You might also like

- Kickstart Your Corporation: The Incorporated Professional's Financial Planning CoachFrom EverandKickstart Your Corporation: The Incorporated Professional's Financial Planning CoachNo ratings yet

- Quiz 14 SolutionsDocument16 pagesQuiz 14 SolutionsAlex OzfordNo ratings yet

- Accounting Quiz 2Document8 pagesAccounting Quiz 2Camille G.No ratings yet

- CorporationDocument4 pagesCorporationJasmine ActaNo ratings yet

- A. Corporate Reorganization: 1.A 6.B 11.D 16.A 2.C 7.C 12.C 17.C 3.D 8.D 13.C 18.B 4.B 9.B 14.C 19.D 5.A 10.D 15.A 20.CDocument23 pagesA. Corporate Reorganization: 1.A 6.B 11.D 16.A 2.C 7.C 12.C 17.C 3.D 8.D 13.C 18.B 4.B 9.B 14.C 19.D 5.A 10.D 15.A 20.CHilario, Jana Rizzette C.No ratings yet

- Acctg110 FinalsDocument21 pagesAcctg110 FinalsRoman Dominic LlanoNo ratings yet

- When To Be RECOGNIZED?: A. Current LiabilitiesDocument10 pagesWhen To Be RECOGNIZED?: A. Current LiabilitiesMark Domingo MendozaNo ratings yet

- Auditing Problem Quiz 2 Long Problem SolutionsDocument7 pagesAuditing Problem Quiz 2 Long Problem Solutionsreina maica terradoNo ratings yet

- Shadden PanaoDocument5 pagesShadden PanaoJoebin Corporal LopezNo ratings yet

- BSA2BQuiz 3Document19 pagesBSA2BQuiz 3Monica Enrico0% (1)

- Quiz 2 Cashflows Final PDFDocument4 pagesQuiz 2 Cashflows Final PDFChito MirandaNo ratings yet

- 115,200.00 Two 100,200.00 TwoDocument19 pages115,200.00 Two 100,200.00 TwoAlexandra Nicole IsaacNo ratings yet

- FS Consolidation at The Date of Acquisition v2Document16 pagesFS Consolidation at The Date of Acquisition v2Pagatpat, Apple Grace C.No ratings yet

- BADVAC1XDocument8 pagesBADVAC1Xfaye pantiNo ratings yet

- Discussion Problems and Solutions On Module 3, Part 1Document28 pagesDiscussion Problems and Solutions On Module 3, Part 1AJ Biagan MoraNo ratings yet

- Solutions To Chapter 6 Vera CruzDocument9 pagesSolutions To Chapter 6 Vera CruzLuzz Landicho100% (1)

- Jawaban Latihan Soal AklDocument11 pagesJawaban Latihan Soal AklFauzi AbdillahNo ratings yet

- Multiple Choice Short Problem Midterm Exams SolutionsDocument13 pagesMultiple Choice Short Problem Midterm Exams SolutionsTrisha Mae BrazaNo ratings yet

- UntitledDocument13 pagesUntitledAnne GuamosNo ratings yet

- Direct LaborDocument8 pagesDirect LaborAreli DuyoNo ratings yet

- Cash Flows PAS7Document10 pagesCash Flows PAS7Jenyl Mae NobleNo ratings yet

- Shareholders EquityDocument11 pagesShareholders EquityJasmine ActaNo ratings yet

- LeahDocument6 pagesLeahJoebin Corporal LopezNo ratings yet

- Problem 1Document4 pagesProblem 1Rio De LeonNo ratings yet

- Cash Flow Statement QuestionDocument5 pagesCash Flow Statement QuestionsatyaNo ratings yet

- AACA2 AssignmentsDocument20 pagesAACA2 AssignmentsadieNo ratings yet

- Chapter 1 Abc Suggested SolutionsDocument7 pagesChapter 1 Abc Suggested SolutionsAlthea Lyn ReyesNo ratings yet

- Particulars Debit CreditDocument10 pagesParticulars Debit CreditJasmine ActaNo ratings yet

- Audit of Shareholders Equity ActivityDocument31 pagesAudit of Shareholders Equity ActivityIris FenelleNo ratings yet

- Seatwork Problem 1Document11 pagesSeatwork Problem 1Zihr EllerycNo ratings yet

- Accounting AssignmentDocument13 pagesAccounting AssignmentPetrinaNo ratings yet

- Corporation Issuance of Shares Illutsrative ProblemDocument15 pagesCorporation Issuance of Shares Illutsrative ProblemHoney MuliNo ratings yet

