You might also like

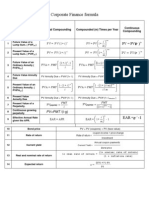

- Corporate Finance FormulasDocument3 pagesCorporate Finance FormulasMustafa Yavuzcan83% (12)

- Time Value of Money FormulasDocument1 pageTime Value of Money FormulasAmit Shankar Choudhary100% (1)

- DeliveryDocument25 pagesDeliverymarcusjwheeler013No ratings yet

- Formula Sheet - PDF For Week 10Document2 pagesFormula Sheet - PDF For Week 10Nat Siow100% (1)

- Formula Sheet Principles of FinanceDocument6 pagesFormula Sheet Principles of FinanceSI PNo ratings yet

- Accounting EquationDocument2 pagesAccounting Equationanalea aguirreNo ratings yet

- Formula Sheet - Quantitative FinanceDocument1 pageFormula Sheet - Quantitative FinanceInês SoaresNo ratings yet

- Midterm Exam AST With AnswersDocument15 pagesMidterm Exam AST With AnswersJames CantorneNo ratings yet

- Micro-Finance Study in JalandharDocument53 pagesMicro-Finance Study in Jalandharkaran_tiff100% (1)

- Corporate Finance Formulas - PDF - Cost of Capital - Present ValueDocument7 pagesCorporate Finance Formulas - PDF - Cost of Capital - Present ValueSurojit PattanayakNo ratings yet

- Formula SheetDocument1 pageFormula Sheetnick07052004No ratings yet

- Chapter 8Document5 pagesChapter 8Hiệp Nguyễn Thị MinhNo ratings yet

- MATH 01 FormulaDocument3 pagesMATH 01 FormulaJae Bert UbisoftNo ratings yet

- Correlation Analysis Regression Analysis: t b−β s/sDocument2 pagesCorrelation Analysis Regression Analysis: t b−β s/sKaren YapNo ratings yet

- Lecture 03 - Mathematics of Finance - W3Document27 pagesLecture 03 - Mathematics of Finance - W3Shiro ChanNo ratings yet

- Untitled Notebook ClassDocument12 pagesUntitled Notebook ClassJose LlundoNo ratings yet

- BU283 Midterm1 Formula SheetDocument1 pageBU283 Midterm1 Formula SheetClarissa MichaelsNo ratings yet

- Formula in Engineering EconimicsDocument2 pagesFormula in Engineering EconimicsWYNDYLL ARTUZNo ratings yet

- Formulas: F - Future Value P - Present/Principal ValueDocument2 pagesFormulas: F - Future Value P - Present/Principal ValueJimuel Ace SarmientoNo ratings yet

- DTFT VS CTFTDocument1 pageDTFT VS CTFTHansen LienardiNo ratings yet

- Class 11 Complex Number Solutions DPP 1Document10 pagesClass 11 Complex Number Solutions DPP 1nabhijain9No ratings yet

- Midterm MathDocument4 pagesMidterm MathTuong TranNo ratings yet

- Assignment 1 ADocument3 pagesAssignment 1 ABin ChristianNo ratings yet

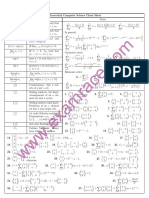

- Data Analysis Formula Sheet Tables (DADM)Document8 pagesData Analysis Formula Sheet Tables (DADM)Karina BoenardiNo ratings yet

- 09 SuitesDocument1 page09 SuiteszouaouacherNo ratings yet

- Edexcel C1 NotesDocument28 pagesEdexcel C1 NotesAmeerHamzaaNo ratings yet

- MAF101 Formula Sheet-2010TR1Document2 pagesMAF101 Formula Sheet-2010TR1Ann VuNo ratings yet

- Math Final CardDocument2 pagesMath Final Cardapi-3859599No ratings yet

- FV FVDocument19 pagesFV FVNhi HoangNo ratings yet

- Matemáticas Aplicadas A La EconomíaDocument9 pagesMatemáticas Aplicadas A La EconomíaLore PauNo ratings yet

