You might also like

- EIB Working Papers 2019/10 - Structural and cyclical determinants of access to finance: Evidence from EgyptFrom EverandEIB Working Papers 2019/10 - Structural and cyclical determinants of access to finance: Evidence from EgyptNo ratings yet

- Determinants of Non-Performing Loan in Nepalese Commercial BanksDocument17 pagesDeterminants of Non-Performing Loan in Nepalese Commercial Bankskripa poudelNo ratings yet

- EIB Working Papers 2019/07 - What firms don't like about bank loans: New evidence from survey dataFrom EverandEIB Working Papers 2019/07 - What firms don't like about bank loans: New evidence from survey dataNo ratings yet

- Bank capital,Deposits and Size Effects onProfitability of Commercial Banks in Nepal (1) (2)Document74 pagesBank capital,Deposits and Size Effects onProfitability of Commercial Banks in Nepal (1) (2)Rajendra LamsalNo ratings yet

- CREDIT RISK AND COMMERCIAL BANKS' PERFORMANCE IN NIGERIA: A PANEL Model APPROACHDocument8 pagesCREDIT RISK AND COMMERCIAL BANKS' PERFORMANCE IN NIGERIA: A PANEL Model APPROACHdarkniightNo ratings yet

- V18I02A27 DW2G3-29Vlb1y430J62UQDocument12 pagesV18I02A27 DW2G3-29Vlb1y430J62UQZinebNo ratings yet

- Wollo University Final 2014Document26 pagesWollo University Final 2014yonas getachewNo ratings yet

- Risk Components and The Financial PerforDocument8 pagesRisk Components and The Financial PerforRasaq MojeedNo ratings yet

- Published ManuscriptDocument13 pagesPublished ManuscriptmdhsohailNo ratings yet

- Mahmud Rani FriendDocument25 pagesMahmud Rani FriendMOHAMMED ABDULMALIKNo ratings yet

- An Evaluation of Credit Risks Management and PerfoDocument27 pagesAn Evaluation of Credit Risks Management and PerfoOGUNBULE OPEYEMINo ratings yet

- Financial Ratio Model and ApplDocument13 pagesFinancial Ratio Model and ApplDenda Gesva Meisi NoniNo ratings yet

- Effect of Credit Risk Management On Financial Performance of Nepalese Commercial BanksDocument12 pagesEffect of Credit Risk Management On Financial Performance of Nepalese Commercial BanksSonam ShahNo ratings yet

- 1 PBDocument10 pages1 PBNorainun AzwaNo ratings yet

- Influence of Operational and Liquidity Risk on Financial Performance of Microfinance Banks in KenyaDocument12 pagesInfluence of Operational and Liquidity Risk on Financial Performance of Microfinance Banks in KenyaHeru ErlanggaNo ratings yet

- ProposalDocument34 pagesProposalAli JafferyNo ratings yet

- Impact of Non-Performing Loans On Bank's Profitability: Empirical Evidence From Commercial Banks in TanzaniaDocument9 pagesImpact of Non-Performing Loans On Bank's Profitability: Empirical Evidence From Commercial Banks in TanzaniaChương Nguyễn ĐìnhNo ratings yet

- Effects of Credit Risk Management on Financial Performance of Commercial BanksDocument8 pagesEffects of Credit Risk Management on Financial Performance of Commercial BanksGizachewNo ratings yet

- Determinants of Non-Performing Loans in Pakistan: Tanweer@s3h.nust - Edu.pkDocument15 pagesDeterminants of Non-Performing Loans in Pakistan: Tanweer@s3h.nust - Edu.pkChương Nguyễn ĐìnhNo ratings yet

- VietnamDocument49 pagesVietnamShoikot BishwasNo ratings yet

- CccrupDocument15 pagesCccrupIbrahim MuhammadibrahimNo ratings yet

- GRP RevisedDocument11 pagesGRP RevisedAakanshya SharmaNo ratings yet

- Impact The CREDIT RISK of The Credit Operations On The Credit Effectiveness of Commercial Banks A Case of HCMC and Dong Nai Province 1939Document11 pagesImpact The CREDIT RISK of The Credit Operations On The Credit Effectiveness of Commercial Banks A Case of HCMC and Dong Nai Province 1939bien xanh2013No ratings yet

