You might also like

- Ms December 2021Document15 pagesMs December 2021Kuok Hei LeungNo ratings yet

- ASE20101 Mark-Scheme April-2019Document17 pagesASE20101 Mark-Scheme April-2019YAN YAN TSOINo ratings yet

- 2017 June Mark SchemeDocument20 pages2017 June Mark SchemeMe MeNo ratings yet

- Ms ASE20104Document16 pagesMs ASE20104Aung Zaw HtweNo ratings yet

- June 2021 Mark SchemeDocument17 pagesJune 2021 Mark SchemeElenaNo ratings yet

- 2019 May MS 4ac0 2R PDFDocument9 pages2019 May MS 4ac0 2R PDFmahdiarahman10No ratings yet

- ASE20093 Mark Scheme November 2019Document16 pagesASE20093 Mark Scheme November 2019Myomin Htay100% (4)

- Mark Scheme December 2016: ResultsDocument14 pagesMark Scheme December 2016: ResultsThan Than HtaikNo ratings yet

- ASE20104 Mark Scheme July 2019Document16 pagesASE20104 Mark Scheme July 2019Ti SodiumNo ratings yet

- ASE20104 - Mark Scheme - January 2019Document16 pagesASE20104 - Mark Scheme - January 2019Aung Zaw Htwe88% (8)

- Mark Scheme: September 2020Document15 pagesMark Scheme: September 2020Thaw Thaw SoeNo ratings yet

- AFE 5008 Model Answers for Final ExamsDocument10 pagesAFE 5008 Model Answers for Final ExamsDiana TuckerNo ratings yet

- WAC11 01 Rms 20180815Document36 pagesWAC11 01 Rms 20180815MirHaiderAliShaurovNo ratings yet

- Mark Scheme (Results) Summer 2016: Pearson Edexcel International GCSE Accounting (4AC0) Paper 1Document12 pagesMark Scheme (Results) Summer 2016: Pearson Edexcel International GCSE Accounting (4AC0) Paper 1Vraj PatelNo ratings yet

- 4ac1 02 Rms 20240125Document9 pages4ac1 02 Rms 20240125Nang Phyu Sin Yadanar KyawNo ratings yet

- MS Ase20104Document17 pagesMS Ase20104Aung Zaw HtweNo ratings yet

- Ase20093 01 Results Mark Scheme 20220404 January 2022 SeriesDocument15 pagesAse20093 01 Results Mark Scheme 20220404 January 2022 SeriesTheint ThiriNo ratings yet

- Ms April 2022Document16 pagesMs April 2022Kuok Hei LeungNo ratings yet

- MS Dec-17Document12 pagesMS Dec-17Than Than HtaikNo ratings yet

- MS ASE20104 September 2018 - FINAL REVISEDDocument17 pagesMS ASE20104 September 2018 - FINAL REVISEDAung Zaw HtweNo ratings yet

- 9706 w10 Ms 41Document5 pages9706 w10 Ms 41kanz_h118No ratings yet

- ASE20104 - Mark Scheme - April 2019 PDFDocument15 pagesASE20104 - Mark Scheme - April 2019 PDFAung Zaw HtweNo ratings yet

- Mark Scheme (Provisional)Document24 pagesMark Scheme (Provisional)new yearNo ratings yet

- WAC11 01 MSC 20210517Document24 pagesWAC11 01 MSC 20210517Mashhood Babar ButtNo ratings yet

- Mark Scheme (Results) Summer 2016: Pearson Edexcel IAL in Accounting (WAC11) Paper 01 The Accounting System and CostingDocument30 pagesMark Scheme (Results) Summer 2016: Pearson Edexcel IAL in Accounting (WAC11) Paper 01 The Accounting System and CostingFahim AhmedNo ratings yet

- Mark Scheme (Results) Summer 2016: Pearson Edexcel IAL in Accounting (WAC11) Paper 01 The Accounting System and CostingDocument30 pagesMark Scheme (Results) Summer 2016: Pearson Edexcel IAL in Accounting (WAC11) Paper 01 The Accounting System and CostingFarhad AhmedNo ratings yet

- Mark Scheme (Results) October 2016: Pearson Edexcel IAL in Accounting (WAC11) Paper 01 The Accounting System and CostingDocument29 pagesMark Scheme (Results) October 2016: Pearson Edexcel IAL in Accounting (WAC11) Paper 01 The Accounting System and CostingFarhad AhmedNo ratings yet

- Igcse May 2022 Paper 2R MSDocument10 pagesIgcse May 2022 Paper 2R MSmihirNo ratings yet

- 2017 July Mark SchemeDocument20 pages2017 July Mark SchemeNandar YuNo ratings yet

- Mark Scheme: Extra Assessment Material For First Teaching September 2017Document8 pagesMark Scheme: Extra Assessment Material For First Teaching September 2017shamNo ratings yet

- ASE20104 - Mark Scheme - November 2018Document18 pagesASE20104 - Mark Scheme - November 2018Aung Zaw Htwe100% (3)

