You might also like

- Homework 5Document3 pagesHomework 5Kevin0% (3)

- Acccob3 HW2Document18 pagesAcccob3 HW2Aaron HuangNo ratings yet

- Strategic Marketing 1st Edition Mooradian Test BankDocument9 pagesStrategic Marketing 1st Edition Mooradian Test Bankmeganfloresyfwemzsrdp100% (15)

- Supply Chain Strategy Analysis of The Benetton CaseDocument6 pagesSupply Chain Strategy Analysis of The Benetton CasebizaczkiNo ratings yet

- Marginal Costing & Absorption CostingDocument56 pagesMarginal Costing & Absorption CostingHoàng Phương ThảoNo ratings yet

- Chapter 2 EOQ MODELDocument24 pagesChapter 2 EOQ MODELHamdan Hassin100% (2)

- Research Report On Strategies of Amul and SarasDocument84 pagesResearch Report On Strategies of Amul and Sarasswatigupta8880% (5)

- Chapter 2 Cost ClassificationsDocument18 pagesChapter 2 Cost Classificationsmarizemeyer2No ratings yet

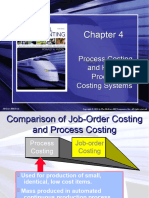

- Chapter No.04 - Process Costing and Hybrid Product-Costing SystemsDocument39 pagesChapter No.04 - Process Costing and Hybrid Product-Costing SystemsWali NoorzadNo ratings yet

- Akb Bab4Document37 pagesAkb Bab4MulyaniNo ratings yet

- Hilton 11e Chap004 PPT-STUDocument42 pagesHilton 11e Chap004 PPT-STULạnh LùngNo ratings yet

- Process Costing and Hybrid Product-Costing SystemsDocument38 pagesProcess Costing and Hybrid Product-Costing SystemsZia UddinNo ratings yet

- Hilton Chapter 4 Prerecorded LectureDocument12 pagesHilton Chapter 4 Prerecorded Lecturesunq hccnNo ratings yet

- Chap4 (E)Document47 pagesChap4 (E)Kiên Lê TrungNo ratings yet

- Process Costing and Hybrid Product-Costing Systems: Mcgraw-Hill/IrwinDocument44 pagesProcess Costing and Hybrid Product-Costing Systems: Mcgraw-Hill/Irwinsunanda mNo ratings yet

- Chap004 7e EditedDocument47 pagesChap004 7e EditedfarahNo ratings yet

- Cost - Terms Concepts and ClassificationsDocument17 pagesCost - Terms Concepts and ClassificationsSwap WerdNo ratings yet

- (Revised) Week 13 - ReviewDocument94 pages(Revised) Week 13 - ReviewCheuk Ling SoNo ratings yet

- Hilton Chapter 3 Live Adobe ConnectDocument13 pagesHilton Chapter 3 Live Adobe ConnectaksNo ratings yet

- Hilton Chapter 4 Live Adobe ConnectDocument15 pagesHilton Chapter 4 Live Adobe ConnectJaved ImranNo ratings yet

- Absorption Costing Vs Variable CostingDocument20 pagesAbsorption Costing Vs Variable CostingMa. Alene MagdaraogNo ratings yet

- Chaitra B Chaitra C MDocument28 pagesChaitra B Chaitra C MChaitra MuralidharaNo ratings yet

- Cost Terminologies and ClassficationsDocument51 pagesCost Terminologies and ClassficationsLim Jie XiNo ratings yet

- NOTE CHAPTER 9 - Absorption Costing & Marginal CostingDocument18 pagesNOTE CHAPTER 9 - Absorption Costing & Marginal CostingNUR ANIS SYAMIMI BINTI MUSTAFA / UPMNo ratings yet

- 07 Module 03 AVC PDFDocument12 pages07 Module 03 AVC PDFMarriah Izzabelle Suarez RamadaNo ratings yet

- Inventory Costing: Chapter NineDocument39 pagesInventory Costing: Chapter NineDio VinosaNo ratings yet

- Cost Term, Concept and ClassificationsDocument28 pagesCost Term, Concept and ClassificationskumarNo ratings yet

- Costman Variable CostingDocument2 pagesCostman Variable CostingJeremi BernardoNo ratings yet

- Ma1 PDFDocument65 pagesMa1 PDFĐức TrầnNo ratings yet

- Cost TutorialDocument26 pagesCost TutorialedrianclydeNo ratings yet

- AF3112 Management Accounting 2: Process CostingDocument66 pagesAF3112 Management Accounting 2: Process Costing行歌No ratings yet

