You might also like

- Loan PolicyDocument5 pagesLoan PolicySoumya BanerjeeNo ratings yet

- Fair Practice CodeDocument4 pagesFair Practice CodeShashi Bhushan PrinceNo ratings yet

- Annexure-A Guidelines For Conventional Banking CustomersDocument2 pagesAnnexure-A Guidelines For Conventional Banking Customersumerbashir743No ratings yet

- To Be Stamped As An AgreementDocument9 pagesTo Be Stamped As An AgreementManikumarNo ratings yet

- Opening of AccountsDocument6 pagesOpening of AccountswubeNo ratings yet

- Deposit Policy: 3.1.1 Savings AccountDocument15 pagesDeposit Policy: 3.1.1 Savings AccountKumar RockyNo ratings yet

- SIB's Policy On Bank Deposits: PreambleDocument8 pagesSIB's Policy On Bank Deposits: PreamblenithiananthiNo ratings yet

- FD_Terms-and-Conditions_0Document10 pagesFD_Terms-and-Conditions_0iamtom101516No ratings yet

- Terms Deposit Rules Terms & ConditionDocument2 pagesTerms Deposit Rules Terms & ConditionKrrish LaraieNo ratings yet

- Most Important TNCDocument4 pagesMost Important TNCsanjana pagareNo ratings yet

- Comprehensive Deposit PolicyDocument13 pagesComprehensive Deposit PolicyShakirkapraNo ratings yet

- Customer AccountsDocument32 pagesCustomer AccountsJitendra VirahyasNo ratings yet

- Module 4 Banking LawDocument12 pagesModule 4 Banking LawNishant RajNo ratings yet

- A) IBA Model Policy On Collection of Cheques - InstrumentsDocument8 pagesA) IBA Model Policy On Collection of Cheques - InstrumentsSudarshan TrichurNo ratings yet

- DownloadDocument14 pagesDownloadashadabral.bjpNo ratings yet

- Prudential NormsDocument22 pagesPrudential NormsLil-daku SainiNo ratings yet

- Banking Principle,,,Ch - 2Document11 pagesBanking Principle,,,Ch - 2Mubarik AhmedinNo ratings yet

- Co LendingDocument7 pagesCo Lending22satendraNo ratings yet

- Auto FD Account DeclarationDocument2 pagesAuto FD Account DeclarationsumitNo ratings yet

- HSBC Model Policy on Bank DepositsDocument6 pagesHSBC Model Policy on Bank DepositsprojectbmsNo ratings yet

- Compensation Policy 28 03 2019Document10 pagesCompensation Policy 28 03 2019Arnab MitraNo ratings yet

- Bob Auto Renewal Sanction Letter 1167708Document6 pagesBob Auto Renewal Sanction Letter 1167708Navin DongreNo ratings yet

- Compensation Policy EnglishDocument5 pagesCompensation Policy EnglishpratibhashawNo ratings yet

- Compensation PolicyDocument17 pagesCompensation PolicySwetha BuridiNo ratings yet

- Compensation Policy 2020 21Document14 pagesCompensation Policy 2020 21K. NikhilNo ratings yet

- Amended RBPF PolicyDocument2 pagesAmended RBPF Policynfk roeNo ratings yet

- RD - Terms and ConditionsDocument9 pagesRD - Terms and ConditionsDhiraj NemadeNo ratings yet

- RBI COVID relief guidelinesDocument4 pagesRBI COVID relief guidelinesvikas bhanvraNo ratings yet

- 22MC894E2203DDDF4E0ABCA714DCE21F8F6CDocument63 pages22MC894E2203DDDF4E0ABCA714DCE21F8F6Caspimpale1999No ratings yet

- RBI Master Circular on Management of Advances for UCBsDocument57 pagesRBI Master Circular on Management of Advances for UCBsashwini.krs80No ratings yet

- Ila FD TermsAndConditions Final ARDocument5 pagesIla FD TermsAndConditions Final ARamerabdullah030No ratings yet

- Customer Compensation PolicyDocument15 pagesCustomer Compensation PolicyVaishnaviNo ratings yet

- Microfinance Loan Policy - SBI - 20.1.2023Document25 pagesMicrofinance Loan Policy - SBI - 20.1.2023Madhusudan ParwalNo ratings yet

