You might also like

- CIE AS Level Business Studies NotesDocument19 pagesCIE AS Level Business Studies NotesGharf Sz75% (8)

- Elec 4 OFM4 Module 1. Legal Office ProceduresDocument46 pagesElec 4 OFM4 Module 1. Legal Office ProceduresGalendez JaelNo ratings yet

- Strategic Management ReviewerDocument15 pagesStrategic Management ReviewersuperhoonieNo ratings yet

- Contract To SellDocument2 pagesContract To SellFrancis DayoNo ratings yet

- Organizational Restructuring: Twelve Steps and Key Guidelines to Help Business ManagersFrom EverandOrganizational Restructuring: Twelve Steps and Key Guidelines to Help Business ManagersNo ratings yet

- The Guide To Private Company ValuationDocument15 pagesThe Guide To Private Company ValuationShay BhatterNo ratings yet

- Organizational Development Interventions and Strategies. 1.0Document6 pagesOrganizational Development Interventions and Strategies. 1.0Atique Arif KhanNo ratings yet

- Report On Environment, Social and Governance ReportingDocument18 pagesReport On Environment, Social and Governance ReportingCA Manish BasnetNo ratings yet

- TLE W5 JennilynlucasDocument20 pagesTLE W5 Jennilynlucasrezel joyce catloanNo ratings yet

- Balance Scorecard Implementation Case StudyDocument10 pagesBalance Scorecard Implementation Case StudyAnonymous AGkPX6No ratings yet

- 25213-Article Text-42988-1-10-20230405Document12 pages25213-Article Text-42988-1-10-20230405Dimaz Dwicky Syah PutraNo ratings yet

- Managment Practices Chapter TwoDocument16 pagesManagment Practices Chapter TwoTolu OlusakinNo ratings yet

- Langevin 2013Document14 pagesLangevin 2013nisaNo ratings yet

- The Connection Between Strategy and Structure: Published by Asian Society of Business and Commerce ResearchDocument12 pagesThe Connection Between Strategy and Structure: Published by Asian Society of Business and Commerce ResearchPranav KumarNo ratings yet

- Ece Set of 4Document33 pagesEce Set of 4pranathiNo ratings yet

- Advantages and Disadvantages of Performance ManagementDocument9 pagesAdvantages and Disadvantages of Performance ManagementsaidaNo ratings yet

- The Connection Between Strategy and Structure PDFDocument12 pagesThe Connection Between Strategy and Structure PDFMukul JainNo ratings yet

- Critical Factors Needed To Make Organizations More Effective - EditedDocument9 pagesCritical Factors Needed To Make Organizations More Effective - Editedwangathioli 1No ratings yet

- Performance Measuresof Knowledge ManagementDocument6 pagesPerformance Measuresof Knowledge Managementsamuel petrosNo ratings yet

- Draft 3Document14 pagesDraft 3ariwodola daramolaNo ratings yet

- Ranjith Kumar Performance MainDocument25 pagesRanjith Kumar Performance MainPoovarasan Karnan100% (1)

- Jurnal ManagementDocument4 pagesJurnal ManagementAry Andika PratamaNo ratings yet

- A Study On Strategic Management Practices in Private and Public Sector Banks With Special Reference To Chennai CityDocument20 pagesA Study On Strategic Management Practices in Private and Public Sector Banks With Special Reference To Chennai CitySrinath SmartNo ratings yet

- 3 C 07Document6 pages3 C 07A.s.qudah QudahNo ratings yet

- Ijm 11 05 086Document13 pagesIjm 11 05 086chethan jagadeeswaraNo ratings yet

- Chapter 2 - 13-02-23Document46 pagesChapter 2 - 13-02-23KIKOUNo ratings yet

- EJMCM - Volume 8 - Issue 1 - Pages 1200-1212Document13 pagesEJMCM - Volume 8 - Issue 1 - Pages 1200-1212Morrison Omokiniovo Jessa Snr100% (1)

- Conflict Management Strategies and Organizational Performance (A Survey of Microfinance Institutions in Nairobi)Document16 pagesConflict Management Strategies and Organizational Performance (A Survey of Microfinance Institutions in Nairobi)HINSARMUNo ratings yet

- Journal ArticlesDocument13 pagesJournal ArticlesHur Aftab GambhirNo ratings yet

- Lecture Management 2014Document8 pagesLecture Management 2014nahi11No ratings yet

- Study Material - Strategic ManagementDocument111 pagesStudy Material - Strategic ManagementFactaco IndiaNo ratings yet

