You might also like

- Dwnload Full Principles of Financial Accounting Canadian 1st Edition Weygandt Solutions Manual PDFDocument27 pagesDwnload Full Principles of Financial Accounting Canadian 1st Edition Weygandt Solutions Manual PDFwelked.gourami8nu9d100% (11)

- Principles of Financial Accounting Canadian 1st Edition Weygandt Solutions ManualDocument25 pagesPrinciples of Financial Accounting Canadian 1st Edition Weygandt Solutions ManualDavidBishopsryz100% (41)

- Legal Advice Letter SampleDocument4 pagesLegal Advice Letter SampleMichelle Hatol100% (5)

- Syllabus IntAcc 2&3Document8 pagesSyllabus IntAcc 2&3Valery Joy CerenadoNo ratings yet

- BS-AEF Double Degree ID 120Document27 pagesBS-AEF Double Degree ID 120Blu BNo ratings yet

- Bsa 121Document2 pagesBsa 121rdvgcyfjpgNo ratings yet

- Aei BsaDocument2 pagesAei BsaJulienne VinaraoNo ratings yet

- Aef BsaDocument2 pagesAef BsaJulienne VinaraoNo ratings yet

- R. A. Podar College of Commerce and Economics:, (Autonomous)Document45 pagesR. A. Podar College of Commerce and Economics:, (Autonomous)MANAS GAVHANENo ratings yet

- Tp-Btmp1533-Sem 2 2020.2021Document11 pagesTp-Btmp1533-Sem 2 2020.2021Carrot SusuNo ratings yet

- Cir Pac1163Document4 pagesCir Pac1163NUR AISYAH BINTINISWADI (BG)No ratings yet

- Solutions For Intermediate Accounting 15th Edition by KiesoDocument37 pagesSolutions For Intermediate Accounting 15th Edition by Kiesosadafidoudind100% (16)

- CAF Syllabus PDFDocument88 pagesCAF Syllabus PDFAbdullah AbidNo ratings yet

- CAF SyllabusDocument89 pagesCAF SyllabusFaheem MajeedNo ratings yet

- CAF 1 GridDocument5 pagesCAF 1 GridRiot SkinNo ratings yet

- Caf Syllabus Summary Certificate in Accounts and FinanceDocument89 pagesCaf Syllabus Summary Certificate in Accounts and Financesaad.office101No ratings yet

- لقطة شاشة ٢٠٢٤-٠١-١٤ في ٨.١٧.٥٦ مDocument5 pagesلقطة شاشة ٢٠٢٤-٠١-١٤ في ٨.١٧.٥٦ مbvwdzy9k2sNo ratings yet

- CAF SyllabusDocument89 pagesCAF Syllabusmanadish nawazNo ratings yet

- CPALE TOS Eff May 2019Document25 pagesCPALE TOS Eff May 2019Dale Abrams Dimataga75% (4)

- R. A. Podar College of Commerce and Economics:, (Autonomous)Document45 pagesR. A. Podar College of Commerce and Economics:, (Autonomous)Rashi thiNo ratings yet

- BOA TOS MAS - Revised.eaa.1Document3 pagesBOA TOS MAS - Revised.eaa.1kathleenNo ratings yet

- Table of Specifications Management Accounting & ServicesDocument3 pagesTable of Specifications Management Accounting & ServicesAnonymous PbzIFYXLgNo ratings yet

- Revised 2021 FM ProspectusDocument2 pagesRevised 2021 FM ProspectusGly JapNo ratings yet

- CAF SyllabusDocument88 pagesCAF SyllabusTeen CharaghNo ratings yet

- FAM 2022 - Course Plan - V4Document12 pagesFAM 2022 - Course Plan - V4bharath.bkNo ratings yet

- BS Accountancy 1Document2 pagesBS Accountancy 1Jana May Faustino MedranoNo ratings yet

- Bsba FMDocument2 pagesBsba FMPrecious DionisioNo ratings yet

- Aef ApcDocument2 pagesAef ApcJulienne VinaraoNo ratings yet

- FlowchartDocument2 pagesFlowchartSamuel HutchkinsNo ratings yet

- Far Syllabus PDFDocument25 pagesFar Syllabus PDFChristy Laiza AcuestaNo ratings yet

- Table of Specifications May 2019Document25 pagesTable of Specifications May 2019Justine Joyce Gabia90% (10)

- Table of Specifications Management Advisory Services: Remembering Understanding Application Analyzing Evaluating CreatingDocument25 pagesTable of Specifications Management Advisory Services: Remembering Understanding Application Analyzing Evaluating CreatingJoshua JoshNo ratings yet

