You might also like

- Fritz Springmeier InterviewDocument59 pagesFritz Springmeier InterviewCzink Tiberiu100% (4)

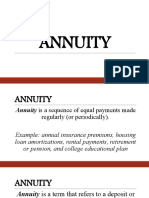

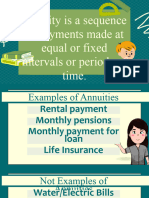

- AnnuityDocument46 pagesAnnuityJeffreyMitra100% (2)

- Module 7. Annuities: 1. Simple AnnuityDocument19 pagesModule 7. Annuities: 1. Simple AnnuityMori OugaiNo ratings yet

- Value Investors Club - Treasure ASA (TRE ASA)Document9 pagesValue Investors Club - Treasure ASA (TRE ASA)Lukas Savickas100% (1)

- Gen Math Q2 - Week 3 - Simple AnnuityDocument23 pagesGen Math Q2 - Week 3 - Simple AnnuityFrancisco, Ashley Dominique V.No ratings yet

- GENMATH - Simple and General AnnuitiesDocument2 pagesGENMATH - Simple and General AnnuitiesBern Balingit-Arnaiz100% (5)

- CBLM Bartending Ncii # 1 & 4aDocument265 pagesCBLM Bartending Ncii # 1 & 4aQueenly Mendoza Aguilar81% (21)

- General Mathematics: Quarter 2 - Module 7 AnnuitiesDocument40 pagesGeneral Mathematics: Quarter 2 - Module 7 AnnuitiesBreanna CIel E. Cabahit100% (1)

- GENMATH - Business and Consumer LoansDocument1 pageGENMATH - Business and Consumer LoansBern Balingit-ArnaizNo ratings yet

- Image Steganography ScopeDocument13 pagesImage Steganography ScopeMUHAMMAD FARAZ HAIDERNo ratings yet

- Nanotechnology in Civil EngineeringDocument22 pagesNanotechnology in Civil EngineeringNehad AhmedNo ratings yet

- Grade-9 (1st)Document42 pagesGrade-9 (1st)Jen Ina Lora-Velasco GacutanNo ratings yet

- Time ValueDocument6 pagesTime Valuechris david100% (1)

- AnnuitiesDocument12 pagesAnnuitiesNapoleon ChiongNo ratings yet

- Gen Math PPT - KaeDocument29 pagesGen Math PPT - KaeKayezel BanasigNo ratings yet

- Simple AnnuityDocument2 pagesSimple AnnuityArden AnagapNo ratings yet

- Annuities Part 1 FinalDocument28 pagesAnnuities Part 1 FinalENGLAND DE ASIS ESCLAMADONo ratings yet

- Annuity - Introduction Ordinary AnnuityDocument24 pagesAnnuity - Introduction Ordinary AnnuityThomasaquinos msigala JrNo ratings yet

- Simple Annuities PDFDocument6 pagesSimple Annuities PDFNhel AlvaroNo ratings yet

- Module 7-8-AnnuityDocument19 pagesModule 7-8-AnnuityI am AngelllNo ratings yet

- Effective and Nominal Interest Rates: (A) What Annual Interest Rate Did You Earn If Interest Is Compounded Yearly?Document6 pagesEffective and Nominal Interest Rates: (A) What Annual Interest Rate Did You Earn If Interest Is Compounded Yearly?Owene Miles AguinaldoNo ratings yet

- Simple AnnuityDocument22 pagesSimple AnnuityAshley AniganNo ratings yet

- Section 1.9.1 Annuity-ImmediateDocument15 pagesSection 1.9.1 Annuity-ImmediateMary Dianneil MandinNo ratings yet

- Interest and Money Time Relationship 1Document45 pagesInterest and Money Time Relationship 1john jkillerzsNo ratings yet

- Math 101 Simple AnnuityDocument30 pagesMath 101 Simple AnnuityAdi Garcia ArcenasNo ratings yet

- Module 12 - Simple AnnuityDocument41 pagesModule 12 - Simple AnnuityColleen Mae San DiegoNo ratings yet

- Chapter 6 AnnuityDocument35 pagesChapter 6 AnnuityfatinNo ratings yet

- Examples of Bank SavingsDocument6 pagesExamples of Bank SavingsjaneNo ratings yet

