You might also like

- Purchase OrderDocument6 pagesPurchase OrderMANGAL MUNSHINo ratings yet

- Pbe Form 1Document3 pagesPbe Form 1sam yadavNo ratings yet

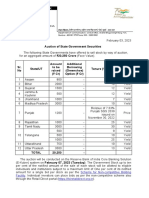

- Auction of State Government Securities 10,930 Cr. (Face Value)Document2 pagesAuction of State Government Securities 10,930 Cr. (Face Value)A-Series OfficialNo ratings yet

- Update On State Government Borrowings-18 Aug20Document3 pagesUpdate On State Government Borrowings-18 Aug20Santosh HiredesaiNo ratings yet

- Karnataka Forest DepartmentDocument1 pageKarnataka Forest DepartmentVinayaka GombiNo ratings yet

- Igst Rules, 2017Document8 pagesIgst Rules, 2017Royal GoyalNo ratings yet

- Ayurvedic MedicineDocument29 pagesAyurvedic Medicineakki_6551No ratings yet

- NABH Fee Structure For All ProgramsDocument4 pagesNABH Fee Structure For All ProgramsJayakrishnan TjNo ratings yet

- Requ Equest For Proposal For: Nodal AgencyDocument136 pagesRequ Equest For Proposal For: Nodal Agencynikitasha DNo ratings yet

- Approved Sixth Pay Commission Arrears CalculatorDocument16 pagesApproved Sixth Pay Commission Arrears CalculatorSaurabh SinghNo ratings yet

- Brief-River View SouthDocument1 pageBrief-River View SouthAL-HUSSAIN PROPERTIESNo ratings yet

- Course DetailsDocument2 pagesCourse Detailsbharat paliwalNo ratings yet

- PRC-2018 Proposals - STU T.SDocument34 pagesPRC-2018 Proposals - STU T.SNagaraju DanamNo ratings yet

- Order Date Order No Student NameDocument23 pagesOrder Date Order No Student NameDhiraj Singh JadonNo ratings yet

- Faqs LPG Part 4Document4 pagesFaqs LPG Part 4DeepakNo ratings yet

- Downloaded File 3Document10 pagesDownloaded File 3HemantSharmaNo ratings yet

- Gaur City Center Kiosk Price List W.E.F. 01.02.2020Document1 pageGaur City Center Kiosk Price List W.E.F. 01.02.2020neh SinghNo ratings yet

- Approved Sixth Pay Commission Arrears CalculatorDocument3 pagesApproved Sixth Pay Commission Arrears Calculatorsahil101263100% (91)

- Special Release: Philippine Statistics AuthorityDocument7 pagesSpecial Release: Philippine Statistics AuthorityYumie YamazukiNo ratings yet

- BCB F002 - Fee Structure - MSDocument4 pagesBCB F002 - Fee Structure - MSAhammad Niyas kNo ratings yet

- In The Books of ATITHI: Name PRN No. Division BatchDocument10 pagesIn The Books of ATITHI: Name PRN No. Division BatchAnanya ChoudharyNo ratings yet

- CashVoucher PODocument1 pageCashVoucher POomjanNo ratings yet

- UN DSA Circular 082016Document55 pagesUN DSA Circular 082016Mahalmadane Toure0% (1)

- HSS 21-22Document785 pagesHSS 21-22aparna tiwariNo ratings yet

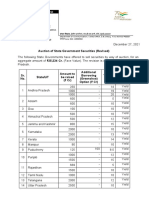

- Update On State Government Borrowings - 25 August 2020Document3 pagesUpdate On State Government Borrowings - 25 August 2020aniket guptaNo ratings yet

- LDCEIP NotificationDocument5 pagesLDCEIP NotificationHridyesh KumarNo ratings yet

- Utilization Certificate - 2019Document2 pagesUtilization Certificate - 2019venkateshNo ratings yet

- Course Registration Form: Sayyedha Sidrah Nisar Muhammad Nisar KhanDocument2 pagesCourse Registration Form: Sayyedha Sidrah Nisar Muhammad Nisar KhanAli SyedNo ratings yet

- Gha 2018 2019 School Fees Structure PDFDocument2 pagesGha 2018 2019 School Fees Structure PDFGilbert KamanziNo ratings yet

- Special Release: Philippine Statistics AuthorityDocument8 pagesSpecial Release: Philippine Statistics AuthorityYumie YamazukiNo ratings yet

- PR1667ASGDocument2 pagesPR1667ASGBhupinder PawarNo ratings yet

- Cliffton Valley Price ListDocument2 pagesCliffton Valley Price Listsishir mandalNo ratings yet

- Project Report On Poultry Farming BHOG PURDocument29 pagesProject Report On Poultry Farming BHOG PURpj singhNo ratings yet

- Total Total Total: (In Block Letters) (In Block Letters) (In Block Letters)Document1 pageTotal Total Total: (In Block Letters) (In Block Letters) (In Block Letters)Adnan BashirNo ratings yet

