You might also like

- Adim Jati Seva PartyDocument4 pagesAdim Jati Seva Partypankajnirvana_598449No ratings yet

- NF Order ZD330523079501L 20230517040905Document4 pagesNF Order ZD330523079501L 20230517040905Boomi BalanNo ratings yet

- Date Ext TD1427Document1 pageDate Ext TD1427Sweta ChouNo ratings yet

- Style Textile PDFDocument1 pageStyle Textile PDFabdul hananNo ratings yet

- Dot Notice ZD070923053452D 20230926013050Document2 pagesDot Notice ZD070923053452D 20230926013050Himanshu GugnaniNo ratings yet

- Asmt 10 Asian Steels 19-20Document3 pagesAsmt 10 Asian Steels 19-20hakkim satharNo ratings yet

- Flat No.801 Sharad Surendra Gupta-2Document1 pageFlat No.801 Sharad Surendra Gupta-2Sharad GuptaNo ratings yet

- NoteDocument5 pagesNotemyfoot1991No ratings yet

- AA & FS For Maintenance Work Year 202122Document2 pagesAA & FS For Maintenance Work Year 202122ashishNo ratings yet

- GSTR2B 20CHSPM6149M1ZS 032023 10062023Document7 pagesGSTR2B 20CHSPM6149M1ZS 032023 10062023laxmi handloommdpNo ratings yet

- Dot Notice ZD080623051455D 20230615041115Document5 pagesDot Notice ZD080623051455D 20230615041115khushinagar9009No ratings yet

- Exercising of OptionDocument3 pagesExercising of OptionaaosarlbNo ratings yet

- Alert Circular - Dibrugarh C'rteDocument7 pagesAlert Circular - Dibrugarh C'rteIAS MeenaNo ratings yet

- GSTR2BQ 23Z6 032024 24042024Document7 pagesGSTR2BQ 23Z6 032024 24042024Neha JainNo ratings yet

- SNGPL - Web BillDocument2 pagesSNGPL - Web BillMuhammad Irfan100% (1)

- Patanjali Arogya Kendra 2018-19Document5 pagesPatanjali Arogya Kendra 2018-19tuensangnagaland2018No ratings yet

- Faridpur Sugar Mills Ltd. 2019-20Document24 pagesFaridpur Sugar Mills Ltd. 2019-20Prosad DharNo ratings yet

- 12 PDFDocument2 pages12 PDFNarayana rao dubaNo ratings yet

- Nation: MarketDocument9 pagesNation: MarketDebashis MitraNo ratings yet

- Sri Chowdeshwari Rice TradersDocument2 pagesSri Chowdeshwari Rice Tradershemanth1234No ratings yet

- Dot Notice Zd180124031595i 20240120035605Document2 pagesDot Notice Zd180124031595i 20240120035605tuensangnagaland2018No ratings yet

- SNGPL - Web BillDocument1 pageSNGPL - Web BillMaazAliYousufNo ratings yet

- SNGPL - Web Bill PDFDocument1 pageSNGPL - Web Bill PDFSheran Shahid0% (1)

- Sri ByraveshwaraDocument3 pagesSri Byraveshwarahemanth1234No ratings yet

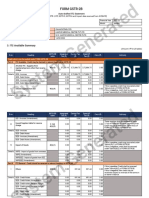

- Form Gstr-2B: 3. ITC Available SummaryDocument7 pagesForm Gstr-2B: 3. ITC Available SummaryRohit GoyalNo ratings yet

- Form Gstr-2B: 3. ITC Available SummaryDocument7 pagesForm Gstr-2B: 3. ITC Available SummaryRohit GoyalNo ratings yet

- Secured Advance Measurement Sheet of II ND RA BILLDocument2 pagesSecured Advance Measurement Sheet of II ND RA BILLVikas VivenNo ratings yet

- In LN: ThreeDocument48 pagesIn LN: ThreeS UDAY KUMARNo ratings yet

- RectificationOrder ZD080124036008R 20240112013906Document7 pagesRectificationOrder ZD080124036008R 20240112013906Ram kunwar KumawatNo ratings yet

- Haritha Hotel SiddipetDocument1 pageHaritha Hotel SiddipetAditya SharmaNo ratings yet

- Dot Notice ZD2409230503986 20230929011717Document2 pagesDot Notice ZD2409230503986 20230929011717Ashish MehtaNo ratings yet

- GSTR2B 06alzps2257h2zf 032022 24092022Document7 pagesGSTR2B 06alzps2257h2zf 032022 24092022Robin JoseNo ratings yet

