You might also like

- Assessment of Cash Management Practice in Cooperative: Bank of Oromia (In Case Study of Muger Branch)Document42 pagesAssessment of Cash Management Practice in Cooperative: Bank of Oromia (In Case Study of Muger Branch)dawitkersalfdNo ratings yet

- Zeru ResearchDocument42 pagesZeru ResearchMohammed AbduNo ratings yet

- Wolkite University College of Social Sciences and Humanities Department of Governance and Development Studies Challenges and ProspectsDocument41 pagesWolkite University College of Social Sciences and Humanities Department of Governance and Development Studies Challenges and ProspectsSefa MisebahNo ratings yet

- Bisirat BekeleDocument90 pagesBisirat Bekeleselman bedruNo ratings yet

- ErtalDocument8 pagesErtalYonatanNo ratings yet

- Prepared By-Biruk Gezahegni Advisor - Abdulwali MDocument44 pagesPrepared By-Biruk Gezahegni Advisor - Abdulwali MGadisa GudinaNo ratings yet

- UntitledDocument46 pagesUntitledMagarsaa Qana'iiNo ratings yet

- Microeconomics: Assumptions and DefinitionsDocument12 pagesMicroeconomics: Assumptions and DefinitionssharifNo ratings yet

- The Impact of Financial Management System On Human Resource Utilization (A Case in Gondar Municipality)Document67 pagesThe Impact of Financial Management System On Human Resource Utilization (A Case in Gondar Municipality)meseret sisayNo ratings yet

- Mahder GeletaDocument90 pagesMahder GeletaFanuel MarqosNo ratings yet

- Organizational Culture Assessment on Employee CommitmentDocument34 pagesOrganizational Culture Assessment on Employee CommitmentFiteh KNo ratings yet

- Birhan Final Research PaperDocument109 pagesBirhan Final Research PaperyibeltalNo ratings yet

- Wello Jemal Research1Document43 pagesWello Jemal Research1Javeed ForeverNo ratings yet

- Impact of Internet Banking on Customer RetentionDocument61 pagesImpact of Internet Banking on Customer RetentionsijinyooNo ratings yet

- Bikila ResearchDocument57 pagesBikila ResearchBobasa S AhmedNo ratings yet

- Maximizing Garlic Yield through Mulching and Nitrogen ApplicationDocument39 pagesMaximizing Garlic Yield through Mulching and Nitrogen ApplicationKumsa SanbataNo ratings yet

- Business Research Method Assignment 3 Manish Chauhan (09-1128)Document8 pagesBusiness Research Method Assignment 3 Manish Chauhan (09-1128)manishNo ratings yet

- Misrak SeyoumDocument90 pagesMisrak SeyoumYemane MergiaNo ratings yet

- EEU ERP Project Management Roles AssessmentDocument64 pagesEEU ERP Project Management Roles Assessmentobsinan dejeneNo ratings yet

- Fim ... CH1Document43 pagesFim ... CH1Robel AddisNo ratings yet

- Determinants of Household Water Demand: (Case of Hagereselam Town)Document23 pagesDeterminants of Household Water Demand: (Case of Hagereselam Town)asmelash gideyNo ratings yet

- Ambo University Woliso Campus School of Business and EconomicsDocument23 pagesAmbo University Woliso Campus School of Business and EconomicsDagim Fekadu100% (1)

- Group Assignment QAFMDM Bedelle 2Document16 pagesGroup Assignment QAFMDM Bedelle 2Dejen TagelewNo ratings yet

- Assessment of Non-Performing Loan Management System of Oromia International Bank in Case of Wolkite BranchDocument31 pagesAssessment of Non-Performing Loan Management System of Oromia International Bank in Case of Wolkite BranchAjaib ZinabNo ratings yet

- Measuring St George Brewery's Outbound LogisticsDocument24 pagesMeasuring St George Brewery's Outbound LogisticsZinashbizu LemmaNo ratings yet

- Fi AssignmentDocument9 pagesFi Assignmentyohannes kindalem0% (1)

- (In Case of Arba Minch Town) : Arbaminch, EthiopiaDocument42 pages(In Case of Arba Minch Town) : Arbaminch, EthiopiaSolomon ArbaNo ratings yet