- Table of Specifications Management Advisory Services: Remembering Understanding Application Analyzing Evaluating CreatingDocument25 pagesTable of Specifications Management Advisory Services: Remembering Understanding Application Analyzing Evaluating CreatingJoshua JoshNo ratings yet

- CPALE TOS Eff May 2019Document25 pagesCPALE TOS Eff May 2019Joshua JoshNo ratings yet

- 2022-30 BOA TOS FinalDocument38 pages2022-30 BOA TOS Finalsara mejiaNo ratings yet

- Conceptual Framework For Financial Reporting: Assignment Classification Table (By Topic)Document43 pagesConceptual Framework For Financial Reporting: Assignment Classification Table (By Topic)Ching Yin HoNo ratings yet

- BSA Retention Policy PDFDocument17 pagesBSA Retention Policy PDFKezNo ratings yet

- 2008-09 BCA Structure & First YearDocument31 pages2008-09 BCA Structure & First YearmaneganeshNo ratings yet

- Acc C606Document9 pagesAcc C606Gailee VinNo ratings yet

- SOW Form 5 POA Term 2 2020 2021Document9 pagesSOW Form 5 POA Term 2 2020 2021Peta-Gay Brown-JohnsonNo ratings yet

- Remembering Understanding Analyzing Evaluating Creating: TotalDocument6 pagesRemembering Understanding Analyzing Evaluating Creating: TotalannarheaNo ratings yet

- Accounting SyllabusDocument62 pagesAccounting SyllabusAhasanul RahhatNo ratings yet

- Course Checklist ID 120 Bachelor of Science in Legal ManagementDocument2 pagesCourse Checklist ID 120 Bachelor of Science in Legal ManagementGil ChanNo ratings yet

- Table of Specifications - Financial Accounting and ReportingDocument1 pageTable of Specifications - Financial Accounting and ReportingEren CuestaNo ratings yet

- Format For Course Curriculum: Course Title: Course Code: Credit Units: 3 Level: UG Course ObjectivesDocument3 pagesFormat For Course Curriculum: Course Title: Course Code: Credit Units: 3 Level: UG Course Objectivesparakh malhotraNo ratings yet

- BBSC Curriculum From 2021 Intake Onwards - 0Document170 pagesBBSC Curriculum From 2021 Intake Onwards - 0Nishantha FernandoNo ratings yet

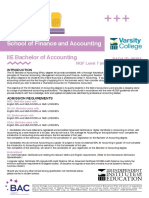

- IIE Bachelor of Accounting Factsheet 2020 V1Document2 pagesIIE Bachelor of Accounting Factsheet 2020 V1Sakila AkterNo ratings yet

- 2019-Intermediate Accounting IIIDocument5 pages2019-Intermediate Accounting IIIdewi nabilaNo ratings yet

- 2021 22 Bbs Exchange Student Module HandbookDocument119 pages2021 22 Bbs Exchange Student Module HandbookanastasiaaNo ratings yet

- Intermediate Accounting Kieso 13th Edition Solutions ManualDocument24 pagesIntermediate Accounting Kieso 13th Edition Solutions ManualJasonLewiscpkx100% (29)

- RPS - Akuntansi Keuangan MenengahDocument11 pagesRPS - Akuntansi Keuangan MenengahSales & CS MenikNo ratings yet

- Os Lii - IvDocument145 pagesOs Lii - Ivteshome neguseNo ratings yet

- CA Foundations Unit Guides 2024Document86 pagesCA Foundations Unit Guides 2024Anna LinNo ratings yet

- Dwnload Full Intermediate Accounting 16th Edition Kieso Solutions Manual PDFDocument6 pagesDwnload Full Intermediate Accounting 16th Edition Kieso Solutions Manual PDFspitznoglecorynn100% (11)

- BBA - 2020 - 2023 SyllabusDocument117 pagesBBA - 2020 - 2023 Syllabuswild worldNo ratings yet

- 2023 OL Subject ReportDocument133 pages2023 OL Subject ReportSand FossohNo ratings yet

- CA Foundations Unit Guide 2022Document88 pagesCA Foundations Unit Guide 2022Ahmed HamedNo ratings yet

- 3.BS Management AccountingDocument17 pages3.BS Management AccountingTurtle ArtNo ratings yet

- Final NEP FYBAF Syllabus 23 24Document86 pagesFinal NEP FYBAF Syllabus 23 24Jai ShahNo ratings yet

- Financial Steering: Valuation, KPI Management and the Interaction with IFRSFrom EverandFinancial Steering: Valuation, KPI Management and the Interaction with IFRSNo ratings yet

- Codification of Statements on Standards for Accounting and Review Services: Numbers 21-24From EverandCodification of Statements on Standards for Accounting and Review Services: Numbers 21-24No ratings yet