- A Research Report On Cost Efficiency and Credit Management Variables of Banking Industry: A Study On Sunrise Bank and Siddhartha BankDocument16 pagesA Research Report On Cost Efficiency and Credit Management Variables of Banking Industry: A Study On Sunrise Bank and Siddhartha BankBinod thakurNo ratings yet

- FRM Final ProjectDocument5 pagesFRM Final ProjectOkasha AliNo ratings yet

- An Analysis of Loan Portfolio Management On Organization Profitability: Case of Commercial Banks in KenyaDocument13 pagesAn Analysis of Loan Portfolio Management On Organization Profitability: Case of Commercial Banks in Kenyashubham roteNo ratings yet

- SSRN Id2938546Document16 pagesSSRN Id2938546Hesti PermatasariNo ratings yet

- 173 PDFDocument11 pages173 PDFmuhammad bagusNo ratings yet

- Asset Valuation An Its Effect On Financial Statement of Nigeria Deposit Money BankDocument30 pagesAsset Valuation An Its Effect On Financial Statement of Nigeria Deposit Money BankAFOLABI AZEEZ OLUWASEGUN100% (1)

- MR ZulfaDocument14 pagesMR ZulfaHalim Pandu LatifahNo ratings yet

- Corporate Governance and Operational Risk Management of The Listed Deposit Money Banks (DMBS) in Nigeria: Conceptual FrameworkDocument14 pagesCorporate Governance and Operational Risk Management of The Listed Deposit Money Banks (DMBS) in Nigeria: Conceptual Frameworkiaset123No ratings yet

- Chapter One: Introduction: 1.1. Background of The StudyDocument18 pagesChapter One: Introduction: 1.1. Background of The StudyTsegay T GirgirNo ratings yet

- Non Performing Loans Perception of Somali BankersDocument27 pagesNon Performing Loans Perception of Somali BankersIJARP PublicationsNo ratings yet

- Ihtisham Sir PapperDocument17 pagesIhtisham Sir PapperIbrahim MuhammadibrahimNo ratings yet

- 295-306 Vol 3 Issue 5 May 2014Document12 pages295-306 Vol 3 Issue 5 May 2014Anonymous ed8Y8fCxkSNo ratings yet

- Research Journal of Finance and Accounting ISSN 2222-1697 (Paper) ISSN 2222-2847 (Online) DOI: 10.7176/RJFA Vol.10, No.3, 2019Document12 pagesResearch Journal of Finance and Accounting ISSN 2222-1697 (Paper) ISSN 2222-2847 (Online) DOI: 10.7176/RJFA Vol.10, No.3, 2019daniel nugusieNo ratings yet

- MPRA Paper 112482Document24 pagesMPRA Paper 112482Hafiz Muhammad SaleemNo ratings yet

- FR15Document21 pagesFR15Yehia SalehNo ratings yet

- Effect of Risk Management On Banks' Financial Performance: Evidences From Ethiopian Commercial BanksDocument7 pagesEffect of Risk Management On Banks' Financial Performance: Evidences From Ethiopian Commercial BanksIAEME PublicationNo ratings yet

- Relationship Between Credit Risk Management and Financial Performance: Empirical Evidence From Microfinance Banks in KenyaDocument28 pagesRelationship Between Credit Risk Management and Financial Performance: Empirical Evidence From Microfinance Banks in KenyaCatherine AteNo ratings yet

- Ae 75Document9 pagesAe 75BudhaNo ratings yet

- Factors That Affect Profitability of Banks Comparative Study Between Indonesian and Hong KongDocument21 pagesFactors That Affect Profitability of Banks Comparative Study Between Indonesian and Hong Kongroy manchenNo ratings yet