- Problems (Annuity)Document23 pagesProblems (Annuity)22-07322No ratings yet

- Appendix A: Formula Sheet: The Following Are Useful Formulae 1. Simple Interest FormulaDocument53 pagesAppendix A: Formula Sheet: The Following Are Useful Formulae 1. Simple Interest FormulasilentNo ratings yet

- Exercise 4Document2 pagesExercise 4inbvt esxcdNo ratings yet

- Finance MathDocument1 pageFinance MathDiana CañasNo ratings yet

- XII. Support Vector MachinesDocument6 pagesXII. Support Vector Machinescharu.hitechrobot2889No ratings yet

- Lin AlgDocument1 pageLin AlgDavid LiuNo ratings yet

- FormulárioDocument1 pageFormulárioGuilhermeNo ratings yet

- Quiz 1 FormulasDocument2 pagesQuiz 1 FormulasCristina Beatrice MallariNo ratings yet

- FormelnDocument1 pageFormelnhanna.ericssonkleinNo ratings yet

- Lecture Notes (Chapter 4) ASC2014 Life Contingencies IDocument39 pagesLecture Notes (Chapter 4) ASC2014 Life Contingencies IYamunaa RatakrishnanNo ratings yet

- Screenshot 2022-08-01 at 8.38.49 PMDocument8 pagesScreenshot 2022-08-01 at 8.38.49 PMdivyanshvashisht22No ratings yet

- Green Electric Energy: Engineering EconomicsDocument45 pagesGreen Electric Energy: Engineering EconomicsdishantpNo ratings yet

- CH 2Document6 pagesCH 2Hemant GoyalNo ratings yet

- Graphing and Properties of ParabolasDocument8 pagesGraphing and Properties of ParabolasMastermsyNo ratings yet

- Engineering Economy Formulas: D A 2b 2b +K + 4 B C 2 BDocument4 pagesEngineering Economy Formulas: D A 2b 2b +K + 4 B C 2 BCrystel ReyesNo ratings yet

- Analysis 3Document10 pagesAnalysis 3Phúc Trần Võ MỹNo ratings yet

- Transportation Economics and Decision Making: Lecture-3Document55 pagesTransportation Economics and Decision Making: Lecture-3Amit AgarwalNo ratings yet

- Formula in StatsDocument2 pagesFormula in StatsHanchey ElipseNo ratings yet

- "Arro.: Qua'low: BoyDocument1 page"Arro.: Qua'low: BoyNgan MaiNo ratings yet

- 04.0 PP 1 27 Binomial PricerDocument27 pages04.0 PP 1 27 Binomial PricerWasilyNo ratings yet

- Assignment On Fundamentals of FinanceDocument29 pagesAssignment On Fundamentals of FinanceIsmail AliNo ratings yet

- 9223 Et EtDocument12 pages9223 Et EtKIYONGA ALEXNo ratings yet

- Devoir 2Document4 pagesDevoir 2ihab acharguiNo ratings yet

- Helpful FormulaeDocument2 pagesHelpful FormulaeBhuvan BhatiaNo ratings yet

- Chapter 1Document20 pagesChapter 1janice ngNo ratings yet

- Integral CalculusDocument4 pagesIntegral CalculusSamNo ratings yet

- Computer Science FormulasDocument10 pagesComputer Science FormulasSheeraz AhmedNo ratings yet

- Consolidated - BondDocument13 pagesConsolidated - BondNurul Waheedatun FatimahNo ratings yet

- Mayes 8e CH02 SolutionsDocument36 pagesMayes 8e CH02 SolutionsRamez AhmedNo ratings yet

- Assignment 4 Revised 1 PDFDocument2 pagesAssignment 4 Revised 1 PDFzuimaoNo ratings yet

- Group Corporate Structure: Commercial Banking Investment BankingDocument1 pageGroup Corporate Structure: Commercial Banking Investment BankingizhsaidinNo ratings yet

