61507 cp15Document91 pages76124bos61507 cp15Pandey PujaNo ratings yet

- Gadna Sheet Fy 23-24Document1 pageGadna Sheet Fy 23-24prtiwari1914No ratings yet

- FormDocument1 pageFormpardeep sanwalNo ratings yet

- Form GST ADT-01 (See Rule 101 (2) )Document3 pagesForm GST ADT-01 (See Rule 101 (2) )Harsh JainNo ratings yet

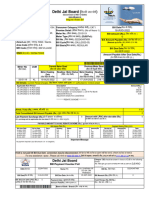

- Delhi Jal BoardDocument2 pagesDelhi Jal BoardLucky GuptaNo ratings yet

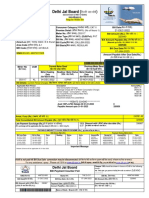

- Delhi Jal BoardDocument2 pagesDelhi Jal BoardGanesh ChandraNo ratings yet

- View PDFDocument2 pagesView PDFSusheel GroverNo ratings yet

- FormDocument1 pageFormmohit singhNo ratings yet

- FormDocument1 pageFormmohit singhNo ratings yet

- Jaan TiwariDocument2 pagesJaan TiwariAshishNo ratings yet

- Sonu KumarDocument2 pagesSonu KumarAshishNo ratings yet

- BudgetDocument2 pagesBudgetshahbaz ahmedNo ratings yet

- 10.accountant - PDF NCL Exam PaperDocument12 pages10.accountant - PDF NCL Exam PapersurjitNo ratings yet

- Satya PrakashDocument1 pageSatya PrakashChaudhary VipinNo ratings yet

- Water BillDocument2 pagesWater BillKAMAL SONINo ratings yet

- View PDFDocument2 pagesView PDFgurdyal672No ratings yet

- Vijay MechatronicsDocument3 pagesVijay Mechatronicsbirpal singhNo ratings yet

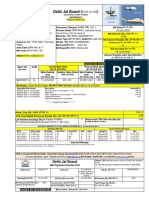

- Delhi Jal BoardDocument2 pagesDelhi Jal BoardVishal KhannaNo ratings yet

- Power Grid Corporation Of India Limited - DOI: शुभाशीष बसु/Subhasis BasuDocument1 pagePower Grid Corporation Of India Limited - DOI: शुभाशीष बसु/Subhasis BasuPowergrid GangtokNo ratings yet

- View PDFDocument2 pagesView PDFAshishNo ratings yet

- View PDFDocument2 pagesView PDFCA Atul NarangNo ratings yet

- View PDFDocument2 pagesView PDFpankaj kumar singhNo ratings yet

- Sonu KumarDocument2 pagesSonu KumarAshishNo ratings yet

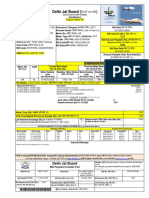

- DJBBill 638386065991Document2 pagesDJBBill 638386065991shubhamNo ratings yet

- TDS CPC, Aaykar Bhawan, Sector - 3, Vaishali, Ghaziabad, U.P. - 201010 Telephone: 0120 - 4814600 (Toll Free) : 18001030344 Website: Email IDDocument3 pagesTDS CPC, Aaykar Bhawan, Sector - 3, Vaishali, Ghaziabad, U.P. - 201010 Telephone: 0120 - 4814600 (Toll Free) : 18001030344 Website: Email IDRajesh SinghNo ratings yet

- Bob It ComptDocument5 pagesBob It ComptPremeshor LaishramNo ratings yet

- Salary SlipDocument1 pageSalary Slipramesh epili100% (1)

- April 2023Document1 pageApril 2023Chetan KaleNo ratings yet

- Invoice Type: Credit Amount 0 Amount Payable 2494.44 2544.33Document1 pageInvoice Type: Credit Amount 0 Amount Payable 2494.44 2544.33Chetan ChoudharyNo ratings yet

- BillDocument2 pagesBillsameerNo ratings yet

- View PDFServletDocument1 pageView PDFServletpraveen139No ratings yet

- Igl BillDocument1 pageIgl BillvikfabNo ratings yet

- Receipt Budget 2016-17Document3 pagesReceipt Budget 2016-17RR AnalystNo ratings yet

- View PDFDocument2 pagesView PDFLAXMIKANTNo ratings yet

- DJBBill 228035718680Document2 pagesDJBBill 228035718680himanshu5513No ratings yet

- Water BillDocument2 pagesWater BilltoolsthriveNo ratings yet

- BillDocument2 pagesBilldevendra4200.dkNo ratings yet

- DJBBill 619938077696Document2 pagesDJBBill 619938077696nitesh mulhallNo ratings yet

- View PDFDocument2 pagesView PDFManoj KumarNo ratings yet

- FormDocument2 pagesFormAasifNo ratings yet

- Ideal Question Paper, GST B.com HONS. SEM 6.Document7 pagesIdeal Question Paper, GST B.com HONS. SEM 6.rtgdfgNo ratings yet

- ViewPDF (1) AbcdDocument2 pagesViewPDF (1) Abcdshivadigi3No ratings yet

- View PDFDocument2 pagesView PDFAditya PanwarNo ratings yet

- View PDFDocument1 pageView PDF02051974No ratings yet

- DJBBill 540734008390Document2 pagesDJBBill 540734008390shubhamNo ratings yet

- View PDFDocument2 pagesView PDFthapliyalneeraj1985No ratings yet

- Air Net ServicesDocument1 pageAir Net Servicesbirpal singhNo ratings yet

- Dinesh Medical Store 17-18 DRC 07Document2 pagesDinesh Medical Store 17-18 DRC 07skd9559No ratings yet

- View PDFDocument1 pageView PDFBashir KhatriNo ratings yet

- RSCFA Mock Test III - Summary4576Document4 pagesRSCFA Mock Test III - Summary4576vivek sharmaNo ratings yet

- GSR 308 (E) 22 May 2020 Emission Standards Bharat Stage VI (BS-VI) For QuadricycleDocument11 pagesGSR 308 (E) 22 May 2020 Emission Standards Bharat Stage VI (BS-VI) For Quadricyclebipul rayNo ratings yet

- View PDFDocument2 pagesView PDFKirti SachdevaNo ratings yet

- View PDFDocument2 pagesView PDFManoj kumarNo ratings yet

- Companies Accounts Amendment Rules 2022 - PDFDocument15 pagesCompanies Accounts Amendment Rules 2022 - PDFAnjali SaraogiNo ratings yet

- Electricity Bill-1Document1 pageElectricity Bill-1sharadrastogi321No ratings yet

- View PDFDocument2 pagesView PDFArchit BahugunaNo ratings yet

- Khrab BillDocument1 pageKhrab BillSumit PandeyNo ratings yet