You might also like

- Lecture-6 Adjusted Trial BalanceDocument22 pagesLecture-6 Adjusted Trial BalanceWajiha NadeemNo ratings yet

- Adjusting ProcessDocument57 pagesAdjusting ProcessMarquez, Lynn Andrea L.No ratings yet

- Accounting LM3Document6 pagesAccounting LM3Nathan Kurt LeeNo ratings yet

- Accounting Chapter 3: Adjusting The AccountsDocument16 pagesAccounting Chapter 3: Adjusting The Accountskareem abozeedNo ratings yet

- DDA 1 Niaga C Materials - 4th MeetingDocument32 pagesDDA 1 Niaga C Materials - 4th MeetingZenalina Hadi PutriNo ratings yet

- Lesson 3b Adjusting The AccountsDocument3 pagesLesson 3b Adjusting The AccountsBenedict CladoNo ratings yet

- Module 4 Completion The Accounting CycleDocument27 pagesModule 4 Completion The Accounting CycleJane Russel SolatorioNo ratings yet

- Introduction To Accounting - Adjusting EntriesDocument39 pagesIntroduction To Accounting - Adjusting EntriesRon Hoover Mercene100% (1)

- Adj. EntriesDocument16 pagesAdj. EntriesBea Nicole EstradaNo ratings yet

- Preparation of Adjusting EntriesDocument25 pagesPreparation of Adjusting EntriesMemey C.100% (1)

- Adjusting Entry1 - AnswerDocument9 pagesAdjusting Entry1 - AnswerReighjon Ashley C. Tolentino100% (1)

- ADJUSTING ENTRIES NotesDocument6 pagesADJUSTING ENTRIES NotesDE GUZMAN Cristian MarlonNo ratings yet

- FINAL FABM2 Handouts #3.pdf  Version 1Document12 pagesFINAL FABM2 Handouts #3.pdf  Version 1Kristy Veyna BautistaNo ratings yet

- Adjustment Process NotesDocument4 pagesAdjustment Process NotesMa. Clovel MosasoNo ratings yet

- Notes Adjusting EntriesDocument14 pagesNotes Adjusting EntriesGelesabeth Garcia100% (1)

- AEC 12 - Adjusting EntriesDocument38 pagesAEC 12 - Adjusting EntriesCarlo Jade TuhodNo ratings yet

- Definition of ReceivableDocument9 pagesDefinition of Receivableegram2022No ratings yet

- CH 1Document11 pagesCH 1alemayehuNo ratings yet

- Far ReviewerDocument9 pagesFar ReviewerKathlen PilarNo ratings yet

- Unearned Revenue 2 Methods of Recording Unearned Income Income Method Liability MethodDocument2 pagesUnearned Revenue 2 Methods of Recording Unearned Income Income Method Liability MethodJennilou AñascoNo ratings yet

- Chapter 6 ReceivablesDocument8 pagesChapter 6 ReceivablesHaileluel WondimnehNo ratings yet

- Purpose of Adjusting Entries: Depreciation Expense Depreciable Value Estimated Useful LifeDocument7 pagesPurpose of Adjusting Entries: Depreciation Expense Depreciable Value Estimated Useful LifeJhon Robert Belando100% (1)

- AdjustmentsDocument18 pagesAdjustmentsIca MontanoNo ratings yet

- BS1 Basic AccountingDocument16 pagesBS1 Basic AccountingLoren MarcialNo ratings yet

- Midterm Exam-Adjusting EntriesDocument5 pagesMidterm Exam-Adjusting EntriesHassanhor Guro BacolodNo ratings yet

- Adjusting Journal EntriesDocument3 pagesAdjusting Journal EntriesZonio Nina Bonita T.No ratings yet

- Adjusting ProcessDocument16 pagesAdjusting ProcessJenny SaynoNo ratings yet

- 3-Adjusting EntriesDocument71 pages3-Adjusting EntriesKei Tamundong100% (1)

- Adjusting EntriesDocument9 pagesAdjusting EntriesCharmaine Montimor OrdonioNo ratings yet

- Accounting Concepts and PrinciplesDocument16 pagesAccounting Concepts and PrinciplesKristine Lei Del MundoNo ratings yet

- Basic Accounting Lecture 2Document22 pagesBasic Accounting Lecture 2Alpha HoNo ratings yet

- Adjusting The Book of AccountsDocument33 pagesAdjusting The Book of Accountsjoshua zabala100% (1)

- Notes On Adjusting EntriesDocument6 pagesNotes On Adjusting EntriesRedNo ratings yet