- Solution Key To StudentsDocument2 pagesSolution Key To StudentsS M Prathik KumarNo ratings yet

- Solutions To Exercises and Problems Exercises E5.1 Combination and Consolidation, Date of Acquisition (See Related E3.1)Document36 pagesSolutions To Exercises and Problems Exercises E5.1 Combination and Consolidation, Date of Acquisition (See Related E3.1)sunnyauliaNo ratings yet

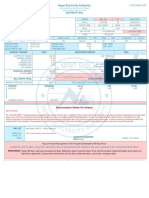

- Nepal Electricity Authority: Div: S & D ParsaDocument1 pageNepal Electricity Authority: Div: S & D ParsaMd Abul Bashar SumonNo ratings yet

- 4001 4607Document1,214 pages4001 4607DrPraveen Kumar TyagiNo ratings yet

- CV - Laroza, Philip Dan Jayson M.Document1 pageCV - Laroza, Philip Dan Jayson M.Philip LarozaNo ratings yet

- Internal Assignment (April 2022 Examination) Financial Accounting and AnalysisDocument6 pagesInternal Assignment (April 2022 Examination) Financial Accounting and AnalysisNageshwar SinghNo ratings yet

- SOP Procedure NarrativesDocument9 pagesSOP Procedure NarrativesPeter MulilaNo ratings yet

- Distribution Waterfall 5 ExamplesDocument14 pagesDistribution Waterfall 5 ExamplesChristian Leon PalominoNo ratings yet

- CLC Customer Info Update Form v3Document1 pageCLC Customer Info Update Form v3John Philip Repol LoberianoNo ratings yet

- C GTQ W4 N Pyvg PFedhDocument2 pagesC GTQ W4 N Pyvg PFedhAbhinav VermaNo ratings yet

- Pioma Plastics Company Cash Flow Statement For The Year Ended July 31 Amount in Rs. Amount in Rs. Cash Flow From Operating ActivitiesDocument4 pagesPioma Plastics Company Cash Flow Statement For The Year Ended July 31 Amount in Rs. Amount in Rs. Cash Flow From Operating ActivitiesPrajwal PaiNo ratings yet

- Aavas FinanciersDocument8 pagesAavas FinanciersSirish GopalanNo ratings yet

- Audit of Cash and Cash Equivalents - Set BDocument5 pagesAudit of Cash and Cash Equivalents - Set BZyrah Mae SaezNo ratings yet

- Multiple Choices QuestionsDocument7 pagesMultiple Choices QuestionsrenoNo ratings yet

- SBI Rin Raksha BroucherDocument8 pagesSBI Rin Raksha BroucherCharan BochkerNo ratings yet

- Account Statement From 1 Aug 2021 To 13 Nov 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument6 pagesAccount Statement From 1 Aug 2021 To 13 Nov 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancemadhusudhan reddyNo ratings yet

- ZOMATO Sec Comp 26052022222835Document4 pagesZOMATO Sec Comp 26052022222835bimacag338No ratings yet

- B Com Semester 6 Auditing and Assurance Multiple Choice QuestionsDocument113 pagesB Com Semester 6 Auditing and Assurance Multiple Choice QuestionsBhavesh DhandeNo ratings yet

- Ca Inter Audit Paper July - 2021 Paper Review by CA Kapil GoyalDocument13 pagesCa Inter Audit Paper July - 2021 Paper Review by CA Kapil GoyalEdwin MartinNo ratings yet

- Solved Simon Graduated From Lessard University Last Year He Financed HDocument1 pageSolved Simon Graduated From Lessard University Last Year He Financed HAnbu jaromiaNo ratings yet

- LOPEZ, ELLA MARIE - QUIZ 2 FinAnaRepDocument4 pagesLOPEZ, ELLA MARIE - QUIZ 2 FinAnaRepElla Marie LopezNo ratings yet

- Life Insurance Corporation of India PDFDocument6 pagesLife Insurance Corporation of India PDFAxe ExaNo ratings yet