You might also like

- Answers - FA 1Document7 pagesAnswers - FA 1AsmaNo ratings yet

- Business ValuationDocument24 pagesBusiness ValuationBurhan100% (1)

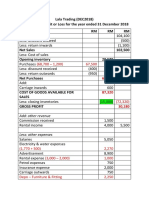

- Lala Trading DEC2018 - SOPL & SOFP DEC2018 AFTER ADJUSTMENTDocument3 pagesLala Trading DEC2018 - SOPL & SOFP DEC2018 AFTER ADJUSTMENTAFIQ RAFIQIN RAHMADNo ratings yet

- Unit-4 Financing DecisionDocument58 pagesUnit-4 Financing DecisionFaraz SiddiquiNo ratings yet

- PART 5 - Statement of Comprehensive Income and Its ElementsDocument6 pagesPART 5 - Statement of Comprehensive Income and Its ElementsHeidee BitancorNo ratings yet

- Financial Leverage and Capital Structure Policy: Conducted by Ranjika Perera & Chanaka KarunasenaDocument53 pagesFinancial Leverage and Capital Structure Policy: Conducted by Ranjika Perera & Chanaka Karunasenacharitha007No ratings yet

- FinanceDocument34 pagesFinanceJared OtienoNo ratings yet

- Financial Ratio Analysis Putting The Numbers To Work PDFDocument5 pagesFinancial Ratio Analysis Putting The Numbers To Work PDFSchemf SalamancaNo ratings yet

- Strategic Financial Management-84-97-8Document1 pageStrategic Financial Management-84-97-8joko waluyoNo ratings yet

- Financial Statement Analysis Chapter 2Document10 pagesFinancial Statement Analysis Chapter 2Houn Pisey100% (1)

- Capital StructureDocument32 pagesCapital Structurestd30000No ratings yet

- Lesson 24 - Note PDFDocument15 pagesLesson 24 - Note PDFFathik FouzanNo ratings yet

- Business ValuationDocument17 pagesBusiness ValuationWassi Ademola MoudachirouNo ratings yet

- Value Added StatementDocument6 pagesValue Added StatementPooja SheoranNo ratings yet

- Capital Structure and Leverage AnalysisDocument57 pagesCapital Structure and Leverage AnalysisbirhanuNo ratings yet

- Four Financial StatementDocument17 pagesFour Financial StatementAbeiku QuansahNo ratings yet

- Chapter 2 FM ContinuedDocument58 pagesChapter 2 FM ContinuedDesu GashuNo ratings yet

- CH01 Introduction To Accounting PDFDocument40 pagesCH01 Introduction To Accounting PDFindra6rusadie100% (1)

- Managing finance profit statement ratiosDocument6 pagesManaging finance profit statement ratiosCarolina Guzman TorresNo ratings yet

- LeveragesDocument50 pagesLeveragesPrem KishanNo ratings yet

- Profitability RatioDocument3 pagesProfitability Ratiobhawna.licdu318No ratings yet

- Corp Fin - Session 11 & 12 - Capital StructureDocument31 pagesCorp Fin - Session 11 & 12 - Capital StructurebipokNo ratings yet

- Chapter 1-4Document20 pagesChapter 1-4BookDownNo ratings yet

- Finanacial Restructuring 2Document48 pagesFinanacial Restructuring 2Jim Mathilakathu100% (2)

- Fundamentals of Accounting: Interpretation of Financial StatementsDocument44 pagesFundamentals of Accounting: Interpretation of Financial Statementscons theNo ratings yet

- Financial Accounting & Analysis: Key ConceptsDocument6 pagesFinancial Accounting & Analysis: Key ConceptsDimpleNo ratings yet

- Lecture 1-Financial Statements I-SDocument75 pagesLecture 1-Financial Statements I-SjamesbinstrateNo ratings yet

- Ratio AnalysisDocument17 pagesRatio AnalysisPGNo ratings yet

- EFIN542 U09 T01 PowerPointDocument26 pagesEFIN542 U09 T01 PowerPointcustomsgyanNo ratings yet

- NIM Genap 2. - in Equity Security Market There Are Two Kind of Analysis Namely Fundamental and TechnicalDocument3 pagesNIM Genap 2. - in Equity Security Market There Are Two Kind of Analysis Namely Fundamental and TechnicalyudaNo ratings yet

- Leverage AND TYPES of LeaverageDocument10 pagesLeverage AND TYPES of Leaveragesalim1321100% (2)

- 33 Advanced AccountingDocument264 pages33 Advanced AccountingKrunal ShahNo ratings yet

- Corporate Finance DecisionsDocument17 pagesCorporate Finance DecisionsSahil SharmaNo ratings yet