- UpdateDocument3 pagesUpdateheenaNo ratings yet

- Pakistan Medical Commission Pakistan Medical Commission Pakistan Medical CommissionDocument1 pagePakistan Medical Commission Pakistan Medical Commission Pakistan Medical CommissionZahira RushanNo ratings yet

- Nit 735Document13 pagesNit 735Raju BNo ratings yet

- Special Release Carabao Situation ReportDocument7 pagesSpecial Release Carabao Situation ReportYumie YamazukiNo ratings yet

- Uppsc2017 PDFDocument13 pagesUppsc2017 PDFRekhaSharmaNo ratings yet

- Mr. AnandDocument1 pageMr. AnandAnand shrivastavaNo ratings yet

- Action Research Academic Performance of Kindergarten Pupils With Parents Involvements of Tandag Central Elementry School (Tandag City Division)Document8 pagesAction Research Academic Performance of Kindergarten Pupils With Parents Involvements of Tandag Central Elementry School (Tandag City Division)KLeb VillalozNo ratings yet

- Account Slip 0134041 PSDocument3 pagesAccount Slip 0134041 PSSourav KartikNo ratings yet

- JunaidDocument34 pagesJunaidMOHAN ChandNo ratings yet

- New AI Based Vegetable Price/arrival/demand Forecasting Model & A Superior Vegetable Trading Business in IndiaDocument16 pagesNew AI Based Vegetable Price/arrival/demand Forecasting Model & A Superior Vegetable Trading Business in IndiaDumitru MihaiNo ratings yet

- A Case Study On The Food Tech Start-Up in IndiaDocument8 pagesA Case Study On The Food Tech Start-Up in IndiaLaxman nadigNo ratings yet

- Demand Analysis: E. Sales ForecastDocument8 pagesDemand Analysis: E. Sales Forecastanon_478172718No ratings yet

- Demand Analysis: E. Sales ForecastDocument8 pagesDemand Analysis: E. Sales Forecastanon_478172718No ratings yet

- Rich and Ppor Dad BookDocument1 pageRich and Ppor Dad BookŤŕī ŚhāñNo ratings yet

- Sky City FeesDocument2 pagesSky City Feesthatomokoma347No ratings yet

- Dprpackage Sheep & GoatDocument29 pagesDprpackage Sheep & Goatakki_6551No ratings yet

- P&A Briefing - Income Tax Rates 2080-2081 (2023-2024 A.D.) 20.07.23Document10 pagesP&A Briefing - Income Tax Rates 2080-2081 (2023-2024 A.D.) 20.07.23alpha NEPALNo ratings yet

- Kerala - Media RatesDocument20 pagesKerala - Media RatesVinod VaiyapuriNo ratings yet

- Apeamcet-2020 Admissions (M.P.C Stream) : Payment of Processing FeeDocument4 pagesApeamcet-2020 Admissions (M.P.C Stream) : Payment of Processing FeeSai NeerajNo ratings yet

- A Project of KIPS Preparations (PVT) LTD A Project of KIPS Preparations (PVT) LTD A Project of KIPS Preparations (PVT) LTDDocument1 pageA Project of KIPS Preparations (PVT) LTD A Project of KIPS Preparations (PVT) LTD A Project of KIPS Preparations (PVT) LTDTalha AwanNo ratings yet

- Jawaban Contoh Soal PA 2Document8 pagesJawaban Contoh Soal PA 2Radinne Fakhri Al WafaNo ratings yet

- Habib Bank Limited Habib Bank Limited Habib Bank Limited Habib Bank LimitedDocument1 pageHabib Bank Limited Habib Bank Limited Habib Bank Limited Habib Bank LimitedZamir HussainNo ratings yet

- Form Isian Untuk FKTPDocument4 pagesForm Isian Untuk FKTPririn safithriNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific-Seventh EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific-Seventh EditionNo ratings yet

- Vibes of Indian Economy-II: Focus on evolving economic Issues of RajasthanFrom EverandVibes of Indian Economy-II: Focus on evolving economic Issues of RajasthanNo ratings yet

- The Enabling Environment for Disaster Risk Financing in Pakistan: Country Diagnostics AssessmentFrom EverandThe Enabling Environment for Disaster Risk Financing in Pakistan: Country Diagnostics AssessmentNo ratings yet

- Aid for Trade in Asia and the Pacific: Promoting Connectivity for Inclusive DevelopmentFrom EverandAid for Trade in Asia and the Pacific: Promoting Connectivity for Inclusive DevelopmentNo ratings yet

- Regional Well-Being Across Kazakhstan: Harnessing Survey Data for Inclusive DevelopmentFrom EverandRegional Well-Being Across Kazakhstan: Harnessing Survey Data for Inclusive DevelopmentNo ratings yet

- Advanced Auditing and Professional Ethics-3 QDocument16 pagesAdvanced Auditing and Professional Ethics-3 QCAtestseriesNo ratings yet

