You might also like

- Strengthening the Operational Pillar: The Building Blocks of World-Class Production Planning and Inventory Control SystemsFrom EverandStrengthening the Operational Pillar: The Building Blocks of World-Class Production Planning and Inventory Control SystemsNo ratings yet

- SCM Inventory PlanningDocument1 pageSCM Inventory PlanningsyedtalhamanzarNo ratings yet

- Improve inventory accuracy with automated toolsDocument7 pagesImprove inventory accuracy with automated toolsAndrea UyNo ratings yet

- Supply Chain and Procurement Quick Reference: How to navigate and be successful in structured organizationsFrom EverandSupply Chain and Procurement Quick Reference: How to navigate and be successful in structured organizationsNo ratings yet

- LR, Report, SynDocument49 pagesLR, Report, Synvijay_gautam33No ratings yet

- Supply Chain Business Startup Guide: Step-by-Step Tips for SuccessFrom EverandSupply Chain Business Startup Guide: Step-by-Step Tips for SuccessNo ratings yet

- Theoretical FrameworkDocument6 pagesTheoretical Frameworkassyla rukkNo ratings yet

- Better Inventory Management: Big Challenges, Big Data, Emerging SolutionsDocument10 pagesBetter Inventory Management: Big Challenges, Big Data, Emerging SolutionsFattabiouniNo ratings yet

- What is inventoryDocument10 pagesWhat is inventoryrokhankhogyani313No ratings yet

- Wollo University: Lennox Wholesaler Group (Document16 pagesWollo University: Lennox Wholesaler Group (malede gashawNo ratings yet

- Sage ERP Better Inventory Management WPDocument10 pagesSage ERP Better Inventory Management WPMohit AssudaniNo ratings yet

- Inventory Management System ProjectDocument27 pagesInventory Management System Projectaayanshaikh775No ratings yet

- Inventory Control Management TecumsehDocument77 pagesInventory Control Management TecumsehRajesh BathulaNo ratings yet

- Inventory p1Document5 pagesInventory p1Rüel DellovaNo ratings yet

- End Term OF Strategic Cost Management: AssignmentDocument13 pagesEnd Term OF Strategic Cost Management: AssignmentRajshree soniNo ratings yet

- LOGISTIC PLANNINGDocument7 pagesLOGISTIC PLANNINGHarshit AgrawalNo ratings yet

- Inventory Planning and Control TechniquesDocument3 pagesInventory Planning and Control TechniquesJohn Paul Palomino AndradeNo ratings yet

- 5.4 Inventory MagtDocument48 pages5.4 Inventory Magtbha_goNo ratings yet

- Inventory Management: Definition, Types, Process, Importance, ChallengesDocument10 pagesInventory Management: Definition, Types, Process, Importance, ChallengesAarti RaneNo ratings yet

- Inventory Management and JIT Group AssignmentDocument24 pagesInventory Management and JIT Group AssignmenthuleNo ratings yet

- The Importance and Role of Inventory Management and Warehousing in The Performance of ZaraDocument15 pagesThe Importance and Role of Inventory Management and Warehousing in The Performance of Zaraayalmn09No ratings yet

- A Synopsis On Inventory Management SystemDocument9 pagesA Synopsis On Inventory Management Systemshaikh parwezNo ratings yet

- Quantitative Techniques For Business DecisionsDocument8 pagesQuantitative Techniques For Business DecisionsSourav MandalNo ratings yet

- 001Document8 pages001Anna Jane CatubagNo ratings yet

- What Is Inventory Management Process? Flow ExplainedDocument9 pagesWhat Is Inventory Management Process? Flow ExplainedTarun VBRSITNo ratings yet

- Inventory Management Definitions and ConceptsDocument7 pagesInventory Management Definitions and ConceptsKãrtïKêyRåthõdNo ratings yet

- Varuna's vision to provide total water solutions and contribute to societyDocument5 pagesVaruna's vision to provide total water solutions and contribute to societyVikrant KansaraNo ratings yet

- Clothes MBA Mini ProjectDocument31 pagesClothes MBA Mini Projectavadhesh kumarNo ratings yet

- Ritik Synopsis PDFDocument10 pagesRitik Synopsis PDFVaibhav TanejaNo ratings yet

- Planning and Inventory ManagementDocument3 pagesPlanning and Inventory ManagementKarthikNo ratings yet

- Inventory Management: Inventory Management Must Be Designed To Meet The Dictates of MarketDocument17 pagesInventory Management: Inventory Management Must Be Designed To Meet The Dictates of MarketHumaira FathimaNo ratings yet