- Financial Statements: Prepared By: Muhammad AkhtarDocument11 pagesFinancial Statements: Prepared By: Muhammad AkhtarMuhammad akhtarNo ratings yet

- Leverage: Definition 1Document11 pagesLeverage: Definition 1diptishahNo ratings yet

- LeverageDocument6 pagesLeverageAhsane RNo ratings yet

- AF1401 2020 Autumn Lecture 2Document38 pagesAF1401 2020 Autumn Lecture 2Dhan AnugrahNo ratings yet

- LeverageDocument7 pagesLeverageKomal ThakurNo ratings yet

- Chapter 4 - Balance SheetDocument10 pagesChapter 4 - Balance SheetrtohattonNo ratings yet

- Value Added StatementDocument14 pagesValue Added StatementInigorani0% (2)

- Ratio Analysis:: Analysis of Fin Statements IIDocument88 pagesRatio Analysis:: Analysis of Fin Statements IIHANEESHA BNo ratings yet

- Background Note 2 - Operating LeverageDocument8 pagesBackground Note 2 - Operating LeverageENS SunNo ratings yet

- Dwnload Full Financial Management For Decision Makers Canadian 2nd Edition Atrill Solutions Manual PDFDocument35 pagesDwnload Full Financial Management For Decision Makers Canadian 2nd Edition Atrill Solutions Manual PDFbenboydr8pl100% (12)

- Finance For Managers-Module 4B-LeveragesDocument27 pagesFinance For Managers-Module 4B-LeveragesChayaGandhiNo ratings yet

- LeveragesDocument41 pagesLeveragesSohini ChakrabortyNo ratings yet

- LeverageDocument8 pagesLeverageKalam SikderNo ratings yet

- Leverages 1Document13 pagesLeverages 1Jayant RaneNo ratings yet

- Value Added Metrics: A Group 3 PresentationDocument43 pagesValue Added Metrics: A Group 3 PresentationJeson MalinaoNo ratings yet

- Maximizing Firm Value with Optimal Capital StructureDocument11 pagesMaximizing Firm Value with Optimal Capital StructurebashirNo ratings yet

- Rahul FM - Rahul GoyalDocument5 pagesRahul FM - Rahul GoyalVishvesh GargNo ratings yet

- P&L STATEMENT BREAKDOWN FOR CASE ANALYSISDocument3 pagesP&L STATEMENT BREAKDOWN FOR CASE ANALYSISNeha AroraNo ratings yet

- Payroll AccountingDocument2 pagesPayroll Accountingsunil.ctNo ratings yet

- Corporate Restructuring-ValuationDocument17 pagesCorporate Restructuring-ValuationHimanshi AplaniNo ratings yet

- Statement of Comprehensive IncomeDocument2 pagesStatement of Comprehensive IncomeRandom AcNo ratings yet

- Operating LeverageDocument5 pagesOperating LeverageSalman MajeedNo ratings yet

- 4.1 Value Added: Meaning: Chapter 4: Value Added and Economic Value Added Analysis 85Document5 pages4.1 Value Added: Meaning: Chapter 4: Value Added and Economic Value Added Analysis 85nupurNo ratings yet

- Assignment-2-Group 5Document4 pagesAssignment-2-Group 5Raven RoxasNo ratings yet

- LeverageDocument14 pagesLeverageSurya ElvinoNo ratings yet

- Unit 2 Uderstanding Financial StatementsDocument23 pagesUnit 2 Uderstanding Financial StatementsSG dNo ratings yet

- Operating Leverage: DefinitionDocument3 pagesOperating Leverage: DefinitionJessaNo ratings yet

- TutorialDocument153 pagesTutorialReddyNo ratings yet

- Whats NewDocument36 pagesWhats Newlil telNo ratings yet

- C ApiDocument336 pagesC ApiRaj A DesaiNo ratings yet

- Howto FunctionalDocument20 pagesHowto FunctionalPavan KalyanNo ratings yet

- Howto IpaddressDocument6 pagesHowto IpaddressXerach GHNo ratings yet

- Howto UnicodeDocument13 pagesHowto UnicodeITTeamNo ratings yet

- Howto InstrumentationDocument8 pagesHowto InstrumentationPavan KalyanNo ratings yet

- Howto Isolating ExtensionsDocument8 pagesHowto Isolating Extensionslil telNo ratings yet

- Python Descriptor HowTo GuideDocument21 pagesPython Descriptor HowTo Guideandrea 01No ratings yet

- Howto CursesDocument8 pagesHowto CursesXerach GHNo ratings yet

- Howto SocketsDocument6 pagesHowto SocketskidbarrocoNo ratings yet

- Industrial Attachment ReportDocument47 pagesIndustrial Attachment Reportlil telNo ratings yet

