You might also like

- Wealth MGT QBDocument15 pagesWealth MGT QBAnagha PranjapeNo ratings yet

- Insurance & Risk ManagementDocument8 pagesInsurance & Risk ManagementJASONM22No ratings yet

- Overview of Premium Financed Life InsuranceDocument17 pagesOverview of Premium Financed Life InsuranceProvada Insurance Services100% (1)

- Textbook of Urgent Care Management: Chapter 9, Insurance Requirements for the Urgent Care CenterFrom EverandTextbook of Urgent Care Management: Chapter 9, Insurance Requirements for the Urgent Care CenterNo ratings yet

- Can I Withdraw My Fixed Deposit Without Any Penalties?Document6 pagesCan I Withdraw My Fixed Deposit Without Any Penalties?InvestkraftNo ratings yet

- risk assignmentDocument5 pagesrisk assignmentabebeb967No ratings yet

- Marketing of Financial ServicesDocument6 pagesMarketing of Financial ServicesSolve AssignmentNo ratings yet

- Project Report ON: University of MumbaiDocument55 pagesProject Report ON: University of MumbaiNayak SandeshNo ratings yet

- Consumer Perceptions and Buying Behaviour Towards Life InsuranceDocument28 pagesConsumer Perceptions and Buying Behaviour Towards Life InsuranceMayank MahajanNo ratings yet

- Max New York Life, Axis Bank Sign Bancassurance RelationshipDocument22 pagesMax New York Life, Axis Bank Sign Bancassurance RelationshipAnurag PateriaNo ratings yet

- The Benefit For Life Insurance - AliDocument2 pagesThe Benefit For Life Insurance - Aliyaoping songNo ratings yet

- 6 Lic Surrender ValueDocument1 page6 Lic Surrender ValueAJIT TRADERNo ratings yet

- Life Insurance in India - 4Document7 pagesLife Insurance in India - 4Himansu S MNo ratings yet

- Term Life Insurance PolicyDocument4 pagesTerm Life Insurance PolicyShubham NamdevNo ratings yet

- "ULIP As An Investment AvenueDocument60 pages"ULIP As An Investment AvenueMahesh ThallapelliNo ratings yet

- Actuarial Principles & Premium SettingDocument21 pagesActuarial Principles & Premium Settingd6xm4ng9jtNo ratings yet

- Unit 3 InsuranceDocument29 pagesUnit 3 InsuranceNikita ShekhawatNo ratings yet

- Insurance Commission Exam ReviewerDocument5 pagesInsurance Commission Exam ReviewerApolinar Alvarez Jr.97% (38)

- Commercial Premium Financing: Exit StrategiesDocument3 pagesCommercial Premium Financing: Exit StrategiesKevin WheelerNo ratings yet

- Futura KFD - UAE MSP11934 PDFDocument20 pagesFutura KFD - UAE MSP11934 PDFsardust2020No ratings yet

- Personal Finance Chapter 12Document3 pagesPersonal Finance Chapter 12api-526065196No ratings yet

- Terminologies: 1. Partial Withdrawl:-Unit Policies Provide Flexibility To ItsDocument4 pagesTerminologies: 1. Partial Withdrawl:-Unit Policies Provide Flexibility To ItsRASHMINo ratings yet

- Irda - Hand Book On Life InsuranceDocument12 pagesIrda - Hand Book On Life InsuranceRajesh SinghNo ratings yet

- UNIT 6-Rate MakingDocument7 pagesUNIT 6-Rate Makingsabu lamaNo ratings yet

- Life Insurance HandbookDocument12 pagesLife Insurance HandbookChi MnuNo ratings yet

- Insurance 1 2Document18 pagesInsurance 1 2Udisha SinghNo ratings yet

- Savings Assurance PlanDocument1 pageSavings Assurance Planrajeshdubey7No ratings yet

- Elements of Good Life Insurance PolicyDocument4 pagesElements of Good Life Insurance PolicySaumya JaiswalNo ratings yet

- INSURANCEDocument28 pagesINSURANCEcharuNo ratings yet

- FINANCIAL-LITERACY_073131Document29 pagesFINANCIAL-LITERACY_073131Jennarose PadernosNo ratings yet