- Ajays BankDocument18 pagesAjays BankAyushJainNo ratings yet

- Deposit - Policy in EnglishDocument22 pagesDeposit - Policy in Englishpawan soniNo ratings yet

- Deposit Poicy 2018 20 25082020Document27 pagesDeposit Poicy 2018 20 25082020NK PKNo ratings yet

- Sub: Compensation Cum Customer Relation Policy 2021 - 22: Operation & Services DeptDocument20 pagesSub: Compensation Cum Customer Relation Policy 2021 - 22: Operation & Services DeptAmitKumarNo ratings yet

- Deposit PolicyDocument21 pagesDeposit Policysaurabh shuklaNo ratings yet

- Fair Practices Code: ObjectiveDocument16 pagesFair Practices Code: ObjectiveBADRI VENKATESHNo ratings yet

- Customer Deposit Policy 03.05.2018Document10 pagesCustomer Deposit Policy 03.05.2018Rupan ChakrabortyNo ratings yet

- Policy On Bank Deposits PreambleDocument8 pagesPolicy On Bank Deposits PreambleJOGA SINGHNo ratings yet

- DepositpolicyDocument21 pagesDepositpolicyBalaji Jagalpure100% (1)

- RBI Master Circular on Interest Rates for Co-operative Bank DepositsDocument27 pagesRBI Master Circular on Interest Rates for Co-operative Bank DepositsNeelam PatilNo ratings yet

- Terms and Conditions Personal Loan 1687845092306Document7 pagesTerms and Conditions Personal Loan 1687845092306vishal kademaniNo ratings yet

- Terms and Condition Personal LoanDocument1 pageTerms and Condition Personal LoanSasmita PanigrahyNo ratings yet

- Terms and Conditions Personal Loan 1694167502237Document9 pagesTerms and Conditions Personal Loan 1694167502237LAXMIDHAR BEHERANo ratings yet

- Fair Practices Code April 2023Document4 pagesFair Practices Code April 2023devyanijain553No ratings yet

- PNB Registers 16.7% Growth, Aims Rs 10 Lakh Crore Turnover By2013Document8 pagesPNB Registers 16.7% Growth, Aims Rs 10 Lakh Crore Turnover By2013Anil DhankharNo ratings yet

- Google INSEAD PresentationDocument4 pagesGoogle INSEAD PresentationOjoOluwaseunSamsonNo ratings yet

- Debt To Income RatioDocument7 pagesDebt To Income Ratioco samNo ratings yet

- Special Pre-Approved Personal Loan TermsDocument1 pageSpecial Pre-Approved Personal Loan TermsRam Kannan PNo ratings yet

- Policy On Bank Deposits: PreambleDocument6 pagesPolicy On Bank Deposits: PreambleLukumoni GogoiNo ratings yet

- Product Disclosure Sheet: HSBC Bank Malaysia Berhad Revolving LoanDocument4 pagesProduct Disclosure Sheet: HSBC Bank Malaysia Berhad Revolving Loanthong_wheiNo ratings yet

- Deutsche Bank Compensation PolicyDocument7 pagesDeutsche Bank Compensation PolicySyed Ali AbbasNo ratings yet

- Rbi NPA ASSETS PurchaseDocument48 pagesRbi NPA ASSETS PurchasesunilharlalkaNo ratings yet

- HSBC Everyday Global Account Bonus Interest PromotionDocument3 pagesHSBC Everyday Global Account Bonus Interest PromotionhjwhtfvttrvakjjchoNo ratings yet

- terms_and_conditions_personal_loan_1710164964727Document7 pagesterms_and_conditions_personal_loan_1710164964727THENDRAL 05No ratings yet

- Customer Service in Banks - RBI RulesDocument15 pagesCustomer Service in Banks - RBI RulesRAMESHBABUNo ratings yet

- Unit 4: Ethiopian Bank'S Loans and Advances ProceduresDocument37 pagesUnit 4: Ethiopian Bank'S Loans and Advances Proceduresመስቀል ኃይላችን ነውNo ratings yet

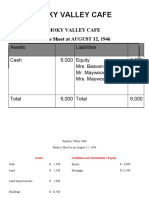

- Smoky Valley CafeDocument3 pagesSmoky Valley CafeRajkumar KrishnamoorthyNo ratings yet

