You might also like

- Lesson 10Document19 pagesLesson 10visiontanzania2022No ratings yet

- Value Added Tax-1Document9 pagesValue Added Tax-1IreneNo ratings yet

- Value Added Tax - VatDocument37 pagesValue Added Tax - VatTimoth MbwiloNo ratings yet

- Value Added TaxDocument17 pagesValue Added TaxkirigofortunateNo ratings yet

- HANDOUT FOR VAT-NewDocument25 pagesHANDOUT FOR VAT-NewCristian RenatusNo ratings yet

- 1.1. Problems On VAT (With Answers and Solutions)Document29 pages1.1. Problems On VAT (With Answers and Solutions)Jem Valmonte92% (25)

- Value Added Taxes Part 1 ExplainedDocument75 pagesValue Added Taxes Part 1 ExplainedLEILALYN NICOLAS100% (1)

- A Value Added TaxDocument6 pagesA Value Added TaxReeta SinghNo ratings yet

- Pdfcoffee Problems On VatDocument30 pagesPdfcoffee Problems On VatJunmar AMITNo ratings yet

- Value Added TaxDocument9 pagesValue Added TaxĴõ ĔĺNo ratings yet

- VAT CALCULATIONDocument14 pagesVAT CALCULATIONJishu Twaddler D'CruxNo ratings yet

- Service TaxDocument10 pagesService TaxMonika GuptaNo ratings yet

- VAT GuideZRADocument56 pagesVAT GuideZRADaniel Glen-WilliamsonNo ratings yet

- Introduction To VATDocument25 pagesIntroduction To VATIshmael OneyaNo ratings yet

- The Value Added Tax On SalesDocument7 pagesThe Value Added Tax On SalesShen Mani PadillaNo ratings yet

- Transfer Tax NotesDocument3 pagesTransfer Tax NotesCamille SalvadorNo ratings yet

- Chap-Vat 29Document4 pagesChap-Vat 29Tanya TandonNo ratings yet

- Chapter 5 Vat Concepts and General PrinciplesDocument18 pagesChapter 5 Vat Concepts and General Principlessalonid17No ratings yet

- Value Added Tax Get The MaxDocument23 pagesValue Added Tax Get The MaxSubhash SahuNo ratings yet

- VatDocument50 pagesVatnikolaevnavalentinaNo ratings yet

- Baf 306 Baf 3 - Introduction Vat Notes 1Document16 pagesBaf 306 Baf 3 - Introduction Vat Notes 1yudamwambafula30No ratings yet

- Value Added TaxDocument11 pagesValue Added TaxPreethi RajasekaranNo ratings yet

- VAT ArticleDocument4 pagesVAT ArticleSachi SrivastavaNo ratings yet

- IAS 12 TaxationDocument30 pagesIAS 12 Taxationwakemeup143No ratings yet

- Quiz - Business TaxesDocument4 pagesQuiz - Business TaxesFery Ann C. BravoNo ratings yet

- V A TDocument64 pagesV A TJennifer Garcia EreseNo ratings yet

- Chapter 19 & 20Document23 pagesChapter 19 & 20Kershey Salac100% (6)

- TAXATION 2 Chapter 10 Value Added TaxDocument7 pagesTAXATION 2 Chapter 10 Value Added TaxKim Cristian MaañoNo ratings yet

- Vat Training ModuleDocument59 pagesVat Training Modulebandajobanda100% (3)

- Introduction to Consumption TaxesDocument5 pagesIntroduction to Consumption TaxesHazel Jane EsclamadaNo ratings yet

- Tax 2 - BanggawanDocument175 pagesTax 2 - BanggawanJessica IslaNo ratings yet

- Value Added Tax (VAT) : A Presentation by Sanjay JagarwalDocument39 pagesValue Added Tax (VAT) : A Presentation by Sanjay JagarwalJishu Twaddler D'CruxNo ratings yet

- Business EnvironmentDocument12 pagesBusiness EnvironmentArpit JainNo ratings yet

- Introduction To Consumption Tax PDFDocument20 pagesIntroduction To Consumption Tax PDFShamae Duma-anNo ratings yet

- SlidesCh07show PpsDocument12 pagesSlidesCh07show PpsKhaja ZakiuddinNo ratings yet

- UP Nepal Tax FeeDocument7 pagesUP Nepal Tax FeeAnil ShahNo ratings yet

- Tax - Vat GuidenotesDocument13 pagesTax - Vat GuidenotesNardz AndananNo ratings yet

- Chapter 1 ConsumptionDocument41 pagesChapter 1 ConsumptionBeatrix Domingo SampangNo ratings yet

- Chapter 1 Introduction To Consumption TaxesDocument6 pagesChapter 1 Introduction To Consumption TaxesJason MablesNo ratings yet

- Project Report on Comparative Study of CENVAT V/S M-VATDocument53 pagesProject Report on Comparative Study of CENVAT V/S M-VATrani26oct100% (4)

- 3..sales Tax ProvisionsDocument82 pages3..sales Tax ProvisionsUmair GOLDNo ratings yet

- Introduction to Value Added Tax in MaharashtraDocument38 pagesIntroduction to Value Added Tax in MaharashtraKavita NadarNo ratings yet

- Chapter 1 Introduction To Consumption TaxesDocument21 pagesChapter 1 Introduction To Consumption TaxesNacpil, Alyssa JesseNo ratings yet

- VAT Guide 2023Document46 pagesVAT Guide 2023ELIJAHNo ratings yet

- M3 Excise Tax Students Copy Revised PDFDocument73 pagesM3 Excise Tax Students Copy Revised PDFTokis SabaNo ratings yet

- Introduction To Business TaxDocument7 pagesIntroduction To Business TaxDrew BanlutaNo ratings yet