- LM Imp TopicsDocument17 pagesLM Imp TopicsPallavi SinhaNo ratings yet

- Inventory ManagementDocument24 pagesInventory ManagementBhanushekhar YadavNo ratings yet

- Inventory ManagementDocument23 pagesInventory ManagementChanchal GuptaNo ratings yet

- lacson_025452Document8 pageslacson_025452mickaellacson5No ratings yet

- INVENTORY MANAGEMENTDocument14 pagesINVENTORY MANAGEMENTTina VargheseNo ratings yet

- Westside Inventory Replenishment Model AnalysisDocument32 pagesWestside Inventory Replenishment Model AnalysisManvi Taneja100% (2)

- Assignment-2 Spare Part Inventory Management For A Manufacturing CompanyDocument5 pagesAssignment-2 Spare Part Inventory Management For A Manufacturing Companyparth limbachiyaNo ratings yet

- How effective warehouse management improves supply chain performanceDocument2 pagesHow effective warehouse management improves supply chain performanceAsad MahmoodNo ratings yet

- KANHADocument40 pagesKANHAdebasis tripathyNo ratings yet

- Inventory Final 97-03Document62 pagesInventory Final 97-03navneet9702No ratings yet

- Literature ReviewDocument14 pagesLiterature Reviewniftiangautam70% (2)

- Mgt5013w3ar 22071Document5 pagesMgt5013w3ar 22071NarasimhaBadriNo ratings yet

- Understanding Manufacturing Costs and Inventory ManagementDocument5 pagesUnderstanding Manufacturing Costs and Inventory ManagementJo GreedyNo ratings yet

- Ijrpr2914 A Study of Inventory Management TechniqueDocument3 pagesIjrpr2914 A Study of Inventory Management TechniqueStatus LoverNo ratings yet

- Inventory Management System ProjectDocument3 pagesInventory Management System ProjectKaviya SNo ratings yet

- SCMDocument16 pagesSCMArjun KRNo ratings yet

- Bahao MSDocument1 pageBahao MSMichaela BahaoNo ratings yet

- Material and Store Management:: Introduction, Objectives and FunctionsDocument21 pagesMaterial and Store Management:: Introduction, Objectives and FunctionsStephane chisebweNo ratings yet

- Philippine Christian University: 1648 Taft Avenue Corner Pedro Gil ST., ManilaDocument5 pagesPhilippine Christian University: 1648 Taft Avenue Corner Pedro Gil ST., ManilaKatrizia FauniNo ratings yet

- Role of Inventory Management and Control in A Manufacturing CompanyDocument8 pagesRole of Inventory Management and Control in A Manufacturing CompanyIJRASETPublicationsNo ratings yet

- What Is Inventory ManagementDocument9 pagesWhat Is Inventory ManagementmartgetaliaNo ratings yet

- Material ManagmentDocument6 pagesMaterial ManagmentParamesh PalanichamyNo ratings yet

- The Importance of Successful Inventory Management To Enterprises-A CaseDocument4 pagesThe Importance of Successful Inventory Management To Enterprises-A CaseAmit SahaNo ratings yet

- System? Definition of Inventory Management Systems, Benefits, Best Practices & MoreDocument23 pagesSystem? Definition of Inventory Management Systems, Benefits, Best Practices & Moregetasew altasebNo ratings yet

- Ba 506 Operations ManagementDocument8 pagesBa 506 Operations ManagementRuth Ann DimalaluanNo ratings yet

- Procurement strategies in the hotel industryDocument10 pagesProcurement strategies in the hotel industryVisnu ManimaranNo ratings yet

- SCM U-3Document6 pagesSCM U-3MOHAMMAD ZUBERNo ratings yet

- Introduction To Inventory ManagementDocument4 pagesIntroduction To Inventory ManagementKeerthiga MageshkumarNo ratings yet

- The Tools of Management ScienceDocument3 pagesThe Tools of Management ScienceSuhailShaikhNo ratings yet

- The Role of An Industrial EngineerDocument2 pagesThe Role of An Industrial EngineerSuhailShaikhNo ratings yet

- Applications of Industrial EngineeringDocument1 pageApplications of Industrial EngineeringSuhailShaikhNo ratings yet

- The Concept of Industrial Engineering Enhancing Efficiency and ProductivityDocument2 pagesThe Concept of Industrial Engineering Enhancing Efficiency and ProductivitySuhailShaikhNo ratings yet

- The Role of An Industrial EngineerDocument2 pagesThe Role of An Industrial EngineerSuhailShaikhNo ratings yet