- Cost Accounting ReviewerDocument7 pagesCost Accounting Reviewerjaninasachadelacruz0119No ratings yet

- Cost Accountingpractical 2021-22 PDFDocument42 pagesCost Accountingpractical 2021-22 PDFSora 1211100% (1)

- Cost Concepts: Ilene D. Padilla Cpa, MbaDocument53 pagesCost Concepts: Ilene D. Padilla Cpa, Mbaharley_quinn11No ratings yet

- Process Costing and Hybrid Product-Costing SystemsDocument17 pagesProcess Costing and Hybrid Product-Costing SystemsWailNo ratings yet

- ACT121 - Topic 5Document5 pagesACT121 - Topic 5Juan FrivaldoNo ratings yet

- Chapter 4 OverheadDocument21 pagesChapter 4 OverheadMUHAMMAD ZAIM HAMZI MUHAMMAD ZINNo ratings yet

- Absorption and Variable CostingDocument2 pagesAbsorption and Variable CostingFelimar CalaNo ratings yet

- IWB Chapter 5 - Marginal and Absorption CostingDocument28 pagesIWB Chapter 5 - Marginal and Absorption Costingjulioruiz891No ratings yet

- Acc GR 11 T4 Week 1&2 Manuftring Costs ENGDocument4 pagesAcc GR 11 T4 Week 1&2 Manuftring Costs ENGsihlemooi3No ratings yet

- Variable Costing: A Tool For Management: Chapter SevenDocument37 pagesVariable Costing: A Tool For Management: Chapter SevenJavier TsangNo ratings yet

- Cost Terms, Concepts, and ClassificationsDocument22 pagesCost Terms, Concepts, and ClassificationsKi xxiNo ratings yet

- Session - 4&5 (A) : Product CostingDocument38 pagesSession - 4&5 (A) : Product CostingAnkitShettyNo ratings yet

- Cost and Cost Behavior IntroductionDocument1 pageCost and Cost Behavior IntroductionArvin BeduralNo ratings yet

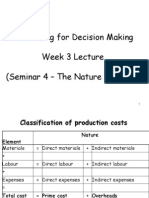

- Accounting For Decision Making Week 3 Lecture (Seminar 4 - The Nature of Costs)Document51 pagesAccounting For Decision Making Week 3 Lecture (Seminar 4 - The Nature of Costs)nwcbenny337No ratings yet

- ReviewDocument68 pagesReviewHồng Phạm Thị ÁnhNo ratings yet

- (Cpar2017) Mas-8205 (Product Costing) PDFDocument12 pages(Cpar2017) Mas-8205 (Product Costing) PDFSusan Esteban Espartero50% (2)

- Ronald Hilton Chapter 3Document25 pagesRonald Hilton Chapter 3Difen L HaradiniNo ratings yet

- SCM Unit 4 Variable and Absorption CostingDocument9 pagesSCM Unit 4 Variable and Absorption CostingMargie Garcia LausaNo ratings yet

- Mas: Variable and Absorption Costing Concept Summary: Comparison As To Treatment of Operating CostsDocument3 pagesMas: Variable and Absorption Costing Concept Summary: Comparison As To Treatment of Operating CostsClyde RamosNo ratings yet

- Chap 004Document15 pagesChap 004Ahmad Restu FauziNo ratings yet

- Lecture 2 Cost Terms, Concepts and ClassificationDocument34 pagesLecture 2 Cost Terms, Concepts and ClassificationTgrh TgrhNo ratings yet

- Absorption and Variable Costing: Types of Product Costing MethodDocument2 pagesAbsorption and Variable Costing: Types of Product Costing MethodKuya ANo ratings yet

- Cost Terms, Concepts, and ClassificationDocument27 pagesCost Terms, Concepts, and ClassificationParadise VillageNo ratings yet

- Segment Reporting and Performance EvaluationDocument23 pagesSegment Reporting and Performance EvaluationiqbalrzzNo ratings yet

- Direct Costing2Document11 pagesDirect Costing2Lamtiur LidiaqNo ratings yet

- Chapter 4: Type of Cost: Direct Costs (Prime Costs) Indirect Costs (Overheads)Document8 pagesChapter 4: Type of Cost: Direct Costs (Prime Costs) Indirect Costs (Overheads)Claudia WongNo ratings yet

- Week 2-Basic Cost ManagementDocument21 pagesWeek 2-Basic Cost ManagementRichard Oliver CortezNo ratings yet

- PGP-CMA-Cost Fundamentals PDFDocument53 pagesPGP-CMA-Cost Fundamentals PDFRiturajPaulNo ratings yet

- Topic 6 - Process CostingDocument7 pagesTopic 6 - Process CostingMuhammad Alif100% (1)