- eEASY Save FAQs PDFDocument6 pageseEASY Save FAQs PDFterrygohNo ratings yet

- Chapter 5Document15 pagesChapter 5mark sanadNo ratings yet

- Profile ChangeDocument5 pagesProfile ChangeAbhishekNo ratings yet

- Claim ProcessDocument7 pagesClaim Processbipin1989No ratings yet

- Drive SPRING 2015 Program Mf0018 Insurance and Risk ManagementDocument12 pagesDrive SPRING 2015 Program Mf0018 Insurance and Risk ManagementRoshan KumarNo ratings yet

- RCMF - Loan Against InsuranceDocument8 pagesRCMF - Loan Against InsuranceAnuj KumarNo ratings yet

- Chapter - I: HDFC Standard Life Insurance Company LTD in Customer-Buying Behaviour in Life Insurance IndustryDocument3 pagesChapter - I: HDFC Standard Life Insurance Company LTD in Customer-Buying Behaviour in Life Insurance IndustryNaman NotiyalNo ratings yet

- What Is An InvestmentDocument20 pagesWhat Is An InvestmentSebin SebastianNo ratings yet

- Baf) 1Document8 pagesBaf) 1mesfinabera180No ratings yet

- MF0018Document7 pagesMF0018Pawan Dimri50% (2)

- Assignment Cover Page: Course Code Course TitleDocument5 pagesAssignment Cover Page: Course Code Course TitleMD FySLNo ratings yet

- MGFC20 Ch10 More InsurancesDocument5 pagesMGFC20 Ch10 More Insurancesbingus dingusNo ratings yet

- Safe Money First: Your Guidebook to Annuities and Safe Retirement Financial Planning StrategiesFrom EverandSafe Money First: Your Guidebook to Annuities and Safe Retirement Financial Planning StrategiesNo ratings yet

- Frequently Asked Questions: 1. Why Should I Buy An Insurance PolicyDocument4 pagesFrequently Asked Questions: 1. Why Should I Buy An Insurance PolicySatender KumarNo ratings yet

- Conceptual Framework: ULIP Is A Market Linked Investment Where The Premium Paid Is Invested in FundsDocument7 pagesConceptual Framework: ULIP Is A Market Linked Investment Where The Premium Paid Is Invested in Fundsreliable panditNo ratings yet

- LIFE INSURANCE AS AN INVESTMENTDocument7 pagesLIFE INSURANCE AS AN INVESTMENTNelson MathewNo ratings yet

- InsuranceDocument41 pagesInsuranceClarisse GonzalesNo ratings yet

- 7 Things To Check Before You Buy Your Income Protection PolicyDocument2 pages7 Things To Check Before You Buy Your Income Protection PolicytkeshavNo ratings yet

- Insurance - deciding best insurance for familyDocument3 pagesInsurance - deciding best insurance for familyHarris ArifinNo ratings yet

- Unit 1 LifeDocument10 pagesUnit 1 LifeMohammed HussainNo ratings yet

- Insurance Industry OverviewDocument42 pagesInsurance Industry OverviewAkhilesh desaiNo ratings yet

- Savings Account Home Mortgage Insurance Pension: AnnuityDocument3 pagesSavings Account Home Mortgage Insurance Pension: AnnuityRuffamae BartolomeNo ratings yet

- RISK Chapter 5Document19 pagesRISK Chapter 5Taresa AdugnaNo ratings yet

- Chapter - I: HDFC Standard Life Insurance Company LTD in Customer-Buying Behaviour in Life Insurance IndustryDocument27 pagesChapter - I: HDFC Standard Life Insurance Company LTD in Customer-Buying Behaviour in Life Insurance IndustryNaman NotiyalNo ratings yet

- Benefits of Insurance PoliciesDocument17 pagesBenefits of Insurance PoliciesSaksham MathurNo ratings yet

- RISK Assignment 2Document4 pagesRISK Assignment 2Firaol GeremuNo ratings yet

- Is your insurance company listeningDocument21 pagesIs your insurance company listeningSourabh KulkarniNo ratings yet

