You might also like

- One Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020From EverandOne Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020No ratings yet

- Nov 2019 Paper 2A Questions EngDocument10 pagesNov 2019 Paper 2A Questions EngTerry MaNo ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- F5 BAFS Final - 1920 - DraftDocument3 pagesF5 BAFS Final - 1920 - Draft4E-27 Tsoi Cheuk Ying (Ada)No ratings yet

- CFP Exam Calculation Workbook: 400+ Calculations to Prepare for the CFP Exam (2018 Edition)From EverandCFP Exam Calculation Workbook: 400+ Calculations to Prepare for the CFP Exam (2018 Edition)Rating: 5 out of 5 stars5/5 (1)

- Cambridge International Advanced Subsidiary and Advanced LevelDocument12 pagesCambridge International Advanced Subsidiary and Advanced LevelSSSNIPDNo ratings yet

- 9706 31 Insert o N 20Document5 pages9706 31 Insert o N 20chirag mehtaNo ratings yet

- November 2020 Insert Paper 31Document12 pagesNovember 2020 Insert Paper 31Shahmeer HasanNo ratings yet

- BAFS_Mock Paper 2A_Set 10_eng.doc (3)Document9 pagesBAFS_Mock Paper 2A_Set 10_eng.doc (3)hannahho0723No ratings yet

- BACC 2021 - 22 Sem 2 - MST Questions 2Document5 pagesBACC 2021 - 22 Sem 2 - MST Questions 2xa. vieNo ratings yet

- Activity 1 - Manufacturing Accounting Cycle: Problem 1Document2 pagesActivity 1 - Manufacturing Accounting Cycle: Problem 1AJ OrtegaNo ratings yet

- Trial Paper 1 2019Document20 pagesTrial Paper 1 2019Cikgu kannaNo ratings yet

- ENT503M MidtermQuestionnaireDocument7 pagesENT503M MidtermQuestionnaireNevan NovaNo ratings yet

- MJ 21Document1 pageMJ 21Ayesha sheikhNo ratings yet

- Fadm / Group Case Study/ Joyo IncDocument3 pagesFadm / Group Case Study/ Joyo IncS GuptaNo ratings yet

- F5 First UT Mock 2021 - 2022Document17 pagesF5 First UT Mock 2021 - 2022Isaac ChowNo ratings yet

- Nov 19 Q PDFDocument9 pagesNov 19 Q PDFTenywa SalimNo ratings yet

- Disposal Group and Subsequent Events Journal EntriesDocument4 pagesDisposal Group and Subsequent Events Journal EntriesSmelly DonkeyNo ratings yet

- Term Exam - PaperDocument11 pagesTerm Exam - Paperhamna wahabNo ratings yet

- 2019 Dse Bafs 2a (E)Document10 pages2019 Dse Bafs 2a (E)lehcarNo ratings yet

- ACCT 312 - Exam 2 (Part 1) - Spring 2022 FinalDocument8 pagesACCT 312 - Exam 2 (Part 1) - Spring 2022 FinalMercy Jerop KimutaiNo ratings yet

- Practice Problems - Notes and Loans Receivable: General InstructionsDocument2 pagesPractice Problems - Notes and Loans Receivable: General Instructionseia aieNo ratings yet

- Singapore Institute of Management: University of London Preliminary Exam 2020Document20 pagesSingapore Institute of Management: University of London Preliminary Exam 2020Kəmalə AslanzadəNo ratings yet

- B326: Advanced Financial Accounting: Take Home Exam For Final Assignment 2020-2021/spring (V1)Document6 pagesB326: Advanced Financial Accounting: Take Home Exam For Final Assignment 2020-2021/spring (V1)Abdulaziz Reda BinshihoonNo ratings yet

- Sample IA QuestionDocument3 pagesSample IA QuestionElisa Ferrer RamosNo ratings yet

- IA 2 Quiz #1 - Investment in BondsDocument2 pagesIA 2 Quiz #1 - Investment in BondsSkeeter Britney CostaNo ratings yet

- Income Statement Chapter 23 QuestionsDocument5 pagesIncome Statement Chapter 23 QuestionsAutoDefenceNo ratings yet

- ACT 205 Assignment - Spring 2019-20Document5 pagesACT 205 Assignment - Spring 2019-20Muhammad AhamdNo ratings yet

- Acctg 205A Quiz NOV. 6,2020Document3 pagesAcctg 205A Quiz NOV. 6,2020Rheu ReyesNo ratings yet

- Audprob Answer 2Document2 pagesAudprob Answer 2venice cambryNo ratings yet

- 2021-06 Icmab FL 001 Pac Year Question June 2021Document3 pages2021-06 Icmab FL 001 Pac Year Question June 2021Mohammad ShahidNo ratings yet

- 9706 m19 QP 12Document12 pages9706 m19 QP 12Ryan Xavier M. BiscochoNo ratings yet

- Intermediate - Accounting - 2 - Quiz - 1.pdf Filename - UTF-8''InterDocument3 pagesIntermediate - Accounting - 2 - Quiz - 1.pdf Filename - UTF-8''InterClaire Magbunag AntidoNo ratings yet