- Act 202 Chapter 2Document52 pagesAct 202 Chapter 2Shaon KhanNo ratings yet

- Manufacturing Cost AcctgDocument6 pagesManufacturing Cost AcctgDivine Nicole Sabit AguirreNo ratings yet

- MPA 602: Cost and Managerial Accounting: Cost Accounting Methods - Job Order Costing, ABC, Process CostingDocument81 pagesMPA 602: Cost and Managerial Accounting: Cost Accounting Methods - Job Order Costing, ABC, Process CostingMd. ZakariaNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Chapter 5 - 6 - Inventory Accounting and ValuationDocument61 pagesChapter 5 - 6 - Inventory Accounting and ValuationNaeemullah baig100% (1)

- Larson17ceV1 SM CH04Document153 pagesLarson17ceV1 SM CH04AdedoyinNo ratings yet

- Financial Regulation and Capital Adequacy: Arthur Centonze FIN644 - Slides 6Document45 pagesFinancial Regulation and Capital Adequacy: Arthur Centonze FIN644 - Slides 6Robert LongoNo ratings yet

- Holcim - HDFC SecuritiesDocument7 pagesHolcim - HDFC SecuritiessachinoakNo ratings yet

- Shri Mahila Griha Udyog Lijjat PapadDocument86 pagesShri Mahila Griha Udyog Lijjat PapadpRiNcE DuDhAtRa60% (5)

- SCM Assignment - Mid - Term - JOCKEYDocument13 pagesSCM Assignment - Mid - Term - JOCKEYPOORNENDUKRISHNA RAONo ratings yet

- CRM NotesDocument32 pagesCRM NotesHari KrishnanNo ratings yet

- Entrep12 - Q2 - M6 - 4MS of Production and Business ModelDocument25 pagesEntrep12 - Q2 - M6 - 4MS of Production and Business ModelRose Marie D TupasNo ratings yet

- Blue DartDocument2 pagesBlue DartPushkar AshtekarNo ratings yet

- Economics Question PaperDocument3 pagesEconomics Question Papershehzad MandrawalaNo ratings yet

- Chap 4Document7 pagesChap 4Christine Joy OriginalNo ratings yet

- The Impact of Rebranding On Guest Satisfaction and Financial PerfDocument57 pagesThe Impact of Rebranding On Guest Satisfaction and Financial PerfNguyen VyNo ratings yet

- Mocha Feelings CompanyDocument11 pagesMocha Feelings CompanyTunelyNo ratings yet

- Assignment 3 Wida Widiawati 19AKJ 194020034Document8 pagesAssignment 3 Wida Widiawati 19AKJ 194020034wida widiawatiNo ratings yet

- Glossary of Terms: Acpl A-Ifrs Asic ASX Barrel (Per Barrel) or BBL Biofuels MarketingDocument1 pageGlossary of Terms: Acpl A-Ifrs Asic ASX Barrel (Per Barrel) or BBL Biofuels MarketingDanny DukeranNo ratings yet

- The State of Social Enterprise in Malaysia British Council Low ResDocument114 pagesThe State of Social Enterprise in Malaysia British Council Low ResRichard T. PetersonNo ratings yet

- Basic Accounting ExamDocument8 pagesBasic Accounting ExamJollibee JollibeeeNo ratings yet

- Tapal DanedarDocument15 pagesTapal DanedarAli Raza100% (1)

- Company Performance - Comuicare in Afaceri in Limba EnglezaDocument10 pagesCompany Performance - Comuicare in Afaceri in Limba EnglezaMincu IulianNo ratings yet

- Retailer Supplier PartnershipDocument12 pagesRetailer Supplier PartnershipSanjeev Bishnoi100% (1)

- SapolioDocument7 pagesSapolioJuan Diego Vasquez BeraunNo ratings yet

- What Is Your Criteria For Selecting A Brand in Terms of Value and WhyDocument3 pagesWhat Is Your Criteria For Selecting A Brand in Terms of Value and WhyMadan JhaNo ratings yet

- PDF Sales Force Management Leadership Innovation Technology 12Th Edition Mark W Johnston Ebook Full ChapterDocument53 pagesPDF Sales Force Management Leadership Innovation Technology 12Th Edition Mark W Johnston Ebook Full Chaptercharity.robichaux234100% (1)

- Anu Ujin Bat Erdene CV Resume PDFDocument1 pageAnu Ujin Bat Erdene CV Resume PDFAnuUjin BatErdeneNo ratings yet

- DD Termsheet-2Document2 pagesDD Termsheet-2Operation BluepayNo ratings yet