You might also like

- Stock Market Crash in BangladeshDocument26 pagesStock Market Crash in BangladeshhrikilNo ratings yet

- Recent Trend of Capital Market of Bangladesh by Syed Golam Shahjarul AlamDocument44 pagesRecent Trend of Capital Market of Bangladesh by Syed Golam Shahjarul AlamSyed Golam Shahjarul AlamNo ratings yet

- Executive SummaryDocument27 pagesExecutive Summarybalal_hossain_1No ratings yet

- Executive SummaryDocument33 pagesExecutive SummaryNavin KabirNo ratings yet

- Bangladesh Stock Market Analysis ReportDocument46 pagesBangladesh Stock Market Analysis Reportanon_472625099100% (2)

- M I E B: Anik AhmedDocument6 pagesM I E B: Anik Ahmedmahir5109No ratings yet

- Stock Market Crash in 2010: An Empirical Study On Retail Investor's Perception in BangladeshDocument15 pagesStock Market Crash in 2010: An Empirical Study On Retail Investor's Perception in BangladeshNiladriAcholNo ratings yet

- Stock Market Crash in BD 1996 - ReportDocument24 pagesStock Market Crash in BD 1996 - ReportSubrata DebnathNo ratings yet

- Macro Economics - Anik AhmedDocument6 pagesMacro Economics - Anik AhmedAnupam BiswasNo ratings yet

- Stock Market Crash 2010: Retail Investor Perception in BangladeshDocument15 pagesStock Market Crash 2010: Retail Investor Perception in BangladeshmilonNo ratings yet

- An Overview of Bangladesh Stock MarketMd Moniruzzaman MoniDocument74 pagesAn Overview of Bangladesh Stock MarketMd Moniruzzaman MoniAshraful FerdousNo ratings yet

- Performance Analysis of Small Investors in The Capital Market of Bangladesh (A Case Study of Chittagong Stock Exchange (CSE) )Document15 pagesPerformance Analysis of Small Investors in The Capital Market of Bangladesh (A Case Study of Chittagong Stock Exchange (CSE) )N. MehrajNo ratings yet

- The Potential of Derivatives Market in BangladeshDocument47 pagesThe Potential of Derivatives Market in BangladeshNahid Md. AlamNo ratings yet

- Factors Influencing Crashes in Bangladesh's Share MarketsDocument10 pagesFactors Influencing Crashes in Bangladesh's Share MarketsmilonNo ratings yet

- Bangladesh Capital Market Contribution to GDPDocument6 pagesBangladesh Capital Market Contribution to GDPAltaf HossainNo ratings yet

- Derivatives Individual AssignmentDocument24 pagesDerivatives Individual AssignmentCarine TeeNo ratings yet

- Financial Markets in IndiaDocument15 pagesFinancial Markets in Indiaamitinfo_mishraNo ratings yet

- Chapter 1 To 5Document51 pagesChapter 1 To 5abelNo ratings yet

- Role of Capital Market For Economic Development of BangladeshDocument6 pagesRole of Capital Market For Economic Development of Bangladeshfiroz chowdhury0% (1)

- Capital Market in Bangladesh - An Overview in The Present ContextDocument33 pagesCapital Market in Bangladesh - An Overview in The Present ContextMd Asifur Rahman89% (65)

- International Journal of Business and Management Invention (IJBMI)Document8 pagesInternational Journal of Business and Management Invention (IJBMI)inventionjournalsNo ratings yet

- Investment in Financial Securities in India Since GlobalisationDocument10 pagesInvestment in Financial Securities in India Since GlobalisationrajatNo ratings yet

- Fundamental Analysis in Capital MarketsDocument120 pagesFundamental Analysis in Capital Marketssaurabh khatateNo ratings yet

- Determinants of Bangladesh Stock Market Debacle 2010-2011Document33 pagesDeterminants of Bangladesh Stock Market Debacle 2010-2011Falguni Chowdhury100% (1)

- Money MarketDocument6 pagesMoney MarketAbhisek BaradiaNo ratings yet

- Derivative Market of BDDocument47 pagesDerivative Market of BDConnorLokman0% (3)

- Importance of Housing Finance Companies in Development of Financial Markets of BangladeshDocument15 pagesImportance of Housing Finance Companies in Development of Financial Markets of Bangladeshjohn017312586No ratings yet

- INFINEETI Go A Institute of Management Anish Bhattacharya Indian Debt Market Need For DevelopmentDocument4 pagesINFINEETI Go A Institute of Management Anish Bhattacharya Indian Debt Market Need For DevelopmentAnish BhattacharyaNo ratings yet

