You might also like

- CHASE PRIVATE CLIENT CHECKING Statement For Account Ending in 5229 DaDocument4 pagesCHASE PRIVATE CLIENT CHECKING Statement For Account Ending in 5229 Darocky fletcher100% (1)

- Akshay PatraDocument1 pageAkshay PatraTANAY PUROHITNo ratings yet

- Income Taxation Banggawan 2019 Ed Solution ManualDocument40 pagesIncome Taxation Banggawan 2019 Ed Solution ManualVanilla VanillaNo ratings yet

- Pffcu Auto Event March 18-27. Get Your Autodraft Today-Shop With Financing in Hand. Rates As Low As 2.24% Apr . Easy To Apply. Fast Loan Decisions. See The Shield For DetailsDocument5 pagesPffcu Auto Event March 18-27. Get Your Autodraft Today-Shop With Financing in Hand. Rates As Low As 2.24% Apr . Easy To Apply. Fast Loan Decisions. See The Shield For DetailsSimone TurnerNo ratings yet

- RR 13-2000Document4 pagesRR 13-2000doraemoan100% (1)

- RR 13-00Document2 pagesRR 13-00saintkarri100% (2)

- Tax Deduction at SourceDocument62 pagesTax Deduction at SourcePallavisweet100% (1)

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Shashank ReddyNo ratings yet

- Circular 5 2023Document5 pagesCircular 5 2023ravirulesvitNo ratings yet

- Frequently Asked Questions On Online GamingDocument1 pageFrequently Asked Questions On Online Gamingvelugulasuresh2No ratings yet

- Tax Deducted at SourceDocument29 pagesTax Deducted at SourceChaitany Joshi0% (2)

- Tds Rate Chart 13 14Document4 pagesTds Rate Chart 13 14rockyrrNo ratings yet

- Tax Deduction at SourceDocument5 pagesTax Deduction at SourceSarayu BhardwajNo ratings yet

- Indirect Tax Notes Tybaf Sem 6Document27 pagesIndirect Tax Notes Tybaf Sem 6Krutika sutar100% (1)

- Bhubaneswar 08112015 Session I PDFDocument42 pagesBhubaneswar 08112015 Session I PDFsachin NegiNo ratings yet

- Tax Deducted at SourceDocument29 pagesTax Deducted at SourceAmbar Pratik MishraNo ratings yet

- EY - Budget 2023 - Media and Entertainment SectorDocument6 pagesEY - Budget 2023 - Media and Entertainment SectorAditya BajoriaNo ratings yet

- 2015 PRACTICE NOTES 2 Withholding Tax17022015095605 PDFDocument18 pages2015 PRACTICE NOTES 2 Withholding Tax17022015095605 PDFtendaicrosby100% (1)

- Tax Deductable AtsourceDocument22 pagesTax Deductable AtsourceMohd. Shadab khanNo ratings yet

- 1035 Withholding TaxDocument8 pages1035 Withholding TaxViren GandhiNo ratings yet

- Taxability of Winnings From Games and LotteriesDocument2 pagesTaxability of Winnings From Games and LotteriesravirulesvitNo ratings yet

- Electronic Credit LedgerDocument2 pagesElectronic Credit LedgerAakshaNo ratings yet

- Online GamingDocument8 pagesOnline GamingayushimohagaonkarNo ratings yet

- 20238-2000-Implementing Section 34 B of The Tax Code Of20211213-11-1kbooi9Document5 pages20238-2000-Implementing Section 34 B of The Tax Code Of20211213-11-1kbooi9Ramos Claude VinzonNo ratings yet

- TDS DocumentDocument34 pagesTDS DocumentSaleem JavedNo ratings yet

- TDS Tax Deduction at Source: Prepared By: Visharad ShuklaDocument25 pagesTDS Tax Deduction at Source: Prepared By: Visharad ShuklaPriyanshi GandhiNo ratings yet

- BDO Income Tax Alert - October 2022Document8 pagesBDO Income Tax Alert - October 2022ThiruNo ratings yet

- Individual Heads of IncomeDocument5 pagesIndividual Heads of Incomeamitratha77No ratings yet

- TDS Rate Financial Year 13-14Document10 pagesTDS Rate Financial Year 13-14Heena AgreNo ratings yet

- Payment OF Taxes Under GST: Submitted By: Submitted ToDocument10 pagesPayment OF Taxes Under GST: Submitted By: Submitted Toakshit sharmaNo ratings yet

- Overview of GSTDocument83 pagesOverview of GSTPankaj MahantaNo ratings yet

- Taxation of Cryptocurrency 2022 Final Update 2022Document17 pagesTaxation of Cryptocurrency 2022 Final Update 2022aryan sarangNo ratings yet