- 9 Acq ReserveDocument43 pages9 Acq ReserveMuthuNo ratings yet

- 23 Negociable Instruments PDFDocument43 pages23 Negociable Instruments PDFCarli Fiorotto100% (1)

- Account Statement 12-10-2023T22 26 37Document1 pageAccount Statement 12-10-2023T22 26 37muawiyakhanaNo ratings yet

- Accounts Receivable ActivityDocument2 pagesAccounts Receivable ActivityFrancine Denise PalacolNo ratings yet

- Fee Deposit SlipDocument1 pageFee Deposit Slipsachingoel19825509No ratings yet

- The Negotiable Instruments Act, 1881 - E-Notes - Udesh Regular - Group 1Document37 pagesThe Negotiable Instruments Act, 1881 - E-Notes - Udesh Regular - Group 1Uday TomarNo ratings yet

- Project DemoDocument59 pagesProject DemoSHIREESHMA TNo ratings yet

- Banking ArindamSingh 200101037Document22 pagesBanking ArindamSingh 200101037TopperNo ratings yet

- CLAW6031 International Financial Crime Problem Week 2, 2022Document2 pagesCLAW6031 International Financial Crime Problem Week 2, 2022yue xuNo ratings yet

- Information On The Constitution of IDBIDocument2 pagesInformation On The Constitution of IDBIPallavi MishraNo ratings yet

- State Bank of Patiala: Rtgs/Neft/Application FormDocument2 pagesState Bank of Patiala: Rtgs/Neft/Application FormAnonymous wfgcPmJYNo ratings yet

- Subsidiary Books - DPP 03 - (Aarambh 2024)Document3 pagesSubsidiary Books - DPP 03 - (Aarambh 2024)Shubh KhandelwalNo ratings yet

- ICICI STACK: Digital Solutions for CustomersDocument6 pagesICICI STACK: Digital Solutions for CustomersMadhav KhuranaNo ratings yet

- Securitizing Rural Microloans ColombiaDocument2 pagesSecuritizing Rural Microloans ColombiaMikeNo ratings yet

- Unit Test: The Accounting Cycle Part A: Completing The Accounting CycleDocument7 pagesUnit Test: The Accounting Cycle Part A: Completing The Accounting CycleKevin PanesarNo ratings yet

- Module 1 Notes and Loans Receivable PDFDocument43 pagesModule 1 Notes and Loans Receivable PDFALEXA GENMARY GULFAN0% (1)

- Account StatementDocument12 pagesAccount StatementPRABHAKAR REDDY TBSF - TELANGANANo ratings yet

- 29 - Speech by Dr. Deepali Pant Joshi, Executive Director, Reserve Bank of IndiaDocument11 pages29 - Speech by Dr. Deepali Pant Joshi, Executive Director, Reserve Bank of IndiagirishrajsNo ratings yet

- Fin433 Dynamos 1Document27 pagesFin433 Dynamos 1Mohammad Fahim HossainNo ratings yet

- Visa EMV 3DS Compliant Vendor Product List - 30mar2022Document11 pagesVisa EMV 3DS Compliant Vendor Product List - 30mar2022Ahmed AyadNo ratings yet

- Acct Statement - XX6550 - 09122023Document6 pagesAcct Statement - XX6550 - 09122023seapause26No ratings yet

- Banking Related GamesDocument5 pagesBanking Related GamesSoru Granale BalingbingNo ratings yet

- SidbiDocument3 pagesSidbiPaavni SharmaNo ratings yet

- Sonam Phoenix Refund Form 1Document1 pageSonam Phoenix Refund Form 1pema lhamoNo ratings yet

- JP Morgan Chase & Co History, Products, WorkforceDocument15 pagesJP Morgan Chase & Co History, Products, WorkforceAjeet YadavNo ratings yet

- Domiciliation RequestDocument2 pagesDomiciliation RequestOtunba Adeyemi Kingsley100% (3)

- Future Value InggrisDocument2 pagesFuture Value InggrisDian AgustinaNo ratings yet

- List of Documents For TrustDocument4 pagesList of Documents For TrustSunil SoniNo ratings yet

- Histori TransaksiDocument4 pagesHistori TransaksiRita PratiwiNo ratings yet