- Accounting For Price Level Changes 1Document8 pagesAccounting For Price Level Changes 1lil telNo ratings yet

- Python Docs ExtendingDocument109 pagesPython Docs ExtendingRaj A DesaiNo ratings yet

- Lesson 2 LeaseDocument26 pagesLesson 2 Leaselil telNo ratings yet

- Conditional Statements in JavaDocument15 pagesConditional Statements in Javalil telNo ratings yet

- Com 322 Sensitivity 2Document11 pagesCom 322 Sensitivity 2lil telNo ratings yet

- Silo - Tips - Student S Attachment Log BookDocument13 pagesSilo - Tips - Student S Attachment Log Booklil telNo ratings yet

- EconomicDocument32 pagesEconomicSeyiNo ratings yet

- Nitafan v. Cir Case DigestDocument1 pageNitafan v. Cir Case DigestNina Majica PagaduanNo ratings yet

- Bos 50847 MCQP 7Document150 pagesBos 50847 MCQP 7keshav bajajNo ratings yet

- W6 Module 5 Dupont System of AnalysisDocument14 pagesW6 Module 5 Dupont System of AnalysisDanica VetuzNo ratings yet

- Feasib ScriptDocument3 pagesFeasib ScriptJeremy James AlbayNo ratings yet

- Exam in Accounting-FinalsDocument5 pagesExam in Accounting-FinalsIyarna YasraNo ratings yet

- P&G Phils Can Claim Tax RefundDocument3 pagesP&G Phils Can Claim Tax RefundKarl MinglanaNo ratings yet

- Adam Smith Father of EconomicsDocument3 pagesAdam Smith Father of EconomicsGleizuly VaughnNo ratings yet

- Business Solution Enterprise Statement of Financial Position As of December 31, 2018 AssetsDocument4 pagesBusiness Solution Enterprise Statement of Financial Position As of December 31, 2018 AssetsCheche Casaljay AmpoanNo ratings yet

- AMICAE Housings Co-OperativeDocument5 pagesAMICAE Housings Co-OperativeTia clemenNo ratings yet

- Form16 Fiserv 2018-19Document8 pagesForm16 Fiserv 2018-19SiddharthNo ratings yet

- Salary Slip NovDocument1 pageSalary Slip NovRahul RajawatNo ratings yet

- Equity Program FAQDocument14 pagesEquity Program FAQNikhil SinghalNo ratings yet

- Module 3 Exercises Statement of Changes in EquityDocument3 pagesModule 3 Exercises Statement of Changes in EquityArjay CorderoNo ratings yet

- 'Unshell' - Rules To Prevent The Misuse of Shell EntitiesDocument8 pages'Unshell' - Rules To Prevent The Misuse of Shell EntitiesKgjkg KjkgNo ratings yet

- Engineering Economy Refresher Set PdfbooksforumDocument5 pagesEngineering Economy Refresher Set PdfbooksforumEdmond BautistaNo ratings yet

- Accounting What The Numbers Mean 10th Edition Marshall Test BankDocument48 pagesAccounting What The Numbers Mean 10th Edition Marshall Test Banklarrybrownjcdnotkfab100% (25)

- Topic 3 -Joint ArrangementsDocument5 pagesTopic 3 -Joint Arrangementsduguitjinky20.svcNo ratings yet

- UNIT-3: Assessment of Firms Section-ADocument6 pagesUNIT-3: Assessment of Firms Section-ANaveenNo ratings yet

- 20 EU / EEA Certificate: Personal DetailsDocument3 pages20 EU / EEA Certificate: Personal Detailsgaga sebiskveradzeNo ratings yet

- Making Capital Investment Decisions Incremental Cash Flows: Skema Business SchoolDocument30 pagesMaking Capital Investment Decisions Incremental Cash Flows: Skema Business Schooldongyi YuNo ratings yet

- Funtional Areas of FinanceDocument3 pagesFuntional Areas of FinanceAyushi TiwariNo ratings yet

- The Cheat Sheet RatiosDocument6 pagesThe Cheat Sheet RatiosDan ButuzaNo ratings yet

- Home Assignments, Week 1, 2023Document4 pagesHome Assignments, Week 1, 2023jovanaNo ratings yet

- 1082 Muhasibat Aqil E.Document12 pages1082 Muhasibat Aqil E.DanielNo ratings yet

- Income From House PropertyDocument6 pagesIncome From House PropertyPraveen EkkaNo ratings yet

- Sales ForecastingDocument16 pagesSales ForecastingvaishalicNo ratings yet

- Business Taxation Prelim PDFDocument30 pagesBusiness Taxation Prelim PDFTrine De LeonNo ratings yet