- HERITAGEDocument2 pagesHERITAGEhemanth1234No ratings yet

- Form Gstr-2B: 3. ITC Available SummaryDocument7 pagesForm Gstr-2B: 3. ITC Available SummaryRohit GoyalNo ratings yet

- GSTR2B 06alzps2257h2zf 072022 24092022Document7 pagesGSTR2B 06alzps2257h2zf 072022 24092022Robin JoseNo ratings yet

- Cellsons Appeal StatementDocument45 pagesCellsons Appeal Statementjenniferthanu1521No ratings yet

- Multan: Muhammad Waseem House No 144 Model TownDocument1 pageMultan: Muhammad Waseem House No 144 Model TownMadina Madina 1.0No ratings yet

- Form GST ASMT - 11 - NNNNNDocument2 pagesForm GST ASMT - 11 - NNNNNGovindNo ratings yet

- SNGPL - Web BillDocument1 pageSNGPL - Web BillOwais KhanNo ratings yet

- Cmlertrt3Y: /3ofto/o G7-Ig/2022-23Document22 pagesCmlertrt3Y: /3ofto/o G7-Ig/2022-23R-TECH ComputersNo ratings yet

- Ram NameDocument2 pagesRam NameStock PsychologistNo ratings yet

- Hotel Bill 9975Document1 pageHotel Bill 9975Gautam GuptaNo ratings yet

- Form Gstr-2B: 3. ITC Available SummaryDocument7 pagesForm Gstr-2B: 3. ITC Available SummaryRohit GoyalNo ratings yet

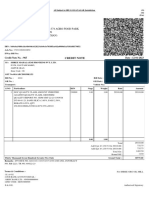

- CPC-TRD-Gurgaon-HY 1467, Sector-4, Urban Estate Gurgaon, HR: Tax InvoiceDocument3 pagesCPC-TRD-Gurgaon-HY 1467, Sector-4, Urban Estate Gurgaon, HR: Tax InvoiceMann BhandariNo ratings yet

- Credit Note Quality Rebate rb-2223 TR No 016Document1 pageCredit Note Quality Rebate rb-2223 TR No 016Kapil sharmaNo ratings yet

- Deppak Traders Rustplene BillDocument2 pagesDeppak Traders Rustplene BillAntarnad VishwarupNo ratings yet

- Form 1619042024 085917Document3 pagesForm 1619042024 085917SODHI SINGHNo ratings yet

- Final Bill & Its EnclosuresDocument17 pagesFinal Bill & Its EnclosuresmanikandanNo ratings yet

- DRC07 Order ZD181223066048F 20231231023238Document4 pagesDRC07 Order ZD181223066048F 20231231023238tuensangnagaland2018No ratings yet

- EY-Sales Report - June 1st Fortnight 2022Document1 pageEY-Sales Report - June 1st Fortnight 2022Sanjida KamalNo ratings yet

- GST Pass Order PDFDocument4 pagesGST Pass Order PDFvenkat dNo ratings yet

- Notfctn 79 Central Tax English 2020Document19 pagesNotfctn 79 Central Tax English 2020Shaik MastanvaliNo ratings yet

- DRC01C PartA 09FZMPP1720E2Z8 092023Document2 pagesDRC01C PartA 09FZMPP1720E2Z8 092023ANISH SHAIKHNo ratings yet

- LOC Proposal 2nd QTR DT 6 7 2022Document2 pagesLOC Proposal 2nd QTR DT 6 7 2022pintu sainiNo ratings yet

- Signed Do MSTC TVC 22-23-2237Document2 pagesSigned Do MSTC TVC 22-23-2237Tajamul PashaNo ratings yet

- Do MSTC JPR 23-24 2049Document2 pagesDo MSTC JPR 23-24 2049vikas agrawalNo ratings yet

- GSTR2B 06alzps2257h2zf 112020 24092022Document7 pagesGSTR2B 06alzps2257h2zf 112020 24092022Robin JoseNo ratings yet

- Sri Vasavi Medical Agencies Invoice Rpaug002Document1 pageSri Vasavi Medical Agencies Invoice Rpaug002amareshNo ratings yet

- Shyama Health Care &fitness Solution: Ret No.018 13636203Document1 pageShyama Health Care &fitness Solution: Ret No.018 13636203Wjajshs UshdNo ratings yet

- WHI Research Note-20240131Document21 pagesWHI Research Note-20240131Vincent OngNo ratings yet

- Classification of AccountsDocument4 pagesClassification of Accountsvikas sunnyNo ratings yet