- Long Run Performance of IPO Stocks in BangladeshDocument23 pagesLong Run Performance of IPO Stocks in BangladeshAyesha SiddikaNo ratings yet

- Growth and Development of Bond Market in Bangladesh-An Evaluative StudyDocument14 pagesGrowth and Development of Bond Market in Bangladesh-An Evaluative StudyFatema JidnaNo ratings yet

- Financial Derivatives in Bangladesh PerspectivesDocument37 pagesFinancial Derivatives in Bangladesh PerspectivesArfan Pias-Us-ZamanNo ratings yet

- Capital Market in BangladeshDocument7 pagesCapital Market in BangladeshJack HunterNo ratings yet

- 3 Arco 100114Document40 pages3 Arco 100114Arun HariharanNo ratings yet

- Reason Behind Crashing Capital Market in Bangladesh in 2010Document6 pagesReason Behind Crashing Capital Market in Bangladesh in 2010hasib santobuNo ratings yet

- Article Nusrat Nargis Stock MarketDocument8 pagesArticle Nusrat Nargis Stock MarketNazir Ahmed ZihadNo ratings yet

- Bond in BangladeshDocument14 pagesBond in BangladeshMarshal Richard0% (1)

- Accounting 5Document69 pagesAccounting 5Faith MoneyNo ratings yet

- Capital Market Project PDFDocument99 pagesCapital Market Project PDFNelson RajNo ratings yet

- Capital MarketDocument64 pagesCapital MarketRita PalNo ratings yet

- Financial Issues Faced by Retail InvestorsDocument51 pagesFinancial Issues Faced by Retail InvestorsMoneylife Foundation100% (2)

- ART12010201 2 With Cover Page v2Document48 pagesART12010201 2 With Cover Page v2Arfan Pias-Us-ZamanNo ratings yet

- A Project Report O1Document49 pagesA Project Report O1niraj3handeNo ratings yet

- Chapter No.2 Review of LiteratureDocument28 pagesChapter No.2 Review of Literaturepooja shandilyaNo ratings yet

- Reasons For Fluctuations in Share Prices in Secondary Market.Document79 pagesReasons For Fluctuations in Share Prices in Secondary Market.Abu Awal Md. Shoeb0% (1)

- CorpBond Market IndiaDocument32 pagesCorpBond Market Indiamahajanamol89No ratings yet

- A Project On Capital Market: Submitted To: Punjab Technical University, JalandharDocument95 pagesA Project On Capital Market: Submitted To: Punjab Technical University, JalandharSourav ChoudharyNo ratings yet

- Investment AssignmentDocument5 pagesInvestment AssignmentPrince Hiwot Ethiopia100% (1)

- 1 Origin of The Report:: 1 - PageDocument36 pages1 Origin of The Report:: 1 - PageMohammad ShibliNo ratings yet

- Capstone 182051012Document35 pagesCapstone 182051012Kishan YadavNo ratings yet

- A Comparative Analysis of Mutual Funds With Respect To IL CoDocument175 pagesA Comparative Analysis of Mutual Funds With Respect To IL CoUpasana BhattacharyaNo ratings yet

- Capital Market Project AnalysisDocument53 pagesCapital Market Project AnalysisShuchi KaintholaNo ratings yet

- 5indian Bond Market WP Nipfp 2012Document22 pages5indian Bond Market WP Nipfp 2012Rajat KaushikNo ratings yet

- Stock Market and Foreign Exchange Market: An Empirical GuidanceFrom EverandStock Market and Foreign Exchange Market: An Empirical GuidanceNo ratings yet

- Indian Stock Market and Investors StrategyFrom EverandIndian Stock Market and Investors StrategyRating: 3.5 out of 5 stars3.5/5 (3)

- Market Players: A Guide to the Institutions in Today's Financial MarketsFrom EverandMarket Players: A Guide to the Institutions in Today's Financial MarketsRating: 5 out of 5 stars5/5 (4)

- Financial Markets Fundamentals: Why, how and what Products are traded on Financial Markets. Understand the Emotions that drive TradingFrom EverandFinancial Markets Fundamentals: Why, how and what Products are traded on Financial Markets. Understand the Emotions that drive TradingNo ratings yet

- EIB Working Papers 2019/10 - Structural and cyclical determinants of access to finance: Evidence from EgyptFrom EverandEIB Working Papers 2019/10 - Structural and cyclical determinants of access to finance: Evidence from EgyptNo ratings yet

- The Following Information Is Available To Reconcile Style Co SDocument2 pagesThe Following Information Is Available To Reconcile Style Co SAmit PandeyNo ratings yet