- ME Module-1 PDF Final 2Document101 pagesME Module-1 PDF Final 2ANKIT EKKANo ratings yet

- Change ManagementDocument5 pagesChange ManagementJenelle OngNo ratings yet

- The Role of Behavioral Factors and National CulturDocument25 pagesThe Role of Behavioral Factors and National CulturPriyaNo ratings yet

- Education InstitutionDocument8 pagesEducation Institutionrobertottawa144No ratings yet

- Block 1 MS 10 Unit 1Document16 pagesBlock 1 MS 10 Unit 1imranpathan30No ratings yet

- Study MaterialDocument130 pagesStudy MaterialaditiNo ratings yet

- Capstone Unit 2 Assignment - Strategic LeadershipDocument7 pagesCapstone Unit 2 Assignment - Strategic LeadershipGinger RosseterNo ratings yet

- OD InterventionsDocument3 pagesOD InterventionsYash GuptaNo ratings yet

- The Connection Between Strategy and Structure: March 2012Document13 pagesThe Connection Between Strategy and Structure: March 2012Leticia ColónNo ratings yet

- Pmpaper 41Document11 pagesPmpaper 41sushil.tripathiNo ratings yet

- Principle of ManagementDocument144 pagesPrinciple of Management5071 NithishNo ratings yet

- Shiridi Sai ElectricalsDocument11 pagesShiridi Sai ElectricalsVidya BudihalNo ratings yet

- Nature & Structure of An OrganisationDocument11 pagesNature & Structure of An OrganisationMuhammad Sajid Saeed0% (1)

- Organizational Development Interventions and Strategies. 1.0Document6 pagesOrganizational Development Interventions and Strategies. 1.0Atique Arif KhanNo ratings yet

- The Impact of Employee Loyalty Towards Organizational Culture On Organizational Performance Reference To Private Banks in Coimbatore CityDocument6 pagesThe Impact of Employee Loyalty Towards Organizational Culture On Organizational Performance Reference To Private Banks in Coimbatore CityEditor IJTSRDNo ratings yet

- Assignments 1.Document5 pagesAssignments 1.abanoub khalaf 22No ratings yet

- Performance Management Jane Maley: Intended Learning OutcomesDocument34 pagesPerformance Management Jane Maley: Intended Learning OutcomesAindrila BeraNo ratings yet

- Management and Organization Development - completeMU0002Document18 pagesManagement and Organization Development - completeMU0002Shwetadhuri_15No ratings yet

- NMDCDocument42 pagesNMDCLost HumeraNo ratings yet

- Effectiveness of Integrated Financial Management Information System Strategy Implementation PDFDocument29 pagesEffectiveness of Integrated Financial Management Information System Strategy Implementation PDFAnonymous vcDRaofwZNo ratings yet

- Strategy Implications of IS Planning ExecutiveDocument8 pagesStrategy Implications of IS Planning ExecutiveRandy NarinesinghNo ratings yet

- Chapter 1 A Strategic Management Model HRDDocument10 pagesChapter 1 A Strategic Management Model HRDJanrhey EnriquezNo ratings yet

- Microsoft 1 Running Head: Operations Management ProjectDocument11 pagesMicrosoft 1 Running Head: Operations Management ProjectHelen McPhaulNo ratings yet

- Vine 38,1: Conceptual Framework of KM and Contextual Dimensions of OrganizationsDocument5 pagesVine 38,1: Conceptual Framework of KM and Contextual Dimensions of OrganizationsAkanshaNo ratings yet

- Running Head: Management Control System 1Document5 pagesRunning Head: Management Control System 1Sammy DeeNo ratings yet

- Running Head: Management Control System 1Document5 pagesRunning Head: Management Control System 1Sammy DeeNo ratings yet

- Managing Organisational Health Individual P-1 EssayDocument7 pagesManaging Organisational Health Individual P-1 Essaysauganshrestha30No ratings yet

- Key Elements of Strategic Management: Australian Journal of Basic and Applied SciencesDocument8 pagesKey Elements of Strategic Management: Australian Journal of Basic and Applied SciencesHassan ElmiNo ratings yet

- Module 14Document11 pagesModule 14Gemma Daquio - AdovoNo ratings yet

- Review of Related Literature Financial ManagementDocument19 pagesReview of Related Literature Financial ManagementFav TangonanNo ratings yet

- Performance ManagementDocument7 pagesPerformance ManagementKenny NgNo ratings yet