- Ms-Ase20098Document13 pagesMs-Ase20098Ti SodiumNo ratings yet

- Mark Scheme (Results) : January 2017Document27 pagesMark Scheme (Results) : January 2017Farhad AhmedNo ratings yet

- ASE20098 Mark Scheme March 2019Document11 pagesASE20098 Mark Scheme March 2019Ti SodiumNo ratings yet

- Ase20093 01 Results Mark Scheme 220826 June 2022 SeriesDocument17 pagesAse20093 01 Results Mark Scheme 220826 June 2022 SeriesTheint ThiriNo ratings yet

- 4AC1 01 Rms 20190822Document19 pages4AC1 01 Rms 20190822DURAIMURUGAN MIS 17-18 MYP ACCOUNTS STAFFNo ratings yet

- Wac12 2018 May A2 MSDocument28 pagesWac12 2018 May A2 MSYani ChuNo ratings yet

- Mark Scheme (Results) January 2018Document34 pagesMark Scheme (Results) January 2018Samin AhmedNo ratings yet

- 4ac1-02-rms-20220825Document10 pages4ac1-02-rms-20220825attackdfg2002No ratings yet

- ASE20091 June 2021 Mark SchemeDocument16 pagesASE20091 June 2021 Mark SchemeMusthari KhanNo ratings yet

- 9706 Accounting: MARK SCHEME For The May/June 2008 Question PaperDocument5 pages9706 Accounting: MARK SCHEME For The May/June 2008 Question PaperRoukaiya PeerkhanNo ratings yet

- Vyaderm Caseanalysis PDFDocument6 pagesVyaderm Caseanalysis PDFSahil Azher RashidNo ratings yet

- FM. Final Exam (December 2018)Document11 pagesFM. Final Exam (December 2018)elodie Helme GuizonNo ratings yet

- F2 May 2012 Examiners AnswersDocument14 pagesF2 May 2012 Examiners AnswersFahadNo ratings yet

- Wac11 2018 Jan A2 MSDocument31 pagesWac11 2018 Jan A2 MSFatema NawrinNo ratings yet

- MS Paper 2Document10 pagesMS Paper 2Abdul MoizNo ratings yet

- Mark Scheme (Results) : Pearson Edexcel IAL Accounting in Accounting (WAC11) Paper 01 The Accounting System and CostingDocument33 pagesMark Scheme (Results) : Pearson Edexcel IAL Accounting in Accounting (WAC11) Paper 01 The Accounting System and CostingJawad NadeemNo ratings yet

- Mark Scheme: July 2019Document16 pagesMark Scheme: July 2019KoniiNo ratings yet

- Cambridge International AS & A Level: Accounting 9706/22 March 2020Document7 pagesCambridge International AS & A Level: Accounting 9706/22 March 2020Javed MushtaqNo ratings yet

- Pearson LCCI Level 3 Certificate in Accounting (IAS) : Series 2 2013 (ASE3902)Document10 pagesPearson LCCI Level 3 Certificate in Accounting (IAS) : Series 2 2013 (ASE3902)Gloria WanNo ratings yet

- 9706_w20_ms_31Document9 pages9706_w20_ms_31djgq2xn5wmNo ratings yet

- Consolidated financial statements of Pal CorporationDocument5 pagesConsolidated financial statements of Pal CorporationfebbiniaNo ratings yet

- Ial Wac11 Oct19 MSDocument37 pagesIal Wac11 Oct19 MSsoren50% (2)

- WAC11 01 MSC 20200123Document37 pagesWAC11 01 MSC 20200123Sijia TaoNo ratings yet

- B326 TMA 23-24 (Fall) V1Document5 pagesB326 TMA 23-24 (Fall) V1adel.dahbour9733% (3)

- ASE 3902 - IAS - Revised Syllabus - Answers To Specimen Paper 2008 16307Document8 pagesASE 3902 - IAS - Revised Syllabus - Answers To Specimen Paper 2008 16307WinnieOngNo ratings yet

- Mark Scheme (Results) January 2022Document28 pagesMark Scheme (Results) January 2022Fahim AhmedNo ratings yet

- List of Key Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Profitability Ratios and the Other Most Important Financial RatiosFrom EverandList of Key Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Profitability Ratios and the Other Most Important Financial RatiosNo ratings yet

- List of the Most Important Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Key Financial RatiosFrom EverandList of the Most Important Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Key Financial RatiosNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- 螢幕截圖 2023-12-09 下午7.06.53Document52 pages螢幕截圖 2023-12-09 下午7.06.53YAN YAN TSOINo ratings yet

- Httpsdse.lifestaticppgeogchidse2012p1.PDF 18Document26 pagesHttpsdse.lifestaticppgeogchidse2012p1.PDF 18YAN YAN TSOINo ratings yet

- 2023 CTA Exam_Paper 2 Syllabus_May23Document8 pages2023 CTA Exam_Paper 2 Syllabus_May23YAN YAN TSOINo ratings yet

- 螢幕截圖 2024-03-05 下午9.33.07Document72 pages螢幕截圖 2024-03-05 下午9.33.07YAN YAN TSOINo ratings yet

- 螢幕截圖 2024-01-06 下午10.34.57Document17 pages螢幕截圖 2024-01-06 下午10.34.57YAN YAN TSOINo ratings yet