- December 2013 5Document13 pagesDecember 2013 5bedilu77No ratings yet

- Effect of Credit Risk, Liquidity Risk, and Market Risk Banking To Profitability Bank (Study On Devised Banks in Indonesia Stock Exchange)Document8 pagesEffect of Credit Risk, Liquidity Risk, and Market Risk Banking To Profitability Bank (Study On Devised Banks in Indonesia Stock Exchange)miko sondangNo ratings yet

- Published Article 2 June 2016 PDFDocument15 pagesPublished Article 2 June 2016 PDFFredNo ratings yet

- Factors Affecting Deposit Mobilization in Myanmar BanksDocument10 pagesFactors Affecting Deposit Mobilization in Myanmar BanksRocky BhaiNo ratings yet

- Impact of Credit Risk On Profitability ADocument7 pagesImpact of Credit Risk On Profitability ANikeladam JNo ratings yet

- Alshebmi 2020 E R1Document22 pagesAlshebmi 2020 E R1Lorrente LopezNo ratings yet

- Thesis On Credit Risk Management in Commercial Banks of NepalDocument6 pagesThesis On Credit Risk Management in Commercial Banks of Nepalabbyjohnsonmanchester100% (2)

- Assessment of Credit Risk Management System in Ethiopian BankingDocument13 pagesAssessment of Credit Risk Management System in Ethiopian Bankinginventionjournals100% (1)

- Olompyacustartoo PDFDocument20 pagesOlompyacustartoo PDFHenizionNo ratings yet

- Factors Affecting The Net Interest Margin of Commercial Bank of EthiopiaDocument12 pagesFactors Affecting The Net Interest Margin of Commercial Bank of EthiopiaJASH MATHEWNo ratings yet

- Proceedings Banks Efficiency and The Determinans of Non-Performing Financing of Full-Fledged Islamic Banks in IndonesiaDocument13 pagesProceedings Banks Efficiency and The Determinans of Non-Performing Financing of Full-Fledged Islamic Banks in IndonesiaAera Queency ApicomNo ratings yet

- 623-Article Text-2128-2234-10-20190629Document18 pages623-Article Text-2128-2234-10-20190629CorisytNo ratings yet

- Research ProposalDocument2 pagesResearch ProposalFasika JrNo ratings yet

- 01 J Isoss 7 1Document18 pages01 J Isoss 7 1Faiza LiaqatNo ratings yet

- Wa0015.Document4 pagesWa0015.pandeynikhil080No ratings yet

- Credit Risk, Liquidity Risk and Profitability in Nepalese Commercial BanksDocument9 pagesCredit Risk, Liquidity Risk and Profitability in Nepalese Commercial BanksKarim FarjallahNo ratings yet

- Al MagharemDocument15 pagesAl MagharemPham NamNo ratings yet

- Assessment of The Determinants of Non-Performing Loans and Their Effects On Performance of Commercial Banks in KenyaDocument23 pagesAssessment of The Determinants of Non-Performing Loans and Their Effects On Performance of Commercial Banks in KenyaOIRCNo ratings yet

- feasibility4Document3 pagesfeasibility4Zeleke WondimuNo ratings yet

- Course Content-Adv Plant PHYSIOLOGY CONTENT-AGRONOMYDocument4 pagesCourse Content-Adv Plant PHYSIOLOGY CONTENT-AGRONOMYZeleke Wondimu100% (1)

- ConceptualDocument1 pageConceptualZeleke WondimuNo ratings yet

- CommentDocument60 pagesCommentZeleke WondimuNo ratings yet

- Performance A and To Survive in Such A Competitive EnvironmentDocument3 pagesPerformance A and To Survive in Such A Competitive EnvironmentZeleke WondimuNo ratings yet

- Alemayehu Tadesse Third Draft Proposal, Alex3 LastDocument37 pagesAlemayehu Tadesse Third Draft Proposal, Alex3 LastZeleke WondimuNo ratings yet

- Final Corrected - Jony's New FinalDocument36 pagesFinal Corrected - Jony's New FinalZeleke WondimuNo ratings yet

- Gere 2nd Commented ProposalDocument46 pagesGere 2nd Commented ProposalZeleke WondimuNo ratings yet