- Indian Tax SystemDocument18 pagesIndian Tax SystemMahakNo ratings yet

- I. Introduction To Consumption TaxesDocument18 pagesI. Introduction To Consumption TaxescarlaNo ratings yet

- CH11 - Value Added TaxDocument33 pagesCH11 - Value Added TaxDimple AtienzaNo ratings yet

- Red Is The Color at The End of The Spectrum of Visible Light Next To Orange and Opposite VioletDocument11 pagesRed Is The Color at The End of The Spectrum of Visible Light Next To Orange and Opposite VioletLaqshman KumarNo ratings yet

- Draft VAT FAQDocument17 pagesDraft VAT FAQreazvat786No ratings yet

- Value Added Tax (VAT) : A Project OnDocument24 pagesValue Added Tax (VAT) : A Project OnSourabh SinghNo ratings yet

- Value Added Tax ActDocument18 pagesValue Added Tax ActStephen Amobi OkoronkwoNo ratings yet

- VAT FEATURESDocument3 pagesVAT FEATURESSiva Subramanian100% (2)

- Vat 1Document77 pagesVat 1Shajid HassanNo ratings yet

- Notes On VATDocument15 pagesNotes On VATErnest Benz Sabella DavilaNo ratings yet

- Very Awkward Tax: A bite-size guide to VAT for small businessFrom EverandVery Awkward Tax: A bite-size guide to VAT for small businessNo ratings yet

- Bir Ruling Da 381-04Document9 pagesBir Ruling Da 381-04vhbautistaNo ratings yet

- MerchandisingDocument7 pagesMerchandisingPearl AudeNo ratings yet

- Tolentino Vs Sec of Finance DigestDocument1 pageTolentino Vs Sec of Finance Digestheymissruby100% (1)

- World Bank Participants' ProfilesDocument50 pagesWorld Bank Participants' ProfilesJigisha VasaNo ratings yet

- DevMeth RRLDocument16 pagesDevMeth RRLacc_num2No ratings yet

- Fichier GRP 93 2Document164 pagesFichier GRP 93 2Judicial Watch, Inc.No ratings yet

- Your PLDT Statement for OctoberDocument6 pagesYour PLDT Statement for OctoberAkosi RizNo ratings yet

- 1 - Lmi CHPDocument162 pages1 - Lmi CHPAnonymous 9kzuGaYNo ratings yet

- GST DK Goel Practical QsDocument8 pagesGST DK Goel Practical QsAranya HaldarNo ratings yet

- VAT Concept MapDocument9 pagesVAT Concept MapMuadz HassanNo ratings yet

- Republic of The Philippines Court of Tax Appeals Quezon City First DivisionDocument79 pagesRepublic of The Philippines Court of Tax Appeals Quezon City First DivisionYna YnaNo ratings yet

- Functions and Rules of The Procurement CommitteeDocument14 pagesFunctions and Rules of The Procurement CommitteeEngr.Iqbal BaigNo ratings yet

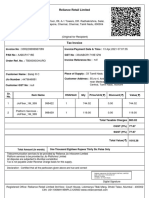

- Reliance Retail Limited: Total Amount (In Words) One Thousand Eighteen Rupees Thirty Six Paisa OnlyDocument3 pagesReliance Retail Limited: Total Amount (In Words) One Thousand Eighteen Rupees Thirty Six Paisa OnlyBalaNo ratings yet

- Reliance Industries in ChinaDocument24 pagesReliance Industries in ChinaSanddeepTirukoveleNo ratings yet

- How To Start and Run A Successful Cleaning BusinessDocument193 pagesHow To Start and Run A Successful Cleaning Businessblueman900100% (4)

- Tax Workbook 2022 - NodrmDocument399 pagesTax Workbook 2022 - NodrmNosipho Nyathi100% (2)

- EBS 122 Cum RCD FinanceDocument106 pagesEBS 122 Cum RCD FinanceMd MuzaffarNo ratings yet

- Tybcom Notes On GSTDocument9 pagesTybcom Notes On GSTJIYA DOSHI100% (1)

- Economics and Market Structure of StarbucksDocument9 pagesEconomics and Market Structure of StarbucksZakiah Abu KasimNo ratings yet

- Term PaperDocument4 pagesTerm PaperMarzuq Hussain100% (2)

- CSR 16-17 AmtDocument283 pagesCSR 16-17 AmtgauravNo ratings yet

- GST Study On Real Estate and Works ContractDocument22 pagesGST Study On Real Estate and Works ContractLGopal ShahNo ratings yet

- Tally - ERP 9 Advance Video ContentsDocument6 pagesTally - ERP 9 Advance Video ContentsAjay MaheshwariNo ratings yet

- Tendernotice - 1 - 2020-09-24T142931.718Document18 pagesTendernotice - 1 - 2020-09-24T142931.718SriChandraNo ratings yet

- Purchase Order: Order No.: RFQ No.: Fpso AboDocument2 pagesPurchase Order: Order No.: RFQ No.: Fpso AboDiri, Dienye Hez.No ratings yet

- Palil10PhD PDFDocument457 pagesPalil10PhD PDFMarsel wijayaNo ratings yet

- Big Ed's Whitegoods LTD: Part ADocument20 pagesBig Ed's Whitegoods LTD: Part AAnu SarochNo ratings yet

- Pranay - Darne Final Internship ReportDocument30 pagesPranay - Darne Final Internship ReportDhruv KumarNo ratings yet

- JHJKHDocument1 pageJHJKHJitesh SharmaNo ratings yet

- Profit and Loss Statement TemplateDocument2 pagesProfit and Loss Statement TemplateAlisa VisanNo ratings yet