You might also like

- RadNet Investor PresentationDocument23 pagesRadNet Investor PresentationtheredcornerNo ratings yet

- Making Foreign Direct Investment Work for Sub-Saharan AfricaFrom EverandMaking Foreign Direct Investment Work for Sub-Saharan AfricaNo ratings yet

- 205 FinalDocument42 pages205 FinalAustin BijuNo ratings yet

- FalconDocument11 pagesFalconNikhilNo ratings yet

- Performance: Numerai's Relative Performance (Net of Costs and Fees)Document5 pagesPerformance: Numerai's Relative Performance (Net of Costs and Fees)Jagdeep MaviNo ratings yet

- PUMD Initial Report 11.11.2010Document26 pagesPUMD Initial Report 11.11.2010Ana BozovicNo ratings yet

- Axis Global Innovation FoF NFO LeafletDocument2 pagesAxis Global Innovation FoF NFO LeafletKamalnath SinghNo ratings yet

- SPDR S&P Midcap 400 ETF Trust: Fund Inception Date Cusip Key Features About This BenchmarkDocument2 pagesSPDR S&P Midcap 400 ETF Trust: Fund Inception Date Cusip Key Features About This BenchmarkmuaadhNo ratings yet

- Reliq Health Technologies Inc (RHT - V) : Monitor This Stock: Explosive Growth AheadDocument17 pagesReliq Health Technologies Inc (RHT - V) : Monitor This Stock: Explosive Growth AheadNikhil GuptaNo ratings yet

- Genpact v2Document2 pagesGenpact v2Alan HsiehNo ratings yet

- IPO Vijaya Diagnostic - 01092021 1630476491Document6 pagesIPO Vijaya Diagnostic - 01092021 1630476491Neil MannikarNo ratings yet

- Ey Cafta CC 2022Document18 pagesEy Cafta CC 2022Aditisawhney collegeNo ratings yet

- SBI Focused Equity Fund (1) 09162022Document4 pagesSBI Focused Equity Fund (1) 09162022chandana kumarNo ratings yet

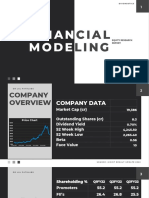

- Financial ModelingDocument40 pagesFinancial ModelingmetrotorNo ratings yet

- End Term Exam DCP 2021Document4 pagesEnd Term Exam DCP 2021PuneetNo ratings yet

- Wipro Investor PresentationDocument18 pagesWipro Investor PresentationursimmiNo ratings yet

- Nanox Investor Presentation - April 2021Document41 pagesNanox Investor Presentation - April 2021wuxichina geNo ratings yet

- RegTech Medici Top-21Document38 pagesRegTech Medici Top-21ShakespeareWallaNo ratings yet

- HowHealthtechisshapingtheindustry May2021Document6 pagesHowHealthtechisshapingtheindustry May2021Vansh AggarwalNo ratings yet

- Purolite Investor PresentationDocument17 pagesPurolite Investor PresentationQuốc Anh KhổngNo ratings yet

- Healthcare Technology Mailer v14Document4 pagesHealthcare Technology Mailer v14William HarrisNo ratings yet

- 2023-05-01-APH.N-TD Cowen-Model Update - PT To $70 From $75-101746375Document11 pages2023-05-01-APH.N-TD Cowen-Model Update - PT To $70 From $75-101746375Nikhil PadiaNo ratings yet

- 340B ProgramDocument68 pages340B Programapi-26219976No ratings yet

- Top Picks - 2022Document14 pagesTop Picks - 2022Bineet KumarNo ratings yet

- PWC PreSIP Diptimaya SarangiDocument15 pagesPWC PreSIP Diptimaya SarangiChandan KumarNo ratings yet

- Water Purifier PDFDocument10 pagesWater Purifier PDFSanyam JainNo ratings yet

- Reducing Length of Stay Using LeanDocument42 pagesReducing Length of Stay Using LeanAsiimwe D Pius100% (1)

- Ipg 2016 Investor Day PresentationDocument122 pagesIpg 2016 Investor Day PresentationyaacovNo ratings yet

- MTI Overview (August 2018) PDFDocument23 pagesMTI Overview (August 2018) PDFAnubhav TripathiNo ratings yet

- NTT DATA-SF CapabilitiesDocument26 pagesNTT DATA-SF CapabilitiesAjay KakadeNo ratings yet

- AAPL.O Apple Inc. Profile - ReutersDocument7 pagesAAPL.O Apple Inc. Profile - ReutersSheryl PajaNo ratings yet

- JP Morgan Presentation - 1-11-11 - FNLDocument26 pagesJP Morgan Presentation - 1-11-11 - FNLDhaval JobanputraNo ratings yet