- Ballentine's Law 3rd Edition - Sec. UDocument0 pagesBallentine's Law 3rd Edition - Sec. UHilary E. MainsNo ratings yet

- Marine Insurance Claims in ShippingDocument10 pagesMarine Insurance Claims in ShippingldigasNo ratings yet

- New Issue Market: Submitted To: Submitted By: Mrs - Simmi Vashishtha Rupanci Ishu Mba (SM) FDocument28 pagesNew Issue Market: Submitted To: Submitted By: Mrs - Simmi Vashishtha Rupanci Ishu Mba (SM) FrupanciNo ratings yet

- Ic-38 Health Q&aDocument6 pagesIc-38 Health Q&askumaritesNo ratings yet

- ProofofinsuranceDocument4 pagesProofofinsuranceapi-379311219No ratings yet

- Ondeck Asset Securitization Trust II LLC Series 2016 1 Rating ReportDocument16 pagesOndeck Asset Securitization Trust II LLC Series 2016 1 Rating ReportMarkNo ratings yet

- AlopDocument39 pagesAlopabhishekmantri100% (1)

- Michael D Randolph, ResumeDocument2 pagesMichael D Randolph, ResumemdrandolphNo ratings yet

- Quality Control ChecklistDocument7 pagesQuality Control Checklistdarma bonarNo ratings yet

- Understanding the IPO ProcessDocument16 pagesUnderstanding the IPO ProcessZahid BashirNo ratings yet

- Dr. D. Shree Devi - Portability of Health InsuranceDocument10 pagesDr. D. Shree Devi - Portability of Health InsuranceZohaib AhmedNo ratings yet

- User Guide - Reuters Fundamentals PDFDocument631 pagesUser Guide - Reuters Fundamentals PDFHimadri ShuklaNo ratings yet

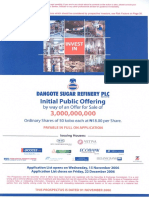

- Dangote Sugar Offer SummaryDocument79 pagesDangote Sugar Offer SummaryBilly LeeNo ratings yet

- Understand Health Insurance in 40 CharactersDocument38 pagesUnderstand Health Insurance in 40 CharactersMitali PathakNo ratings yet

- World Insurance Report 2020Document28 pagesWorld Insurance Report 2020Jose TenorioNo ratings yet

- Technology in Retail LendingDocument31 pagesTechnology in Retail LendingRedSunNo ratings yet

- Ins 210-1-1Document40 pagesIns 210-1-1Daniel AdegboyeNo ratings yet

- Chapter 18 Project Financing FinnertyDocument44 pagesChapter 18 Project Financing FinnertyRachma PratiwiNo ratings yet

- Question Bank FormatDocument5 pagesQuestion Bank Formatmahidpr18No ratings yet

- Merchant Banking: Chapter 1 - IntroductionDocument38 pagesMerchant Banking: Chapter 1 - IntroductionJermaine WeissNo ratings yet

- VIETNAM 2018 SALARY GUIDEDocument31 pagesVIETNAM 2018 SALARY GUIDEChu ToànNo ratings yet

- 2015-2016 Tax Case DigestDocument114 pages2015-2016 Tax Case DigestD Del Sal100% (3)

- Casualty Actuarial Basic Ratemaking Chapter 2Document19 pagesCasualty Actuarial Basic Ratemaking Chapter 2djqNo ratings yet

- SEBIDocument22 pagesSEBIGautam Jayasurya0% (1)

- Funding Chart Book (Book 4)Document75 pagesFunding Chart Book (Book 4)Sharvari jadhavNo ratings yet

- IRDAI Annual Report 2019-20 - EnglishDocument242 pagesIRDAI Annual Report 2019-20 - EnglishKishore mohan ManapuramNo ratings yet

- Chapter-5 Merchant: BankingDocument29 pagesChapter-5 Merchant: BankingaswinecebeNo ratings yet

- BMA 2020 Climate Change Survey ReportDocument16 pagesBMA 2020 Climate Change Survey ReportBernewsAdminNo ratings yet

- IPO/FPO Book Building Process ExplainedDocument80 pagesIPO/FPO Book Building Process Explainedvinodvarghese123100% (1)