- 螢幕截圖 2024-03-05 下午9.33.07Document72 pages螢幕截圖 2024-03-05 下午9.33.07YAN YAN TSOINo ratings yet

- 螢幕截圖 2023-12-09 下午7.07.00Document52 pages螢幕截圖 2023-12-09 下午7.07.00YAN YAN TSOINo ratings yet

- 螢幕截圖 2023-12-09 下午7.08.28Document52 pages螢幕截圖 2023-12-09 下午7.08.28YAN YAN TSOINo ratings yet

- Economic History: The IndiaDocument231 pagesEconomic History: The IndiaShubhang Shankar SrivastavaNo ratings yet

- Info On Tuition Free Universities in SwedenDocument4 pagesInfo On Tuition Free Universities in SwedencezeomedoNo ratings yet

- Applied Auditing: 3/F F. Facundo Hall, B & E Bldg. Matina, Davao City Philippines Phone No.: (082) 305-0645Document7 pagesApplied Auditing: 3/F F. Facundo Hall, B & E Bldg. Matina, Davao City Philippines Phone No.: (082) 305-0645Bryan PiañarNo ratings yet

- Bond ValuationDocument13 pagesBond Valuationrahul_iiimNo ratings yet

- Nonprofit Organizations Update Summer 2007Document6 pagesNonprofit Organizations Update Summer 2007Arnstein & Lehr LLP100% (1)

- CA Intermediate - Financial Management: Swapnil Patni's ClassesDocument3 pagesCA Intermediate - Financial Management: Swapnil Patni's ClassesAniket PatelNo ratings yet

- Cup - AuditDocument7 pagesCup - AuditJerauld BucolNo ratings yet

- Maths: (Two and A Half Hours)Document6 pagesMaths: (Two and A Half Hours)parthNo ratings yet

- Real World Asset ReportDocument34 pagesReal World Asset ReportTolga BilgiçNo ratings yet

- Costco Strategy WareshousingDocument16 pagesCostco Strategy WareshousingNuri SusantiNo ratings yet

- ASE 3012 Revised Syllabus - Answers To Specimen Paper 2008Document8 pagesASE 3012 Revised Syllabus - Answers To Specimen Paper 2008luckystar2013No ratings yet

- Auditing Theory: Completing The AuditDocument10 pagesAuditing Theory: Completing The AuditAljur SalamedaNo ratings yet

- Managerial Accounting: Solutions ManualDocument58 pagesManagerial Accounting: Solutions ManualЧинболдNo ratings yet

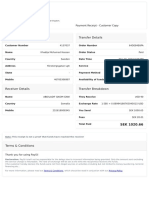

- Sender Details Transfer Details: Payment Receipt - CustomerDocument1 pageSender Details Transfer Details: Payment Receipt - CustomerAbshira Abdi AliNo ratings yet

- Crim Pro SyllabusDocument303 pagesCrim Pro SyllabusAling KinaiNo ratings yet

- MIDTERM EXAM With Answer KeyDocument10 pagesMIDTERM EXAM With Answer KeyDavon JymesNo ratings yet

- Persistent Annual Report 2022Document2 pagesPersistent Annual Report 2022Ashwin GophanNo ratings yet

- CAP Timetable 2016-2017Document2 pagesCAP Timetable 2016-2017Trung NguyenNo ratings yet

- Position and Competency Profile: Job SummaryDocument20 pagesPosition and Competency Profile: Job Summaryjohnrey_lidresNo ratings yet

- Incentive PlansDocument21 pagesIncentive Plansnmhrk1118No ratings yet

- Partnership EssentialsDocument48 pagesPartnership EssentialsMary Pascua Abella100% (1)

- Call Center Business Plan ExampleDocument33 pagesCall Center Business Plan ExamplemeozenemyNo ratings yet

- Value Investing - A Presentation by Prof Sanjay BakshiDocument22 pagesValue Investing - A Presentation by Prof Sanjay BakshisubrataberaNo ratings yet

- Outerwest Recycling Plant 365 04 K W Solar Cell Crowdsale 46de3e4b34Document41 pagesOuterwest Recycling Plant 365 04 K W Solar Cell Crowdsale 46de3e4b34Koya MatsunoNo ratings yet

- RTC Batangas Civil Case Collection MoneyDocument3 pagesRTC Batangas Civil Case Collection MoneyÝel Äcedillo100% (2)

- Accounting recap for sole proprietor and partnership final accountsDocument10 pagesAccounting recap for sole proprietor and partnership final accountsShivamNo ratings yet

- CH 04Document52 pagesCH 04indahmuliasariNo ratings yet

- PTA V Metropolitan Bank and Trust CoDocument1 pagePTA V Metropolitan Bank and Trust CoPerry RubioNo ratings yet

- The Neoliberal State and The Depoliticization of Poverty. Activist Anthropology and Ethnography From Below - Lyon-CalloDocument30 pagesThe Neoliberal State and The Depoliticization of Poverty. Activist Anthropology and Ethnography From Below - Lyon-CalloJozch EstebanNo ratings yet