- BCom (H) - IIyear - 4.2 - Business - Maths - Week2 - (MOF) AshaRaniDocument33 pagesBCom (H) - IIyear - 4.2 - Business - Maths - Week2 - (MOF) AshaRaniMai LenNo ratings yet

- OrdinaryAnnuity Part 1Document20 pagesOrdinaryAnnuity Part 1Kim TNo ratings yet

- MA170 Chapter 4 & 5Document15 pagesMA170 Chapter 4 & 5ishanissantaNo ratings yet

- ORDINARY ANNUITY - Future and Present ValueDocument33 pagesORDINARY ANNUITY - Future and Present ValueSALIM SHARIFUNo ratings yet

- Unit 4 - AnnuityDocument5 pagesUnit 4 - AnnuityShashank HundiaNo ratings yet

- GenMath 8Document8 pagesGenMath 8ChristoneNo ratings yet

- Annuity Cash Flow Diagram Economic EquivalenceDocument76 pagesAnnuity Cash Flow Diagram Economic EquivalenceDarkie DrakieNo ratings yet

- Time Value of Money Part IIIDocument4 pagesTime Value of Money Part IIINailiah MacakilingNo ratings yet

- SSLM in General Mathematics For G11 Q2 Module 3Document6 pagesSSLM in General Mathematics For G11 Q2 Module 3Darren JuneNo ratings yet

- Chapter-4 AnnuityDocument10 pagesChapter-4 AnnuityThea De guzmanNo ratings yet

- 06 - Slide Time Value of Money #2 ShareDocument43 pages06 - Slide Time Value of Money #2 ShareyuditoktanelNo ratings yet

- CH 2 Time Value of MoneyDocument15 pagesCH 2 Time Value of MoneyNikita AggarwalNo ratings yet

- Lecture9 - ES301 Engineering EconomicsDocument19 pagesLecture9 - ES301 Engineering EconomicsLory Liza Bulay-ogNo ratings yet

- Day 3 Ordinary AnnuityDocument16 pagesDay 3 Ordinary AnnuityHAYLIE ANGELICA ALBERTONo ratings yet

- Amortization (Math of Investment)Document55 pagesAmortization (Math of Investment)Eubert Arl MoradaNo ratings yet

- Chapter03 Time Value of MoneyDocument15 pagesChapter03 Time Value of MoneyJahirul Islam ShovonNo ratings yet

- Hand Out PPT For INSET DemoDocument14 pagesHand Out PPT For INSET DemoJeseryl VillosoNo ratings yet

- DivD 4731 DikshaJain Assignment1Document9 pagesDivD 4731 DikshaJain Assignment1Diksha JainNo ratings yet

- Simple AnnuityDocument12 pagesSimple Annuityprincessnylighte13No ratings yet

- Define The Types of Annuities Overdue, Early, Differed, Undefined, Perpetual, General.Document19 pagesDefine The Types of Annuities Overdue, Early, Differed, Undefined, Perpetual, General.Fernando CooperNo ratings yet

- General Mathematics 2nd Quarter Week 3 TERESA A. TACIS NHC HS NewDocument11 pagesGeneral Mathematics 2nd Quarter Week 3 TERESA A. TACIS NHC HS NewjohnNo ratings yet

- Engineering EconomyDocument33 pagesEngineering EconomyDaniel Tanus MararangNo ratings yet

- AnnuityDocument1 pageAnnuityEzequiel Posadas BocacaoNo ratings yet

- Chapter 5 - AnnuitiesDocument13 pagesChapter 5 - AnnuitiesEthan ChristiansNo ratings yet

- 4SOGS RM Lecture 4 - Time Value of Money (Part III)Document21 pages4SOGS RM Lecture 4 - Time Value of Money (Part III)Right Karl-Maccoy HattohNo ratings yet

- Examples of Bank SavingsDocument2 pagesExamples of Bank SavingsAnonymous swEjW5ncYNo ratings yet

- Financial MathematicsDocument20 pagesFinancial MathematicsabdullahiismailisaNo ratings yet

- 3.2 AnnuitiesDocument6 pages3.2 AnnuitiesAngela 18 PhotosNo ratings yet

- Module 5 - Es 125Document2 pagesModule 5 - Es 125Rolly Mar ArandingNo ratings yet

