You might also like

- Management Control System Chapter 1Document14 pagesManagement Control System Chapter 1raplyhollow_68780740No ratings yet

- Management Control SystemsDocument287 pagesManagement Control SystemsMurtaza A Zaveri100% (2)

- Dode - Ebook MANAGEMENT CONTROL SYSTEMSDocument286 pagesDode - Ebook MANAGEMENT CONTROL SYSTEMSannisah nsa20100% (1)

- Nature of Management Control System: Mcs Is Must For Organisations Practicing DecentralisationDocument15 pagesNature of Management Control System: Mcs Is Must For Organisations Practicing DecentralisationdevilNo ratings yet

- Management Control System Module 1 NotesDocument14 pagesManagement Control System Module 1 NotesBhavnikNo ratings yet

- A222 - Topic 1 MacsDocument24 pagesA222 - Topic 1 MacsfiqNo ratings yet

- Management Control SystemDocument324 pagesManagement Control Systemnesma sooppi100% (1)

- 01 - The Nature of Management Control SystemsDocument28 pages01 - The Nature of Management Control Systemsjasonkurniawan21No ratings yet

- Mcs Ch1 s1 Dan MaksiDocument25 pagesMcs Ch1 s1 Dan MaksiFauzia RahmahNo ratings yet

- Using Diagnostic and Interactive Control SystemDocument20 pagesUsing Diagnostic and Interactive Control SystemNovi KusumaNo ratings yet

- Chapter Contents: Chapter 1 Introduction To Management Control SystemDocument10 pagesChapter Contents: Chapter 1 Introduction To Management Control SystemNesru SirajNo ratings yet

- MCS1st SessionDocument29 pagesMCS1st SessionLea WigiartiNo ratings yet

- CH 1 The Nature of Management Control SystemsDocument21 pagesCH 1 The Nature of Management Control SystemsAurellia AngelineNo ratings yet

- Framework For Analysis: Ikke Devlina Yulidar 0510233076Document4 pagesFramework For Analysis: Ikke Devlina Yulidar 0510233076Ikke DephlinaNo ratings yet

- Nature of Management Control SystemDocument28 pagesNature of Management Control Systemurvidave1231211No ratings yet

- CH 1 Nature of MCSDocument28 pagesCH 1 Nature of MCSp4priyaaNo ratings yet

- SPM 1Document18 pagesSPM 1Alia AzharaNo ratings yet

- The Internal Auditing Handbook Supplement Five Management ControlsDocument14 pagesThe Internal Auditing Handbook Supplement Five Management ControlstgaNo ratings yet

- MCS All ChaptersDocument52 pagesMCS All Chaptersrohitkamble09No ratings yet

- Nature of Management Control System: Dr. Aayat FatimaDocument18 pagesNature of Management Control System: Dr. Aayat FatimaKashif TradingNo ratings yet

- Modified Chapter 1Document7 pagesModified Chapter 1Rahul GargNo ratings yet

- MANAGEMENT CONTROL SYSTEM by LlahmDocument18 pagesMANAGEMENT CONTROL SYSTEM by Llahmmelow_issNo ratings yet

- Introduction: Meaning Nature and Basic Concepts: ObjectivesDocument16 pagesIntroduction: Meaning Nature and Basic Concepts: ObjectivesKetema AsfawNo ratings yet

- Management Control System CH5Document36 pagesManagement Control System CH5Dinaol Teshome100% (1)

- TOPIC 8-ControllingDocument19 pagesTOPIC 8-Controllingrani aliasNo ratings yet

- Management Control Systems QDocument12 pagesManagement Control Systems QramyasrivinaNo ratings yet

- Management Control SystemsDocument14 pagesManagement Control SystemsTejashree SavantNo ratings yet

- CH 09 ImaimDocument27 pagesCH 09 Imaimkevin echiverriNo ratings yet

- Controlling ProcessDocument3 pagesControlling ProcessRavi Kumar RabhaNo ratings yet

- Mcs NotesDocument196 pagesMcs NotesYonasNo ratings yet

- PPM Article Review-ControllingDocument7 pagesPPM Article Review-Controllinganisha kanbargiNo ratings yet