- Table of Contents and Chapter 1 Introduction to EconomicsDocument127 pagesTable of Contents and Chapter 1 Introduction to EconomicsAl kuyuudiNo ratings yet

- Process financial transactions and reportsDocument49 pagesProcess financial transactions and reportsabelu habite neri100% (1)

- 08 - Chapter 1Document25 pages08 - Chapter 1प्रेम हेNo ratings yet

- Capacity Utilisation in Small Scale Industries A StudyDocument10 pagesCapacity Utilisation in Small Scale Industries A StudyBalaji VaradharajanNo ratings yet

- MBA Thesis - FekakFINALDocument82 pagesMBA Thesis - FekakFINALtamrat lisanworkNo ratings yet

- Draft ThesisDocument86 pagesDraft Thesismulugeta wondimuNo ratings yet

- Wollega University Shambu Campus: Advisor: Adugna (MSC)Document38 pagesWollega University Shambu Campus: Advisor: Adugna (MSC)Adugna MegenasaNo ratings yet

- June, 2016.ethiopiaDocument60 pagesJune, 2016.ethiopiasamuel debebeNo ratings yet

- CH 3 Risk and ReturnDocument9 pagesCH 3 Risk and ReturnNikita AggarwalNo ratings yet

- Rift Valley University: Prepared By: Tiblet Tsadiku AdvisorDocument46 pagesRift Valley University: Prepared By: Tiblet Tsadiku Advisorkassahun meseleNo ratings yet

- Alpha University College Mba Program Worksheet (Practice Questions) For The Course Quantitative Analysis For Management DecisionDocument3 pagesAlpha University College Mba Program Worksheet (Practice Questions) For The Course Quantitative Analysis For Management DecisionAmanuel Mitiku100% (1)

- SMU-final Approved OneDocument61 pagesSMU-final Approved OneGadaa TDh100% (1)

- Factors influencing camel milk productionDocument106 pagesFactors influencing camel milk productionraxma cabdilaa guuleedNo ratings yet

- Elias ResearchDocument56 pagesElias Researchtamrat lisanwork100% (2)

- IAS 20 Accounting for Government GrantsDocument19 pagesIAS 20 Accounting for Government GrantsGail Bermudez100% (1)

- Alem GebremedhinDocument101 pagesAlem Gebremedhinbereket tesfayeNo ratings yet

- Department of Project Management: Addis AbabaDocument36 pagesDepartment of Project Management: Addis Ababatesfu dargeNo ratings yet

- Chapter 8 - Portfolio ManagementDocument81 pagesChapter 8 - Portfolio ManagementTRANG NGUYỄN THUNo ratings yet

- Aksum UniversityDocument43 pagesAksum Universitytesfay100% (1)

- Computerized Accounting Boosts Small Business ProfitsDocument44 pagesComputerized Accounting Boosts Small Business ProfitsABDIKARIN MOHAMEDNo ratings yet

- Determinants of Foreign Direct Investment in EthiopiaDocument34 pagesDeterminants of Foreign Direct Investment in Ethiopiakedir mohammedNo ratings yet

- Moh Final, ResearchDocument46 pagesMoh Final, ResearchAbdi HajiNo ratings yet

- Mandya University, Mandya Department of Post-Grduate Studies in CommerceDocument10 pagesMandya University, Mandya Department of Post-Grduate Studies in CommerceRithusri ErNo ratings yet

- Abrahim Research Reseaserch NEWDocument39 pagesAbrahim Research Reseaserch NEWAbdi Mucee TubeNo ratings yet

- Engdawork Tadesse FinalDocument65 pagesEngdawork Tadesse Finaldagim ayenewNo ratings yet

- Risk Focussed Internal Audit (RFIA) : Top of Form 0 False True 0Document9 pagesRisk Focussed Internal Audit (RFIA) : Top of Form 0 False True 0KARIPELLI PRATHIMANo ratings yet

- Assessment of Credit Approval and Collection Management at United BankDocument56 pagesAssessment of Credit Approval and Collection Management at United BankrobelNo ratings yet

