You might also like

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Ca Inter GST Rajkumar Sir Abc AnalysisDocument5 pagesCa Inter GST Rajkumar Sir Abc AnalysisDhruv GolyanNo ratings yet

- CA Important Topics Nov 23Document5 pagesCA Important Topics Nov 23nehabhagat111204No ratings yet

- Valuing Services in Trade: A Toolkit for Competitiveness DiagnosticsFrom EverandValuing Services in Trade: A Toolkit for Competitiveness DiagnosticsNo ratings yet

- @CACell GST Super 60 Important Questions May23Document68 pages@CACell GST Super 60 Important Questions May23Hitesh AgaleNo ratings yet

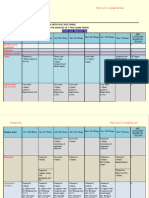

- ABC Analysis CA FinalDocument8 pagesABC Analysis CA FinalvenkatprashanthNo ratings yet

- Exemption Scoring 60 Questions CA CMA CS FINAL MAY NOV 2023Document100 pagesExemption Scoring 60 Questions CA CMA CS FINAL MAY NOV 2023Raghothama Achar RNo ratings yet

- Graduation Documents CompressedDocument7 pagesGraduation Documents CompressedSugandha JhaNo ratings yet

- Service MarketingDocument3 pagesService MarketingKishore Kumar MsvNo ratings yet

- Fakir Mohan Autonomous College, Balasore: Provisional Certificate Cum Grade SheetDocument1 pageFakir Mohan Autonomous College, Balasore: Provisional Certificate Cum Grade SheetAshesh ChandaNo ratings yet

- Finance of International Trade Related Treasury OperationsDocument2 pagesFinance of International Trade Related Treasury OperationsmuhammadNo ratings yet

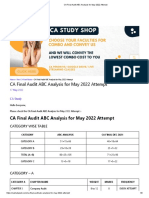

- CA Final Audit ABC Analysis For May 2022 Attempt PDFDocument3 pagesCA Final Audit ABC Analysis For May 2022 Attempt PDFetgerrhrhehNo ratings yet

- B.Tech. CSE PDFDocument8 pagesB.Tech. CSE PDFrajrskNo ratings yet

- KENDRIYA VIDYALAYA SANGATHAN CHENNAI REGION CLASS XI ECONOMICS SAMPLE PAPERDocument1 pageKENDRIYA VIDYALAYA SANGATHAN CHENNAI REGION CLASS XI ECONOMICS SAMPLE PAPERDj gokul jai kumar.vNo ratings yet

- Part-3 Lalit Narayan Mithila University, DarbhangaDocument1 pagePart-3 Lalit Narayan Mithila University, DarbhangaSuraj Kumar BarnwalNo ratings yet

- Emailing SPM PAST PAPER ANALYSIS W-22Document7 pagesEmailing SPM PAST PAPER ANALYSIS W-22Muhammad HamizNo ratings yet

- Concept Diagram - Figure of 8': Quality Kaizen Quality MaintenanceDocument41 pagesConcept Diagram - Figure of 8': Quality Kaizen Quality MaintenanceNARENDER SINGHNo ratings yet

- Screenshot 2023-10-19 at 6.02.55 PMDocument131 pagesScreenshot 2023-10-19 at 6.02.55 PMSunil MaharanaNo ratings yet

- MA Management Accounting Kế Toán Quản TrịDocument410 pagesMA Management Accounting Kế Toán Quản TrịVăn Mạnh100% (2)

- B. Com (CA) SyllabusDocument70 pagesB. Com (CA) SyllabusBhaskar ReddyNo ratings yet

- Vda QFDDocument20 pagesVda QFDlewjoy100% (1)

- ANOVA Step by StepDocument258 pagesANOVA Step by StepVinothNo ratings yet

- Cognitive Process Dimensions: Table of Specification Business Math (1st Quarter)Document2 pagesCognitive Process Dimensions: Table of Specification Business Math (1st Quarter)Marvin Caisip DiloyNo ratings yet

- Business CourseworkDocument36 pagesBusiness Courseworkosmansamsam16No ratings yet

- Q2 Summative Test Answer SheetDocument1 pageQ2 Summative Test Answer SheetJoelmarMondonedoNo ratings yet

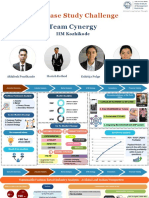

- PWC Case Study Challenge: Team CynergyDocument16 pagesPWC Case Study Challenge: Team CynergyDeepakbalajiNo ratings yet

- Cambridge Assessment International Education: Accounting 0452/21 October/November 2018Document17 pagesCambridge Assessment International Education: Accounting 0452/21 October/November 2018Iron OneNo ratings yet