- History and Development of Industrial EngineeringDocument2 pagesHistory and Development of Industrial EngineeringSuhailShaikhNo ratings yet

- Management Science Its Historical DevelopmentDocument3 pagesManagement Science Its Historical DevelopmentSuhailShaikhNo ratings yet

- Applications of Industrial EngineeringDocument1 pageApplications of Industrial EngineeringSuhailShaikhNo ratings yet

- History and Development of Industrial EngineeringDocument2 pagesHistory and Development of Industrial EngineeringSuhailShaikhNo ratings yet

- Production Management The Key To Efficient ManufacturingDocument2 pagesProduction Management The Key To Efficient ManufacturingSuhailShaikhNo ratings yet

- Production Management The Key To Efficient ManufacturingDocument2 pagesProduction Management The Key To Efficient ManufacturingSuhailShaikhNo ratings yet

- Applications of Industrial EngineeringDocument1 pageApplications of Industrial EngineeringSuhailShaikhNo ratings yet

- The Concept of Industrial Engineering Enhancing Efficiency and ProductivityDocument2 pagesThe Concept of Industrial Engineering Enhancing Efficiency and ProductivitySuhailShaikhNo ratings yet

- The Role of An Industrial EngineerDocument2 pagesThe Role of An Industrial EngineerSuhailShaikhNo ratings yet

- The Role of An Industrial EngineerDocument2 pagesThe Role of An Industrial EngineerSuhailShaikhNo ratings yet

- The Concept of Industrial Engineering Enhancing Efficiency and ProductivityDocument2 pagesThe Concept of Industrial Engineering Enhancing Efficiency and ProductivitySuhailShaikhNo ratings yet

- Production and Productivity Driving Forces of Economic GrowthDocument2 pagesProduction and Productivity Driving Forces of Economic GrowthSuhailShaikhNo ratings yet

- Welcome: A Guide To Accessibility ofDocument18 pagesWelcome: A Guide To Accessibility ofSuhailShaikhNo ratings yet

- 7 Steps To Start Goat Farming Business For ProfitDocument8 pages7 Steps To Start Goat Farming Business For ProfitSuhailShaikhNo ratings yet

- Personnel Management Nurturing Human Capital For Organizational SuccessDocument2 pagesPersonnel Management Nurturing Human Capital For Organizational SuccessSuhailShaikhNo ratings yet

- History and Development of Industrial EngineeringDocument2 pagesHistory and Development of Industrial EngineeringSuhailShaikhNo ratings yet

- Online Restaurant Delivery Guide To Getting Started: Will You Deliver Yourself?Document1 pageOnline Restaurant Delivery Guide To Getting Started: Will You Deliver Yourself?SuhailShaikhNo ratings yet

- The Art and Science of Decision-MakingDocument2 pagesThe Art and Science of Decision-MakingSuhailShaikhNo ratings yet

- Aina - e - Qismat October 2019Document60 pagesAina - e - Qismat October 2019SuhailShaikhNo ratings yet

- Favoritism in The Workplace and Its Effect On The OrganizationDocument11 pagesFavoritism in The Workplace and Its Effect On The OrganizationSuhailShaikhNo ratings yet

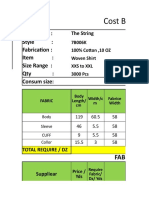

- Costing Sheet For Woven ShirtDocument9 pagesCosting Sheet For Woven ShirtSuhailShaikhNo ratings yet

- National HealthDocument60 pagesNational HealthSuhailShaikhNo ratings yet

- Welcome: A Guide To Accessibility ofDocument18 pagesWelcome: A Guide To Accessibility ofSuhailShaikhNo ratings yet

- Production Planning in The Clothing Industry:: Failing To Plan Is Planning To FailDocument5 pagesProduction Planning in The Clothing Industry:: Failing To Plan Is Planning To Failjatinder.kaler100% (2)

- Performance Polos Classic PolosDocument37 pagesPerformance Polos Classic PolosSuhailShaikhNo ratings yet

- Inventory Sap b1Document8 pagesInventory Sap b1Queen ValleNo ratings yet

- Managing Quality: Integrating The Supply Chain: Sixth EditionDocument26 pagesManaging Quality: Integrating The Supply Chain: Sixth EditionCarmenn LouNo ratings yet

- Afar2 Construction QuizDocument2 pagesAfar2 Construction QuizJoyce Anne MananquilNo ratings yet

- By Laws Amended As at 1 July 2022 PDFDocument364 pagesBy Laws Amended As at 1 July 2022 PDFJING YI LIMNo ratings yet