- Risk Analysis - 2005 - Cox - Some Limitations of Qualitative Risk Rating SystemsDocument12 pagesRisk Analysis - 2005 - Cox - Some Limitations of Qualitative Risk Rating SystemsSung Woo ShinNo ratings yet

- Harambee University Faculty of Business and Economics Master of Business Administration (MBA)Document6 pagesHarambee University Faculty of Business and Economics Master of Business Administration (MBA)Getu Weyessa100% (1)

- Assessing Critical Success Factors of Rural Road ConstructionDocument55 pagesAssessing Critical Success Factors of Rural Road Constructionmisganaw addisNo ratings yet

- College of Business and Economics Departemt of Ecnomics: Debre Berhan UniversityDocument66 pagesCollege of Business and Economics Departemt of Ecnomics: Debre Berhan Universitybitew yirga100% (1)

- Monthly Reports: Figure 1.1: Revenue/Assistance/Loan Report Me/He 21Document13 pagesMonthly Reports: Figure 1.1: Revenue/Assistance/Loan Report Me/He 21GedionNo ratings yet

- Addis Print 2Document49 pagesAddis Print 2Addishiwot seifuNo ratings yet

- Investment Law in EnglishDocument28 pagesInvestment Law in Englishwudineh debebeNo ratings yet

- Pschology Assignment G-3Document7 pagesPschology Assignment G-3wudineh debebeNo ratings yet

- YRRTRHTHHFNDocument7 pagesYRRTRHTHHFNwudineh debebeNo ratings yet

- Marketing SystemsDocument1 pageMarketing Systemswudineh debebeNo ratings yet

- Nutrition AssignmentDocument10 pagesNutrition Assignmentwudineh debebeNo ratings yet

- Rural Finance 1Document17 pagesRural Finance 1wudineh debebeNo ratings yet

- Eastern Command Head Quarter SN Last With Rate End LastDocument33 pagesEastern Command Head Quarter SN Last With Rate End Lastwudineh debebeNo ratings yet

- With Rock PRINT 19.3.2007 Final East Command FinalDocument171 pagesWith Rock PRINT 19.3.2007 Final East Command Finalwudineh debebeNo ratings yet

- Econometrics 2Document135 pagesEconometrics 2wudineh debebeNo ratings yet

- Eastern Command Head Quarter SN Last With Rate End LastDocument33 pagesEastern Command Head Quarter SN Last With Rate End Lastwudineh debebeNo ratings yet

- The Role of Internal Auditors To Implement IFRS9: Case of Lebanese BanksDocument14 pagesThe Role of Internal Auditors To Implement IFRS9: Case of Lebanese Bankswudineh debebeNo ratings yet

- Starting Health Care Waste Management in Medical InstitutionsDocument22 pagesStarting Health Care Waste Management in Medical Institutionswudineh debebeNo ratings yet

- ITER Electrical Design Handbook Codes & StandardsDocument65 pagesITER Electrical Design Handbook Codes & Standardswudineh debebeNo ratings yet

- 1SDC010001D0201 PDFDocument117 pages1SDC010001D0201 PDFDidik RiswantoNo ratings yet

- Audit Techniques and Audit Evidence: Radu FloreaDocument9 pagesAudit Techniques and Audit Evidence: Radu FloreaNor Hanna DanielNo ratings yet

- 2303-125810 SOC Overview Document - WEBDocument7 pages2303-125810 SOC Overview Document - WEBSergio Teixeira de CarvalhoNo ratings yet

- APO-BABE Constitution and By-laws for Alpha Phi Omega Alumni in Baguio and BenguetDocument11 pagesAPO-BABE Constitution and By-laws for Alpha Phi Omega Alumni in Baguio and BenguetRetro SphinxNo ratings yet

- Ched Es2015Document11 pagesChed Es2015demos reaNo ratings yet

- Standard Unmodified Audit ReportDocument20 pagesStandard Unmodified Audit ReportJonathan QuachNo ratings yet

- Internal Auditing Chapter 26 of Arens Chapter 8 and 11:internal Audit Practices in MalaysiaDocument86 pagesInternal Auditing Chapter 26 of Arens Chapter 8 and 11:internal Audit Practices in MalaysiacuixiNo ratings yet