- Basic Concepts of MCSDocument24 pagesBasic Concepts of MCSamit raningaNo ratings yet

- Management Control SystemsDocument41 pagesManagement Control SystemsAmardeep KumarNo ratings yet

- Management Control SystemDocument11 pagesManagement Control Systemi_sonetNo ratings yet

- For ManagementDocument13 pagesFor Managementsyed adilNo ratings yet

- Mcs Unit1 p1Document15 pagesMcs Unit1 p1imranNo ratings yet

- Controlling, Delegation and Interdepartment CoordinationDocument18 pagesControlling, Delegation and Interdepartment Coordinationmann chalaNo ratings yet

- Management Control SystemDocument5 pagesManagement Control SystemArjun Sukumaran100% (1)

- Chapter 2: Goal Congruence and Management Control in Different OrganisationsDocument16 pagesChapter 2: Goal Congruence and Management Control in Different OrganisationsNhung KiềuNo ratings yet

- Management Control SystemsDocument9 pagesManagement Control SystemsKetan BhandariNo ratings yet

- Management Control SystemDocument3 pagesManagement Control SystemArun NagarNo ratings yet

- Assignment On Management Control SystemDocument4 pagesAssignment On Management Control SystemFelix Yesudas0% (1)

- CH-7 MGTDocument5 pagesCH-7 MGTwaster dessieNo ratings yet

- Inflation AccountingDocument24 pagesInflation AccountingAbhinanda BhattacharyaNo ratings yet

- Written Report On Control ManagementDocument6 pagesWritten Report On Control ManagementSheda TawasilNo ratings yet

- MGMT-Control (WORD FORMAT)Document14 pagesMGMT-Control (WORD FORMAT)Yae'kult VIpincepe QuilabNo ratings yet

- Management Control System Unit-1Document11 pagesManagement Control System Unit-1sheleftmeNo ratings yet

- The Controlling Function in ManagementDocument50 pagesThe Controlling Function in Managementahetasam75% (4)

- Chapter 2Document22 pagesChapter 2DK BalochNo ratings yet

- Effectiveness of Management Control System in Organisation..Document4 pagesEffectiveness of Management Control System in Organisation..Arjun SukumaranNo ratings yet

- Control System in ManagementDocument12 pagesControl System in ManagementSyed JunaidNo ratings yet

- A Key Component of Management Is ControllingDocument3 pagesA Key Component of Management Is Controllingmyrzakhmet.altynNo ratings yet

- Chapt Er 26: Nature and Process of ControllingDocument15 pagesChapt Er 26: Nature and Process of ControllingYash GuptaNo ratings yet

- Management - ControlDocument20 pagesManagement - Controlrsikira7905No ratings yet

- Nature of MCSDocument29 pagesNature of MCSshabnurNo ratings yet

- Nature of MCSDocument30 pagesNature of MCSshahmonali694100% (1)

- MGT 1 Principles of MGT OrgDocument23 pagesMGT 1 Principles of MGT OrgJomari RealesNo ratings yet

- DF PDFDocument9 pagesDF PDFAnanda DuttaNo ratings yet

- The Importance of Management Control SystemsDocument2 pagesThe Importance of Management Control SystemsISOFINE PRIVATE LIMITEDNo ratings yet

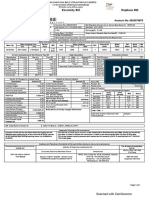

- View BillDocument1 pageView BillISOFINE PRIVATE LIMITEDNo ratings yet

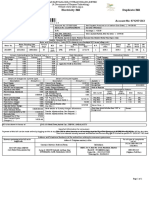

- View BillDocument1 pageView BillISOFINE PRIVATE LIMITEDNo ratings yet

- View BillDocument1 pageView BillISOFINE PRIVATE LIMITEDNo ratings yet

- View Bill LovelyDocument1 pageView Bill LovelyISOFINE PRIVATE LIMITEDNo ratings yet

- View BillDocument1 pageView BillISOFINE PRIVATE LIMITEDNo ratings yet

- Proof Load Test Cert - New 25t Bow Shackle For WOM Double Ram BOPDocument2 pagesProof Load Test Cert - New 25t Bow Shackle For WOM Double Ram BOPmujeebNo ratings yet