- Business CombinationDocument10 pagesBusiness CombinationJaira ClavoNo ratings yet

- Question No 1: A-Gross PayDocument6 pagesQuestion No 1: A-Gross PayArmaghan Ali MalikNo ratings yet

- Assignment Bsma 1a May 27Document14 pagesAssignment Bsma 1a May 27Maeca Angela Serrano100% (1)

- GPV & SCF (Assignment)Document16 pagesGPV & SCF (Assignment)Mica Moreen GuillermoNo ratings yet

- AP 5904Q InvestmentsDocument6 pagesAP 5904Q InvestmentsRhea NograNo ratings yet

- Proceeds of Property Insurance (BV 4,000,000)Document11 pagesProceeds of Property Insurance (BV 4,000,000)zeref dragneelNo ratings yet

- Planed Cash Reciepts: Collection of Account RecievablesDocument11 pagesPlaned Cash Reciepts: Collection of Account RecievablesMani ManandharNo ratings yet

- P and L and BSDocument8 pagesP and L and BSgautam48128No ratings yet

- IA3 Chapter 12 21Document12 pagesIA3 Chapter 12 21ZicoNo ratings yet

- 001 AdvanceDocument6 pages001 AdvanceSa BilNo ratings yet

- 1.) Answer: 1 050 000: Prelim Bring Home ExamDocument12 pages1.) Answer: 1 050 000: Prelim Bring Home ExamMary Joy CabilNo ratings yet

- Atillo, Portfolio 3 - Bsa 314Document7 pagesAtillo, Portfolio 3 - Bsa 314Jeth MahusayNo ratings yet

- Flores Assignment Corporation PDFDocument13 pagesFlores Assignment Corporation PDFGwen Stefani DaugdaugNo ratings yet

- Topic 15Document35 pagesTopic 15Francesjoyze LahoraNo ratings yet

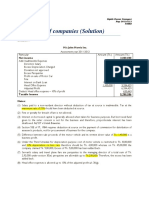

- Assessment of Companies (Solution) : Solution 1 M/s John Morris IncDocument8 pagesAssessment of Companies (Solution) : Solution 1 M/s John Morris IncIQBALNo ratings yet

- CF Statement Solutions 1Document4 pagesCF Statement Solutions 1Joy MukhiNo ratings yet

- Pas 1, Pas 2, Pas 7Document29 pagesPas 1, Pas 2, Pas 7MPCINo ratings yet

- GROUP 6 Problem 3 7 To 3 9Document24 pagesGROUP 6 Problem 3 7 To 3 9Hans ManaliliNo ratings yet

- Cash Flow Statement-ExampleDocument18 pagesCash Flow Statement-ExampleAnakha RadhakrishnanNo ratings yet

- Final Summative Assessment - Ae112 (1St Sem 2020-2021) - Quiz 1 Suggested Key AnswerDocument3 pagesFinal Summative Assessment - Ae112 (1St Sem 2020-2021) - Quiz 1 Suggested Key AnswerDjunah ArellanoNo ratings yet

- Homework Answer (Quiz 1-2 Revision)Document7 pagesHomework Answer (Quiz 1-2 Revision)Kccc siniNo ratings yet

- Sample Problems Cash Flow AnalysisDocument2 pagesSample Problems Cash Flow AnalysisTeresa AlbertoNo ratings yet

- Oria, Maybelyn S. Cfas - Sec 10: What Total Amount Should Be Reported As Shareholders' Equity?Document52 pagesOria, Maybelyn S. Cfas - Sec 10: What Total Amount Should Be Reported As Shareholders' Equity?May OriaNo ratings yet

- Chapter 19 Exercises & ProblemsDocument10 pagesChapter 19 Exercises & ProblemsRiza Mae AlceNo ratings yet

- Enriquez, Vixen Aaron M. - Assignment On Audit of InvestmentsDocument2 pagesEnriquez, Vixen Aaron M. - Assignment On Audit of InvestmentsVixen Aaron EnriquezNo ratings yet

- Advanced-Accounting-Part 2-Dayag-2015-Chapter-15Document31 pagesAdvanced-Accounting-Part 2-Dayag-2015-Chapter-15allysa amping100% (1)

- Class Activity 1 Cash Flow StatementDocument2 pagesClass Activity 1 Cash Flow StatementHacker SKNo ratings yet

- Akuntansi Keuangan Lanjutan 1Document14 pagesAkuntansi Keuangan Lanjutan 1darwas darwasNo ratings yet