- SarahDocument17 pagesSarahkiaNo ratings yet

- Module 5 - Es 125Document2 pagesModule 5 - Es 125AzhelNo ratings yet

- Module 2 AnnuityDocument38 pagesModule 2 AnnuityOwel CabugawanNo ratings yet

- Annuity ProblemDocument8 pagesAnnuity ProblemPamela McmahonNo ratings yet

- Fidelia Agatha - 2106715765 - Summary & Problem MK - Pertemuan Ke-4Document12 pagesFidelia Agatha - 2106715765 - Summary & Problem MK - Pertemuan Ke-4Fidelia AgathaNo ratings yet

- Las q2w3-4Document5 pagesLas q2w3-4Mark Anthony Bell BacangNo ratings yet

- Time Value of MoneyDocument8 pagesTime Value of MoneyShiv Deep Sharma 20mmb087No ratings yet

- Unit Circle IAKTDocument5 pagesUnit Circle IAKTAnthony KhooNo ratings yet

- Grade 11 Reco ScriptDocument2 pagesGrade 11 Reco ScriptCecill Nicanor LabininayNo ratings yet

- Latihan Soal Dan Evaluasi Materi ComplimentDocument6 pagesLatihan Soal Dan Evaluasi Materi ComplimentAvildaAfrinAmmaraNo ratings yet

- Surfactants and Emulsifying Agents: January 2009Document7 pagesSurfactants and Emulsifying Agents: January 2009Jocc Dee LightNo ratings yet

- Organ TransplantationDocument36 pagesOrgan TransplantationAnonymous 4TUSi0SqNo ratings yet

- Bernardo Carpio - Mark Bryan NatontonDocument18 pagesBernardo Carpio - Mark Bryan NatontonMark Bryan NatontonNo ratings yet

- Current Logk VkbaDocument8 pagesCurrent Logk Vkba21muhammad ilham thabariNo ratings yet

- PSV Circular 29 of 2023Document422 pagesPSV Circular 29 of 2023Bee MashigoNo ratings yet

- NPJH50465Document3 pagesNPJH50465Samuel PerezNo ratings yet

- E Id - Like - To - BeDocument9 pagesE Id - Like - To - BeNatalia IlhanNo ratings yet

- Johannes KepplerDocument2 pagesJohannes KepplermakNo ratings yet

- Preparation and Practice Answer KeyDocument16 pagesPreparation and Practice Answer KeyHiệp Nguyễn TuấnNo ratings yet

- CW-80 ManualDocument12 pagesCW-80 ManualBrian YostNo ratings yet

- Loan Modifications - Workout Plans and ModificationDocument43 pagesLoan Modifications - Workout Plans and ModificationSudershan ThaibaNo ratings yet

- Chapter 9 Formulation of National Trade Policies: International Business, 8e (Griffin/Pustay)Document28 pagesChapter 9 Formulation of National Trade Policies: International Business, 8e (Griffin/Pustay)Yomi BrainNo ratings yet

- 3.6-6kva Battery Cabinet: 1600Xp/1600Xpi SeriesDocument22 pages3.6-6kva Battery Cabinet: 1600Xp/1600Xpi SeriesIsraelNo ratings yet

- Technical Support Questions and Answers: How Do I Access Commseciress?Document3 pagesTechnical Support Questions and Answers: How Do I Access Commseciress?goviperumal_33237245No ratings yet

- Your Best American GirlDocument9 pagesYour Best American GirlCrystaelechanNo ratings yet

- Homework Organization ChartDocument5 pagesHomework Organization Chartafetbsaez100% (1)

- Bacc Form 02Document2 pagesBacc Form 02Jeanpaul PorrasNo ratings yet

- Comp2-Cause-Effect EssayDocument4 pagesComp2-Cause-Effect Essayapi-316060728No ratings yet

- Laws Releated To Honour KillingDocument2 pagesLaws Releated To Honour KillingMukul Singh RathoreNo ratings yet

- Book Review - 1: Reviewer: Devajyoti BiswasDocument3 pagesBook Review - 1: Reviewer: Devajyoti BiswassaemoonNo ratings yet

- SSLD Stairways LowresDocument44 pagesSSLD Stairways LowresboyNo ratings yet