- Project Organization: Chapter FourDocument32 pagesProject Organization: Chapter Fourgeachew mihiretuNo ratings yet

- Updated List of Common Codes For CFS 3 2019 10-30-06!40!35Document1 pageUpdated List of Common Codes For CFS 3 2019 10-30-06!40!35Jpvasu DevanNo ratings yet

- Vizpcarshd v001Document10 pagesVizpcarshd v001Cliff OliveiraNo ratings yet

- Bi Draft 2.0Document15 pagesBi Draft 2.0Sofia KNo ratings yet

- Intro To Rice Retail.Document5 pagesIntro To Rice Retail.maha AkhtarNo ratings yet

- Structure 1 - Merged - CompressedDocument3 pagesStructure 1 - Merged - CompressedsujatmikoNo ratings yet

- Preliminary Enga Gement ActivitiesDocument7 pagesPreliminary Enga Gement ActivitiesJuliana ChengNo ratings yet

- Norsok Standard R-003 Safe Use of Lifting EquipmentDocument58 pagesNorsok Standard R-003 Safe Use of Lifting EquipmentDing Liu100% (1)

- Assessment 2: Last Day of Submission: 23 March 2023Document44 pagesAssessment 2: Last Day of Submission: 23 March 2023Adolfo DiazNo ratings yet

- VLSPDFREPORTDocument7 pagesVLSPDFREPORTranvijayNo ratings yet

- Guidelines UGCF BCOMP 2.1 Corporate AccountingDocument7 pagesGuidelines UGCF BCOMP 2.1 Corporate AccountingShiv KumarNo ratings yet

- Test of Control Working PaperDocument4 pagesTest of Control Working PaperMich Angeles50% (2)

- Live Chat USDDocument5 pagesLive Chat USD13217061 DevanandaNo ratings yet

- ADS Chapter 302 USAID Direct ContractingDocument83 pagesADS Chapter 302 USAID Direct Contractinggern strongthornNo ratings yet

- Customer PerspectiveDocument3 pagesCustomer PerspectiveSakshi ShahNo ratings yet

- Summary Chapter 1 Essentials of Entrepreneurship and Small Business ManagementDocument3 pagesSummary Chapter 1 Essentials of Entrepreneurship and Small Business ManagementRameen AlviNo ratings yet

- PPT 02Document33 pagesPPT 02Diaz Hesron Deo SimorangkirNo ratings yet

- 14 - Project Procurement Management (Online LectureDocument19 pages14 - Project Procurement Management (Online LectureAftab AhmedNo ratings yet

- Cbmec 2Document10 pagesCbmec 2Ivy Joy ComediaNo ratings yet

- Ayush GuptaDocument2 pagesAyush GuptaThe Cultural CommitteeNo ratings yet

- Turnover LetterDocument3 pagesTurnover LetterGEARLINES TRUCKING 2022No ratings yet

- Statement of PurposeDocument2 pagesStatement of PurposeMustafa AliNo ratings yet

- Profit Loss DiscountDocument34 pagesProfit Loss DiscountMusicLover21 AdityansinghNo ratings yet

- JD Asst Manager-QA ForgingDocument2 pagesJD Asst Manager-QA ForgingParveen (Atam Valves)No ratings yet

- (KODE 05) - BI - CP (Kuantitatif) - Q1 - (Edited)Document9 pages(KODE 05) - BI - CP (Kuantitatif) - Q1 - (Edited)Arif Kathon SubhektiNo ratings yet

- Biodata Sheet - Vere Technical 2022-2023 FixedDocument7 pagesBiodata Sheet - Vere Technical 2022-2023 FixedjessyNo ratings yet

- Chapter 4 Events After Reporting PeriodDocument2 pagesChapter 4 Events After Reporting Periodsonchaenyoung2No ratings yet

- 1 Logbook For Registered Chs Candidates - Rev 6 19/02/2016Document16 pages1 Logbook For Registered Chs Candidates - Rev 6 19/02/2016Amukelani100% (1)

- V 6 o JDks 4Document3 pagesV 6 o JDks 4Noel JenningsNo ratings yet