- LeadershipDocument11 pagesLeadershipAmna AnwarNo ratings yet

- Management Control SystemsDocument3 pagesManagement Control SystemsISOFINE PRIVATE LIMITEDNo ratings yet

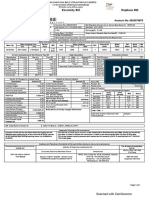

- View BillDocument1 pageView BillISOFINE PRIVATE LIMITEDNo ratings yet

- View BillDocument1 pageView BillISOFINE PRIVATE LIMITEDNo ratings yet

- View BillDocument1 pageView BillISOFINE PRIVATE LIMITEDNo ratings yet

- View BillDocument1 pageView BillISOFINE PRIVATE LIMITEDNo ratings yet

- View Bill LovelyDocument1 pageView Bill LovelyISOFINE PRIVATE LIMITEDNo ratings yet

- JanSamarth Finance PortalDocument5 pagesJanSamarth Finance PortalAkshitaNo ratings yet

- Fire StandardsDocument45 pagesFire StandardskareemulllahNo ratings yet

- No. 7, Jairey Towers, Natham Main Road, Dindigul - 624 003. GSTIN/UIN: 33BDCPJ2107B1ZI State Name: Tamil Nadu, Code: 33Document1 pageNo. 7, Jairey Towers, Natham Main Road, Dindigul - 624 003. GSTIN/UIN: 33BDCPJ2107B1ZI State Name: Tamil Nadu, Code: 33Helan ChristinaNo ratings yet

- Reculta - Investor Deck - 25012019 - Utsav BhattacharjeeDocument22 pagesReculta - Investor Deck - 25012019 - Utsav BhattacharjeeAkash DhimanNo ratings yet

- Last Mile Connectivity: Sponsored byDocument29 pagesLast Mile Connectivity: Sponsored byVinod ChakaravarthyNo ratings yet

- Finals Bcacc MQCDocument12 pagesFinals Bcacc MQCLaurence BacaniNo ratings yet

- 18191101034, Sumaiya HowladarDocument9 pages18191101034, Sumaiya HowladarSumaiya Howladar034No ratings yet

- Pateros Executive Summary 2021Document9 pagesPateros Executive Summary 2021Ruffus TooqueroNo ratings yet

- Blockchain in Supply Management PDFDocument13 pagesBlockchain in Supply Management PDFambujsa1027No ratings yet

- Renewal of Your Optima Restore Floater Insurance PolicyDocument4 pagesRenewal of Your Optima Restore Floater Insurance PolicyAarti BalmikiNo ratings yet

- Yeu Log BookDocument36 pagesYeu Log BookDylanNo ratings yet

- Business EnvironmentDocument23 pagesBusiness Environmentniraj jainNo ratings yet

- BioRes 13 2 2182 Laleicke Editorial Wood Waste Challenges Commun Innov 13522Document2 pagesBioRes 13 2 2182 Laleicke Editorial Wood Waste Challenges Commun Innov 13522nurizzaatiNo ratings yet

- BC Lecture Notes DCSDocument63 pagesBC Lecture Notes DCSBipul KumarNo ratings yet

- Which of The Following Will Not Improve Return On Investment If Other Factors Remain Constant?Document3 pagesWhich of The Following Will Not Improve Return On Investment If Other Factors Remain Constant?Kath LeynesNo ratings yet

- Ed 6061Document1 pageEd 6061darknightNo ratings yet

- Free Download PPT Format Sample Recruitment Strategy TemplateDocument15 pagesFree Download PPT Format Sample Recruitment Strategy TemplateAkash ChauhanNo ratings yet

- Grammar PracticeDocument4 pagesGrammar PracticeMaríaSolGuarinoNo ratings yet

- Elimination Round QuestionnairesDocument5 pagesElimination Round Questionnairesmitakumo uwuNo ratings yet

- Quality Manual CGPLDocument39 pagesQuality Manual CGPLወይኩን ፍቃድከNo ratings yet

- BioDrive CaseDocument10 pagesBioDrive CaseKarim KhalifiNo ratings yet

- Jack Ma Case StudyDocument3 pagesJack Ma Case StudyFaiq UbaidillahNo ratings yet

- Next Generation CR and Sustainability Jobs - 2017Document10 pagesNext Generation CR and Sustainability Jobs - 2017Ghadeer MohammedNo ratings yet

- 2122 1 ES034 Courseware Week6Document14 pages2122 1 ES034 Courseware Week6Christian Breth BurgosNo ratings yet