- The Commerce Villa: Time: 3 Hours Mock Test (EC - 10) Marks: 80 Section A (Macro Economics)Document15 pagesThe Commerce Villa: Time: 3 Hours Mock Test (EC - 10) Marks: 80 Section A (Macro Economics)Shreyas PremiumNo ratings yet

- Addendum1 Acl Patrimonial Capital 3b FFDocument7 pagesAddendum1 Acl Patrimonial Capital 3b FFOriannys de CardenasNo ratings yet

- Wells Fargo Business Bank Statement PDFDocument4 pagesWells Fargo Business Bank Statement PDFquannbui9577% (13)

- Invest IndiaDocument1 pageInvest IndiaAmandeepNo ratings yet

- Business Banking: You and Wells FargoDocument4 pagesBusiness Banking: You and Wells Fargobilly barker white50% (2)

- Top 10 Reasons Why Maintenance Planning Is Not EffectiveDocument7 pagesTop 10 Reasons Why Maintenance Planning Is Not Effectivemenz502No ratings yet

- Airtel Black Bill 3Document8 pagesAirtel Black Bill 3Akshay KharolaNo ratings yet

- b3 17 Traits of Wealth Titans Special Report EbookDocument38 pagesb3 17 Traits of Wealth Titans Special Report EbookAdolfo NoronhaNo ratings yet

- CHAPTER 6-Suppply Chain DriversDocument32 pagesCHAPTER 6-Suppply Chain DriversRonit TandukarNo ratings yet

- Postpaid TN CDocument67 pagesPostpaid TN CHimanshu MahorNo ratings yet

- A Splendid Exchange - Wilkiam BernteinDocument17 pagesA Splendid Exchange - Wilkiam BernteinMasood ThaheemNo ratings yet

- Mycbseguide: Class 12 - Accountancy Sample Paper 07Document15 pagesMycbseguide: Class 12 - Accountancy Sample Paper 07sneha muralidharanNo ratings yet

- Elasticity: Chapter OutlineDocument37 pagesElasticity: Chapter OutlineLatifah NurhalizaNo ratings yet

- 11 Value4HerEthiopiaDocument3 pages11 Value4HerEthiopiabizuayehu admasuNo ratings yet

- Regulatory Framework of Mutual FundsDocument24 pagesRegulatory Framework of Mutual FundsLovepreet NegiNo ratings yet

- Walmart-Flipkart: A Deal Worth Its Price?Document4 pagesWalmart-Flipkart: A Deal Worth Its Price?AkashNo ratings yet

- Revista Dry Cargo 2205Document136 pagesRevista Dry Cargo 2205Alexsandro MachadoNo ratings yet

- AACT 2173 FM Lesson 4 Tutorial (Additional)Document11 pagesAACT 2173 FM Lesson 4 Tutorial (Additional)Ashvin Kaur100% (1)

- OnGrid - Trust Platform of IndiaDocument6 pagesOnGrid - Trust Platform of IndiaRaghavendra Vishwas KNo ratings yet

- Freight Forwarder Foreign Contact InformationDocument11 pagesFreight Forwarder Foreign Contact InformationBenhurNo ratings yet

- Dow Theory - From Bear Markets T - Michael YoungDocument25 pagesDow Theory - From Bear Markets T - Michael YoungYigermal FantayeNo ratings yet

- Excel FinanceDocument28 pagesExcel FinanceabdullahNo ratings yet

- 7 CPA FINANCIAL REPORTING Paper 7Document13 pages7 CPA FINANCIAL REPORTING Paper 7dennis greenNo ratings yet

- Elasticity: Q Q Q P P PDocument5 pagesElasticity: Q Q Q P P PsamioNo ratings yet

- Balance Sheet: 07 - Standalone Financial - 28-06-2019.indd 206 7/5/2019 6:36:18 PMDocument1 pageBalance Sheet: 07 - Standalone Financial - 28-06-2019.indd 206 7/5/2019 6:36:18 PMharshit abrolNo ratings yet

- 22private Sect PowerDocument14 pages22private Sect PowerSanjana KoliNo ratings yet

- Brics: Nikhil K Gowda Psir Notes Brics 2022Document10 pagesBrics: Nikhil K Gowda Psir Notes Brics 2022Avijith ChandramouliNo ratings yet

- Disruptive Innovation, Business Models, and Encroachment StrategiesDocument13 pagesDisruptive Innovation, Business Models, and Encroachment StrategiesLavanya SubramaniamNo ratings yet