- InteretrustDocument21 pagesInteretrustConstantin WellsNo ratings yet

- Equitas Small Finance Bank Company UpdateDocument10 pagesEquitas Small Finance Bank Company Updatefinal bossuNo ratings yet

- The Fortinet Security Fabric: Broad Integrated AutomatedDocument12 pagesThe Fortinet Security Fabric: Broad Integrated AutomatedMUMNo ratings yet

- LT Tech - 4qfy19 - HDFC SecDocument12 pagesLT Tech - 4qfy19 - HDFC SecdarshanmadeNo ratings yet

- September 2020Document41 pagesSeptember 2020Santiago J. GahnNo ratings yet

- Digital Enterprise MaturityDocument72 pagesDigital Enterprise MaturityTing wongNo ratings yet

- Infrastructure Is Driving India's Growth. Buckle Up.: Invest in L&T Infrastructure FundDocument2 pagesInfrastructure Is Driving India's Growth. Buckle Up.: Invest in L&T Infrastructure FundDeepak Singh PundirNo ratings yet

- Cjenm Ir Book 202005Document21 pagesCjenm Ir Book 202005backup tringuyenNo ratings yet

- Medplus IPO Note - VenturaDocument19 pagesMedplus IPO Note - Venturaaniket birariNo ratings yet

- HSBC Global TradeDocument35 pagesHSBC Global TradeRokesh NaiduNo ratings yet

- Radnet, Inc.: Financing An Acquisition: Rev. May 20, 2014Document22 pagesRadnet, Inc.: Financing An Acquisition: Rev. May 20, 2014Luisa FernandaNo ratings yet

- Percepatan Deteksi Awal Covid-19 Dengan Artificial Intelligent (AI) Bidang Radiologi PERSI - 01 Agustus 2020Document14 pagesPercepatan Deteksi Awal Covid-19 Dengan Artificial Intelligent (AI) Bidang Radiologi PERSI - 01 Agustus 2020Enggay OmdoNo ratings yet

- Media Chinese Int'l: Corporate HighlightsDocument4 pagesMedia Chinese Int'l: Corporate HighlightsRhb InvestNo ratings yet

- So-Young Innovating The Business Model in China FinalDocument19 pagesSo-Young Innovating The Business Model in China FinalTony LuNo ratings yet

- SVCA PEVC-backed IPOs Study and Industry CommentaryDocument13 pagesSVCA PEVC-backed IPOs Study and Industry CommentaryCarlos JesenaNo ratings yet

- McKinsey Capturing The Data and Analytics OpporunityDocument24 pagesMcKinsey Capturing The Data and Analytics OpporunityJonathan WenNo ratings yet

- Autonomy Pitch Book Qatalyst PDFDocument14 pagesAutonomy Pitch Book Qatalyst PDFRishabh Bansal100% (1)

- Ge HCInvestorDay 12022019Document75 pagesGe HCInvestorDay 12022019SRMPR CRMNo ratings yet

- Everest Group Engineering Services Top 50 2019Document7 pagesEverest Group Engineering Services Top 50 2019Ashish RanjanNo ratings yet

- Task 13: Industry Analysis - Financial Services Sector & Case StudiesDocument5 pagesTask 13: Industry Analysis - Financial Services Sector & Case StudiesVidhi SanchetiNo ratings yet

- Cjenm Ir Book 202008Document20 pagesCjenm Ir Book 202008backup tringuyenNo ratings yet

- QL Resources Berhad: Still A Solid Food Package - 25/05/2010Document3 pagesQL Resources Berhad: Still A Solid Food Package - 25/05/2010Rhb InvestNo ratings yet

- Alantra Software Valuation Update Q4 2020Document68 pagesAlantra Software Valuation Update Q4 2020Aniruddha RoyNo ratings yet

- Brochure - Teleradiology Market - Forecast To 2025Document32 pagesBrochure - Teleradiology Market - Forecast To 2025Purav PillaiNo ratings yet

- Cyient LTD - Pick of The Week - Axis Direct - 10022024 - 12!02!2024 - 12Document4 pagesCyient LTD - Pick of The Week - Axis Direct - 10022024 - 12!02!2024 - 12Sanjeedeep Mishra , 315No ratings yet

- Wipro Consumer Care Presentation June 2022Document25 pagesWipro Consumer Care Presentation June 2022Jasneet BaidNo ratings yet

- Infrastructure Is Driving India's Growth. Buckle Up.: Invest in L&T Infrastructure FundDocument2 pagesInfrastructure Is Driving India's Growth. Buckle Up.: Invest in L&T Infrastructure FundGaurangNo ratings yet

- Corporate Bylaws ofDocument10 pagesCorporate Bylaws ofJoebell VillanuevaNo ratings yet