- Accounting For Operating LeaseDocument4 pagesAccounting For Operating LeaseMhico MateoNo ratings yet

- FOA Completing The Accounting Cycle For A Service Business 5Document36 pagesFOA Completing The Accounting Cycle For A Service Business 5hzp6kgvkzxNo ratings yet

- Adjustment Process NotesDocument6 pagesAdjustment Process NotesNicole ElaineNo ratings yet

- ADJUSTING ENTRIES Part 1Document6 pagesADJUSTING ENTRIES Part 1MOCHI SSABELLENo ratings yet

- Adjusting EntriesDocument2 pagesAdjusting Entriesitsayuhthing100% (1)

- Adjusting Entries: Impairment Loss of ReceivablesDocument16 pagesAdjusting Entries: Impairment Loss of ReceivablesL Onifur100% (1)

- M7B Adjusting Process Overview and Accrued IncomeDocument3 pagesM7B Adjusting Process Overview and Accrued IncomeCharles Eli AlejandroNo ratings yet

- Sas Certified Accounting Technician Level 1 Module 2Document29 pagesSas Certified Accounting Technician Level 1 Module 2Plame GaseroNo ratings yet

- Adjusting Entries NotesDocument5 pagesAdjusting Entries NoteswingNo ratings yet

- Accruals & Defferals Chapter-3Document6 pagesAccruals & Defferals Chapter-3mareg malgeNo ratings yet

- Chapter 8 Financial Liability - Notes PayableDocument35 pagesChapter 8 Financial Liability - Notes Payablewala akong pake sayoNo ratings yet

- ADJUSTING ENTRIES Answer QUIZ ACCRUALS & DEFERRALSDocument5 pagesADJUSTING ENTRIES Answer QUIZ ACCRUALS & DEFERRALSHassanhor Guro BacolodNo ratings yet

- Defferals and Accruals Transportation Cost Exercises Per Lecture Dated Dec. 12 2022Document2 pagesDefferals and Accruals Transportation Cost Exercises Per Lecture Dated Dec. 12 2022lheamaecayabyab4No ratings yet

- ADJUSTING ENTRIES With Answers by AlagangWencyDocument3 pagesADJUSTING ENTRIES With Answers by AlagangWencyHello KittyNo ratings yet

- Fundamentals of Accounting Part 2Document20 pagesFundamentals of Accounting Part 2MICHAEL DIPUTADO100% (1)

- Adjusting Entries and Adjusted Trial BalanceDocument19 pagesAdjusting Entries and Adjusted Trial Balancesunny sideNo ratings yet

- Handouts ACCOUNTING-2Document39 pagesHandouts ACCOUNTING-2Marc John IlanoNo ratings yet

- ACGA 504 1 With AnswerDocument22 pagesACGA 504 1 With AnswerEliza BethNo ratings yet

- Adjusting Entry - AnswerDocument8 pagesAdjusting Entry - AnswerReighjon Ashley C. TolentinoNo ratings yet

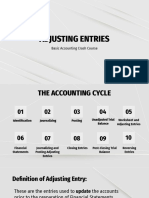

- Adjusting Entries: Basic Accounting Crash CourseDocument77 pagesAdjusting Entries: Basic Accounting Crash CoursesmileseptemberNo ratings yet

- FABM1 11 Quarter 4 Week 1 Las 1Document1 pageFABM1 11 Quarter 4 Week 1 Las 1Janna PleteNo ratings yet

- Adjusting EntriesDocument37 pagesAdjusting Entriesallijah100% (1)

- Additional Lesson Materials - Adjusting EntriesDocument9 pagesAdditional Lesson Materials - Adjusting EntriesMemey C.No ratings yet

- PPP Business Transaction AnalysisDocument16 pagesPPP Business Transaction AnalysisInitiative customsNo ratings yet

- Adjusting Entries - Theory #4Document27 pagesAdjusting Entries - Theory #4Rae Antonette Solana100% (1)

- ACCT 251 Practice Set 2021 - 1Document28 pagesACCT 251 Practice Set 2021 - 1Earl Justine FerrerNo ratings yet

- Class Action Lawsuit - Nivea My SilhouetteDocument14 pagesClass Action Lawsuit - Nivea My SilhouetteJeff OrensteinNo ratings yet

- TALVARDocument4 pagesTALVARhasithaNo ratings yet

- Australia - Measures Affecting Importation of Salmon: Appellate Body ReportDocument11 pagesAustralia - Measures Affecting Importation of Salmon: Appellate Body ReportAditya Pratap SinghNo ratings yet