- Buscom Lecture-3Document4 pagesBuscom Lecture-3Dai SyNo ratings yet

- CMA MCQ Self Entrance-1Document2 pagesCMA MCQ Self Entrance-1Ava DasNo ratings yet

- BA3 Mock Exam 01 - PILOT PAPER Nov 2020Document8 pagesBA3 Mock Exam 01 - PILOT PAPER Nov 2020Sanjeev JayaratnaNo ratings yet

- AF2110 Exam QuestionsDocument10 pagesAF2110 Exam QuestionsHOYEE ZHANGNo ratings yet

- Final Exam Accounting Undergraduate ProgramDocument2 pagesFinal Exam Accounting Undergraduate ProgramPutu Deny WijayaNo ratings yet

- Midterm Exam ReviewDocument12 pagesMidterm Exam ReviewAllison0% (1)

- Afar (2018-2022)Document49 pagesAfar (2018-2022)Princess KeithNo ratings yet

- Set B Quiz 2 Final Basic Earning and Diluted Earning Per ShareDocument1 pageSet B Quiz 2 Final Basic Earning and Diluted Earning Per ShareMega MindNo ratings yet

- Philippine School of Business Administration Financial Accounting and Reporting Problems Final ExamDocument11 pagesPhilippine School of Business Administration Financial Accounting and Reporting Problems Final ExamNicole Aragon0% (1)

- Bad Debt To Manufacturing Practise Q 3Document10 pagesBad Debt To Manufacturing Practise Q 3Zin MgNo ratings yet

- Assignment #1 Questions ONLY (ISpace)Document4 pagesAssignment #1 Questions ONLY (ISpace)ziqingyeNo ratings yet

- Cambridge International Advanced Subsidiary and Advanced LevelDocument12 pagesCambridge International Advanced Subsidiary and Advanced LevelKKNo ratings yet

- INTERNATIONAL ACCOUNTING FINAL TEST 2020Document8 pagesINTERNATIONAL ACCOUNTING FINAL TEST 2020Faisel MohamedNo ratings yet

- T3int 2010 Jun QDocument9 pagesT3int 2010 Jun QMuhammad SaadNo ratings yet

- Activity 2 - ReceivableDocument2 pagesActivity 2 - ReceivableMa. Alexandra Teddy Buen0% (1)

- CH 10Document9 pagesCH 10Tien Thanh DangNo ratings yet

- Drills Notes Receivable To Discounting of ReceivableDocument3 pagesDrills Notes Receivable To Discounting of ReceivableVincent AbellaNo ratings yet

- Workshop F2 May 2011Document18 pagesWorkshop F2 May 2011roukaiya_peerkhanNo ratings yet

- Domondon - Acctg 3 - Prelim Quiz 1Document2 pagesDomondon - Acctg 3 - Prelim Quiz 1Prince Anton DomondonNo ratings yet

- AUDIT-INVESTMENTS-REPORTSDocument2 pagesAUDIT-INVESTMENTS-REPORTSSabel FordNo ratings yet

- Accountancy and Auditing-2017Document5 pagesAccountancy and Auditing-2017Jassmine RoseNo ratings yet

- Assignment No. 5 Hoba Franchising Joint ArrangementsDocument4 pagesAssignment No. 5 Hoba Franchising Joint ArrangementsJean TatsadoNo ratings yet

- Exam 1 8Document9 pagesExam 1 8Kenneth DelacruzNo ratings yet

- Audit of Other Income Statement ComponentsDocument6 pagesAudit of Other Income Statement ComponentsVip BigbangNo ratings yet

- 9706 w19 QP 31Document13 pages9706 w19 QP 31PontuChowdhuryNo ratings yet

- CAG v.11.0 1st Wave QuestionsDocument7 pagesCAG v.11.0 1st Wave QuestionsIan Paolo CaylanNo ratings yet

- Ae 191 F-Test 1Document3 pagesAe 191 F-Test 1Venus PalmencoNo ratings yet

- Strat SheetDocument1 pageStrat Sheetcourier12No ratings yet

- Rohit G CV - 21062023-1Document2 pagesRohit G CV - 21062023-1Rohit GNo ratings yet

- Sale ChannelsDocument4 pagesSale ChannelsThùy DươngNo ratings yet

- SC EX 6-1 Bank Account ManagersDocument3 pagesSC EX 6-1 Bank Account ManagersJack WestNo ratings yet

- RHB Report Ind - Consumer - Sector Update - 20230306 - RHB Regional ConsumerDocument4 pagesRHB Report Ind - Consumer - Sector Update - 20230306 - RHB Regional ConsumerjovalNo ratings yet

- Project On Allen SollyDocument81 pagesProject On Allen Sollymkkanna626No ratings yet

- Account Statement 100323 280323Document5 pagesAccount Statement 100323 280323Mainak BhattacharjeeNo ratings yet

- BNP Paribas Steer™: - GlobalDocument17 pagesBNP Paribas Steer™: - Globalmateomejia741No ratings yet