- Tax ChangesDocument7 pagesTax ChangesSujan SanjayNo ratings yet

- Pay As You Earn PAYE Refunds 1Document2 pagesPay As You Earn PAYE Refunds 1bwalilubemba7No ratings yet

- Goods and Service Tax (GST)Document19 pagesGoods and Service Tax (GST)Saurabh Kumar SharmaNo ratings yet

- Income From Other SourcesDocument27 pagesIncome From Other Sourcesanilchavan100% (1)

- Ayush PendDocument62 pagesAyush PendPankaj MahantaNo ratings yet

- Income Tax, IndiaDocument11 pagesIncome Tax, Indiahimanshu_mathur88No ratings yet

- Income Tax in IndiaDocument19 pagesIncome Tax in IndiaConcepts TreeNo ratings yet

- LKS White Paper On Taxability of Online Gaming IncomeDocument28 pagesLKS White Paper On Taxability of Online Gaming IncomeSaurin ThakkarNo ratings yet

- TDS Under Sec 194A EtcDocument26 pagesTDS Under Sec 194A EtcDivyaNo ratings yet

- TDS TRS GST (2) 20211228151919Document38 pagesTDS TRS GST (2) 20211228151919Rishi PriyadarshiNo ratings yet

- All About Tax Deducted at Source (TDS) - Taxguru - inDocument11 pagesAll About Tax Deducted at Source (TDS) - Taxguru - inwaqtkeebaatein12No ratings yet

- What Is Tax Deducted at Source?Document5 pagesWhat Is Tax Deducted at Source?Bhagyashree SondagarNo ratings yet

- OL 4 - BLT Study Text Suppliment 2021 - On New Tax AmmendmentsDocument28 pagesOL 4 - BLT Study Text Suppliment 2021 - On New Tax Ammendmentshte19031No ratings yet

- JT GST Amendment Dec 2023 - 231226 - 175329Document7 pagesJT GST Amendment Dec 2023 - 231226 - 175329shahsakshi172002No ratings yet

- Advance Payment of TaxDocument3 pagesAdvance Payment of Taxinsathi50% (2)

- Tax Liab. of Ind.Document13 pagesTax Liab. of Ind.Arun SwamiNo ratings yet

- KoinX-Complete Tax Report - OptionsDocument13 pagesKoinX-Complete Tax Report - OptionsBhavsmeetforeverNo ratings yet

- GST Payments - GST Refund Online & OfflineDocument6 pagesGST Payments - GST Refund Online & Offlineajayprajapti828No ratings yet

- Tax Deducted at Source IMPORTANT POINTSDocument2 pagesTax Deducted at Source IMPORTANT POINTSnABSAMNNo ratings yet

- Tax Payment Under GSTDocument7 pagesTax Payment Under GSTAbhay GroverNo ratings yet

- Partnership TaxDocument24 pagesPartnership TaxMadurikaNo ratings yet

- What Is Tax Deducted at SourceDocument6 pagesWhat Is Tax Deducted at SourcejdonNo ratings yet

- Minimum Corporate Income Tax (MCIT), Improperly Accumulated Earnings Tax (IAET), and Gross Income Tax (GIT)Document57 pagesMinimum Corporate Income Tax (MCIT), Improperly Accumulated Earnings Tax (IAET), and Gross Income Tax (GIT)kyleramosNo ratings yet

- Wapda Taxmemo2013Document50 pagesWapda Taxmemo2013Naveed ShaheenNo ratings yet

- Tax Reckoner 2013-14: Snapshot of Tax Rates Specific To Mutual FundsDocument2 pagesTax Reckoner 2013-14: Snapshot of Tax Rates Specific To Mutual FundsZia Ur RehmanNo ratings yet

- New Tax ReformDocument4 pagesNew Tax ReformEDISON SAGUIRERNo ratings yet

- TDS & TCSDocument3 pagesTDS & TCSRajashree DasNo ratings yet

- Income Tax Questions and AnswersDocument9 pagesIncome Tax Questions and AnswersHeraldWilsonNo ratings yet

- 10-Practical Questions of Individuals (78-113)Document38 pages10-Practical Questions of Individuals (78-113)Sajid Saith0% (1)

- Republic Act No. 10963: Tax Reform For Acceleration and Inclusion (Train)Document24 pagesRepublic Act No. 10963: Tax Reform For Acceleration and Inclusion (Train)Johayra AbbasNo ratings yet