- Riches v. Simpson Et Al - Document No. 3Document3 pagesRiches v. Simpson Et Al - Document No. 3Justia.comNo ratings yet

- Fco Rail Scrap 08 - 04Document11 pagesFco Rail Scrap 08 - 04Raghavendra100% (1)

- Global Citizenship: Jesus G. Valenzona JRDocument10 pagesGlobal Citizenship: Jesus G. Valenzona JRJesus Valenzona Jr.No ratings yet

- Tax Challenges Arising From DigitalisationDocument250 pagesTax Challenges Arising From DigitalisationlaisecaceoNo ratings yet

- Covered California Grants: For Outreach To IndividualsDocument2 pagesCovered California Grants: For Outreach To IndividualsKelli RobertsNo ratings yet

- Instructions: Personal History Statement FILE NODocument6 pagesInstructions: Personal History Statement FILE NONichole Dianne Dime DiazNo ratings yet

- Application Form: I.K. Akhunbaev Kyrgyz State Medical Academy-Bishkek, Kyrgy RepublicDocument3 pagesApplication Form: I.K. Akhunbaev Kyrgyz State Medical Academy-Bishkek, Kyrgy RepublicsalimNo ratings yet

- PIChE Code of Ethics and Code of Good Governance Alignment MatrixDocument10 pagesPIChE Code of Ethics and Code of Good Governance Alignment MatrixBabeejay2No ratings yet

- Natural Justice and Institutional DecisionsDocument6 pagesNatural Justice and Institutional DecisionsLMRP2 LMRP2No ratings yet

- Clinical Investigation Dossier - List of Documents Required by ANSM and CPPDocument5 pagesClinical Investigation Dossier - List of Documents Required by ANSM and CPPPoupeney ClothildeNo ratings yet

- Crimson Skies (2000) ManualDocument37 pagesCrimson Skies (2000) ManualJing CaiNo ratings yet

- April11.2014 Dspeaker Feliciano Belmonte, Jr.'s Statement On The Divorce Bill and Possible Abortion BillDocument1 pageApril11.2014 Dspeaker Feliciano Belmonte, Jr.'s Statement On The Divorce Bill and Possible Abortion Billpribhor2No ratings yet

- Medical Certificate TemplateDocument1 pageMedical Certificate TemplateAnjo Alba100% (1)

- Immunization RecordDocument1 pageImmunization RecordJordan Simmons ThomasNo ratings yet

- AK Opening StatementDocument1 pageAK Opening StatementPaul Nikko DegolladoNo ratings yet

- Yamaha Digital Multi-Function Command Link Tachometer, Square 6y8-8350t-01-00 EbayDocument1 pageYamaha Digital Multi-Function Command Link Tachometer, Square 6y8-8350t-01-00 EbayYoises SolisNo ratings yet

- Raw Jute Consumption Reconciliation For 2019 2020 Product Wise 07.9.2020Document34 pagesRaw Jute Consumption Reconciliation For 2019 2020 Product Wise 07.9.2020Swastik MaheshwaryNo ratings yet

- De Leon Vs EsperonDocument21 pagesDe Leon Vs EsperonelobeniaNo ratings yet

- Export Import Procedures and Documentation in India PDFDocument2 pagesExport Import Procedures and Documentation in India PDFTerraNo ratings yet

- M-2022-008 - Guidelines On The Submission of The SupplementalDocument3 pagesM-2022-008 - Guidelines On The Submission of The Supplementalwilma balandoNo ratings yet

- Chua v. Absolute Management Corp.Document10 pagesChua v. Absolute Management Corp.Hv EstokNo ratings yet

- Boy Scouts of The Philippines vs. Commission On AuditDocument13 pagesBoy Scouts of The Philippines vs. Commission On AuditWendy PeñafielNo ratings yet

- Nietzsche and The Origins of ChristianityDocument20 pagesNietzsche and The Origins of ChristianityElianMNo ratings yet

- NRDA NOC Received For A FileDocument2 pagesNRDA NOC Received For A FileMuktesh SwamyNo ratings yet

- Sane Retail Private Limited,: Grand TotalDocument1 pageSane Retail Private Limited,: Grand TotalBhaskarNo ratings yet

- 2024 CPA Information Systems & Controls (ISC) Mock Exam AnswersDocument52 pages2024 CPA Information Systems & Controls (ISC) Mock Exam AnswerscraigsappletreeNo ratings yet

- Record of Barangay Inhabitants by Household: Date AccomplishedDocument3 pagesRecord of Barangay Inhabitants by Household: Date Accomplishedrandy hernandez100% (2)