- Bank-Specific and Social Factors of Non-Performing Loans of Pakistani Banking Sector: A Qualitative StudyDocument23 pagesBank-Specific and Social Factors of Non-Performing Loans of Pakistani Banking Sector: A Qualitative StudyInternational Journal of Management Research and Emerging SciencesNo ratings yet

- Ch11 10th Ed Ecsy Cola in InglistanDocument2 pagesCh11 10th Ed Ecsy Cola in InglistanBerke AkkayaNo ratings yet

- Diane Lee - ResumeDocument2 pagesDiane Lee - ResumeDiane LeeNo ratings yet

- Managerial Economics Theory Applications and Cases 8Th Edition Allen Test Bank Full Chapter PDFDocument33 pagesManagerial Economics Theory Applications and Cases 8Th Edition Allen Test Bank Full Chapter PDFarnoldiris65c100% (10)

- Law of Financial Institutions and Securities BLO3405: Vu - Edu.auDocument35 pagesLaw of Financial Institutions and Securities BLO3405: Vu - Edu.auYuting WangNo ratings yet

- Topik 1 Dan 2Document32 pagesTopik 1 Dan 2Joanne ValescaNo ratings yet

- Unit - 1 by Neha PandyaDocument30 pagesUnit - 1 by Neha Pandyarmnjbyjs5qNo ratings yet

- ECommerce - Prof. Mona Nasr Chapter 11Document13 pagesECommerce - Prof. Mona Nasr Chapter 11Ahmed faragNo ratings yet

- Candidate Information Securities Disclosure PolicyDocument1 pageCandidate Information Securities Disclosure PolicyprinceNo ratings yet

- Advanced Financial Accounting IDocument7 pagesAdvanced Financial Accounting IRoNo ratings yet

- Unit 2 - 3 Buying and Handling MerchandiseDocument27 pagesUnit 2 - 3 Buying and Handling MerchandiseroyalmayankojhaNo ratings yet

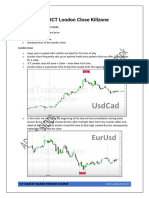

- The ICT London Close KillzoneDocument3 pagesThe ICT London Close Killzonehuda EcharkaouiNo ratings yet

- Ch-4 Risk and ReturnDocument40 pagesCh-4 Risk and ReturnEyuel SintayehuNo ratings yet

- Capstone Partners Middle Market Leveraged Finance Report - June 2021Document2 pagesCapstone Partners Middle Market Leveraged Finance Report - June 2021raielloNo ratings yet

- Futures Sept MagazineDocument55 pagesFutures Sept Magazinebenpmd7No ratings yet

- CCPSDocument2 pagesCCPSelitevaluation2022No ratings yet

- Student Name: - : 1) A) B) C) D)Document6 pagesStudent Name: - : 1) A) B) C) D)bhavik patelNo ratings yet

- Siq 251Document25 pagesSiq 251jazzydefiantNo ratings yet

- Ultimate Social Enterprise Pitch Deck TemplateDocument31 pagesUltimate Social Enterprise Pitch Deck TemplatejaishitaNo ratings yet

- Partnership FormationDocument8 pagesPartnership FormationAira Kaye MartosNo ratings yet

- Adobe Scan 17-Dec-2022Document18 pagesAdobe Scan 17-Dec-2022unnuNo ratings yet

- PFRS 10 - Consolidate FSDocument11 pagesPFRS 10 - Consolidate FSHannah TaduranNo ratings yet

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (13)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- The One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyFrom EverandThe One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyRating: 4.5 out of 5 stars4.5/5 (37)

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantFrom EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantRating: 4.5 out of 5 stars4.5/5 (146)

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- Ledger Legends: A Bookkeeper's Handbook for Financial Success: Navigating the World of Business Finances with ConfidenceFrom EverandLedger Legends: A Bookkeeper's Handbook for Financial Success: Navigating the World of Business Finances with ConfidenceNo ratings yet

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Profit First for Therapists: A Simple Framework for Financial FreedomFrom EverandProfit First for Therapists: A Simple Framework for Financial FreedomNo ratings yet

- Warren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageFrom EverandWarren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageRating: 4.5 out of 5 stars4.5/5 (109)

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineFrom EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineNo ratings yet

- I'll Make You an Offer You Can't Refuse: Insider Business Tips from a Former Mob Boss (NelsonFree)From EverandI'll Make You an Offer You Can't Refuse: Insider Business Tips from a Former Mob Boss (NelsonFree)Rating: 4.5 out of 5 stars4.5/5 (24)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- Bookkeeping: A Beginner’s Guide to Accounting and Bookkeeping for Small BusinessesFrom EverandBookkeeping: A Beginner’s Guide to Accounting and Bookkeeping for Small BusinessesRating: 5 out of 5 stars5/5 (4)

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyFrom EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyRating: 5 out of 5 stars5/5 (1)

- The Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyFrom EverandThe Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyRating: 4 out of 5 stars4/5 (4)