- Companies Act 2013 Chapter 4Document14 pagesCompanies Act 2013 Chapter 4CAtestseriesNo ratings yet

- Advanced Auditing and Professional Ethics - QDocument16 pagesAdvanced Auditing and Professional Ethics - QCAtestseriesNo ratings yet

- Companies Act 2013 Chapter 6Document14 pagesCompanies Act 2013 Chapter 6CAtestseriesNo ratings yet

- Companies Act 2013 Chapter 8Document11 pagesCompanies Act 2013 Chapter 8CAtestseriesNo ratings yet

- Companies Act 2013 Chapter 1Document13 pagesCompanies Act 2013 Chapter 1CAtestseriesNo ratings yet

- Final New Indirect Tax Laws Test 1 Detailed May Solution 1617180196Document10 pagesFinal New Indirect Tax Laws Test 1 Detailed May Solution 1617180196CAtestseriesNo ratings yet

- Final New Indirect Tax Laws Test 4 Test 1617180304Document7 pagesFinal New Indirect Tax Laws Test 4 Test 1617180304CAtestseriesNo ratings yet

- Corporate and Economic Laws Test 3 May Solution 1609311077Document11 pagesCorporate and Economic Laws Test 3 May Solution 1609311077CAtestseriesNo ratings yet

- The 47th Meeting of GST Council Was Held at Chandigarh On 28thDocument27 pagesThe 47th Meeting of GST Council Was Held at Chandigarh On 28thAjit GuptaNo ratings yet

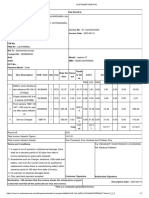

- InvoiceDocument1 pageInvoiceShabbir BurhanpurwalaNo ratings yet

- Sage UBS v9.9.3.9H1 1 Release NotesDocument80 pagesSage UBS v9.9.3.9H1 1 Release NotesSyah MuhammadNo ratings yet

- Pe Resin Price As On 01 Feb 2021Document93 pagesPe Resin Price As On 01 Feb 2021Akshat JainNo ratings yet

- Time of Supply-20Document44 pagesTime of Supply-20Sidhant GoyalNo ratings yet

- Bill 15Document1 pageBill 15jay_p_shahNo ratings yet

- Guru Nanak International Public School: Conomics Project OnDocument42 pagesGuru Nanak International Public School: Conomics Project OnRohit NagarNo ratings yet

- Day 6 & 7Document23 pagesDay 6 & 7PrasanthNo ratings yet

- Sri ByraveshwaraDocument3 pagesSri Byraveshwarahemanth1234No ratings yet

- 19e0i0078974Document1 page19e0i0078974subalbeuraNo ratings yet

- The Impact of GST On IndiaDocument8 pagesThe Impact of GST On Indiasahil khanNo ratings yet

- Invoice Home TownDocument1 pageInvoice Home TownRajan KumarNo ratings yet

- Nabin SharmaDocument4 pagesNabin SharmaAfsar AbdulNo ratings yet

- All About GST REFUNDS - Refrence ManualDocument451 pagesAll About GST REFUNDS - Refrence ManualSwarnadevi GanesanNo ratings yet

- Daikin VRV SheetDocument6 pagesDaikin VRV SheetSridhar ReddyNo ratings yet

- Challlan XT BillDocument1 pageChalllan XT BillbuntyphotoelectronicsNo ratings yet

- Books Bill 2Document1 pageBooks Bill 2asics leedsNo ratings yet

- 121 NEW Sales RegisterDocument24 pages121 NEW Sales RegistersowdrishivaNo ratings yet

- Ref - No. 9861606-14040852-3: Bharroth Raj KumarDocument4 pagesRef - No. 9861606-14040852-3: Bharroth Raj KumarRajkumarNo ratings yet

- Mahaveer Enterprises: Tax InvoiceDocument1 pageMahaveer Enterprises: Tax InvoiceAyush SrivastavNo ratings yet

- GST - ITC Rule 42, 43Document22 pagesGST - ITC Rule 42, 43Sanjay DwivediNo ratings yet

- Car InsuranceDocument14 pagesCar InsurancesheikNo ratings yet

- PF InvoiceDocument1 pagePF InvoiceALOKE GANGULYNo ratings yet

- Cellsons Appeal StatementDocument45 pagesCellsons Appeal Statementjenniferthanu1521No ratings yet

- Bottom CoverDocument11 pagesBottom CoverSSE BOGIE STORESNo ratings yet

- Acronyms: RLWL: Remote Location Waitlist PQWL: Pooled Quota Waitlist RSWL: Road-Side WaitlistDocument1 pageAcronyms: RLWL: Remote Location Waitlist PQWL: Pooled Quota Waitlist RSWL: Road-Side WaitlistAdinarayana RaoNo ratings yet

- Wa0014.Document15 pagesWa0014.No nameNo ratings yet

- Rajkumar TicketDocument3 pagesRajkumar TicketRaju PatelNo ratings yet