- When Should TDS Be Deducted and by Whom in IndiaDocument6 pagesWhen Should TDS Be Deducted and by Whom in Indiaaddishaikh1924No ratings yet

- Payment in Excess of Rs. 1,20,000/-Per Annum Payment in Excess of Rs. 1,20,000/ - Per AnnumDocument1 pagePayment in Excess of Rs. 1,20,000/-Per Annum Payment in Excess of Rs. 1,20,000/ - Per AnnumMadhan RajNo ratings yet

- Double Taxation Avoidance Agreement Final TaxDocument28 pagesDouble Taxation Avoidance Agreement Final TaxkhanafshaNo ratings yet

- Principles of Taxation Question Bank 2021Document243 pagesPrinciples of Taxation Question Bank 2021Khadeeza ShammeeNo ratings yet

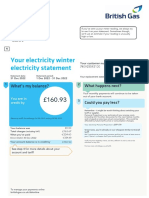

- Your Electricity Winter Electricity Statement: What's My Balance?Document1 pageYour Electricity Winter Electricity Statement: What's My Balance?Nikita TishchenkoNo ratings yet

- Dpjain16 1 23escortDocument1 pageDpjain16 1 23escortPrashant PawadeNo ratings yet

- Pagarbook Quotation - QuotationDocument1 pagePagarbook Quotation - Quotationmohitkashyap.mlzsNo ratings yet

- Sales Quote SQ 381Document1 pageSales Quote SQ 381sivakumarNo ratings yet

- Reception For Ted CruzDocument2 pagesReception For Ted CruzSunlight FoundationNo ratings yet

- BB0019-IncomeTax Valuation PerquisitesDocument314 pagesBB0019-IncomeTax Valuation PerquisitesMohammed Abu ObaidahNo ratings yet

- AP 001 A Proof of Cash LectureDocument6 pagesAP 001 A Proof of Cash LectureKaye MagbirayNo ratings yet

- 0760XXXXXXXXX834831 05 2023Document5 pages0760XXXXXXXXX834831 05 2023dabu choudharyNo ratings yet

- DT Amendments 2024 - CA Saumil Manglani - CS-CMA-CADocument34 pagesDT Amendments 2024 - CA Saumil Manglani - CS-CMA-CAHariniNo ratings yet

- InTax - Items - of - Gross - Income TAMAYAO - GARCIA RESADocument5 pagesInTax - Items - of - Gross - Income TAMAYAO - GARCIA RESAAbby NavarroNo ratings yet

- Earnest Money ReceiptDocument1 pageEarnest Money ReceiptDevanshu MarwahNo ratings yet

- Module 06 The Expenditure Cycle Payroll Processing ProceduresDocument8 pagesModule 06 The Expenditure Cycle Payroll Processing ProceduresRed Reyes100% (1)

- RJFRHXDocument3 pagesRJFRHXCandy ValentineNo ratings yet

- Chapter 3Document55 pagesChapter 3Ahmed hassanNo ratings yet

- Certificate of Registration For VAtDocument1 pageCertificate of Registration For VAtxbmachusNo ratings yet

- Project For Peachtree Accounting: Iii. Trial Balance As of August 31, 2001 Acct. No Account Description Debit CreditDocument8 pagesProject For Peachtree Accounting: Iii. Trial Balance As of August 31, 2001 Acct. No Account Description Debit CreditBeka Asra100% (2)

- Contract: Organisation Details Buyer DetailsDocument4 pagesContract: Organisation Details Buyer DetailsTender 247No ratings yet

- Products and Services Offered by PMC BankDocument7 pagesProducts and Services Offered by PMC BankVivek GusainNo ratings yet

- Handout 4Q Philippine Individual Income Tax Return Sample ProblemsDocument3 pagesHandout 4Q Philippine Individual Income Tax Return Sample ProblemsMaria Jennifer Intong SalazarNo ratings yet

- 28x VenmoDocument1 page28x Venmorckmvp6c8qNo ratings yet

- FAN Without PAN Violates Due ProcessDocument2 pagesFAN Without PAN Violates Due ProcessDesiree SencoNo ratings yet

- Tax Invoice: 41/2 B Diamond Harbour Road, Kolkata Gstin/Uin: 19AAHFM4577H1ZU State Name: West Bengal, Code: 19Document1 pageTax Invoice: 41/2 B Diamond Harbour Road, Kolkata Gstin/Uin: 19AAHFM4577H1ZU State Name: West Bengal, Code: 19Shubham ShawNo ratings yet

- Exam On Foreign Currency Transaction 40Document6 pagesExam On Foreign Currency Transaction 40nigusNo ratings yet