- Associated Materials 2015 10KDocument115 pagesAssociated Materials 2015 10KAnonymous VHXCSbNo ratings yet

- Job Title: Supervisor - Regulatory Reporting Reports To: Lee Telo Department: Finance - Corporate Accounting Location: Pune, IndiaDocument2 pagesJob Title: Supervisor - Regulatory Reporting Reports To: Lee Telo Department: Finance - Corporate Accounting Location: Pune, IndiaPragya SinghNo ratings yet

- Chapter 1 Introduction To Business Research (NEW) .PPT (Autosaved)Document18 pagesChapter 1 Introduction To Business Research (NEW) .PPT (Autosaved)noor marliyahNo ratings yet

- Entrepreneurship Development Paper-GE - 202 Sem Ii - Bba: Unit 1 - IntroductionDocument10 pagesEntrepreneurship Development Paper-GE - 202 Sem Ii - Bba: Unit 1 - IntroductionUtkarsh PrasadNo ratings yet

- Lab 16 - ETAP IntroductionDocument3 pagesLab 16 - ETAP IntroductionOmar Fethi67% (3)

- Raja Metal Catalog October 2022-3Document32 pagesRaja Metal Catalog October 2022-3Tanvir Ahmed Khan0% (1)

- Course Outline For Managerial EconomicsDocument2 pagesCourse Outline For Managerial EconomicsZerihunNo ratings yet

- Complaint - Zajonc v. Electronic Arts (NDCA 2020)Document22 pagesComplaint - Zajonc v. Electronic Arts (NDCA 2020)Darius C. GambinoNo ratings yet

- DS II Optimization Self SolnsDocument68 pagesDS II Optimization Self SolnskeshavNo ratings yet

- Victoria V Inciong DigestDocument3 pagesVictoria V Inciong DigestXryn MortelNo ratings yet

- Wired 6.0 - Problem Statement - HRDocument3 pagesWired 6.0 - Problem Statement - HRKaram Singh Giani H21084No ratings yet

- Fee and Commission Split Agreement 2014 v2Document1 pageFee and Commission Split Agreement 2014 v2trolamc100% (2)

- Role of Auditors in Corporate GovernanceDocument9 pagesRole of Auditors in Corporate GovernanceDevansh SrivastavaNo ratings yet

- Fernando Andres Gimenez Futterknecht English CVDocument2 pagesFernando Andres Gimenez Futterknecht English CVFer GimenezNo ratings yet

- Hse Planning and AuditingDocument4 pagesHse Planning and AuditingCaron KarlosNo ratings yet

- Commissioner of St. Lukes CAse Digest TAxDocument1 pageCommissioner of St. Lukes CAse Digest TAxKayee KatNo ratings yet

- AWS-NAVSEA B2.1-8-308:2016 An American National StandardDocument11 pagesAWS-NAVSEA B2.1-8-308:2016 An American National StandardRemmy Torres VegaNo ratings yet

- Different Types of Customer Satisfaction MetricsDocument8 pagesDifferent Types of Customer Satisfaction MetricsKim Ericka BautistaNo ratings yet

- Greentech CGH Mesh 50x50x1.5Document1 pageGreentech CGH Mesh 50x50x1.5RANo ratings yet

- Service Learning: A Small Business Project: Bkam3023 Management Accounting Ii A192 Second Semester February 2019/2020Document4 pagesService Learning: A Small Business Project: Bkam3023 Management Accounting Ii A192 Second Semester February 2019/2020Irfan izhamNo ratings yet

- Poster About Food - Google SearchDocument4 pagesPoster About Food - Google SearchHudiefah YussufNo ratings yet

- Collection LetterDocument4 pagesCollection LetterKiran KumarNo ratings yet

- Case Study TPM Jet AirwaysDocument15 pagesCase Study TPM Jet AirwaysSanjay Domdiya100% (1)

- CRA01 Confirmation of Residential or Business Address For Online Completion External FormDocument2 pagesCRA01 Confirmation of Residential or Business Address For Online Completion External FormBrandon BothaNo ratings yet

- Railway Hand Book On Internal ChecksDocument308 pagesRailway Hand Book On Internal ChecksHiraBallabh82% (34)

- NU 3.1 PDIC ExerciseDocument12 pagesNU 3.1 PDIC ExerciseBack upNo ratings yet

- Strategic Management-Louis VuittonDocument4 pagesStrategic Management-Louis VuittonPhclivran67% (3)

- Alejandro Fernandez 2Document2 pagesAlejandro Fernandez 2afdez100No ratings yet

- PERSONAL FINANCE Lesson Two Money ManagementDocument6 pagesPERSONAL FINANCE Lesson Two Money ManagementJohn Greg MenianoNo ratings yet