- The Administrative Office Management: Work Office Efficiency ProductivityDocument10 pagesThe Administrative Office Management: Work Office Efficiency ProductivityN-jay ErnietaNo ratings yet

- FBM 3-9-21 Studs and TrackDocument4 pagesFBM 3-9-21 Studs and TrackRamonNo ratings yet

- Product Protocol DetailsDocument10 pagesProduct Protocol DetailsMarysol AlcorizaNo ratings yet

- Reducing Customer Waiting Time of CommerDocument50 pagesReducing Customer Waiting Time of CommerDr. Abhay K SrivastavaNo ratings yet

- The Search For MultibaggersDocument40 pagesThe Search For MultibaggersAditya MittalNo ratings yet

- The Principles of Project Management Cap. 2 ResumenDocument7 pagesThe Principles of Project Management Cap. 2 ResumenlauraNo ratings yet

- Statistics For Engineers and Scientists 4th Edition William Navidi Solutions ManualDocument26 pagesStatistics For Engineers and Scientists 4th Edition William Navidi Solutions ManualMarioAbbottojqd98% (46)

- Uk Water Bill P5Document1 pageUk Water Bill P5Yu FengNo ratings yet

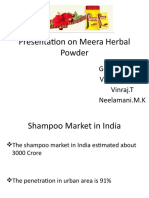

- Presentation On Meera Herbal Powder: Gowrishankar.V Vinothkumar.G Vinraj.T Neelamani.M.KDocument24 pagesPresentation On Meera Herbal Powder: Gowrishankar.V Vinothkumar.G Vinraj.T Neelamani.M.KGowri ShankarNo ratings yet

- Tugas Sap SD Azura TasyaDocument4 pagesTugas Sap SD Azura TasyaREG.A/0218101521/ANISA ARMADIANANo ratings yet

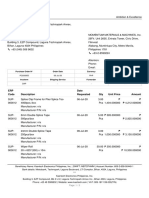

- Kaertech Electronics PO for Splice Clips and TapesDocument2 pagesKaertech Electronics PO for Splice Clips and TapesElena MosnitNo ratings yet

- Sports FootwearDocument17 pagesSports FootwearsuryaNo ratings yet

- Service Design TemplateDocument10 pagesService Design TemplateRobert HeritageNo ratings yet

- Erp Receipt ReverseDocument15 pagesErp Receipt ReversesureshNo ratings yet

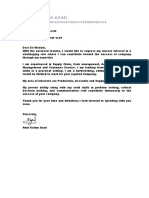

- Abul Kalam Azad - 200806-001-A3Document3 pagesAbul Kalam Azad - 200806-001-A3coy iviNo ratings yet

- E-Tender For Empanelment of Record Management Agencies For Branches/Offices of Punjab & Sind Bank For Delhi/NcrDocument50 pagesE-Tender For Empanelment of Record Management Agencies For Branches/Offices of Punjab & Sind Bank For Delhi/NcrAyushNo ratings yet

- Case Study On Royal MAil WCA ConceptDocument3 pagesCase Study On Royal MAil WCA ConceptRupansh SharmaNo ratings yet

- Business Model CanvasDocument35 pagesBusiness Model CanvasCatherine Mae MacailaoNo ratings yet

- Logistical Interfaces With ProcurementDocument7 pagesLogistical Interfaces With ProcurementJaymark CasingcaNo ratings yet

- NEW Kontoor Manufacturing Routing Guide 2021.22 Version 2.1.FINALDocument29 pagesNEW Kontoor Manufacturing Routing Guide 2021.22 Version 2.1.FINALVeronica BrenisNo ratings yet

- Auditing and Assurance - HonoursDocument2 pagesAuditing and Assurance - HonoursVardaan JaiswalNo ratings yet

- OBAT PT. Anugerah Pharmindo Lestari Agustus Akhir 2021Document1 pageOBAT PT. Anugerah Pharmindo Lestari Agustus Akhir 2021Stenris AnthonyNo ratings yet

- Stats SA Annual Report Book 1Document235 pagesStats SA Annual Report Book 1munya masimbaNo ratings yet

- Economics WorkDocument6 pagesEconomics WorkSarim ZiaNo ratings yet

- Managerial Studies in EnglishDocument148 pagesManagerial Studies in EnglishRa babNo ratings yet

- C11 Strategy DevelopmentDocument30 pagesC11 Strategy DevelopmentPARTI KEADILAN RAKYAT NIBONG TEBALNo ratings yet