- SBR Planner DraftDocument5 pagesSBR Planner DraftIleo AliNo ratings yet

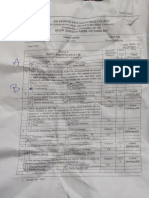

- VIDYA SAGAR ABC Analysis-CA Final Audit FOR DEC - 2021Document5 pagesVIDYA SAGAR ABC Analysis-CA Final Audit FOR DEC - 2021VANDANA GOYALNo ratings yet

- Supplier EvaluationDocument2 pagesSupplier EvaluationTouhidur RahmanNo ratings yet

- SunRice GuestLecture May08Document60 pagesSunRice GuestLecture May08Saket DhamiNo ratings yet

- Industrial Training ReportDocument15 pagesIndustrial Training ReportVishnu NairNo ratings yet

- C-Scheme) : Re-AppearDocument8 pagesC-Scheme) : Re-AppearANUJ MANGLANo ratings yet

- WB - Paper-17 CMA FINALDocument131 pagesWB - Paper-17 CMA FINALvijaykumartaxNo ratings yet

- SL Bus Man Exemplar 3 Marks and Comments 1Document1 pageSL Bus Man Exemplar 3 Marks and Comments 1api-505775092No ratings yet

- Eco Practice PaperDocument33 pagesEco Practice Paperom waghNo ratings yet

- VIDYA SAGAR Analysis-Accounts For Nov 2022Document3 pagesVIDYA SAGAR Analysis-Accounts For Nov 2022MH DESKNo ratings yet

- VIDYA SAGAR Analysis - Audit-1Document3 pagesVIDYA SAGAR Analysis - Audit-1Dharani SsNo ratings yet

- New CA Program Annual Study Planner 2022Document3 pagesNew CA Program Annual Study Planner 2022Dikshant SinghNo ratings yet

- GTU MBA Semester 2 POM Exam Winter 2018Document2 pagesGTU MBA Semester 2 POM Exam Winter 2018hunnyNo ratings yet

- CA24 Auditing and Assurance Pilot PaperDocument2 pagesCA24 Auditing and Assurance Pilot Papermoza salimNo ratings yet

- Rambaan CostDocument433 pagesRambaan CostSanjana SharmaNo ratings yet

- Accounting & Financial ManagementDocument2 pagesAccounting & Financial ManagementNitin VarmanNo ratings yet

- Full Download Ebook Ebook PDF Managerial Economics Applications Strategies and Tactics 14th Edition PDFDocument38 pagesFull Download Ebook Ebook PDF Managerial Economics Applications Strategies and Tactics 14th Edition PDFbryan.myers908100% (43)

- 3rd SEM PDFDocument1 page3rd SEM PDFAnamika VatsaNo ratings yet

- Semester Grade Report: School of LawDocument1 pageSemester Grade Report: School of LawAnamika VatsaNo ratings yet

- Min Marketimg: December 20119 MasterDocument18 pagesMin Marketimg: December 20119 MasterMysterious 16No ratings yet

- Nissan VP Discusses Supplier Collaboration StrategiesDocument26 pagesNissan VP Discusses Supplier Collaboration StrategiesRiselda Myshku KajaNo ratings yet

- XYZ Company Initial Supplier EvaluationDocument2 pagesXYZ Company Initial Supplier EvaluationDrinkwell AccountsNo ratings yet

- Evaluate and Find Which Company Will Be Selected Initially For Supplying MaterialsDocument2 pagesEvaluate and Find Which Company Will Be Selected Initially For Supplying MaterialsDrinkwell AccountsNo ratings yet

- BK1 - Sec 5 - MAF TutsDocument228 pagesBK1 - Sec 5 - MAF TutsBrightonNo ratings yet

- Ca Foundation Detailed Test Series 1644473581Document4 pagesCa Foundation Detailed Test Series 1644473581Shubham RajNo ratings yet

- CLB Support Kit 3Document104 pagesCLB Support Kit 3Melania AlmonteNo ratings yet

- SAP HR Indian PayrollDocument881 pagesSAP HR Indian PayrollSandeep MohapatraNo ratings yet

- All F7 (FR) Technical Articles: (Association of Chartered Certified Accountants)Document160 pagesAll F7 (FR) Technical Articles: (Association of Chartered Certified Accountants)feysal shurieNo ratings yet

- SP 2021 Q Paper Submitted - Milind AkarteDocument5 pagesSP 2021 Q Paper Submitted - Milind AkarteRamkumarArumugapandiNo ratings yet

- BSCPL INFRASTRUCTURE LTD KRA - QA / QCDocument46 pagesBSCPL INFRASTRUCTURE LTD KRA - QA / QCPalla Bhaskara Rao83% (6)