- Work Sheet On Accounting For Share Capital Board Exam Questions Fro 2016-2020Document22 pagesWork Sheet On Accounting For Share Capital Board Exam Questions Fro 2016-2020Cfa Deepti BindalNo ratings yet

- Jodo - Program Manager JDDocument3 pagesJodo - Program Manager JDSarah ShaikhNo ratings yet

- 163 Stokes Vs Continental Trust Co. (Enriquez)Document2 pages163 Stokes Vs Continental Trust Co. (Enriquez)Jovelan EscañoNo ratings yet

- Support IsDocument5 pagesSupport Isdohongvinh40No ratings yet

- FCEBDocument3 pagesFCEBRedefining Success KashishNo ratings yet

- The Daily Profile Guide Volume 1Document22 pagesThe Daily Profile Guide Volume 1AhmedNo ratings yet

- Kelompok 6 ALK - Tugas Case 11-3Document6 pagesKelompok 6 ALK - Tugas Case 11-3Jaisyur Rahman SetyadharmaatmajaNo ratings yet

- Nilai Post Test PJJ Ips Minggu 1 Kelas 9.7 Sampai 9.10Document11 pagesNilai Post Test PJJ Ips Minggu 1 Kelas 9.7 Sampai 9.10irfi nazlaNo ratings yet

- DT.22.2 FM - Midterm ExaminationDocument35 pagesDT.22.2 FM - Midterm ExaminationJericho GeranceNo ratings yet

- PG-20-183 Finlatics Market Performance ReportDocument1 pagePG-20-183 Finlatics Market Performance ReportShreyas KotkarNo ratings yet

- Chapter 14 BBDocument69 pagesChapter 14 BBTaVuKieuNhiNo ratings yet

- 5 6078069466250346586Document168 pages5 6078069466250346586Achuthamohan100% (1)

- Theories of Exchange RateDocument11 pagesTheories of Exchange RateNiharika Satyadev Jaiswal100% (1)

- Chapter 1 of MA4257 (Financial Math II by Min Dai)Document7 pagesChapter 1 of MA4257 (Financial Math II by Min Dai)SNo ratings yet

- Session 13a Rysman Two Sided MktsDocument43 pagesSession 13a Rysman Two Sided MktsDanielaNo ratings yet

- The Logical Trader Applying A Method To The Madness PDFDocument137 pagesThe Logical Trader Applying A Method To The Madness PDFJose GuzmanNo ratings yet

- Solution Manual For Financial Statement Analysis and Valuation 2nd Edition by EastonDocument32 pagesSolution Manual For Financial Statement Analysis and Valuation 2nd Edition by EastonJenniferPalmerdqwf98% (43)

- CSC v1 c10 - DerivativesDocument48 pagesCSC v1 c10 - DerivativessmaliasNo ratings yet

- Module IV - Corporate Level Strategy (Part A)Document23 pagesModule IV - Corporate Level Strategy (Part A)Ashritha SangishettyNo ratings yet

- FINA3303 Lecture 5 Class PDFDocument55 pagesFINA3303 Lecture 5 Class PDFTsui KelvinNo ratings yet

- Buyback of SharesDocument32 pagesBuyback of SharesKARISHMAATA2No ratings yet

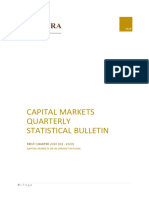

- Capital Markets Statistical Bulletin Q1 - 2020Document23 pagesCapital Markets Statistical Bulletin Q1 - 2020LindaNo ratings yet

- Chapter 4 Stock Valuation (Student)Document10 pagesChapter 4 Stock Valuation (Student)Nguyễn Thái Minh ThưNo ratings yet

- (Blume) Investment Report - 11A+B+C (H1 2014)Document11 pages(Blume) Investment Report - 11A+B+C (H1 2014)hkalertNo ratings yet

- Yes Bank Limited: Update To Credit AnalysisDocument11 pagesYes Bank Limited: Update To Credit AnalysisnaguficoNo ratings yet

- Royal Mail PLC Solution Finance CaseDocument8 pagesRoyal Mail PLC Solution Finance CaseAamir Khan100% (3)

- If Chapter 4 Determining The Exchange RateDocument67 pagesIf Chapter 4 Determining The Exchange Rateธชพร พรหมสีดาNo ratings yet

- Online Resources For Stock Investing and TradingDocument61 pagesOnline Resources For Stock Investing and TradingAJ JarillasNo ratings yet

- Master Circular - CRR and SLR - 2010Document24 pagesMaster Circular - CRR and SLR - 2010prathi05No ratings yet