- Quiz 5 KeyDocument13 pagesQuiz 5 KeyLedayl MaralitNo ratings yet

- Admin ManualDocument122 pagesAdmin ManualBhardwaj MishraNo ratings yet

- Performance Audit PDFDocument17 pagesPerformance Audit PDFEzamUllahNo ratings yet

- CEBU CPAR CENTER - 1st PreboardDocument24 pagesCEBU CPAR CENTER - 1st PreboardMary Alcaflor BarcelaNo ratings yet

- At.3215 - Considering The Risk of Frauds Errors and NOCLARDocument10 pagesAt.3215 - Considering The Risk of Frauds Errors and NOCLARDenny June CraususNo ratings yet

- Chapter 10 - Auditing-1Document31 pagesChapter 10 - Auditing-1Umar FarooqNo ratings yet

- UNOPS Financial Audit of Sri Lanka Coastal Rehab ProjectDocument10 pagesUNOPS Financial Audit of Sri Lanka Coastal Rehab Projectmarie deniegaNo ratings yet

- QMS ProposalDocument22 pagesQMS Proposalflawlessy2kNo ratings yet

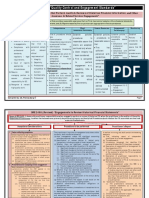

- Chapter 1 "Quality Control and Engagement Standards"Document8 pagesChapter 1 "Quality Control and Engagement Standards"Raul KarkyNo ratings yet

- (Gordon College) Auditing Theory - Part 1Document11 pages(Gordon College) Auditing Theory - Part 1Autumn TirayNo ratings yet

- Internal Factors, External Factors and Earnings Management: Moderating Effects of Auditor Industry SpecializationDocument18 pagesInternal Factors, External Factors and Earnings Management: Moderating Effects of Auditor Industry SpecializationSetiawan RinaldiNo ratings yet

- IT Audit Role and ResponsibilitiesDocument23 pagesIT Audit Role and ResponsibilitiesRudi SyafputraNo ratings yet

- Coursework For AuditDocument7 pagesCoursework For Auditshvfihdjd100% (2)

- Teaching Plan Auditing - PAS2183 - APRIL 2023Document3 pagesTeaching Plan Auditing - PAS2183 - APRIL 2023DIVA RTHININo ratings yet

- Soal Latihan 1 Audit PlanningDocument17 pagesSoal Latihan 1 Audit PlanningBambang HasmaraningtyasNo ratings yet

- CPD TRAINING CENTER FINAL PREBOARD EXAMSDocument5 pagesCPD TRAINING CENTER FINAL PREBOARD EXAMSRandy PaderesNo ratings yet

- Audit I - Chapter 2.1Document5 pagesAudit I - Chapter 2.1Cece LiNo ratings yet

- Auditing Assurance Services and Ethics in Australia 10th Edition Arens Test BankDocument25 pagesAuditing Assurance Services and Ethics in Australia 10th Edition Arens Test BankMelanieThorntonbcmk100% (56)

- Test Bank For Auditing The Art and Science of Assurance Engagements 11th Canadian Edition ArensDocument17 pagesTest Bank For Auditing The Art and Science of Assurance Engagements 11th Canadian Edition ArensJeremySotofmwa100% (39)

- Parkson-2019 Annual Report (Part 2)Document160 pagesParkson-2019 Annual Report (Part 2)Shahdhaan AliNo ratings yet

- Ulster County Industrial Development Agency - March 14, 2012 MinutesDocument8 pagesUlster County Industrial Development Agency - March 14, 2012 MinutesNewPaltzCurrentNo ratings yet

- Seminar AuditDocument7 pagesSeminar AuditMichael BusuiocNo ratings yet

- Audit Opinion PDFDocument2 pagesAudit Opinion PDFIamRuzehl VillaverNo ratings yet

- Hippo Valley Annual Report 2014 - Final Printers' Draft PDFDocument61 pagesHippo Valley Annual Report 2014 - Final Printers' Draft PDFKristi Duran50% (2)