- Flour Milling Feasibility Template AnalysisDocument26 pagesFlour Milling Feasibility Template AnalysisNijam JabbarNo ratings yet

- Bar Graph Unit MonthDocument2 pagesBar Graph Unit MonthshrikantNo ratings yet

- CFAB Accounting QB Chapter 10 C601Document14 pagesCFAB Accounting QB Chapter 10 C601VânAnh NguyễnNo ratings yet

- Partnership Problems Solved Step-by-StepDocument3 pagesPartnership Problems Solved Step-by-StepKez MaxNo ratings yet

- Mission 200Document80 pagesMission 200HITESH PurohitNo ratings yet

- DS Maltego 20190507aNoCropDocument2 pagesDS Maltego 20190507aNoCropJacob ScottNo ratings yet

- Business ValuationDocument5 pagesBusiness ValuationPulkitAgrawalNo ratings yet

- JM Financial Home - CRISIL - CleanedDocument8 pagesJM Financial Home - CRISIL - CleanedSrinivasNo ratings yet

- AIN2601 Assessment 2 Download S2Document24 pagesAIN2601 Assessment 2 Download S2Makhathini KutlwanoNo ratings yet

- Walter Wurster, Et Al. v. Deloitte Et Al.Document63 pagesWalter Wurster, Et Al. v. Deloitte Et Al.Matthew Kish100% (1)

- Sop For Industrial Land Allotment PDFDocument32 pagesSop For Industrial Land Allotment PDFSurajPandeyNo ratings yet

- Scott Meikle, Aristotle and Exchange ValueDocument26 pagesScott Meikle, Aristotle and Exchange ValueSancrucensisNo ratings yet

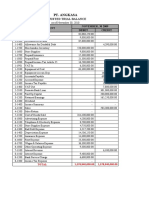

- Kerja Kelompok PT Angkasa BDocument28 pagesKerja Kelompok PT Angkasa BElisa EndrianiiNo ratings yet

- Chapter 3 Financial PlanningDocument25 pagesChapter 3 Financial PlanningChristopher Beltran CauanNo ratings yet

- This Study Resource Was: Problem 1Document2 pagesThis Study Resource Was: Problem 1Michelle J UrbodaNo ratings yet

- Financial System - Introduction ExplainedDocument31 pagesFinancial System - Introduction ExplainedVaidyanathan RavichandranNo ratings yet

- Week 03 - Bank ReconciliationDocument6 pagesWeek 03 - Bank ReconciliationPj ManezNo ratings yet

- CASE STUDY inDocument2 pagesCASE STUDY inNhi YếnNo ratings yet

- Mangalam AR White Kite TransfersDocument7 pagesMangalam AR White Kite TransfersCA Pallavi KNo ratings yet

- Kebs 108Document26 pagesKebs 108Arjun kumar ShresthaNo ratings yet

- 87097-19840-Money MarketDocument8 pages87097-19840-Money MarketVicky HatwalNo ratings yet

- Indore Development Authority v. Shailendra JudgmentDocument198 pagesIndore Development Authority v. Shailendra JudgmentSuyash AgrawalNo ratings yet

- FM PaperDocument3 pagesFM Papermohanraokp2279No ratings yet

- Pro Forma Balance Sheet Template: Company NameDocument5 pagesPro Forma Balance Sheet Template: Company NamePhương ĐinhNo ratings yet

- Extra AfaDocument5 pagesExtra AfaJesmon RajNo ratings yet

- How To Endorse A CheckDocument30 pagesHow To Endorse A Checkfreedompool11391597% (75)

- Chapter 1: Introduction To Digital BankingDocument9 pagesChapter 1: Introduction To Digital BankingPriyanka JNo ratings yet

- Inflation Is The Decline of Purchasing Power of A Given Currency Over TimeDocument2 pagesInflation Is The Decline of Purchasing Power of A Given Currency Over TimeMidz SantayanaNo ratings yet

- Financial ModelingDocument8 pagesFinancial ModelingBishaw Deo MishraNo ratings yet

- Chapter 12 RWJDocument26 pagesChapter 12 RWJKeumalaNo ratings yet