- Compilation of ScalesDocument10 pagesCompilation of ScalesEllaNo ratings yet

- Ntrnal QuizletDocument23 pagesNtrnal QuizletEllaNo ratings yet

- Data Coding Schemes and Ethics CodeDocument6 pagesData Coding Schemes and Ethics CodeEllaNo ratings yet

- Flexible BudgetingDocument46 pagesFlexible BudgetingEllaNo ratings yet

- Incremental AnalysisDocument40 pagesIncremental AnalysisEllaNo ratings yet

- (B117) LAW 100 - Estrada v. EscritorDocument2 pages(B117) LAW 100 - Estrada v. EscritormNo ratings yet

- MR Big Operations Briefing Paper - Dayna OrtlandDocument16 pagesMR Big Operations Briefing Paper - Dayna Ortlandapi-573225016No ratings yet

- 4713 17630 2 PBDocument8 pages4713 17630 2 PBhuertas.rafa9299No ratings yet

- Chapter 4 - Organisational Culture and DiversityDocument27 pagesChapter 4 - Organisational Culture and Diversitybangtam9903No ratings yet

- Tolentino V Secretary of FinanceDocument199 pagesTolentino V Secretary of FinanceMarc Dave AlcardeNo ratings yet

- Why Need A Global LanguageDocument4 pagesWhy Need A Global LanguageGabriel Dan BărbulețNo ratings yet

- Use of Technology and The Rule of Evidence in Law: Munish RathiDocument6 pagesUse of Technology and The Rule of Evidence in Law: Munish RathiDennis KimamboNo ratings yet

- Victor Wooten Latin GrooveDocument6 pagesVictor Wooten Latin GrooveMomsua MomsuaNo ratings yet

- Just Right GovernmentDocument6 pagesJust Right Governmentapi-231584882No ratings yet

- Cyber Frauds, Scams and Their VictimsDocument253 pagesCyber Frauds, Scams and Their Victimsarquivoslivros100% (1)

- Prelims in Reading in Philippine History (GE 2)Document16 pagesPrelims in Reading in Philippine History (GE 2)Florence De LeonNo ratings yet

- Law On Sales Discussion ProblemsDocument7 pagesLaw On Sales Discussion ProblemsJoana Christine BuenaventuraNo ratings yet

- Inner Asia Multi-Book Essays: Xinjiang Close-UpDocument9 pagesInner Asia Multi-Book Essays: Xinjiang Close-Upjuan carlos molano toroNo ratings yet

- Arroyo V People GR 220598Document116 pagesArroyo V People GR 220598Fatzie MendozaNo ratings yet

- Aquilino Q. Pimentel JR vs. COMELECDocument15 pagesAquilino Q. Pimentel JR vs. COMELECRenzo JamerNo ratings yet

- 80 Phil LJ697Document15 pages80 Phil LJ697Agent BlueNo ratings yet

- AG Outlines Proposals For Police Reform in MichiganDocument1 pageAG Outlines Proposals For Police Reform in MichiganWXYZ-TV Channel 7 DetroitNo ratings yet

- Taxation Matters Relating To Securities and DerivativesDocument60 pagesTaxation Matters Relating To Securities and DerivativesAnjali JainNo ratings yet

- Role of Income TaxDocument109 pagesRole of Income TaxS. M. IMRAN100% (1)

- Bora AGM 2023 - Notice and Agenda (To COB)Document4 pagesBora AGM 2023 - Notice and Agenda (To COB)Syazril AriefNo ratings yet

- Css Exam Prep GuideDocument297 pagesCss Exam Prep Guidedale huevoNo ratings yet

- Esdc Emp5519Document16 pagesEsdc Emp5519Manan MughalNo ratings yet

- Academic Nda Non-LiaisonDocument1 pageAcademic Nda Non-Liaisonkumarsanjeev.net9511100% (1)

- PIC COURSE SYLLABUS Theories & Perspective On AS (AS 41A)Document3 pagesPIC COURSE SYLLABUS Theories & Perspective On AS (AS 41A)Darwin TolentinoNo ratings yet

- 28.4.2010-Sparkline Jyoti HR Manual2 FINAL - ChangeDocument28 pages28.4.2010-Sparkline Jyoti HR Manual2 FINAL - ChangeHR RiboNo ratings yet

- The Partnership AgreementDocument4 pagesThe Partnership AgreementMelisa FatiNo ratings yet

- Police Powers DissertationDocument7 pagesPolice Powers DissertationPayForAPaperSingapore100% (2)

- Chapter 2 Issues and Challenges Experienced by The Members of The LGBTQ CommunityDocument7 pagesChapter 2 Issues and Challenges Experienced by The Members of The LGBTQ CommunityJan Mark CastilloNo ratings yet

- Chantilly DocumentDocument5 pagesChantilly DocumentAlbNo ratings yet