- Training in Human Resource ManagementDocument21 pagesTraining in Human Resource ManagementAlok kumarNo ratings yet

- DHL DissertationDocument8 pagesDHL DissertationJahangir AliNo ratings yet

- CS, PS and EfficiencyDocument45 pagesCS, PS and EfficiencySubodh MohapatroNo ratings yet

- MRB Approves Nonconforming PartsDocument3 pagesMRB Approves Nonconforming PartsMiguel RodriguezNo ratings yet

- Design Books and Price Books for American Federal-Period Card TablesDocument16 pagesDesign Books and Price Books for American Federal-Period Card TablesJosh ChoughNo ratings yet

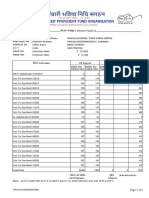

- Member Passbook DetailsDocument2 pagesMember Passbook DetailsNaveen SinghNo ratings yet

- 1271 XII Accountancy Study Material Supplementary Material HOTS and VBQ 2014 15 PDFDocument380 pages1271 XII Accountancy Study Material Supplementary Material HOTS and VBQ 2014 15 PDFBalaji TkpNo ratings yet

- Developing Lean and Agile Automotive Suppliers ManDocument12 pagesDeveloping Lean and Agile Automotive Suppliers ManLia Nurul MulyaniNo ratings yet

- Anush IpDocument24 pagesAnush IpAnsh SharmaNo ratings yet

- Assessment On The Influence of Tax Education On Tax Compliance The Case Study of Tanzania Revenue Authority - Keko Bora Temeke BranchDocument33 pagesAssessment On The Influence of Tax Education On Tax Compliance The Case Study of Tanzania Revenue Authority - Keko Bora Temeke BranchSikudhani MmbagaNo ratings yet

- 00 AY 2022-2023 CA51027 Accounting For Government and Non-Profit Organizations REVISED COURSE PLAN DUE To COVID 19 PANDEMICDocument8 pages00 AY 2022-2023 CA51027 Accounting For Government and Non-Profit Organizations REVISED COURSE PLAN DUE To COVID 19 PANDEMICJaimellNo ratings yet

- 30 Free Leed Ap BD+C Sample QuestionsDocument23 pages30 Free Leed Ap BD+C Sample QuestionsSubhranshu PandaNo ratings yet

- RBI's Credit Monitoring Arrangement and Tandon Committee recommendationsDocument4 pagesRBI's Credit Monitoring Arrangement and Tandon Committee recommendationsAbhi_IMK100% (1)

- Borrowing Costs: DefinitionsDocument23 pagesBorrowing Costs: DefinitionsAbdul Sami100% (1)

- College Fees StructureDocument1 pageCollege Fees StructureVijay MNo ratings yet

- Tata Tea - FADocument27 pagesTata Tea - FASagar BsNo ratings yet

- Goodwill 23.3.23Document1 pageGoodwill 23.3.2308 Ajay Halder 11- CNo ratings yet

- Accounts PaperDocument2 pagesAccounts PaperRohan Ghadge-46No ratings yet

- Explore and Explain:: Grade 12 - EntrepreneurshipDocument12 pagesExplore and Explain:: Grade 12 - EntrepreneurshipLatifah EmamNo ratings yet

- Consumer Behaviour, 2nd Edition - Chapter 1Document42 pagesConsumer Behaviour, 2nd Edition - Chapter 1guptamadras100% (1)

- The Suitability of Sales Promotion Competitions: As A Social Marketing Too)Document330 pagesThe Suitability of Sales Promotion Competitions: As A Social Marketing Too)Nabuweya NoordienNo ratings yet

- Faculty Handbook MGT FinalDocument48 pagesFaculty Handbook MGT FinalTiwanka MadurangaNo ratings yet

- BGC Internship Job Description On LetterheadDocument4 pagesBGC Internship Job Description On Letterheadgadija ishahNo ratings yet

- Statement of Cash FlowsDocument6 pagesStatement of Cash FlowsJustine VeralloNo ratings yet

- Power Purchase AgreementDocument22 pagesPower Purchase Agreementdark webNo ratings yet

- ECON 1580 Discussion Assignment Unit 4Document1 pageECON 1580 Discussion Assignment Unit 4TesfahunNo ratings yet

- Mesfin MuluDocument103 pagesMesfin MuluCanlor Lopes100% (1)

- New Invt MGT KesoramDocument69 pagesNew Invt MGT Kesoramtulasinad123No ratings yet

- Institute of Management Studies and Research: KLE Society'sDocument22 pagesInstitute of Management Studies and Research: KLE Society'sRutuja HukkeriNo ratings yet