- CA Intermediate ABC Analysis and Marks Weightage Mentoring 1679573700Document6 pagesCA Intermediate ABC Analysis and Marks Weightage Mentoring 1679573700Anil ReddyNo ratings yet

- Paper20A Set2Document8 pagesPaper20A Set2Ramanpreet KaurNo ratings yet

- Comparison Among Languages: C. Cappa, J. Fernando, S. GiuliviDocument62 pagesComparison Among Languages: C. Cappa, J. Fernando, S. GiuliviSaoodNo ratings yet

- Peoria County Booking Sheet 11/02/13Document8 pagesPeoria County Booking Sheet 11/02/13Journal Star police documentsNo ratings yet

- اسئلة استرشادية صوتيات قسم الترجمةDocument6 pagesاسئلة استرشادية صوتيات قسم الترجمةMasarra GhaithNo ratings yet

- Persuasive EssayDocument4 pagesPersuasive Essayapi-338650494100% (7)

- March 17, 2019 CSE-PPT Professional List of Passers RO4Document67 pagesMarch 17, 2019 CSE-PPT Professional List of Passers RO4Faniefets SoliterogenNo ratings yet

- Affidavit of damage car accident documentsDocument58 pagesAffidavit of damage car accident documentsJm Borbon MartinezNo ratings yet

- I Twin Technology11 PDFDocument14 pagesI Twin Technology11 PDFChandhanNo ratings yet

- ILNAS-EN 17141:2020: Cleanrooms and Associated Controlled Environments - Biocontamination ControlDocument9 pagesILNAS-EN 17141:2020: Cleanrooms and Associated Controlled Environments - Biocontamination ControlBLUEPRINT Integrated Engineering Services0% (1)

- Weights and Measures 1Document11 pagesWeights and Measures 1Chuck Lizana100% (1)

- Bank Company ActDocument16 pagesBank Company Actmd nazirul islam100% (2)

- Who Was Charlie ChaplinDocument4 pagesWho Was Charlie ChaplinHugo Alonso Llanos CamposNo ratings yet

- Family DiversityDocument4 pagesFamily DiversityAlberto Salazar CarballoNo ratings yet

- Electrical Engineering Portal - Com Substation Fire ProtectionDocument4 pagesElectrical Engineering Portal - Com Substation Fire ProtectionJaeman ParkNo ratings yet

- WebpdfDocument343 pagesWebpdfRahma AbdullahiNo ratings yet

- Affidavit Waiver RightsDocument2 pagesAffidavit Waiver RightsMasa Lyn87% (47)

- CO2 Adsorption On Turkish CoalsDocument133 pagesCO2 Adsorption On Turkish CoalsMaria De La HozNo ratings yet

- Graduation SongsDocument1 pageGraduation SongsRonnie CastilloNo ratings yet

- RPC 2 Page 21 CasesDocument49 pagesRPC 2 Page 21 CasesCarlo Paul Castro SanaNo ratings yet

- Raft Sat1Document3 pagesRaft Sat1api-480681665No ratings yet

- Briefing The Yemen Conflict and CrisisDocument36 pagesBriefing The Yemen Conflict and CrisisFinlay AsherNo ratings yet

- Labor Law Module 5Document11 pagesLabor Law Module 5dennis delrosarioNo ratings yet

- North Carolina Cherokee IndiansDocument7 pagesNorth Carolina Cherokee IndiansLogan ShaddenNo ratings yet

- The Girl in Room 105 Is The Eighth Novel and The Tenth Book Overall Written by The Indian Author Chetan BhagatDocument3 pagesThe Girl in Room 105 Is The Eighth Novel and The Tenth Book Overall Written by The Indian Author Chetan BhagatSiddharrth Prem100% (1)

- Notification No.54/2021 - Customs (N.T.) : Schedule-IDocument3 pagesNotification No.54/2021 - Customs (N.T.) : Schedule-Ianil nayakanahattiNo ratings yet

- Us Bipoc Health Disparities 4.23.21Document22 pagesUs Bipoc Health Disparities 4.23.21Jennifer Maria PadronNo ratings yet

- Nobody Does It Better and Indian Hospitality Will Leave You Feeling Better Too.Document2 pagesNobody Does It Better and Indian Hospitality Will Leave You Feeling Better Too.Abhijeet UmatheNo ratings yet

- MandwaDocument4 pagesMandwaMadhu KumarNo ratings yet

- wcl-20-24 11 2023Document15 pageswcl-20-24 11 2023Codarren VelvindronNo ratings yet

- Communion With The Goddess Priestesses PDFDocument30 pagesCommunion With The Goddess Priestesses PDFAtmageet KaurNo ratings yet

- 3 Factors That Contribute To Gender Inequality in The ClassroomDocument3 pages3 Factors That Contribute To Gender Inequality in The ClassroomGemma LynNo ratings yet